The Complete Valuation Playbook for Biotechnology Businesses

A practical guide to how biotechnology businesses are valued today and what drives high mutliples.

If you are thinking about selling your biotechnology business in the next 1-12 months, valuation is not something to leave until the last minute. In biotech, buyers are more selective than they were during the easiest funding years, and they are looking much harder at revenue quality, regulatory strength, margin durability, and how well your business fits into a larger platform.

This playbook is built to help you understand what biotechnology businesses actually sell for, what drives higher and lower multiples, and how buyers really think about value in this sector. It is based on transaction and public market data from across biotech, diagnostics, life-science tools, and related services - and translated into plain English.

The goal is simple: help you see where your business likely fits today, what could move it up the range, and what you can do in the next 6-12 months to improve the outcome.

1. What Makes Biotechnology Unique

Biotechnology is not one market. It is a broad sector that includes very different business models: branded and specialty pharma, biologics platforms, biosimilars, in vitro diagnostics, molecular testing, life-science reagents, lab services, CDMOs and CROs, cold-chain and biostorage providers, and specialized development or manufacturing platforms. A buyer does not value all of these the same way, because the revenue models, capital needs, and risk profiles are very different.

That is the first thing that makes biotech unique: two businesses with the same revenue can have completely different value depending on what sits underneath the revenue. A company with recurring assay consumables, validated instruments, and sticky lab workflows will usually be valued very differently from a project-based development services business. A profitable cGMP biostorage platform with qualification-heavy customer relationships is also a very different asset from a business that depends on one-off research contracts.

The second thing that makes biotech unique is that buyers are often paying for more than current profit. They are paying for regulatory positioning, installed base, assay menu depth, switching costs, manufacturing know-how, intellectual property, scientific credibility, and platform fit. In some parts of biotech, especially diagnostics and specialty tools, strategic relevance can matter almost as much as near-term EBITDA.

The third thing is risk. In biotech, buyers always check a few things very closely: regulatory exposure, reimbursement risk where relevant, customer concentration, product concentration, scientific defensibility, manufacturing quality, supply chain resilience, and the difference between truly recurring revenue and revenue that only looks recurring. They also care about whether growth is durable or whether it was helped by temporary demand spikes, grant funding, unusual contracts, or underinvestment in the business.

2. What Buyers Look For in a Biotechnology Business

At a basic level, buyers look for the same headline factors they do in most deals: scale, growth, margins, and confidence in future cash flow. But in biotech, the definitions are more specific. Buyers want to know whether your growth comes from repeatable commercial demand, whether your gross margin is structurally strong, and whether your business can grow without costs rising just as fast as revenue.

They also look hard at the shape of your revenue. Is it consumables, reagent pull-through, long-term customer programs, recurring storage contracts, testing volume, licensing income, milestone-heavy revenue, or project work? Buyers usually pay more for revenue that is repeatable, visible, and embedded in customer workflows. They pay less for revenue that is lumpy, customer-specific, or dependent on constant new sales just to stand still.

For many biotechnology businesses, workflow position matters a lot. If your product sits inside a regulated lab process, clinical pathway, manufacturing process, or qualified storage chain, buyers tend to view that as more valuable than a nice-to-have tool. The closer you are to a mission-critical workflow, the harder it is for a customer to switch, and the more strategic you become to a larger acquirer.

Management depth also matters more than many founders expect. Buyers do not just buy the science or product. They buy the ability of the business to keep performing after closing. If too much depends on you personally - the founder, chief scientist, or rainmaker - valuation usually comes under pressure.

How private equity thinks about a biotech deal

Private equity buyers are usually asking three simple questions. First, what multiple am I paying now? Second, what multiple could I sell this for in 3-7 years? Third, what improvements can I make in between?

That means they care a lot about whether your business can become a larger, cleaner, more profitable platform. They will think about pricing, cross-sell, margin improvement, add-on acquisitions, international expansion, manufacturing efficiency, and whether the business can be sold later to a strategic buyer, a larger private equity fund, or in rare cases the public market.

