The Complete Valuation Playbook for Building Materials Supply Businesses

A practical guide to how building materials supply businesses are valued and what drives high multiples.

If you own a privately held Building Materials Supply business and are thinking about a sale in the next 1-12 months, valuation is no longer something to leave until the end of the process. The sector is still highly fragmented, strategic buyers continue to look for scale and route density, and private equity remains interested in businesses that can support add-on acquisitions, margin improvement, and local market expansion.

This playbook is built to answer three practical questions. First, what do Building Materials Supply businesses actually sell for? Second, why do some companies land at the top of the range while others get pushed down? Third, what can you realistically do in the next 6-12 months to improve your position before going to market?

The goal is not to give you a fake precise price tag. It is to help you understand the logic buyers use, where your business likely fits, and which changes can meaningfully improve value.

1. What Makes Building Materials Supply Businesses Unique

Building Materials Supply is not valued like software, and it is not valued like a pure manufacturer either. Most businesses in this space sit somewhere in between wholesale distribution, specialty merchanting, light fabrication, logistics, and customer service. That mix matters because buyers are usually underwriting gross profit quality, local competitive position, and earnings durability more than simple headline revenue.

The sector includes several business models. At one end are general merchants and trade counters selling a broad mix of products to contractors, builders, remodelers, and installers. At the other end are specialty distributors focused on insulation, openings, roofing, plumbing and heating, façade products, or other technically specified categories. Some businesses also add installation, prefabrication, kitting, warehousing, or jobsite delivery, which can improve customer stickiness but can also make the model more operationally complex.

What makes valuation tricky is that two suppliers with the same revenue can be worth very different amounts. A business that earns trusted specification-driven sales, has repeat contractor accounts, strong gross margins, and disciplined inventory management will usually be seen very differently from a merchant that mainly wins on price and lives quarter to quarter with weak margins.

Buyers will always test a few sector-specific risks. They will look closely at end-market exposure - new build versus repair and remodel, residential versus commercial, local contractor concentration, and exposure to cyclical project pipelines. They will also examine gross margin consistency, inventory turns, supplier dependence, branch economics, working capital intensity, and whether the business has any real moat beyond being another place to buy materials.

2. What Buyers Look For in a Building Materials Supply Business

At the most basic level, buyers care about scale, growth, and profit. But in this sector, they care even more about how those things are produced. Revenue that comes from repeat professional customers, specified products, and reliable local relationships is worth more than revenue that depends on one-off price quotes and volatile project timing.

They also care about gross profit quality. In supply businesses, gross margin tells a buyer a lot about pricing power, customer mix, product mix, and service value. A company with disciplined pricing, strong branch management, and a healthy share of specialty categories usually gets a much better reception than one that pushes big volume through thin margins.

Customer mix matters too. Buyers tend to like businesses that serve a large base of small and mid-sized contractors, installers, and trade customers rather than relying too heavily on a few national accounts or developers. The reason is simple: diversified demand is safer, and safer earnings usually support better multiples.

Operational reliability is another major factor. Buyers want to know whether your team can deliver the right product, on time, with low error rates, and without constant founder intervention. In Building Materials Supply, service failures can destroy customer trust fast. A buyer pays more for a business that already runs like a platform, not a personality-driven operation.

How private equity thinks about your business

Private equity buyers usually ask three questions very early.

First, can they buy at a reasonable price and still sell later at an attractive return? That means they care not just about what your business is worth today, but who might buy it from them in 3-7 years. If they believe a larger strategic buyer, a bigger private equity fund, or a scaled industry platform will want the business later, they get more comfortable paying up.

Second, what levers can they pull after closing? In this sector, that often means branch optimization, price discipline, procurement savings, better inventory management, tuck-in acquisitions, cross-selling adjacent categories, and improving salesforce productivity.

Third, how much risk are they taking on? If the business is highly cyclical, overly founder-dependent, or too exposed to low-margin commodity distribution, the entry price usually comes down. If it looks like a clean platform with good cash flow and room for add-on acquisitions, valuation usually improves.

