The Complete Valuation Playbook for Banking Software Businesses

A practical, data-driven guide to how banking software businesses are valued and what drives high multiples.

If you run a Banking Software company and are thinking about a sale in the next 1-12 months, valuation is not just about revenue size. It is about what kind of revenue you have, how deeply your product sits inside a bank, how risky you look to a buyer, and how easy it is for an acquirer to believe your growth story.

That matters even more now. Banking software is still benefiting from long-term digital transformation, but buyers are more selective than they were a few years ago. They will pay up for businesses that are mission-critical, sticky, and clearly positioned around core banking, lending, compliance, payments, or bank workflow automation - and they will mark down businesses that look like custom project work dressed up as software.

This playbook is built to help you understand what Banking Software businesses actually sell for, what drives higher or lower multiples, where your own company may fit, and what you can do in the next 6-12 months to improve the outcome.

1. What Makes Banking Software Unique

Banking Software is not one single category. It includes core banking platforms, digital front-end platforms, account opening and onboarding tools, lending origination and decisioning systems, compliance and regulatory reporting software, payment infrastructure, and banking-focused systems integration or managed services. Those businesses can all serve banks - but they do not get valued the same way.

The reason is simple: buyers care deeply about where your product sits in the bank's workflow. If your software is tied to the core ledger, lending operations, compliance, payment processing, or daily customer servicing, it is harder to remove and easier to justify as mission-critical. That usually supports stronger valuation than software that feels optional, project-based, or dependent on a few consulting-heavy implementations.

Business model also matters more here than in many other software sectors. A Banking Software company may look like SaaS from the outside, but underneath it might have a large implementation layer, customization work, managed services, or reseller revenue. Buyers will separate the recurring, scalable software revenue from the labor-heavy revenue, and they will rarely give both the same multiple.

There are also sector-specific risks that buyers will always check. They will look at customer concentration, because one large bank contract can drive an outsized share of revenue. They will look at implementation risk, because complex go-lives can slip. They will look at regulation, security, uptime, data handling, and audit readiness, because a software issue in banking is not just an inconvenience - it can become an operational, legal, or reputational problem for the customer.

Finally, sales cycles are longer in Banking Software than in many other software markets. That can be a strength if it creates long contracts and low churn, but it also makes visibility important. Buyers want proof that your pipeline is real, your deployments are under control, and your growth is not dependent on one delayed procurement decision.

2. What Buyers Look For in a Banking Software Business

At a high level, buyers look for the same basics they look for in any good software company: growth, recurring revenue, gross margin, customer retention, and believable profitability. But in Banking Software, they also ask a more specific question: how essential are you to the customer, and how painful would it be to replace you?

That is why product position matters so much. A core banking platform, digital origination engine, compliance reporting tool, or deeply embedded payment workflow can command much more attention than a light front-end add-on. Buyers know that banks do not swap out these systems casually. If your product is woven into operations, risk management, or regulated reporting, your revenue tends to look safer.

They also care about customer quality, not just customer count. A well-diversified base of banks, credit unions, lenders, or fintech infrastructure partners is better than a business that depends on two marquee logos. Big-name customers can help your story, but over-dependence on them can hurt valuation if a buyer worries one renewal could change the entire picture.

Another major lens is implementation intensity. If every new client requires heavy services, custom coding, or long on-site support, a buyer will worry that growth is tied to headcount rather than software scalability. On the other hand, if implementations are becoming more repeatable, faster, and more template-driven, that is a sign the business is maturing into a better-quality software asset.

How private equity thinks about it

Private equity buyers usually start with three questions. First, what multiple are they paying to get in? Second, what kind of buyer could they sell to in 3-7 years? Third, what levers can they pull in between to increase value?

For Banking Software, that future buyer could be a larger strategic acquirer, a bigger private equity fund, or in rarer cases the public market. But that only works if the business becomes more scalable and easier to understand over time. Private equity will therefore focus on recurring revenue growth, margin expansion, customer stickiness, pricing power, cross-sell opportunities, and smaller add-on acquisitions.

They also think hard about whether the current multiple can expand later. If they buy a business that still looks partly like services, they will want a path to make it look more like software by improving mix, standardizing delivery, and tightening reporting. That is often where a lot of the upside comes from.

3. Deep Dive: Productized Software vs Services-Heavy Delivery

One of the biggest valuation questions in Banking Software is whether your business is really a software company with implementation support - or a services business with some proprietary software. That distinction can change valuation materially.