In biotech, private equity also cares about how much of the story is execution versus pure scientific uncertainty. They are generally more comfortable paying up for businesses that are already commercial, already revenue-generating, and already positive or close to positive on EBITDA - especially if the upside can be protected through earnouts or performance-linked structures.

3. Deep Dive: Why Workflow Position and Revenue Quality Matter So Much in Biotech

In biotechnology, one of the biggest valuation questions is this: are you a critical part of the customer workflow, or are you easier to replace than you think? That question shows up repeatedly in both the transaction data and the premium drivers. Businesses that sit inside regulated, qualification-heavy, or clinically urgent workflows tend to command stronger valuations than businesses selling more interchangeable products or project labor.

The data supports that. Premium outcomes are concentrated in assets tied to specialized diagnostics, cGMP storage, regulated sample handling, and integration-ready bolt-ons. In other words, the market pays up when a buyer sees a business as an operating node it can plug into a bigger platform, not just a standalone revenue stream.

Why do buyers care so much? Because switching costs matter. If your business is tied into lab validation, sample integrity, regulatory procedures, hospital workflows, assay menus, or long-standing qualification processes, customers do not switch casually. That makes the revenue more dependable, which makes the business more valuable.

Founders often miss the second part: revenue quality is not just about recurring contracts. It is about how hard the revenue is to dislodge. A business with annual consumables revenue linked to an installed instrument base may be worth more than a larger business doing project-based scientific services, because the first one is harder to replace and easier to scale.

A useful way to think about it is this:

If your business looks more like the left column today, the goal in the next 6-12 months is not to reinvent the company. It is to make your revenue look more embedded, more repeatable, and more platform-like. That can mean longer contracts, clearer renewal data, more standardization, stronger integration into customer processes, better proof of recurring pull-through, or packaging your offering as part of a broader workflow rather than a one-off product.

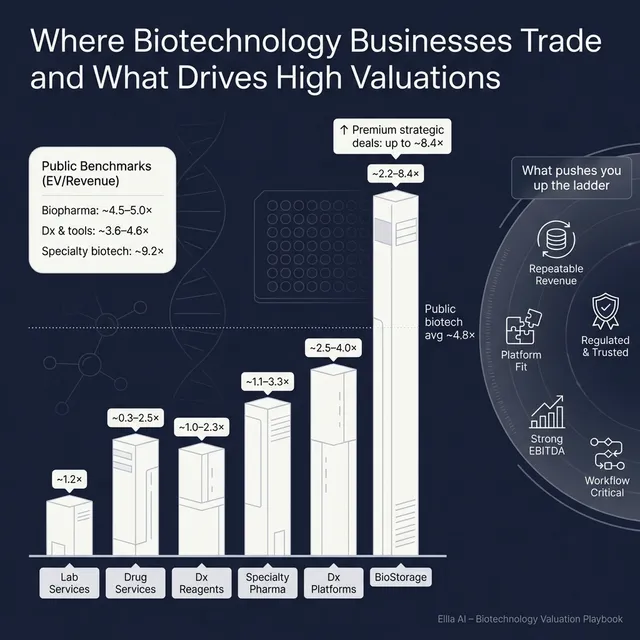

4. What Biotechnology Businesses Sell For - and What Public Markets Show

The data shows a very wide valuation range across biotechnology. That is normal. This sector includes everything from large global biopharma companies to small diagnostics players, reagent businesses, service providers, and infrastructure assets. The right way to use valuation data is not to grab the highest headline multiple - it is to find the part of the market that actually looks like your business.

At a high level, the precedent transaction set in the sources shows an overall average EV/Revenue of about 2.2x and median of about 2.1x, with average EV/EBITDA of about 12.8x and median of about 9.9x. Public markets are richer overall, with average EV/Revenue of about 8.5x and median of about 4.8x, and average EV/EBITDA of about 23.1x with median of about 13.8x. But those overall numbers hide major differences by segment.

4.1 Private Market Deals (Similar Acquisitions)

In private market biotech deals, most businesses transact in a fairly grounded revenue-multiple band unless they have something clearly strategic, scarce, or unusually profitable. The transaction set points to many ordinary deals in the roughly 1.0x-3.3x revenue range, especially for services-heavy, manufacturing-heavy, or more traditional commercial pharma assets. Higher outcomes appear where the business has regulated infrastructure, a differentiated diagnostics niche, or strong profitability that a larger buyer can scale.

