EBITDA Normalization in M&A: What to Adjust, What to Exclude, and Why It Matters

A practical guide to EBITDA normalization in M&A - what adjustments survive due diligence, how buyers evaluate them and why small changes can move your valuation significantly.

A $200K Adjustment Just Cost You $1.8 Million

You're selling your business. You've built it over a decade, and your advisor has put together a financial profile showing $3 million in adjusted EBITDA. Offers come in around 8x - roughly $24 million in enterprise value. Then a buyer's due diligence team runs their own analysis and concludes that $200,000 of your adjustments don't hold up. That $200K doesn't just disappear from EBITDA - it gets multiplied. At 8x, your enterprise value just dropped by $1.6 million. And if that haircut also makes the buyer nervous about the rest of your numbers, the multiple itself might compress from 8x to 7.5x, adding another $2.25 million in lost value.

That's how EBITDA normalization works in M&A. The number that survives financial due diligence - not the number in your CIM - is the one that gets multiplied to determine your company's enterprise value.

EBITDA normalization is the process of adjusting a company's reported earnings to reflect its true, sustainable, recurring profitability - stripping out one-time events, owner-specific costs, and accounting noise so that buyers can see what the business actually earns on a repeatable basis. In mid-market M&A, this normalized EBITDA is typically multiplied by a valuation multiple to set the enterprise value, which means even modest adjustments can shift the final price by millions.

What EBITDA normalization means for your deal price: Normalized EBITDA is the earnings figure that survives buyer due diligence - adjusted for non-recurring costs, owner-specific expenses, and accounting anomalies. In mid-market deals where multiples typically range from 7x to 9.5x, every $100,000 of EBITDA that doesn't survive scrutiny reduces enterprise value by $700K to $950K. The normalization process also affects the valuation multiple itself, deal structure, and financing terms.

Why Small EBITDA Changes Create Outsized Valuation Swings

The math behind EBITDA normalization is deceptively simple, but its impact on deal outcomes is anything but. Enterprise value in most mid-market transactions follows the formula: EV = Normalized EBITDA x EV/EBITDA Multiple. That multiplication is what makes normalization so consequential.

Consider the range of multiples in the current market. GF Data reported average purchase multiples of around 7.5x adjusted EBITDA in Q3 2025 for PE-sponsored middle market deals. At those multiples, every dollar of sustainable EBITDA is "worth" $7.50 in enterprise value.

But here's what makes this especially important: different parties arrive at very different EBITDA figures for the same business. A financial due diligence example can illustrate this starkly - the same company showing $50M in reported EBITDA, can appear as $60M in the sell-side CIM, and $45M after buy-side diligence. At a constant 10x multiple, that translates to a 150M swing in enterprise value, driven entirely by which version of EBITDA you use.

This is why a Quality of Earnings analysis (QoE) - a detailed financial review that converts your "marketing EBITDA" into "bankable EBITDA" - has become central to mid-market dealmaking.

What EBITDA Adjustments Actually Survive Buyer Scrutiny

Not all EBITDA adjustments are created equal, and understanding which ones hold up in due diligence is critical to managing expectations around deal value. EBITDA normalization adjustments broadly fall into categories with very different survival rates.

Adjustments that typically hold up

Owner compensation normalization is one of the most common and generally accepted adjustments, but only when done correctly. If a founder pays themselves $500K when the market rate for an equivalent CEO is $250K, the $250K difference is a legitimate add-back. Where this adjustment fails is when sellers try to add back the entire salary as if no one needs to run the business post-close. Buyers will always normalize to market replacement cost, not to zero.

Genuinely one-time costs with clear documentation also tend to survive - a lawsuit settlement, a one-off relocation expense, or a natural disaster recovery cost. The key word is "genuinely." If it happened once, has clear invoice-level documentation, and there's no pattern of similar costs over the trailing three-year lookback period, buyers will generally accept it.

Related-party transaction normalization is accepted when backed by market comparables. If the founder owns the building and charges the company above-market rent, the difference between what's charged and what a market lease would cost is a defensible adjustment. But this works both ways - if the company occupies the founder's building at below-market rent, buyers will adjust EBITDA downward to reflect what rent would actually cost post-close.

Adjustments that consistently get challenged

Pro forma cost savings and run-rate adjustments is one of the most contested category in buyer due diligence. These include claims like "we just renegotiated our vendor contract" or "we're about to eliminate a department." The problem isn't that these savings are impossible - it's that they're unproven. Buyers treat anything that hasn't been fully implemented and reflected in actual financial results as speculative. Industry data consistently shows that heavier add-backs correlate with projection misses post-close, which is precisely why sophisticated buyers are skeptical of forward-looking adjustments packaged as historical earnings.

