The Complete Valuation Playbook for Cloud Infrastructure Businesses

A guide to how cloud infrastructure businesses are valued today - and what founders can do in the next 6-12 months to move toward the top of the range.

If you run a cloud infrastructure business, the next 1-12 months could be a pivotal time to think about valuation. The market is consolidating: hyperscalers are everywhere, AI/GPU demand is exploding, and security and sovereignty requirements are tightening. At the same time, strategic buyers and private equity funds are actively building platforms across IaaS, MSPs, security, backup and data centers.

This guide is designed to help you, as a founder or CEO, understand how buyers actually think about valuing cloud infrastructure companies - using real transaction data and public market benchmarks from your own sector.

We will walk through:

- What cloud infrastructure businesses like yours actually sell for.

- What drives higher versus lower revenue multiples in this space.

- A worked 10m revenue valuation example.

- A self-assessment framework and 6-12 month action plan to move your business toward the top of the range.

1. What Makes Cloud Infrastructure Unique

Cloud infrastructure is not one uniform category. Most businesses fall into one or more of these buckets:

- Public IaaS/PaaS cloud platforms

- Example model: regional or specialist alternatives to hyperscalers, selling compute, storage, networking and managed Kubernetes.

- Managed cloud & IT services / MSPs with hybrid or private cloud

- Running, securing and supporting workloads on AWS/Azure/GCP, private clouds or hosted VMware.

- Regional cloud/data center builders and systems integrators

- Designing, building and sometimes operating data centers and private cloud stacks.

- Colocation and data center operators

- Long-term, space-and-power plus interconnect providers with REIT-like economics.

- Backup / DRaaS / data protection platforms

- Cloud backup and archiving for Microsoft 365, Google Workspace, servers and databases.

- Cloud infrastructure tooling and DevOps software

- Infrastructure-as-code, security, observability and automation platforms.

- Cloud-native engineering and Microsoft/Azure specialists

- Consulting and managed services focused on Azure, Kubernetes, GitOps, DevSecOps.

- AI/GPU cloud infrastructure providers

- GPU-heavy platforms optimized for AI/HPC workloads.

These models all sit under "cloud infrastructure", but valuation logic differs. Two big reasons this sector is unique:

- Heavy capex and long contracts in some segments

- Data centers and GPU clouds require large up-front investments, but often have long contracts and strong visibility.

- Buyers care a lot about how full your capacity is and how sticky those contracts are.

- Security, sovereignty and compliance are baked into value

- Sovereign-cloud and regulated-sector exposure can support higher EV/EBITDA multiples, around 11.8x and 17.7x respectively, even at modest size.

- Where your workloads live (and under what rules) matters as much as what you technically provide.

Key risk factors buyers will always check for cloud infrastructure:

- Concentration risk

- A few customers making up most of your revenue, or a single hyperscaler relationship that, if lost, would hurt badly.

- Commodity exposure

- Competing mainly on price for basic hosting or resell, with limited differentiation.

- Security and uptime

- Any material incidents, weak certifications, or poor SLAs can hit valuation quickly.

- Capex and utilization

- Overbuilt capacity with poor utilization, or unpredictable future capex needs, will reduce what buyers are willing to pay.

- Regulatory and data residency exposure

- Serving regulated sectors without clean compliance stories, or running cross-border setups that might be at odds with data laws.

2. What Buyers Look For in a Cloud Infrastructure Business

From the outside, it might seem like buyers simply pay a multiple of revenue or EBITDA. In reality, they are asking a more basic question:

"If we own this asset for the next 3-7 years, how much predictable cash can it generate, and how easily can we sell it on?"

The obvious levers (that still matter a lot)

- Scale of revenue

- Bigger businesses are usually worth higher multiples. A 50m revenue MSP often trades at a higher revenue multiple than a 5m one, even with similar margins.

- Growth rate

- Buyers compare your growth to peers. Growing 20-30 percent a year looks very different to flat or low single digits.

- Profitability and margins

- High-margin infrastructure platforms with strong operating leverage have historically commanded very significant valuation premiums relative to the broader market.

- Recurring and contracted revenue

- Multi-year managed services contracts, colocation, and DRaaS subscriptions are more valuable than one-off projects.