3. Deep Dive: Commodity Merchant vs Specialty Value-Added Supplier

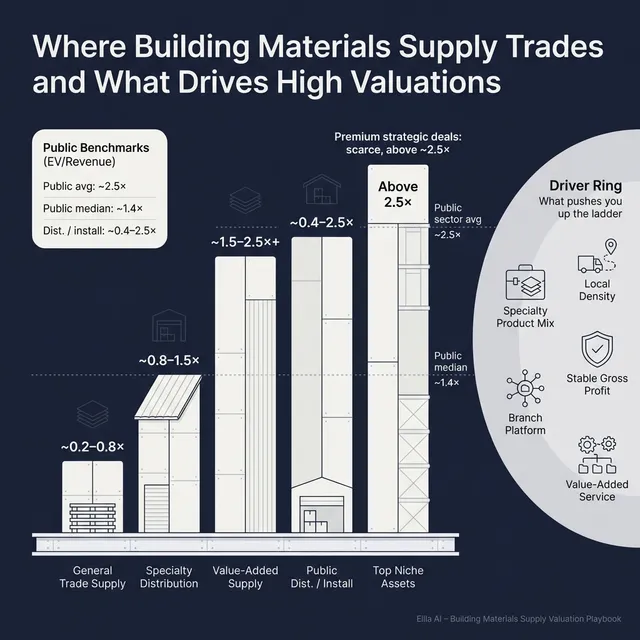

One of the biggest valuation questions in this sector is whether your business looks like a commodity merchant or a specialty, value-added supplier. This matters because the market consistently puts lower valuations on plain distribution and better valuations on businesses with real differentiation.

The data points are clear enough to be useful. Public construction products distribution businesses trade at lower revenue multiples than many higher-margin building product categories. As of mid to late 2025, the public distribution and installation group in the dataset ranged from roughly 0.4x to 2.5x EV/Revenue, with the broad average for public building materials names overall at 2.5x but the median only 1.4x. In private deals, standard trade supply and merchanting transactions in the dataset often sit below 1.0x revenue, while differentiated assets with stronger positioning can move well above that.

Why does this happen? Because buyers know that plain merchanting is easy to understand but hard to defend. If your customers can switch suppliers based mainly on price, and your products are widely available, then future margins are less secure. By contrast, if you are embedded in the workflow - through technical product knowledge, branch relationships, reliable jobsite delivery, fabrication, value-added service, or hard-to-replace supplier access - the earnings look more durable.

This also explains why scale alone does not guarantee a premium. The source data explicitly shows that larger revenue base and full control can help when the acquirer can cross-sell and integrate efficiently, but it also shows that scale without a moat does not automatically lead to higher multiples. In simple terms, buyers pay up for scale only when that scale comes with defensible economics.

If your business looks more like the lower-value version today, the path upward is usually operational rather than theoretical. Move toward categories where technical support matters. Strengthen local account density. Improve branch-level profitability. Build better data on customer retention, gross profit by account, and on-time delivery. That does not turn a merchant into software, but it can turn a commoditized business into a much more attractive acquisition.

4. What Building Materials Supply Businesses Sell For - and What Public Markets Show

Here is what the data actually shows. Building Materials Supply businesses usually trade on modest revenue multiples compared with software or premium industrial technology assets, but the range is wide because business quality varies a lot. The biggest separators are margin quality, differentiation, scale, and whether the buyer sees clear post-deal upside.

4.1 Private Market Deals (Similar Acquisitions)

In the private market data, standard building products distribution and trade supply deals mostly cluster below 1.0x revenue. Examples in the dataset include insulation supply, plumbing and heating trade supply, and smaller merchant-style businesses. That is the core message founders should take seriously: for many supply businesses, revenue alone does not drive value - earnings quality does.

That said, the dataset also shows that differentiated businesses can command much better outcomes. A vertically integrated specialty materials and distribution business cleared around 2.4x revenue, while a windows and doors distributor with stronger economics cleared a much higher revenue multiple. Some outliers exist in adjacent categories, but for a typical privately held Building Materials Supply business, a realistic private-market range is usually well below the headline average unless the company has real differentiation.

These ranges are illustrative, not formal valuation opinions. Your exact outcome will depend on EBITDA margins, growth, customer quality, geography, supplier relationships, and how competitive the sale process is.

4.2 Public Companies

Public market data provides a reference point, not a direct price tag. Across the broader building materials universe in the source set, the overall public average was about 2.5x EV/Revenue and 9.8x EV/EBITDA, while the median was about 1.4x EV/Revenue and 9.5x EV/EBITDA as of mid to late 2025. That gap between average and median tells you something important: a handful of stronger businesses pull the average up, but most names trade lower.

Within that universe, public construction products distribution and installation names traded roughly around 0.4x-2.5x revenue in the data. By contrast, higher-quality building envelope, specialty chemicals, and some differentiated exterior product groups often traded higher. In other words, the public market rewards differentiated product mix, stronger margins, and better growth more than it rewards simple volume.