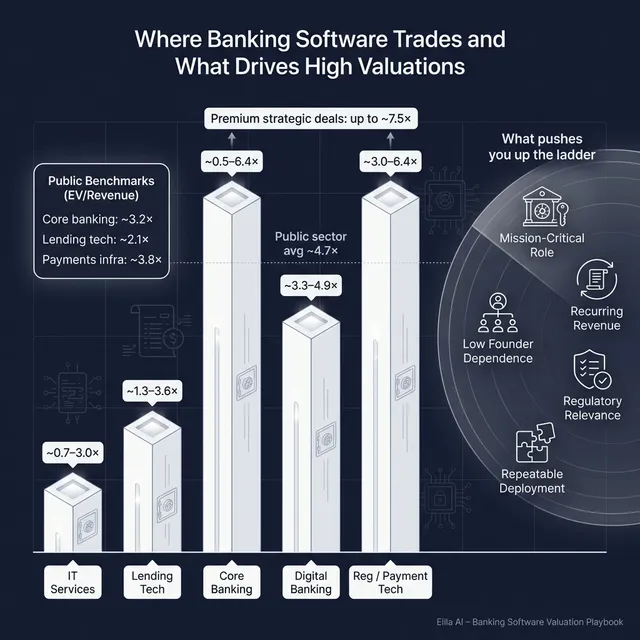

The data shows this clearly. Services-heavy banking IT and systems integration deals have tended to trade around low revenue multiples, roughly from 0.7x to 3.0x revenue in the precedent transactions provided. In contrast, software-led and platform-style assets in banking or adjacent financial workflow areas can reach much higher revenue multiples, especially when the product narrative is stronger and the revenue base is less labor-dependent.

Why do buyers care so much? Because services revenue usually resets every year. It depends on utilization, hiring, project wins, and delivery capacity. Software revenue, by contrast, is more likely to recur, scale without proportional headcount growth, and survive leadership changes. Buyers are not just buying this year's revenue - they are buying future cash flow quality.

This is especially important in Banking Software because many companies genuinely sit in the middle. They may have a strong core product, but they still rely on large implementation projects, customer-specific builds, regulatory tailoring, and managed support. Buyers understand that reality. What they want to see is progress toward repeatability: shorter deployments, more standard modules, more configuration and less custom code, and clearer separation between software revenue and services revenue.

If your business looks more like the left column today, you do not need to reinvent the company before a sale. But you should make it easier for buyers to see the software value inside the business.

A practical founder takeaway: even if your business will always need some implementation work, the market will reward you for proving that your delivery model is getting lighter, more repeatable, and less dependent on heroic services effort.

4. What Banking Software Businesses Sell For - and What Public Markets Show

Here is what the data actually shows. Private deals in this market span a wide range, because Banking Software covers everything from project-led consulting to product platforms tied to open banking, credit decisioning, or core systems. Public markets also show a wide spread, but the broad pattern is clear: software-like, scalable, mission-critical businesses trade higher than services-heavy or lower-growth models.

The most useful way to read the data is not to hunt for one magic multiple. It is to understand the bands, and then ask where your company belongs within them.

4.1 Private Market Deals (Similar Acquisitions)

The private deal data points to two very different valuation worlds. Banking and capital markets IT consulting or systems integration businesses have generally traded at about 0.7x to 3.0x revenue, with profitability sometimes supporting better EBITDA-based outcomes even when revenue multiples remain modest. At the other end, smaller software-led or platform-style assets in data, open banking, or decisioning can trade much higher on revenue, especially when buyers are underwriting future product value.

That does not mean every product company deserves a premium multiple. One of the highest observed revenue multiples in the set came from a very small, early-scale platform asset. In deals like that, the headline multiple can reflect a tiny revenue base and a strategic narrative, not just proven scale. Founders should be careful not to anchor on the highest outlier without asking why it happened.

The core lesson is that private market pricing depends heavily on what kind of business you actually are. A Banking Software company with strong recurring software revenue, regulatory relevance, and repeatable implementation can sit well above the services range. A company with similar revenue but more custom delivery may not.

4.2 Public Companies

As of mid to late 2025, the public comps in and around Banking Software show an overall average of about 4.7x EV/Revenue and 18.9x EV/EBITDA, with medians of about 3.1x and 13.4x respectively. That average is pulled up by stronger, more software-led assets and a few outliers, so founders should pay attention to the segment-level spread, not just the headline average.