The private deal data also shows that buyers will sometimes pay much more for small but strategic assets when the business sits in a valuable workflow. Examples in the data include higher-multiple deals in specialized diagnostics and cGMP storage. But those are exceptions driven by specific deal narratives - not the default for the sector.

The message for founders is simple: the private market does pay premiums in biotech, but only for a reason. Buyers do not reward the sector label by itself. They reward proof that your business is strategically useful, operationally real, and hard to replace.

4.2 Public Companies

Public markets, as of mid to late 2025 in the data provided, show a much broader range. Large global biopharma innovators generally trade around the mid-single-digit revenue multiple area, with examples in the sources ranging roughly from the low-2x area to above 6x, and a strong group of names around 3.0x-6.8x revenue. Large diversified diagnostics and life-science tools businesses mostly sit around 1.8x-6.2x revenue. More specialized or faster-growing biotech names can trade much higher, but those readings can be distorted by very small revenue bases, losses, or public market volatility.

The cleaner lesson is that public markets reward three things again and again: scale, durable margins, and confidence in future growth. Businesses with strong commercial platforms and high profitability tend to trade better than narrower or more volatile businesses. Businesses with tiny revenue bases or inconsistent profitability can show extreme revenue multiples, but founders should treat those with caution.

Public multiples are a reference point, not your price tag. Private companies are usually smaller, less liquid, less diversified, and riskier than public companies, so their valuations are often lower. But public comps still matter because they shape buyer psychology, board expectations, and what an acquirer believes it could eventually own or exit into.

That said, public multiples can also understate the right price for a scarce private asset. If your business fills a real product gap, provides access to a qualified workflow, or accelerates an acquirer’s strategy, a strategic buyer may pay above where a simple small-company discount would suggest. That is why positioning and buyer targeting matter so much in biotech deals.

5. What Drives High Valuations (Premium Valuation Drivers)

The data shows that premium outcomes in biotechnology do not come from one factor alone. They usually come from a combination of commercial proof, strategic fit, margin quality, and reduced execution risk. Here are the themes that move businesses toward the top of the range.

5.1 Real operating leverage and margin quality

Buyers pay more when they believe your margins are not only good today, but can remain strong and expand with scale. In the source data, the strongest EV/EBITDA outcomes line up with businesses that already showed positive EBITDA and strong conversion from gross profit into operating profit.

Why this matters is simple: buyers want to know that additional revenue will create meaningful additional profit. A business with high gross margins but constant custom work, constant scientific firefighting, or hidden cost needs will not get the same credit as a business with clean, scalable economics.

Practical examples:

- A diagnostics company with a validated assay menu and repeat consumables revenue.

- A reagents business with high gross margin and limited customer churn.

- A biostorage platform where the facility is already built and incremental utilization is highly profitable.

5.2 Regulated infrastructure and switching costs

Scarcity value matters in biotech. The source data highlights cGMP storage, regulated sample handling, and similar infrastructure as areas where buyers paid clearly stronger revenue multiples. That makes sense because these assets are hard to replicate quickly and hard for customers to switch away from.

Buyers like assets that are embedded in qualification-heavy environments. Once SOPs, audits, temperature controls, chain-of-custody rules, and customer approvals are in place, the revenue becomes stickier. That stickiness often matters more than headline growth.

Practical examples:

- Controlled storage tied to cell and gene therapy workflows.

- Qualified sample logistics supporting regulated development programs.

- Infrastructure tied to audited pharma or clinical lab environments.

5.3 Clinically important differentiation

In biotech, not all innovation is valued equally. Buyers pay more when your product solves an urgent and clearly valuable problem, especially in diagnostics and infectious disease. The source data points to premium outcomes where the target had a differentiated niche in high-urgency clinical settings.

The key is that the differentiation must be commercially meaningful, not just scientifically interesting. Buyers care about faster results, better sensitivity or specificity, better menu coverage, stronger regulatory positioning, or the ability to win a place in the clinical workflow.

Practical examples:

- An assay that addresses antimicrobial resistance or urgent infectious disease testing.