Founders should use public multiples as upper and lower guideposts, not as a promise. Public companies are usually larger, more diversified, better capitalized, and more liquid than private businesses. That means a private company usually needs to be adjusted downward for smaller scale, customer concentration, and risk.

But the reverse can also happen. If your business is scarce, strategically important in a region, or has unusually strong economics for the sector, a buyer may pay more than a plain public comparison would suggest. That is especially true when there are clear synergies and multiple bidders.

5. What Drives High Valuations (Premium Valuation Drivers)

The source data points to a few themes that repeatedly show up in stronger outcomes. Some are industry-specific, and some are classic M&A fundamentals. Together, they explain why one Building Materials Supply business may get a very ordinary bid while another attracts aggressive interest.

5.1 Differentiation that makes price less important

Buyers pay more when your business is hard to replace. In this sector, that can mean specialty product expertise, exclusive supplier access, local market leadership, technical support, design assistance, prefabrication, or service levels that contractors truly rely on.

The data supports this. Differentiated and vertically integrated assets in the source set were more likely to clear stronger revenue multiples than plain merchanting businesses. Buyers are not paying up for volume alone - they are paying for defensible gross profit.

A practical example is a distributor that does more than sell stock. If your team helps customers choose the right product, avoids installation problems, and gets material to site faster and more reliably than peers, that is real value in a buyer’s eyes.

5.2 Scale that creates integration value

Scale matters, but only when it creates usable synergies. The source commentary notes that larger revenue bases with full control can support higher valuations when the buyer can spread overhead, cross-sell, and improve procurement or logistics.

This matters for founders because a buyer is often thinking one step beyond your current earnings. They may see branch overlap, better freight efficiency, stronger buying power, or the ability to push adjacent categories through your customer base. If your business is large enough and organized enough for that upside to be credible, valuation usually improves.

5.3 EBITDA margins that support debt and future deals

High-quality earnings matter more than impressive top-line revenue. The deal data shows that the cleaner premium outcomes often appeared in businesses with stable EBITDA margins and enough cash flow to support leverage and future acquisitions.

For a Building Materials Supply business, that usually means buyers like to see more than just revenue growth. They want evidence that your margins are real, repeatable, and not inflated by unsustainable pricing or underinvestment. Strong branch-level profitability, good working capital control, and disciplined overhead all matter.

5.4 Exposure to long-term structural themes

The premium driver data also highlights exposure to sustainability and decarbonization themes. In building materials, that can include insulation, energy efficiency, lower-carbon products, waterproofing, retrofit demand, and other categories linked to building performance.

This does not mean you can use green language and expect a premium. The sources are clear that sustainability by itself is not enough. Buyers only care if it connects to something measurable - better growth, better pricing, better margins, or strategic relevance.

5.5 A business model that sits closer to mission-critical decisions

The data also shows that businesses tied to mission-critical performance or specification-sensitive applications can attract stronger strategic interest. In supply, the nearest parallel is when your company is not just a reseller, but a trusted source for products where failure is expensive - fire safety, thermal performance, waterproofing, envelope integrity, or code compliance.

The closer you are to solving costly problems for builders, installers, or owners, the more secure your position becomes. Buyers value that because it makes customer relationships stickier and pricing more rational.

5.6 Clean fundamentals that make diligence easy

Even when not called out directly in the source set, the basics still matter. Clean financials, a diversified customer base, stable leadership beyond the founder, predictable reporting, and credible KPI tracking can all move you toward the top of the range.

A buyer will almost always pay more for a business that is easy to understand and easy to underwrite. Confusion is expensive. Clarity supports valuation.

6. Discount Drivers (What Lowers Multiples)

Most lower-end outcomes are not random. They usually come from a small number of issues buyers see again and again.

The first is commodity exposure without a moat. If your business mainly sells interchangeable products, competes heavily on price, and has limited ability to defend gross margin, buyers will usually value it as a lower-quality distributor. That does not make it unattractive, but it does reduce the multiple.

The second is weak earnings quality. Buyers get nervous when EBITDA is thin, volatile, or hard to reconcile. If margins jump around, inventory discipline is poor, or there is a big gap between reported profit and cash generation, the buyer will normally discount the valuation to protect themselves.

Customer concentration is another common issue. A supply business that depends too heavily on a few contractors, developers, or project relationships can lose value fast because future revenue looks fragile. The same is true for supplier concentration. If one key supplier drives too much of your gross profit, buyers will worry about renegotiation risk.

Founder dependence is also a real discount. If you personally own the customer relationships, the supplier relationships, the pricing decisions, and the operating rhythm of the company, a buyer may still want the business, but they are less likely to stretch on price. They are buying future earnings, not your personal heroics.

