The Complete Valuation Playbook for Business Intelligence Companies

A practical guide to how Business Intelligence companies are valued today and what drives high multiples.

If you run a Business Intelligence business and are thinking about selling in the next 1-12 months, valuation is not just about revenue size. In this sector, two companies with the same top line can attract very different prices depending on what sits underneath that revenue - recurring software, custom analytics work, proprietary data, workflow integration, customer stickiness, and how much the business still depends on you.

This matters more now because buyer appetite has become more selective. Strategic buyers still want data, analytics, and AI capabilities, but they are paying up for assets that are embedded in real workflows, have clean revenue quality, and can scale without adding people in lockstep. At the same time, private equity buyers are more disciplined than they were a few years ago.

This playbook is built to help you see what BI businesses actually sell for, what drives higher versus lower multiples, where your company may fit, and what you can do over the next 6-12 months to improve the outcome.

1. What Makes Business Intelligence Businesses Unique

Business Intelligence is a broad label, and that is exactly why valuation can get messy. In this market, buyers may look at you as one of several different business types: a horizontal analytics platform, a vertical insights provider, a data enablement software business, a subscription research platform, or a services-heavy analytics consultancy. Those are not valued the same way.

The biggest valuation question is usually this: are you really a software and data platform, or are you still partly a people-powered analytics business? Many BI companies sit somewhere in the middle. They may sell dashboards, reports, models, and data products, but still rely heavily on custom projects, implementation work, or founder-led interpretation. Buyers spend a lot of time figuring out which side of that line you are on.

Another sector-specific issue is that BI value often depends on where you sit in the customer workflow. A reporting tool that people check occasionally is usually worth less than a platform that helps decide pricing, sales activity, customer targeting, risk, inventory, or budgeting every day. The closer your product is to an operational decision, the more strategic it becomes.

Buyers also focus hard on data rights, integration depth, and proof that your insights are hard to replace. If your product depends on third-party data you do not control, or on fragile integrations, that can lower value fast. If you own or control unique data, have strong governance and compliance features, and are woven into systems like CRM, ERP, or marketing infrastructure, buyers usually see a stronger moat.

2. What Buyers Look For in a Business Intelligence Business

At the most basic level, buyers care about the same things they care about in any software or tech-enabled business: revenue scale, growth, margins, customer retention, and quality of earnings. But in BI, they also want to know whether your product is truly part of how customers operate, or whether it is nice to have.

They will look closely at recurring revenue. A BI business with annual subscriptions, multi-year enterprise contracts, strong renewal rates, and predictable upsell is much easier to underwrite than one that depends on project work or irregular data studies. Buyers care about whether your customers stick around and pay more over time.

They also care about gross margin, but not in isolation. Your source data shows a useful warning: high reported gross margins do not automatically produce high multiples. Buyers look past headline margins and ask whether the revenue is really productized, repeatable, and scalable. If your margin looks software-like but the delivery still depends on analysts, data engineers, or founders doing custom work, they may still price you like a hybrid business.

Another major issue is customer profile. Enterprise buyers often pay more for customers that are sticky, hard to win, and expensive for competitors to displace. But they also worry about concentration. If one or two customers drive too much revenue, or if a small number of contracts are up for renewal soon, that can reduce price or increase the earnout.

How private equity buyers think about it

Private equity buyers usually start with the entry multiple and ask themselves a simple question: if they buy your business today, who can they sell it to in 3-7 years, and at what kind of multiple? That future buyer could be a larger software company, a bigger private equity fund, or in rare cases the public market.

They also look for levers they can pull after acquisition. In BI, that often means pricing improvements, more disciplined sales, cross-sell into adjacent data products, international expansion, tuck-in acquisitions, and reducing delivery costs by productizing work that is still done manually today.

If you are talking to private equity, they are not just buying your current business. They are buying a future version of it. The more clearly you can show how the business becomes more recurring, more embedded, and less dependent on custom services, the more attractive you become.