Cloud-infrastructure-specific nuances buyers drill into

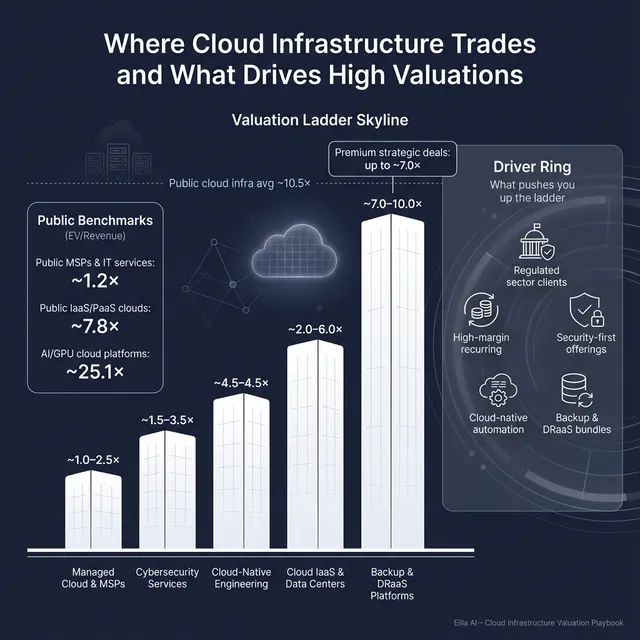

- Where you sit in the stack

- MSPs and IT outsourcing providers tend to transact around 1.0-2.0x revenue on average.

- Cloud IaaS and data center infrastructure deals average around 5.1x revenue, with a median of 2.8x, and can go much higher when scale and margins are strong.

- Backup and DRaaS platforms can command around 9.6x revenue because of highly recurring, stickier revenue.

- Security and sovereign posture

- Businesses operating in sovereign cloud and security for regulated sectors, show strong EV/EBITDA multiples in the low to high teens. This reflects trust, compliance and high switching costs.

- Cloud-native depth

- Cloud-native engineering firms achieved EV/Revenue around 4.8x and EV/EBITDA around 18x, even at relatively modest scale.

- Gross margin structure

- Cloud automation and infrastructure software providers with strong software-like gross margins often trade at a significant premium, even before profitability is reached.

- Contract quality and duration

- Long-term data center or managed services contracts, especially with good escalators, support higher valuation than short-term, easy-to-cancel engagements.

How private equity buyers think in this sector

Private equity (PE) buyers tend to have a structured playbook:

- Entry multiple vs exit multiple

- They ask: "If we buy this business at, say, 3.5x revenue, can we grow it and sell it at 5.0x or higher?"

- That often means looking for areas where your current valuation does not yet fully reflect your strategic profile - for example, strong security capabilities not yet packaged as high-margin managed services.

- Who they could sell to in 3-7 years

- Larger strategics rolling up cloud services.

- Larger PE funds building bigger platforms.

- Occasionally, public markets, though IPO is rare for smaller infra assets.

- Levers they expect to pull

- Pricing: tightening discounts and adding usage-based or value-based pricing.

- Cross-sell: attaching backup/DR, security or managed services across the existing customer base.

- Roll-ups: buying smaller MSPs or niche providers to add scale and expand geography.

- Cost efficiency: standardizing tooling, reducing vendor sprawl, and improving utilization of any owned infrastructure.

If your business clearly shows room for these levers - and clean data to back it up - PE will generally be more comfortable paying toward the upper end of the fair range.

3. Deep Dive: Sovereign, Security and Mission-Critical Cloud vs Commodity Hosting

One of the most powerful valuation nuances in cloud infrastructure today is how "sovereign and secure" your business is perceived to be versus "generic hosting or basic MSP work".

More generic IT services and MSP transactions typically cluster much lower, often between 0.8x and 2.0x revenue.

Why buyers care so much about sovereign and security posture

- Regulated customers are stickier

- Government and financial institutions face higher switching costs and long approval cycles.

- Once you clear their security and compliance hurdles, contracts can last many years.

- Pricing power

- When you are one of a small number of sovereign-eligible or high-compliance providers, you can charge more for the same raw compute or services.

- Lower downside risk

- High security and compliance standards reduce the risk of catastrophic incidents that can damage brand and value.

Moving from "commodity" to "mission-critical" profile

Most cloud infrastructure businesses can move along this spectrum over time.

Practical shifts include:

- From basic hosting to sovereign or regulated-ready services

- Obtain key certifications (ISO27001, SOC2, PCI, local government frameworks) and keep them front-and-center in your pitch.