- A molecular platform that shortens turnaround time in a high-value use case.

- A product that lets the buyer fill a known gap in its menu or platform.

5.4 Integration-ready strategic adjacency

One recurring pattern in the data is that buyers pay up when the asset can slot directly into an existing platform. This is where strategic fit becomes real economics, not just a pitch slide. If the acquirer can plug your business into its commercial footprint, manufacturing base, or workflow network quickly, your value goes up.

That is especially true in biotech because platform fit can create immediate cross-sell, menu expansion, utilization gains, or geographic leverage. Buyers often pay more for an operating node they can scale now than for a loose idea they have to build around.

Practical examples:

- A diagnostics company that expands an acquirer’s testing menu.

- A lab services business that fills a geographic gap.

- A niche tools or storage asset that strengthens an existing pharma services network.

5.5 De-risked growth with earnout-friendly structure

The source data shows an important pattern: some of the stronger outcomes came when buyers could use earnouts or milestone-based consideration. That allowed them to pay more without taking all the risk upfront.

This usually works best when the business is already operating and already generating revenue. In that situation, the earnout becomes a way to share upside rather than rescue a weak story. For founders, that means a premium headline valuation is often easier to achieve when your base business is already credible and the remaining upside is clearly measurable.

5.6 Clean business fundamentals

Even in biotech, premium valuations are not just about science or strategic narrative. Buyers pay more for businesses with clean financial records, predictable revenue, good KPI tracking, diversified customers, low founder dependence, and a management team that can operate after closing.

These basics are easy to overlook because they feel less exciting than product or pipeline. But in real sale processes, they often separate the businesses that get aggressive bids from the businesses that get cautious bids.

6. Discount Drivers (What Lowers Multiples)

Just as premium outcomes follow patterns, lower valuations follow patterns too. In biotech, businesses drift to the lower end of the range when buyers see risk they cannot underwrite clearly.

One of the biggest discount drivers is revenue that looks less durable on closer inspection. That includes highly project-based revenue, concentration in a small number of customers, dependence on one key distributor, demand tied to unusual temporary conditions, or weak evidence of repeat purchasing. In biotech, buyers are always asking: will this revenue still be here in two years?

Another major discount is weak profitability or poor margin quality. Low margins by themselves are not always fatal, especially for growth businesses, but buyers get nervous when they cannot tell whether margins are temporarily depressed for a good reason or structurally weak for a bad one. If the cost base is messy, if revenue recognition is unclear, or if the business needs constant founder intervention just to operate, valuation usually comes down.

Lack of differentiation is also a common problem. If your product is one of many similar offerings, or if your service can be replaced by another qualified vendor without much pain, buyers generally will not pay strategic premiums. In biotech, being technically competent is not the same as being strategically scarce.

A few more red flags commonly lower value:

- Customer or product concentration.

- Regulatory or quality issues, even if small.

- Supply chain fragility.

- A weak second layer of management.

- Growth that comes from underpricing rather than real demand.

- Heavy dependence on one geography, reimbursement path, or channel partner.

There are also industry-specific discount factors that matter a lot in biotech. One is scientific story without commercial proof. Buyers will discount businesses where the product promise sounds strong but adoption, reimbursement, validation, or repeat customer behavior still looks uncertain. Another is manufacturing or quality risk. In regulated industries, buyers do not like surprises around quality systems, batch consistency, documentation, or facility readiness.

The good news is that many discounts are at least partly fixable. Buyers are not looking for perfection. They are looking for honesty, evidence, and a path they can underwrite.

7. Valuation Example: A Biotechnology Company

To show how valuation logic works in practice, let us build a fictional example. The company below is fictional, and the USD 10m revenue level is also fictional. The point is to illustrate how buyers move from market data to a likely valuation range - not to provide formal valuation advice.