Core banking and end-to-end banking system vendors broadly trade from around 0.5x to 6.4x revenue in the set, with the stronger, more scaled platforms clustering in the mid-single digits. Digital banking front-end and workflow platforms sit in a roughly 3.3x to 4.9x range for the stronger software names. Lending workflow and decisioning businesses in the sample sit around 1.3x to 3.6x, while payments infrastructure names span a wide range from the low-single digits up to much higher levels for exceptional assets. Services-heavy IT firms usually sit lower on revenue multiples because the market gives less credit for labor-based revenue.

* EBITDA average is skewed by outliers with unusual margin profiles.** This average is distorted by very high outliers in tiny, low-quality names. For most founders, the more relevant public read-through is still around the mid-single digits or below, depending on quality.

Public multiples are useful, but they are not your price tag. Public companies are larger, more liquid, more diversified, and easier to underwrite than a private company. That usually means a smaller private Banking Software business should be valued below the better public comps if it has lower scale, lower margins, customer concentration, or more implementation risk.

The reverse can also be true in selective cases. If you own a scarce, modern, cloud-native banking platform with strong reference customers and strategic value to multiple buyers, private market competition can sometimes support pricing at or even above the top end of the obvious public range. But that is the exception, not the default.

5. What Drives High Valuations (Premium Valuation Drivers)

Higher valuations in Banking Software usually come from some combination of strategic importance, recurring revenue quality, and believable scalability. Buyers pay more when they feel they are buying a durable platform, not just a current revenue stream.

Mission-critical position in the bank

If your software sits in a must-run part of the bank - core banking, lending operations, regulatory reporting, payment execution, fraud controls, or account opening - buyers are more likely to pay up. These budgets are harder for banks to defer, and replacement is painful.

A founder can often see this in customer behavior. If customers rely on you for daily operations, ask for roadmap influence, and treat you as infrastructure rather than as a nice-to-have tool, that usually helps your valuation story.

Regulatory and compliance relevance

The source data shows that businesses tied to compliance, regulatory reporting, tax reporting, open banking, and similar mandatory workflows can support premium outcomes. Buyers like revenue that is attached to a problem banks must solve, even in tighter spending periods.

In practice, that can mean software supporting capital markets reporting, tax and regulatory workflows, loan compliance, open banking requirements, or customer due diligence. The more you can show that your product is linked to necessary spending rather than discretionary innovation budgets, the better.

Clear EBITDA generation and margin quality

In services-heavy and mixed-model businesses, buyers often pay more attention to EBITDA than founders expect. The deal data shows that visible profitability can support premium EBITDA multiples even when revenue multiples stay modest.

This matters because buyers want proof that the business can generate cash, not just revenue. If you can show clean margin expansion, disciplined delivery, and improving contribution from software versus services, you become easier to underwrite.

Productization and repeatable deployments

A buyer will pay more if they believe each new customer does not require a fresh reinvention. Repeatable implementation, modular architecture, strong APIs, standard integrations, and configuration-led deployment all support a better valuation narrative.

Instead of saying "we can customize anything," the stronger story is usually "we have solved the same banking workflow repeatedly, with a controlled deployment model." That signals scale.

Strategic fit for an acquirer

The data also shows that strategic buyers sometimes pay up when a target can plug directly into an existing delivery or platform engine. In plain English, if a larger buyer can sell your product through its own channels, implement it with its own teams, or cross-sell it into its installed customer base, your value to that buyer may be higher than your stand-alone math suggests.

This is why positioning matters. You are not just telling buyers what your business is worth on paper - you are helping them see why your company makes their platform stronger.

Clean, predictable revenue

Even though this is obvious, it remains one of the biggest drivers of premium outcomes. Buyers pay more for revenue that is contracted, recurring, well retained, and easy to forecast. They especially like usage or subscription revenue that grows within existing accounts without looking volatile.

In Banking Software, this can include platform fees, long-term software licenses with support, transaction-linked revenue with good visibility, or multi-year contracts with low churn and strong renewal history.

Strong management bench and low founder dependency

A premium valuation is easier when the company does not appear to be held together by the founder alone. Buyers want to know who runs product, delivery, sales, compliance, and customer success if you leave after the transaction.

If your leadership team can speak confidently about the business without you in every room, that reduces perceived risk and makes the asset more transferable.

6. Discount Drivers (What Lowers Multiples)

Low-end outcomes are usually not caused by one issue alone. They happen when a buyer sees too much risk and not enough proof.

A common discount driver in Banking Software is a services-heavy revenue mix. If too much of your revenue depends on implementation work, customer-specific projects, or headcount-intensive support, buyers will worry that the business is harder to scale and easier to disrupt.