- Specialize in sectors that genuinely value this - government, financial services, health, critical infrastructure.

- From ad-hoc security add-ons to security-first offerings

- Package managed detection and response, zero-trust designs, and security monitoring into core service tiers.

- Align service descriptions with regulated standards (for example, "OFFICIAL" or "PROTECTED" equivalent levels in your jurisdiction).

- From one-off projects to recurring, security-embedded services

- Turn successful security projects into managed services contracts.

- Bundle backup, DR and security into multi-year subscriptions, especially for Microsoft 365 and major SaaS estates.

A simple way to picture this:

If your business looks more like the left column today, you do not need to become a fully sovereign cloud provider in 6-12 months. But even modest moves toward regulated sectors, cleaner security packaging and more recurring security-embedded revenue can shift your multiple meaningfully.

4. What Cloud Infrastructure Businesses Sell For - and What Public Markets Show

In this section we anchor valuation expectations using real deal and trading data from across the cloud infrastructure landscape.

Think of this as your "data-based reality check" before you form any view on what your company might be worth.

4.1 Private Market Deals (Similar Acquisitions)

Across recent cloud infrastructure transactions, the overall average EV/Revenue multiple is around 3.1x, with a median also around 3.1x. But that average hides major differences by segment.

Using grouped transaction data:

- Managed Cloud Infrastructure & IT Outsourcing Providers

- Average EV/Revenue around 1.7x, median around 1.4x.

- Cloud IaaS & Data Center Infrastructure Providers

- Average EV/Revenue around 5.1x, median around 2.8x.

- Backup, DRaaS & Data Protection Platforms

- Average and median EV/Revenue around 9.6x (based largely on Dropsuite).

- This reflects high recurring revenue, MSP channel leverage and attachment to M365/Google estates.

- Cybersecurity Services & Managed Security Providers

- Average EV/Revenue around 2.9x, median around 1.9x.

- Cloud Infrastructure Tooling & DevOps Software

- Average EV/Revenue around 4.1x, median around 2.3x.

- Cloud-Native Engineering & Microsoft/Azure Specialists

- Average EV/Revenue around 2.1x, median around 1.5x.

- Telecom & Connectivity with Cloud/IT Services

- Average and median EV/Revenue around 1.8x.

You can summarize the private market picture roughly like this:

These are illustrative ranges, not promises. Where your business sits inside (or outside) these bands will depend on your specific mix of revenue, margins, security posture and contracts.

4.2 Public Companies

Public markets offer another reference point - especially for segment leaders. Across the sample of public cloud infrastructure-related companies (as of 2025), the overall average and median EV/Revenue are around 10.5x, and EV/EBITDA around 21.2x. Again, segment differences matter:

*Colocation average revenue multiple is pulled up by extreme outliers. Median closer to 10x is a better reference.

Again, the pattern is clear:

- MSPs and multi-cloud IT services trade near 1-2x revenue.

- Independent cloud platforms and regional data center plays trade in the mid-single-digit revenue multiples for solid names.

- AI/GPU and security-focused infra software can command double-digit revenue multiples, but this is reserved for rare profiles.

For private companies, buyers typically:

- Use public multiples as an upper bound (you are smaller, less liquid, and usually riskier than a large listed peer).

- Apply discounts for scale, growth, private-company risk, and customer concentration.

- Sometimes pay close to public multiples or above for scarce, highly strategic assets (sovereign cloud, unique GPU capacity, or must-have security capabilities).

5. What Drives High Valuations (Premium Valuation Drivers)

Let’s turn the data into a practical checklist of what moves you toward the top of the range.

a) Sovereign cloud and regulated-sector exposure

- Sovereign cloud and security-focused providers serving government and regulated sectors have achieved higher EV/EBITDA multiples, often in the low to high teens, even at relatively modest scale.

- Why buyers pay more:

- Higher trust bar to enter.

- Heavier switching costs.

- Stronger pricing power and longer contracts.

What you can do:

- Build and advertise concrete certifications and accreditations.

- Codify your regulated vertical focus (for example, "public sector and financial services" rather than "everyone").

- Make sure referenceable customers are front-and-center in your materials.

b) Data protection, backup and DRaaS, especially around Microsoft 365

Why this drives premiums:

- Backup and DRaaS are mission-critical, not optional extras.