7.1 Step 1: Start with the right comp set

Suppose your company is HelixCore Diagnostics, a fictional biotechnology business with:

- USD 10m of annual revenue

- Positive EBITDA

- A focused molecular diagnostics product line

- Strong gross margins

- Revenue from both instruments and recurring assay pull-through

- Customers in hospital labs and reference labs

- Some international distribution, but still relatively small scale

The first step is to avoid the wrong comparison. You would not value this business off mega-cap pharma alone, and you would not value it off early-stage biotech companies with tiny revenue and public market volatility. The better anchors are:

- Private transactions in IVD, diagnostics, and niche regulated biotech platforms

- Public diagnostics, life-science tools, and related healthcare platform businesses

- A practical discount for smaller scale and private-company risk

- A practical premium if the business has unusually strong workflow position, margins, or strategic fit

The source data also gives a helpful framework from a large public biotech example: start with the relevant segment, find a sensible core band rather than the full wild range, and then tighten the range around the business's actual profile. That is the right logic for private biotech too.

7.2 Step 2: Build a core valuation range

For a fictional USD 10m-revenue biotech company like HelixCore, a sensible starting point might be a core EV/Revenue band of roughly 2.5x-4.0x. That range reflects the transaction data for ordinary biotech and diagnostics assets, while giving some credit for a more attractive diagnostics profile.

Why not start much higher? Because private companies at this size usually face a scale discount. Even if public market references are higher, buyers adjust down for concentration, lower liquidity, smaller commercial footprint, and execution risk.

Why not start lower? Because if the company is profitable, specialized, and sits inside a real diagnostic workflow, it should not be valued like a generic service asset or an undifferentiated product business.

7.3 Step 3: Move the multiple up or down based on real drivers

From there, the multiple moves based on what is true about the business.

A premium case might apply if HelixCore has:

- Strong assay pull-through and repeat purchasing

- Good evidence of customer stickiness

- A differentiated niche in a clinically important testing area

- Positive EBITDA with room for operating leverage

- Regulatory credibility and good quality systems

- A clear strategic fit for a larger diagnostics platform

A discounted case might apply if:

- Too much revenue is one-time instrument placement

- Customer concentration is high

- Growth is real but not yet durable

- The business still depends heavily on the founder

- Regulatory, reimbursement, or scale-up risks remain meaningful

7.4 Illustrative valuation table

That means two biotechnology businesses with the same USD 10m revenue could plausibly be worth USD 20m or USD 50m-plus depending on revenue quality, strategic fit, margin profile, and risk. That is normal in this sector.

The important lesson is not the exact number. It is the logic. Buyers do not value revenue in biotech as a flat commodity. They value the quality, defensibility, and strategic usefulness of that revenue.

This is only a worked example, not investment advice, not a fairness opinion, and not a formal valuation.

8. Where Your Business Might Fit (Self-Assessment Framework)

A good self-assessment is not about flattering yourself. It is about finding the few factors that most strongly influence where your valuation lands. Score each factor as:

- 0 = weak

- 1 = mixed

- 2 = strong

8.1 Scoring table

8.2 How to interpret the score

If you score mostly 2s in the high-impact category, you are more likely to sit toward the upper half of the valuation range for your subsector. If you are mostly 1s, you are probably in fair-market territory: sellable, but not obviously premium. If you have several 0s in the high-impact factors, the biggest value creation may come from preparation before launching a process.

A simple interpretation guide:

The point is not to create a fake scorecard. The point is to identify where one good fix could have an outsized payoff. In biotech, one improvement in workflow stickiness, quality readiness, or revenue visibility can matter more than five smaller cosmetic fixes.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes founders make is rushing into a sale before the business is ready. If your numbers are messy, your story is unclear, or your customer and product data are not organized, buyers will sense uncertainty and price it in. A rushed process almost always weakens leverage.

Another common mistake is hiding problems. In biotech, issues always come out in diligence - quality gaps, regulatory questions, customer concentration, soft renewals, margin adjustments, weak documentation, or founder dependence. If a buyer discovers those late instead of hearing about them early and honestly, trust drops fast and valuation usually follows.

Weak financial records are also costly. If you can improve your reporting in the next 6-12 months, do it. Buyers want to see clean revenue breakdowns, gross margin by product or service line, customer concentration, cohort behavior where relevant, renewal or reorder data, and a credible bridge from revenue to EBITDA. In biotech, better reporting often makes the difference between a cautious bid and a confident one.