3. Deep Dive: Productized, Embedded BI vs Services-Heavy Analytics

This is one of the biggest valuation dividing lines in the BI market. Many founders describe their company as a software platform, but buyers look deeper. They ask how much of the customer value comes from the product itself and how much still comes from human effort around the product.

Your deal data supports this divide. The highest private multiples in the set tend to show up where the target is tightly adjacent to a larger platform, is clearly software-led, or has a governance or enablement layer that feels strategic. Lower or more mixed outcomes often show up where revenue looks more services-led, less repeatable, or harder to scale cleanly.

Why do buyers care so much? Because productized, embedded BI is easier to grow without adding headcount at the same rate. It is usually easier to cross-sell, easier to retain, and harder for the customer to rip out. A dashboarding layer alone can be replaced. A BI platform tied into CRM, ERP, customer engagement, cataloging, governance, lineage, or decision workflows is much harder to dislodge.

Founders can usually move their business in the right direction over time. That does not mean reinventing the company in six months. It means turning custom deliverables into standard modules, reducing one-off work, packaging your best insights into repeatable products, and proving that customers are buying the platform - not just your team.

If your business looks more like the left column today, the good news is that buyers will still care if the market need is real. But they are more likely to structure value through earnouts, milestone payments, or a lower upfront multiple.

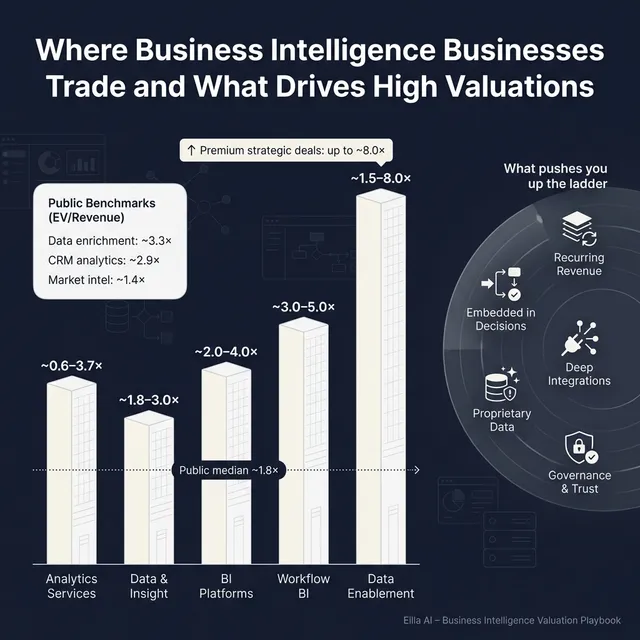

4. What Business Intelligence Businesses Sell For - and What Public Markets Show

Here is the cleanest way to read the market: private deals in this space show a wide spread because BI covers very different business models, and public market trading sets a reference band rather than a direct price tag. The right multiple for your business depends on where you sit between software, data asset, workflow tool, and services.

The overall precedent transaction set in your source data averages about 3.9x EV/Revenue with a 3.0x median, and about 11.4x EV/EBITDA with an 11.8x median. The public comp set is much wider, with an overall average of 5.8x EV/Revenue but a median of only 1.8x, which tells you a few very highly valued names are pulling the average up. For founders, that means the median often tells the more realistic story.

4.1 Private Market Deals (Similar Acquisitions)

The private market data suggests that most BI-style businesses do not sell on one universal “sector multiple.” Instead, buyers sort them into deal types. Vertical data and insights platforms tend to trade in the low-to-mid revenue multiple range. Enterprise data enablement assets can reach much higher levels when the product has strategic adjacency to a larger platform. Services-led analytics businesses can trade anywhere from low multiples to solid EBITDA-based outcomes depending on profitability and scale.

A good practical reading of your source set is this: if your business is early-stage, mixed software and services, and lacks strong proof on retention or scale, buyers are more likely to anchor toward the low end of the range. If it is productized, strategically embedded, and useful to a larger acquirer’s distribution or data stack, it can move toward the top end.