"One-time" costs that recur every year are another common failure point. If a company adds back restructuring costs, legal fees, or consulting expenses every single year, buyers stop treating them as non-recurring. The buyer heuristic is straightforward: if it shows up more than once in the lookback period, it's operational until proven otherwise.

Payroll savings from unfilled positions often fail because they suggest underinvestment rather than sustainable efficiency. A buyer planning to operate or grow the business assumes those roles will eventually be filled, which means the "savings" are temporary margin inflation that reverses as soon as the business returns to a normal operating posture.

Capitalized development costs in software and tech businesses are a particularly nuanced area. Capitalizing internal development costs boosts EBITDA on paper by moving expenses below the line, but it doesn't change the underlying cash economics of the business. Buyers focused on sustainable free cash flow will often reverse aggressive capitalization policies during diligence, which can significantly reduce adjusted EBITDA for tech companies that have been capitalizing heavily.

The five tests buyers apply to every adjustment

Across due diligence processes, buyer scrutiny tends to follow a consistent pattern. Each adjustment gets tested against a set of practical questions: Can it be traced back to specific general ledger entries, invoices, and bank statements? Does it appear more than once in the historical period, and if so, what evidence supports the claim that it won't recur? If the cost is removed, what replacement cost does the buyer need to budget for post-close? Is the adjustment already baked into the financial forecast or value creation plan (double-counting is a common seller mistakes)? And for any pro forma adjustment, what has already been executed versus merely planned?

Adjustments that can't pass these tests don't just get rejected - they erode trust in the entire EBITDA bridge, which can spill over into multiple compression and more aggressive deal structuring.

How PE and Strategic Buyers Treat EBITDA Adjustments Differently

EBITDA normalization doesn't happen in a vacuum - it's interpreted through the lens of whoever is buying the business, and PE firms and strategic acquirers often reach very different conclusions about the same set of numbers.

Private equity buyers underwrite to standalone, financeable cash flow. Their valuation model ultimately needs to work within the constraints of a leveraged capital structure, which means every EBITDA adjustment must survive not only the PE firm's own scrutiny but also the skepticism of their lenders. Industry surveys indicate that most private credit lenders cap permitted EBITDA add-backs in the range of 20-25% of reported EBITDA. That lender reality flows backward into PE diligence - if an add-back won't survive lender review, the PE buyer is unlikely to pay for it.

PE firms typically separate adjustments into two buckets: "true normalization" (historical items that are probably non-recurring) and "value creation" (forward-looking improvements they plan to execute post-close). The critical distinction is that PE buyers almost never give sellers purchase price credit for value creation items. Those improvements are what the PE firm is paying itself to execute.

Strategic buyers underwrite to post-integration economics. They're often willing to model cost synergies (redundant overhead, procurement savings, facility consolidation) and sometimes revenue synergies, because their existing operations create genuine integration opportunities that a standalone PE model doesn't have. This can make strategics more willing to "look through" certain costs that will genuinely disappear after integration.

But strategic buyers bring their own form of skepticism. Research from the CFA Institute specifically aimed at strategic acquirers buying PE-backed businesses recommends a "forensic lens" on recasted EBITDA, calling out adjustments for normalized personnel costs, recurring vendor contracts, and hidden support functions that were previously absorbed by the PE sponsor. Strategic buyers frequently add costs back into the P&L to reflect what the business truly requires under different ownership - effectively running "reverse add-backs."

The practical implication for sellers is significant. If your process includes both PE and strategic buyers, you need to understand that the same EBITDA adjustment may be fully accepted by one buyer type and completely rejected by another. Presenting adjustments in a single format that doesn't account for these differences is a missed opportunity.

A smarter approach is to prepare two reconciliations: a standalone normalized EBITDA (what the business earns today, sustainably) and a synergy bridge for strategic buyers that explicitly shows integration costs and timing alongside the upside. For PE buyers, the standalone version should be formatted in a lender-compatible way, with clear documentation and defined time windows for each adjustment.

How Normalization Affects Deal Structure, Not Just Price

When EBITDA normalization produces disagreement between buyer and seller - or simply adds uncertainty to the earnings story - the impact extends well beyond the headline valuation number. Mid-market deals frequently shift their structure to absorb that uncertainty.