In this sector, weak branch economics can also hurt valuation. Buyers often analyze contribution by branch, region, and salesperson. If parts of the footprint look unproductive, or if growth has come through underperforming locations that soak up working capital, value can slip quickly.

Finally, poor inventory management is one of the easiest ways to lose credibility in a supply business sale. Too much dead stock, weak forecasting, and constant working capital surprises tell buyers the business is not as controlled as it should be.

7. Valuation Example: A Building Materials Supply Company

To make the logic tangible, let’s use a fictional company called NorthPeak Building Supply. This company is entirely made up for illustration, and so is the revenue figure. The goal is simply to show how buyers might frame valuation for a private business in this sector.

Assume NorthPeak has USD 10m of annual revenue. It focuses on specialty insulation, exterior envelope products, and related accessories sold to regional contractors and installers. It has decent gross margins, a repeat customer base, and two branches in one strong metro region.

Step 1: Build the valuation logic

The first step is to pick the right comparison set. For a Building Materials Supply business, the most relevant reference points are usually:

- private deals in trade supply, specialty distribution, and adjacent value-added building products

- public distribution and building materials companies that reflect the broader sector

- an EBITDA-based cross-check if margins are strong enough to matter

The source data suggests a useful baseline. Public mixed manufacturing and distribution profiles can sit around roughly 0.9x-1.1x revenue in a mature, diversified context, while ordinary private supply and merchanting deals are often below that. Better specialty distribution assets can move above the plain merchant range, especially if they show strong gross profit quality, recurring contractor relationships, and operational discipline.

So for a private company like NorthPeak, the right approach is not to copy a public multiple directly. It is to start with a core private-market range, then move up or down based on company-specific strengths and weaknesses.

Step 2: Apply the logic to the fictional company

Let’s assume NorthPeak has the following profile:

- USD 10m revenue

- solid but not exceptional growth

- healthy specialty product mix

- diversified contractor base

- reasonable margins

- moderate founder involvement

That profile probably does not deserve a premium outlier multiple. But it also should not be treated like a generic commodity merchant if the economics are better than average.

What could justify the discounted case?

A lower result could make sense if NorthPeak had weak margins, too much founder dependence, limited customer diversity, inconsistent reporting, or too much commodity product exposure. In that case, a buyer may treat it more like a straightforward merchanting business and stay close to lower-end private comps.

What could justify the base case?

The base case fits a solid specialty supply business with reasonable customer retention, good service reputation, stable gross profit, and no major red flags. This is where many good privately held businesses in the sector would likely sit.

What could justify the premium case?

A premium outcome would require more than nice revenue. NorthPeak would need stronger proof of defensibility - perhaps unusually sticky contractor accounts, superior branch economics, high service reliability, exclusive supplier relationships, clear room for add-on acquisitions, or a product mix tied to building performance and energy efficiency. In a competitive process, those features can push buyers above standard ranges.

The main lesson is simple: two USD 10m businesses in the same sector can be worth very different amounts. Revenue starts the conversation. Business quality decides where it ends.

This is not investment advice or a formal valuation. It is an illustrative example designed to show how valuation logic works in practice.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple self-assessment can help you estimate whether your business is currently closer to the low, middle, or high end of the valuation spectrum. Score each factor as:

- 0 = weak

- 1 = acceptable

- 2 = strong

Be honest. The point is not to flatter yourself. The point is to see where improvement has the biggest payoff.

How to interpret your score

If most of your scores are 2s, you are likely closer to the premium end of the realistic market range for this sector. That does not guarantee a premium multiple, but it means buyers should see a strong story.

If you are mostly 1s, you probably look like a fair market business - good enough to sell, but with room to improve value through better preparation, cleaner reporting, and sharper positioning.

If you have many 0s, you are more likely to be valued as a lower-quality supply business unless the buyer sees very unusual strategic value. That does not mean you should not sell. It means there may be a lot to gain from 6-12 months of focused improvement.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often spend years building the business and only a few weeks preparing for sale. That is backwards. If your numbers are not organized, your margin story is unclear, and your risks are not framed properly, buyers will assume the worst and price accordingly.

Another major mistake is hiding problems. If there is customer concentration, margin pressure, dead stock, an ERP issue, a branch that underperforms, or a supplier relationship that needs explanation, it is far better to frame it early and honestly. These issues almost always surface in due diligence anyway. When a buyer discovers a problem you tried to hide, trust drops and value usually drops with it.