These ranges are illustrative, not promises. A small BI company with real software economics can beat a larger but more services-heavy business. The reverse is also true.

4.2 Public Companies

Public comps are useful, but only if you use them correctly. As of mid to late 2025, the most relevant public segments around BI show clear differences in how the market rewards business models.

Commercial data enrichment and decisioning businesses traded around 3.3x average EV/Revenue and 3.2x median, with EV/EBITDA around 16x on average. Market intelligence and subscription research platforms sat lower, around 1.4x EV/Revenue on average in this data set. CDP and AI marketing cloud businesses were around 3.1x average EV/Revenue, while CRM and customer interaction analytics platforms were around 2.9x average EV/Revenue, though EBITDA multiples in those groups were heavily skewed by scale and market leadership.

The horizontal BI and AI platform bucket is the hardest one to use at face value. In your data, the median is only about 2.4x EV/Revenue, but the average jumps to roughly 19.5x because a few outliers trade at extremely rich levels. That is why small private BI companies should be very careful about pointing to top-decile AI names as direct benchmarks.

The right way to use public multiples is as a reference band, not a price tag. Smaller private companies are usually adjusted downward for lower scale, thinner management depth, less liquidity, and more customer risk. But a scarce, highly strategic asset can still punch above the median if the buyer sees clear strategic value.

5. What Drives High Valuations (Premium Valuation Drivers)

5.1 Deep strategic adjacency

One of the clearest patterns in your source data is that buyers pay more when the target strengthens their core platform or distribution. If your BI product makes a larger acquirer’s CRM, commerce stack, enterprise data platform, or services channel more valuable, you become more than a standalone tool.

In practice, this means buyers care less about “we integrate with major systems” and more about “we drive pull-through inside those systems.” If your product helps a larger platform win more customers, retain them longer, or sell more modules, that can materially improve valuation.

5.2 Productized recurring revenue

Premium businesses in this market do not just sell insights. They sell repeatable access, workflow, and outcomes. Buyers pay more for subscription revenue that renews, expands, and does not need a fresh custom project every quarter.

A founder-friendly test is simple: if a customer stopped asking for custom work, would they still keep paying because the core product is useful on its own? The more the answer is yes, the stronger your valuation profile.

5.3 Governance, compliance, and trust layers

The source data shows that governance-style capabilities can create strategic scarcity. Metadata, lineage, clean-room style collaboration, privacy controls, and data compliance features matter because they sit in the critical path of enterprise data use.

That matters especially in BI because buyers know data access alone is not enough. A platform that helps customers use data safely, document it, share it correctly, and trust it tends to be harder to replace than a pure visualization or analytics layer.

5.4 Operating leverage and real EBITDA conversion

Some of the strongest outcomes in your private comp set are not the highest revenue multiples - they are the best EBITDA multiples. That tells you something important: buyers pay up when they believe earnings are durable and scalable.

If your BI business is already converting revenue into healthy EBITDA, buyers can underwrite near-term cash generation. That can support a better price even if your revenue multiple is not flashy. In plain English: profitability still matters.

5.5 Scale and enterprise serviceability

Buyers are more comfortable paying larger checks when they believe the business can serve bigger customers without breaking. A multi-geo footprint, a stronger delivery engine, and a credible leadership bench can all help.

This does not mean you need to be huge. It means you need to show that growth does not rely on heroic founder effort or on hiring analysts one by one just to deliver more revenue.

5.6 Proprietary data, measurable ROI, and real stickiness

If your product is powered by data that competitors cannot easily copy, and customers can see measurable value from using it, that strengthens your hand. Proprietary data alone is not enough. Buyers want to know it actually improves decisions and that customers renew because of it.

The best version of this is simple: your customers use your product regularly, it changes how they make decisions, and churn is low because replacing you would be painful.

5.7 Clean company building basics

Founders sometimes overlook this because it feels less strategic, but buyers absolutely care. Clean financials, clear KPI reporting, diversified customers, documented data rights, and a management team that is not overly dependent on one founder all support higher valuations because they reduce risk.