- When embedded via MSPs and partners, they tend to drive high retention and low churn.

- They scale well - once built and integrated, they can be rolled out across many customers.

Practical moves:

- Standardize a "secure M365" or "secure SaaS" bundle that includes backup, DR and security monitoring.

- Track and improve attachment rates and retention for these products.

- Make backup/DRaaS a core pillar of your value proposition, not just a line item.

c) Cloud-native engineering, DevSecOps and GitOps maturity

Some deals show that deep cloud-native skills can materially lift multiples:

- These capabilities deliver repeatable, standardized deployments across many clients.

- DevSecOps and GitOps practices reduce risk and improve governance, which is highly valued in regulated and enterprise contexts.

- They open the door to higher-margin managed services layered on top.

Practical moves:

- Invest in internal tooling and automation (IaC, GitOps) and make them part of your pitch.

- Package "reference architectures" for your target verticals and clouds.

- Highlight and document your DevSecOps pipeline in buyer materials.

d) High gross margins from software-like services and scaled infrastructure

Why this matters:

- High gross margin businesses have more room to invest in sales, R&D and acquisitions.

- Buyers see clearer operating leverage - as you grow, profits should scale faster than revenue.

Practical moves:

- Understand and optimize your gross margin by product, customer and segment.

- Move low-margin, project-heavy work into standardized, higher-margin managed services where possible.

- Avoid discounting that permanently compresses margins without strategic benefit.

e) Security-led consolidation, earn-outs and growth weighting

Several security-led and cloud-native platform acquisitions share common features:

- Significant earn-out components tied to future EBITDA and revenue growth.

- Strong security or cloud-native capabilities that a larger platform can cross-sell into its base.

Why this supports premiums:

- Earn-outs let buyers pay for upside if you deliver growth, rather than overpaying today.

- Security and cloud-native skills are valuable glue for a broader cloud modernization offering.

What this means for you:

- If you have genuine growth headroom, a deal structure with earn-outs can increase headline valuation.

- To make this credible, you need clear growth plans, pipeline visibility and KPIs that buyers trust.

f) Clean financials, diversified customers and a strong second line of leadership

Even if not always highlighted in data tables, these standard M&A hygiene factors still drive where you land within the range:

- Well-prepared, accurate financials with clear revenue splits (recurring vs project, by product, by vertical).

- No single customer accounting for a dangerously high share of revenue.

- Leadership bench beyond the founder, with people who can run operations post-deal.

These factors often determine whether a buyer feels comfortable leaning into the higher end of what the numbers would justify.

6. Discount Drivers (What Lowers Multiples)

Now the uncomfortable but important part: why some cloud infrastructure businesses transact at the low end - or below - the headline multiples.

Common discount drivers include:

Structural and commercial issues

- Low recurring revenue and project-heavy mix

- If most of your revenue is one-off implementations or hardware pass-through, buyers will discount heavily.

- Customer concentration

- If one or two customers make up a large share of revenue, buyers will assume higher risk and lower your multiple.

- Low or slowing growth

- Growing at 3-5 percent in a market where peers grow 15-30 percent will pull you toward the bottom of the range.

- Commodity positioning

- If your pitch is mainly price and basic hosting or resell, with little differentiation, you will be compared to the lowest-multiple MSPs and IT services players.

Financial quality and margin issues

- Weak or volatile gross margins

- Poor pricing discipline, too much low-margin hardware, or heavy discounting can push you toward MSP-style 1x revenue multiples or below.

- Messy books and unclear KPIs

- If EBITDA and cash flow are hard to reconcile, or you cannot clearly show churn and retention, buyers assume the worst.

- Hidden capex needs

- A big upcoming data center build, or major hardware refresh not reflected in projections, will reduce what they pay.

Risk and governance

- Security or uptime problems

- Any serious security incident or repeated SLA breaches can be a major red flag.

- Key-person dependence

- If everything runs through you personally, buyers will worry about post-deal execution.

- Weak contracts

- Short-term, easily cancellable engagements with limited auto-renew or price rise mechanisms will hurt valuation.

Process and market exposure

- Limited buyer universe

- Quietly negotiating with one or two buyers reduces competitive tension.

- Unstructured sale process

- Poor materials, slow responses, and incomplete data rooms cause buyers to lower bids or walk away.

The important thing: almost all of these are at least partially fixable over 6-12 months if you focus on them deliberately.