Weak financial records also hurt value more than many founders expect. In this sector, buyers want clear revenue by category, branch, and customer type. They want gross margin visibility, working capital clarity, and a clean bridge from reported earnings to real cash generation. If that reporting is poor, the buyer has to guess - and buyers guess conservatively.

A fourth mistake is running an unstructured process without an advisor. A structured, competitive sale process with a capable advisor usually increases competitive tension, sharpens the positioning, and improves terms. Research commonly shows that advisor-led competitive processes can drive meaningfully higher outcomes, often around 25% higher purchase prices than less structured processes. That does not mean every process will produce that uplift, but it does show the power of real competition.

Another common error is telling buyers the price you want too early. If you say you are looking for USD 10m of enterprise value, buyers will often anchor around that number and come back with offers like USD 10.1m or USD 10.2m instead of revealing what they might have paid otherwise. You kill price discovery when you do the buyer’s job for them.

There are also sector-specific mistakes. One is neglecting inventory quality before a sale. If your stock is bloated, slow-moving, or poorly categorized, buyers may effectively reduce value through working capital adjustments or a lower headline price. Another is failing to explain branch performance properly. In supply businesses, one weak branch can overshadow a lot of good work if the story is not framed clearly and credibly.

10. What Building Materials Supply Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work usually falls into three buckets: improve the numbers, improve the story, and reduce buyer risk.

10.1 Improve the numbers buyers care about

Start with gross margin and branch profitability. In this sector, even modest gains in pricing discipline, mix, freight recovery, purchasing terms, and salesforce focus can make a real difference. Buyers respond well when they see that margin improvement is already happening, not just promised.

Tighten working capital too. Reduce dead stock, improve purchasing accuracy, and clean up inventory reporting. A buyer will notice quickly if the balance sheet is more controlled and cash conversion is improving.

If there are obvious low-hanging fruit areas - weak SKUs, poor branch productivity, underpriced accounts, messy rebates - fix them now. Six months of visible improvement is better than a management slide claiming future upside.

10.2 Improve the narrative and positioning

You need a simple, believable answer to one question: why is your business better than a generic merchant? If the answer is not obvious today, work on it. Sharpen your specialty positioning, segment your customers better, and show where your team adds real value beyond product supply.

Document your customer retention, repeat revenue patterns, service performance, and sales by category. If you can prove that the business has stable contractor relationships and earns trust in technical or time-sensitive categories, you move closer to the better businesses in the market.

Also make your growth story practical. Buyers trust specific plans more than big claims. A credible story might be new branches in adjacent counties, adding complementary categories, deepening wallet share with existing contractors, or improving project conversion rates.

10.3 Reduce founder dependence

If too much runs through you, start transferring relationships and decision-making now. Introduce customers and suppliers more formally to your leadership team. Clarify who owns pricing, who runs operations, and who manages branch performance.

A business that can keep running smoothly after you leave is always worth more than one that cannot. This is one of the most important changes founders can make before a sale.

10.4 Prepare diligence before the buyer asks

Get your financials, contracts, inventory data, and branch reporting in shape before launch. Create clean monthly reporting packs. Reconcile unusual expenses. Separate personal or one-time items from true business earnings.

If there are risks, prepare the explanation and the evidence. Buyers do not expect perfection. They do expect preparation.

10.5 Build competitive tension

The strongest valuation outcomes usually happen when several qualified buyers see the asset at the same time. That means you should identify a broad but relevant buyer universe - strategics, regional consolidators, specialty platforms, and private equity-backed acquirers that understand the sector.

A competitive process is not just about getting more bids. It is about finding the buyer who sees the most strategic value in your specific mix, geography, customer base, and operating footprint.

11. How an AI-Native M&A Advisor Helps

Selling a Building Materials Supply business is partly about valuation math, but a large part of the outcome comes from process quality. The best buyers are not always the most obvious ones, and the highest price often comes from the buyer who sees the strongest strategic fit.

An AI-native M&A advisor helps by expanding the buyer universe far beyond the usual shortlist. Instead of contacting only a limited set of familiar names, AI can identify hundreds of qualified acquirers based on deal history, synergies, financial capacity, geographic logic, and category fit. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal actually closes if one buyer drops out.

It also makes the process faster. With AI-driven buyer matching, outreach support, marketing material creation, and diligence preparation, initial conversations and offers can often be reached in under 6 weeks. That speed matters when market conditions are shifting or when founder momentum is high.

Just as importantly, AI works best when paired with experienced human advisors. You still need expert judgment, sharp negotiation, and credible positioning with acquirers. The advantage is that AI helps those advisors work broader, faster, and with better information - giving you Wall Street-grade advisory quality without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.