6. Discount Drivers (What Lowers Multiples)

The biggest discount driver in BI is revenue that looks like software on the surface but behaves like services underneath. If you have high gross margins but still rely on custom dashboards, consulting-heavy implementations, or manual insight delivery, buyers may discount the story.

Another common issue is weak proof of revenue quality. If you cannot clearly show retention, expansion, contract structure, renewal timing, or product usage, buyers get cautious. In this market, uncertainty usually leads to lower upfront price, more earnouts, or both.

Customer concentration can also hurt. If one or two accounts represent a large share of revenue, or if your biggest clients are on short contracts, buyers will worry about post-close leakage. The same goes for concentration in a single end market if that market is volatile.

In BI, data provenance matters. If your data rights are unclear, your key data sources are licensed on weak terms, or your integrations depend on fragile partner relationships, buyers will mark that risk directly into value.

Other common discount drivers include:

- Heavy founder dependence in sales, product, or customer relationships

- AI claims without clear product adoption or commercial proof

- Weak profitability or no path to operating leverage

- Messy revenue recognition or poor segment reporting

- A large implementation burden that slows new customer rollout

- High employee dependency in delivery or data science teams

The good news is that many of these are fixable. A lower multiple is often not a verdict on the business. It is a reflection of risks the buyer thinks they will have to solve after closing.

7. Valuation Example: A Fictional Business Intelligence Company

Let’s make this practical. Suppose you run a fictional company called SignalForge, a BI platform that helps mid-market and enterprise customers combine internal sales data, external market signals, and customer activity data to guide pricing, demand planning, and commercial decisions.

Assume SignalForge has USD 10m of annual revenue. This company is fictional, and the valuation below is illustrative only. It is not investment advice and not a formal valuation.

Step 1: How to think about the range

The most defensible starting point from your source data is a 2.0x-5.0x EV/Revenue range for a BI business of this size. That comes from triangulating:

- Relevant public reference bands in data enrichment, CRM and customer engagement, and adjacent AI/data software

- Private precedent deals in vertical data and enterprise data enablement

- A downward adjustment for private-company size, liquidity, and execution risk

- An upward adjustment only where there is real proof of strategic value, not just a good story

In other words, you do not start by asking, “What is the highest multiple in the market?” You start by asking, “Which buyer buckets and comp groups genuinely resemble my business?”

Step 2: Apply the logic

Let’s assume SignalForge has these traits:

- 75% recurring subscription revenue

- 25% implementation and custom analytics revenue

- Strong integrations into CRM and ERP

- Good gross margin

- Healthy retention, but not yet elite

- Mid-single-digit EBITDA margin

- No major customer concentration

That profile is better than a services-heavy BI firm, but not yet a top-decile software asset.

What would push it down?

SignalForge would drift toward USD 20-25m if the custom work proved harder to separate from the product, if retention was patchy, if a few customers drove too much revenue, or if data rights and integrations were not well documented.

What would support the core to upper range?

It would move toward USD 30-45m if the recurring product was clearly the main value driver, the integrations were hard to replace, churn was low, and the company could show a credible path to stronger operating leverage.

What would justify the premium end?

To push toward USD 50m, you would usually want several things at once: strong workflow embedding, real strategic fit for a larger buyer, clear product pull-through, clean revenue quality, and evidence that the company is more platform than project business.

The key lesson for founders is simple: two BI businesses with the same USD 10m of revenue can be worth very different amounts. Revenue size matters, but revenue quality matters more.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as a practical scoring tool. Give yourself a score of 0, 1, or 2 on each line. Be honest. The point is not to flatter yourself - it is to see which improvements could move valuation the most.

A rough way to read the score:

- 18-24: You are closer to premium territory. Buyers are more likely to see you as a strategic asset.

- 11-17: You are in fair-market range. A good process matters a lot.

- 0-10: There is probably real value in the business, but more work is needed before you should expect top-of-range outcomes.