Another frequent issue is weak or volatile growth. A modern banking platform with declining revenue, delayed go-lives, or stop-start bookings will not get valued like a smooth, expanding software business. Even if the product is good, buyers will question what is really happening in the market.

Customer concentration also lowers multiples. If one or two banks account for a large share of revenue, every buyer will model the downside case. This is especially true if those relationships are tied to founder trust, special commercial terms, or unfinished implementations.

Poor quality of earnings is another big discount. That can mean messy revenue recognition, unclear separation of software and services margins, heavy capitalization, unusual pass-through revenue, or financial reporting that makes it hard to understand what the business actually earns. Buyers do not pay premium prices for numbers they do not trust.

In this sector, implementation and delivery risk can also drag valuation down fast. If projects are often late, gross margins swing because of custom work, or references say go-lives were painful, a buyer will assume future revenue is less valuable than it appears.

Finally, product sprawl hurts. If your roadmap is too broad, your codebase is highly bespoke, or your product suite is really a bundle of customer-specific solutions, buyers may see a maintenance burden instead of a scalable platform. The good news is that many of these issues can be improved before a sale if you identify them early.

7. Valuation Example: A Banking Software Company

Let us turn the logic into a worked example. The company below is fictional, and the revenue figure is fictional. The valuation range is illustrative only - not investment advice, not a fairness opinion, and not a formal valuation.

Step 1: How the logic works

Suppose you run a cloud-native core and lending platform for mid-sized banks. To value it, you would usually start by looking at the most relevant public comps - especially core banking platforms, digital banking workflow vendors, and selected financial software businesses that are software-led rather than services-led.

From the source data, stronger public banking software names broadly support a reference range in the mid-single digits of revenue, with some better-quality assets trading higher. But you would not simply copy a public multiple. You would adjust for your smaller size, lower liquidity, customer concentration, profitability, growth profile, and delivery risk.

Then you would look at private deals. These help you pressure-test whether your business looks more like a product platform or more like a services-heavy delivery business. If it looks like the former, you may justify a tighter range closer to stronger software comps. If it looks like the latter, your valuation should probably move down.

Step 2: Apply it to a fictional company

Assume a fictional company called NorthRiver Core.

NorthRiver Core sells a cloud-native banking platform to regional banks and digital lenders. It has:

- USD 10.0m revenue

- 78% recurring software and support revenue

- 68% gross margin

- 12% EBITDA margin

- Good customer retention

- 4 larger customers, but none above 22% of revenue

- A meaningful implementation layer, but deployments are becoming more standardized

For this business, a sensible approach would be:

- Use public software-led banking comps as the main anchor

- Ignore low-end IT services comps as the primary benchmark

- Apply a discount to scaled public leaders because NorthRiver is smaller and less proven

- Keep some premium potential if its cloud-native platform is strategically attractive

That leads to an illustrative revenue multiple framework like this:

Step 3: Why the range moves

The discounted case applies if NorthRiver still looks too implementation-heavy, if growth has slowed, or if a buyer sees customer concentration and execution risk. Even good banking software can land here if the business behaves more like a custom delivery firm than a software platform.

The core range applies if the company is solid but not perfect: good recurring revenue, good retention, decent margins, and clear product value, but still some scale and delivery questions. For many founder-owned Banking Software businesses, this is the realistic zone.

The premium case only applies if several strong drivers line up at once: scarce product category, reference customers, sticky use case, clear productization, solid profitability, and strong buyer competition. This is where strategic scarcity starts to matter.

The point is not that NorthRiver is "worth" one exact number. The point is that two Banking Software companies with the same USD 10m revenue can reasonably be worth USD 30m or USD 75m depending on quality, risk, and buyer fit. That is why valuation work should start months before a sale process, not after offers arrive.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple self-assessment can help you estimate whether you are closer to the low end, middle, or top end of the valuation range. Score each factor 0, 1, or 2. Be honest - the value comes from identifying where improvement is possible.

How to score it

- 0 = weak / inconsistent

- 1 = acceptable / mixed

- 2 = strong / clearly proven

How to interpret the score

If you are mostly scoring 2s on the high-impact factors, you are much closer to premium territory. That does not guarantee a premium outcome, but it means your business has the traits buyers usually fight over.

If you are mostly scoring 1s, you are likely in the fair-market middle. That is not a bad place to be, but it means process quality and positioning will matter a lot.

If you are carrying many 0s in the high-impact rows, the business may still sell, but you should expect buyers to focus on risk, structure, and downside protection. In that case, a 6-12 month improvement plan can have real payoff.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Founders often assume the market will "see the value" if the product is strong. It usually does not work that way. If your numbers are not clean, your story is not sharp, and your buyer list is not well built, you can end up anchoring the process around the wrong narrative.