Working capital adjustments: the dollar-for-dollar impact

Most mid-market deals are priced on a cash-free, debt-free basis with a normalized working capital target (often called a "peg"). EBITDA adjustments are multiplied to determine enterprise value, but working capital true-ups hit the purchase price dollar-for-dollar. If the working capital peg is set at $2 million and you deliver $1.8 million at closing, your purchase price drops by $200K - no multiplication, just a straight deduction.

This matters because the working capital peg is typically determined during the same QoE process that normalizes EBITDA. Once buyers tighten their view of what "normal" earnings look like, they often tighten the definition of normal working capital as well. The two analyses are connected, and founders who focus exclusively on defending EBITDA while ignoring working capital dynamics can lose significant value at closing through the back door.

Earn-outs: the negotiation valve for contested EBITDA

When buyer and seller can't agree on what EBITDA "really is," earn-outs are the most common structural compromise. Recent deal-term studies show earn-outs appearing in roughly a quarter to a third of private-company acquisitions, with median earn-out potential around 32% of the closing payment and median duration of 24 months.

What's especially relevant to normalization is that these earn-outs are frequently tied to EBITDA targets. The logic is straightforward: if the seller believes normalized EBITDA is $3 million and the buyer thinks it's $2.5 million, an earn-out bridges the gap by letting the seller prove their number over time. But this comes with real risk - earn-out disputes are common, particularly because EBITDA definitions can shift after the buyer takes operational control. It's worth noting that recent deal data shows a trend toward revenue-based earn-out metrics partly because EBITDA-based metrics create more room for post-close manipulation and definitional disputes.

Financing constraints: when lenders disagree with both parties

Even when a buyer and seller align on adjusted EBITDA, the deal can still shift structurally if lenders don't accept the same adjustments for leverage and covenant purposes. In mid-market leveraged finance, lenders have become increasingly cautious about aggressive add-backs, and disputes over "what counts as EBITDA" for covenant compliance have been rising. If lender-approved EBITDA is lower than the agreed purchase price implies, the deal rebalances - typically through more buyer equity at close, seller financing or deferred consideration, an earn-out component, or a revised price.

This is why sell-side EBITDA normalization isn't just about defending your number to buyers - it's about presenting a number that the entire capital stack can support.

When Normalization Work Pays for Itself (and When It Doesn't)

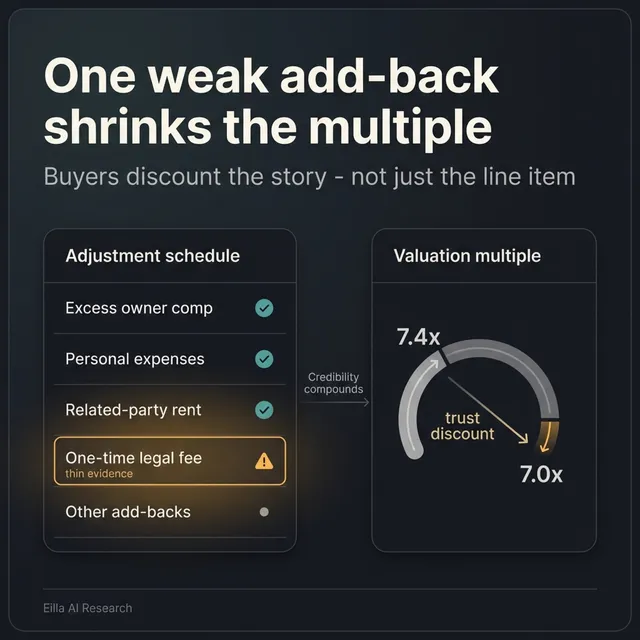

Sell-side Quality of Earnings work - where the seller commissions their own forensic EBITDA analysis before going to market - has become increasingly common. GF Data reports that nearly half of tracked mid-market deals now include a sell-side QoE. The data on outcomes is suggestive: across 360 deals, the average multiple was 7.4x with sell-side QoE versus 7.0x without, and in the $100M-$250M range, the gap widened to a full turn (8.3x vs. 7.3x).

However, this isn't a universal rule. In smaller deal sizes ($10M-$25M), the relationship actually inverted in the same dataset, with sell-side QoE corresponding to lower multiples. That likely reflects different dynamics at smaller scales - the cost of QoE is proportionally higher, the buyer pool is different, and the companies commissioning sell-side work may be doing so precisely because their financials are complex or messy.

The more defensible claim is about timing rather than absolute outcomes. Issues that surface pre-LOI tend to produce smaller price adjustments than issues discovered post-LOI during buyer due diligence. When a buyer's diligence team uncovers a problem the seller didn't flag, it doesn't just change the number - it changes the trust dynamic, which can cascade into tougher negotiation posture, multiple compression, and more aggressive deal structure demands.