The biggest value of this exercise is not the score itself. It is seeing which two or three factors are most likely to change buyer perception.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. If your numbers are not ready, your story is unclear, and your buyer list is thin, you usually leave money on the table. A rushed process makes buyers feel they have leverage.

The second is hiding problems. In deals, issues almost always come out in diligence. If you try to bury churn, customer concentration, messy financials, weak data rights, or delivery dependence, you usually do not save the valuation - you damage trust. That can hurt the price far more than the problem itself.

The third is weak financial records. If you cannot clearly separate subscription revenue from services, show gross margin by segment, explain EBITDA adjustments, and track KPIs like churn, pipeline conversion, contract value, and customer cohort behavior, buyers will struggle to underwrite the business. That usually means a lower price or more contingent consideration.

The fourth is not running a structured, competitive sale process with an advisor. Research often shows that a structured competitive process with an advisor can improve purchase prices by around 25% because more buyers are brought in, the story is framed better, and price tension is created.

The fifth is telling buyers what price you want too early. If you say you are looking for USD 10m of value, do not be surprised if offers come back at USD 10.1m or USD 10.2m. You kill price discovery when you anchor the number before the market has shown its hand.

Two BI-specific mistakes are especially common:

- Selling the AI story before proving the BI value. Buyers want proof that customers use the product and pay for it, not just that you have models.

- Failing to document data ownership, licensing, and usage rights. In a BI deal, this can become a major diligence issue very quickly.

10. What Business Intelligence Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers actually care about

Increase the share of recurring revenue. If part of your business is still custom reporting or project work, see what can be converted into subscription modules, standard data products, or recurring service packages.

Tighten margin reporting. Break out product revenue, services revenue, gross margin by line, and the true cost to deliver custom work. This helps buyers see the software core more clearly.

Focus on retention. Reducing churn, expanding within existing accounts, and improving contract visibility can do more for valuation than adding a few low-quality new logos.

Make the product more embedded

Deepen integrations into the systems your customers already use. BI platforms that sit inside CRM, ERP, marketing, finance, or operational workflows usually command more interest than standalone analytics tools.

Turn repeated customer requests into product features. If your team keeps solving the same problem manually, productize it. That moves you away from labor-heavy delivery and toward software economics.

Show measurable business outcomes. Case studies should not just say customers “like the dashboard.” They should show better pricing, improved conversion, faster decisions, reduced churn, better forecasting, or lower customer acquisition cost.

Reduce risk before buyers find it

Document data rights, contracts, compliance practices, and security processes. If your value depends on external data, make sure the chain of rights is clear and durable.

Reduce customer concentration where possible. Even modest diversification before a process can change buyer confidence.

Build management depth. If everything runs through you, buyers will worry about transition risk. Shifting key relationships and processes to a broader team helps.

Improve sale readiness

Prepare a clean KPI pack. Buyers want to see revenue by product, recurring versus non-recurring mix, churn, expansion, customer concentration, pipeline quality, and margin trends.

Build the buyer narrative early. Do not wait until the process starts to figure out whether you are selling software, data, workflow, or strategic adjacency. That framing matters.

Run a real process. The right buyers for a BI business are often broader than founders expect - software strategics, data platform consolidators, consultancies, private equity-backed platforms, and adjacent workflow players may all care for different reasons.

11. How an AI-Native M&A Advisor Helps

A modern sale process is partly about advice and partly about reach. An AI-native M&A advisor can expand the buyer universe far beyond the usual short list by identifying hundreds of qualified acquirers based on deal history, strategic fit, synergies, and financial capacity. More relevant buyers creates more competition, better offers, and a higher chance the deal closes if one buyer drops out.

It can also make the process faster. With AI helping match buyers, prepare marketing materials, support diligence, and keep the process moving, initial buyer conversations and offers can often be reached in under 6 weeks instead of dragging on through a slow manual process.

That does not replace human advice. It improves it. The best outcome comes from experienced M&A advisors using AI to strengthen buyer targeting, sharpen positioning, and present your business in the language serious acquirers care about. The result is Wall Street-grade advisory quality without the traditional bulge-bracket cost structure.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.