The second mistake is hiding problems. Delivery issues, customer concentration, weak margins, product debt, security incidents, delayed implementations, and churn always surface in diligence. When buyers discover problems late, they rarely just ignore them. More often, they cut price, add earnouts, or lose trust altogether.

The third mistake is weak financial records. This is especially costly in Banking Software because many companies have mixed revenue streams. If you cannot clearly show software revenue, services revenue, gross margin by line, recurring support revenue, and normalized EBITDA, buyers will assume the worst. Often, this is fixable in 6-12 months.

The fourth mistake is running an unstructured sale process. Research and market experience consistently suggest that a competitive process run by a capable advisor can lead to meaningfully higher prices - often around 25% better than a one-buyer conversation - because it creates competition, better framing, and stronger negotiating leverage.

The fifth mistake is naming your price too early. If you tell the market you want USD 10m of enterprise value, do not be surprised when offers come back at USD 10.1m or USD 10.2m instead of the real number a buyer might have paid. Price discovery works best when buyers compete to tell you what the asset is worth to them.

There are also a couple of Banking Software-specific mistakes founders make. One is over-claiming that the business is SaaS when buyers can plainly see that implementations and customization drive the economics. Another is failing to document security, uptime, audit, and compliance readiness. In this market, operational credibility is part of value.

10. What Banking Software Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work is usually not a dramatic pivot. It is a series of practical moves that make your business look safer, cleaner, and more scalable.

Improve the numbers

Separate software revenue from services revenue clearly. Show recurring revenue, renewal rates, implementation margins, support margins, and normalized EBITDA. Tighten revenue recognition and remove accounting ambiguity.

If gross margin or EBITDA margin is being dragged down by inefficient delivery, fix the obvious pain points now. Buyers reward improvement they can see and trust.

Improve the product story

Reduce unnecessary customization where possible. Standardize implementations, narrow the roadmap, and document the modules that deploy repeatedly across customers.

If your product is tied to regulatory or mission-critical workflows, make that case clearly. Show how your software sits inside the customer's real operating environment, not just how it looks in a demo.

Improve the risk profile

Work on customer concentration if you can. Even one or two new meaningful accounts can help the story. Strengthen renewals, lock in multi-year agreements where realistic, and document the health of top accounts.

Also tighten security and compliance readiness. Make sure buyer diligence will find mature answers around uptime, controls, certifications, incident history, and data governance.

Improve delivery scalability

Show that implementations are becoming faster and more repeatable. Create deployment templates, standard integration paths, and documented onboarding processes. Buyers love to see a business getting less dependent on heroic services work.

If possible, track and present implementation metrics: average time to go-live, average services effort per customer, and the share of deployments using standard templates. That turns a vague story into evidence.

Improve the sale narrative

Build a clear market map around where you fit: core banking, digital origination, compliance workflow, payments infrastructure, or another clear category. A focused positioning usually sells better than a broad "we do everything for banks" narrative.

Prepare strong case studies that show measurable customer value. In Banking Software, buyers respond well to proof that banks reduced onboarding time, improved straight-through processing, met regulatory deadlines, lowered servicing cost, or launched products faster because of your platform.

Improve management depth

Make sure your company can be presented as an institution, not a founder extension. Give more visibility to product, delivery, finance, and customer leaders. Buyers want to believe the transition risk is manageable.

None of these moves needs to be massive. But together, they can shift how buyers classify your business - and that classification often matters more than one extra point of growth.

11. How an AI-Native M&A Advisor Helps

A good M&A process is not only about finding one buyer. It is about finding the right set of buyers and creating real competition. An AI-native advisor can widen the buyer universe far beyond the usual short list by identifying hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, and likely synergies. More relevant buyers usually means better offers, stronger leverage, and a higher chance the deal closes even if one buyer drops out.

Speed also matters. AI can help match buyers faster, support outreach, accelerate creation of marketing materials, and make diligence preparation more efficient. That can help founders get to initial conversations and offers in under 6 weeks, instead of losing months in a manual, slow-moving process.

That does not replace human judgment. The best outcome comes from expert human M&A advisors using AI to work faster and more intelligently. You still need experienced people to shape the equity story, prepare the numbers, manage buyer psychology, negotiate structure, and position the business in the most compelling way.

The real benefit is that you get Wall Street-grade advisory quality without traditional bulge bracket costs. If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.