For founders considering this investment, the decision framework is practical: if your financials include meaningful owner-related adjustments, related-party transactions, revenue recognition complexity, or a mix of recurring and non-recurring costs that could be interpreted differently, proactive normalization work is almost always worth it. If your P&L is clean, simple, and requires minimal adjustment, the value of sell-side QoE diminishes.

The Real Cost of Getting Normalization Wrong

The compounding nature of EBITDA normalization in deal outcomes deserves emphasis. When normalization reveals problems, the impact rarely shows up in just one place. A contested EBITDA figure can simultaneously reduce the base earnings number (multiplied by the multiple), compress the multiple itself (because credibility takes a hit), tighten working capital and net debt definitions (dollar-for-dollar deductions), shift deal structure toward earn-outs and deferred consideration, and reduce available leverage (forcing structural changes). These effects don't happen in isolation. They stack.

This is why EBITDA normalization is important for the deal preparation workstream that directly determines how much money you walk away with and on what terms. Understanding which adjustments will hold up, how different buyer types will interpret your numbers, and where the structural pressure points are in your deal is the difference between defending your price and watching it erode during diligence.

Key Takeaways

- EBITDA normalization is an important value driver in mid-market M&A because normalized EBITDA is multiplied by the valuation multiple - a $200K adjustment at 8x moves enterprise value by $1.6M.

- Not all EBITDA adjustments survive due diligence. Pro forma cost savings, recurring "one-time" expenses, and payroll savings from unfilled roles are the most commonly challenged categories.

- PE and strategic buyers treat the same EBITDA adjustments differently. PE underwriting is constrained by lender tolerance for add-backs (typically capped at 20-25% of EBITDA), while strategic buyers value synergies but apply "reverse add-backs" for costs they'll need to absorb.

- Normalization affects deal structure, not just price. Contested EBITDA commonly leads to earn-outs (appearing in 25-33% of private deals), tighter working capital pegs, and changes in financing structure.

- Working capital true-ups hit purchase price dollar-for-dollar, unlike EBITDA adjustments which are multiplied - and the working capital peg is set during the same diligence process that normalizes EBITDA.

- Issues disclosed before the LOI produce smaller price adjustments than issues discovered during buyer due diligence, because late-stage surprises erode trust and trigger cascading negotiation consequences.

- EBITDA normalization effects compound - a single credibility issue can simultaneously reduce the earnings base, compress the multiple, tighten closing mechanics, and force structural concessions.

FAQ

What is EBITDA normalization in M&A? EBITDA normalization is the process of adjusting reported earnings to reflect a company's sustainable, recurring profitability by removing one-time events, owner-specific costs, and accounting anomalies. In mid-market M&A, this normalized number is multiplied by a valuation multiple to determine enterprise value.

What EBITDA adjustments do buyers most commonly reject? Pro forma cost savings and run-rate adjustments are the most challenged category, followed by recurring costs labeled as "one-time," payroll savings from unfilled positions, and aggressive capitalization of development costs. Buyers apply a simple test: if it happened more than once, if it can't be traced to specific invoices, or if there's no evidence of execution, it typically doesn't survive diligence.

How does EBITDA normalization affect the purchase price? Normalized EBITDA is multiplied by the valuation multiple to set enterprise value, so even small changes have outsized impact. Additionally, normalization affects the multiple itself (credible numbers support higher multiples), working capital targets (dollar-for-dollar purchase price adjustments), and deal structure (earn-outs, seller financing, and deferred consideration increase when EBITDA is contested).

Do PE buyers and strategic buyers treat EBITDA add-backs differently? Yes, significantly. PE buyers underwrite to standalone, financeable cash flow and are constrained by lender add-back caps (commonly 20-25% of EBITDA). Strategic buyers can credit synergies but also apply "reverse add-backs" for costs previously covered by a parent company or sponsor. Sellers in mixed processes should prepare separate standalone and synergy-bridge reconciliations.

Is a sell-side Quality of Earnings report worth the cost? For businesses with meaningful owner adjustments, related-party transactions, or complex revenue recognition, a sell-side QoE typically pays for itself by defending value proactively. GF Data shows higher multiples associated with sell-side QoE in mid-to-large transactions, though the benefit is less clear for smaller deals under $25M.

If you're preparing for a potential exit and want to understand how your EBITDA adjustments would hold up under buyer scrutiny, our M&A advisory team can walk you through the normalization dynamics specific to your business and buyer universe.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.