Another major mistake is running an unstructured sale process without an advisor. A structured competitive process usually improves price because it creates real market tension, better buyer matching, and stronger negotiating leverage. Research and market experience consistently suggest that a properly run competitive process with an advisor can increase purchase prices meaningfully - often around 25% compared with a weak one-buyer process.

Founders also hurt themselves when they reveal the price they want too early. If you tell buyers you want USD 10m of enterprise value, many of them will simply anchor around that number and come back with USD 10.1m or USD 10.2m instead of showing what they might have offered in a true price discovery process. In biotech especially, strategic buyers may value an asset much more highly than a founder expects - but only if you let the market speak first.

There are also a couple of biotech-specific mistakes worth calling out. One is overselling pipeline or technical promise while under-explaining commercial proof. Buyers care about what the science could become, but they pay based on what they can underwrite. Another is neglecting quality and regulatory housekeeping. In this sector, small documentation issues can trigger outsized fear.

10. What Biotechnology Founders Can Do in 6-12 Months to Increase Valuation

You do not need a total transformation before a sale. But a focused 6-12 month plan can materially improve how buyers see the business.

10.1 Improve the numbers buyers care about

Start by making revenue quality more visible. Break out recurring versus one-time revenue. Show reorder behavior, instrument pull-through, contract visibility, utilization, renewal rates, customer concentration, and gross margin by business line.

Then improve earnings quality. Clean up cost allocations, separate true operating costs from founder-specific or unusual items, and prepare a simple, credible explanation of margin trends. Buyers do not need perfection - they need clarity.

10.2 Reduce avoidable risk

Fix documentation gaps now, not during diligence. Review regulatory files, quality systems, manufacturing controls, customer agreements, distributor agreements, and IP ownership. If there is an issue, get in front of it and show the fix.

Also reduce dependence on any one person. Build up your second layer of management, document key commercial and technical processes, and make sure customer relationships are broader than just you.

10.3 Make the business look more embedded in customer workflow

If your business has repeatable elements, package them clearly. That may mean multi-year contracts, service bundles, assay menu expansion, customer success processes, or clearer proof that your product sits inside a qualified or sticky workflow.

If you can show that customers do not just buy once - they stay, reorder, qualify, integrate, or expand - you move closer to the profiles that achieve better outcomes.

10.4 Strengthen your strategic narrative

Founders often underestimate how much value comes from framing. You should be able to answer, very clearly: why would a larger buyer care? Do you fill a menu gap, add geography, deepen workflow control, improve a regulated offering, expand manufacturing capability, or create cross-sell potential?

This matters because strategic adjacency is one of the clearest premium themes in the data. If buyers can see how you fit, they are more likely to stretch.

10.5 Build a sale-ready evidence pack

Before going to market, prepare a concise set of proof points:

- Revenue breakdown by product, customer type, and geography

- Gross margin and EBITDA bridge

- Customer concentration and retention or reorder evidence

- Regulatory and quality summary

- Pipeline and product roadmap with commercial logic

- Clear reasons why the business is strategically valuable to multiple buyer types

This is not just presentation polish. It changes how buyers underwrite risk.

11. How an AI-Native M&A Advisor Helps

Selling a biotechnology business is not just about finding one buyer. It is about finding the right buyers, creating competition, and presenting the company in a way that matches how acquirers make decisions. That is where an AI-native M&A advisor can improve outcomes.

First, AI expands the buyer universe. Instead of relying on a short traditional list, an AI-native process can identify hundreds of qualified acquirers based on deal history, strategic fit, product adjacency, financial capacity, and other signals. That broader reach means more relevant conversations, more competition, stronger offers, and a higher chance the deal closes even if one buyer drops out.

Second, AI helps compress timelines. With AI-driven buyer matching and outreach, faster creation of marketing materials, and more efficient support through diligence, initial buyer conversations and first offers can often be reached in under 6 weeks. Speed matters because it keeps momentum high and reduces the risk of a process drifting.

Third, the best outcome still requires expert human judgment. AI works best when it enhances experienced advisors who know how to frame the story, prepare the numbers, manage buyers, and run a disciplined process. That combination can deliver Wall Street-grade advisory quality without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.