7. Valuation Example: A Cloud Infrastructure Company

To make this concrete, let’s walk through a fictional example.

Meet "AtlasCloud" (fictional)

- Business model: regional cloud infrastructure provider offering managed private cloud, backup/DR, and security services, with some GPU capacity.

- Customers: mid-market enterprises and public-sector entities in one region.

- Revenue: USD 10m annual run rate (fictional).

- Profile: 70 percent recurring revenue, 20 percent year-on-year growth, EBITDA margin around 15 percent.

AtlasCloud is a composite example designed to show the logic - it is not based on a single real company, and the valuation numbers below are illustrative, not advice or a formal fairness opinion.

Step 1: Using market data to build a sensible multiple range

From the data:

- MSPs and managed cloud services often transact around 1.0-2.5x revenue.

- Regional cloud and data center plays sit roughly in the 2.0-6.0x band, with outliers like QTS much higher at scale.

- Backup/DRaaS players can reach 7.0-10.0x.

- Public MSPs trade around 1.2x revenue on average; public IaaS/PaaS platforms around 7.8x.

AtlasCloud sits somewhere between a managed cloud/MSP and a regional cloud/backup provider, with some security and sovereign flavor.

A realistic starting point:

- Base services band: 2.0-3.5x revenue (reflecting MSP plus regional cloud profile).

- Premium adjustments for:

- Sovereign/regulated customers.

- Embedded backup/DR and security.

- Healthy growth and margin.

This might support shifting the range up by about 0.5-1.0x, giving:

- Adjusted core range: 2.5-4.5x revenue.

We also keep in mind an upper sensitivity case if AtlasCloud is truly scarce in its region (for example, the only sovereign-capable provider with strong GPU and DRaaS at scale), where a strategic buyer might stretch toward 6.0-7.0x. That’s high, but within what we’ve seen for rare assets in backup and security-led infrastructure.

Step 2: Apply multiples to AtlasCloud’s USD 10m revenue

Now apply this to the fictional USD 10m revenue:

How you might interpret this:

- Discounted case (around 2.0x)

- Maybe AtlasCloud’s growth slows, customer concentration is high, or due diligence uncovers gaps in security documentation or financial quality.

- Core range (2.5-4.5x, USD 25-45m)

- Represents a well-run regional cloud/MSP with decent growth, mostly recurring revenue and some regulated customers, but no extreme scarcity or scale.

- Premium scenario (6.0-7.0x, up to USD 70m)

- Could be justified if:

- A strategic buyer sees AtlasCloud as the missing sovereign node in a key region.

- Backup/DRaaS represents a large portion of revenue with very low churn.

- Contracts are long-term and margins are strong.

- Could be justified if:

The important takeaway: two cloud infrastructure businesses with the same USD 10m of revenue can reasonably be worth USD 20m or USD 70m, depending on their mix of premium and discount drivers.

Your job, over the next 6-12 months, is to shift your profile - and the evidence you can present - so that buyers see you closer to the upper end of what is reasonable, not the lower.

8. Where Your Business Might Fit (Self-Assessment Framework)

Here’s a simple way to roughly position your company on the valuation spectrum before you talk to buyers.

How to use this

- For each row, score yourself 0, 1 or 2.

- Be brutally honest - no one else sees this.

- Then add up your total and see which band you fall into.

A simple interpretation:

- 0-5 points

- You are likely at the lower end of your segment range. Rushing to sell now may lock in a discount; consider working on fundamentals first.

- 6-10 points

- You are probably in the "fair market" band for your segment (for example, 1.5-2.5x for MSP-like profiles, 2.5-4.0x for regional infra, etc.). A good process can still create competition and push you up within this band.

- 11-12 points

- You are edging toward premium territory. With a structured, competitive process and the right buyer universe, you could command multiples at or above the top end of the normal range for your category.

This is deliberately rough, but it gives you a sense of where improvements might have the biggest payoff before you formally launch a sale.

9. Common Mistakes That Could Reduce Valuation

A lot of value is lost not because the business is bad, but because the sale is handled badly. Here are avoidable mistakes that can materially lower your outcome:

- Rushing the sale

- Going to market without clean numbers, a clear story and basic preparation often leads to lower offers and more painful diligence.

- Hiding problems

- Buyers almost always discover issues (churn spikes, security incidents, uptime problems). If they feel you hid them, trust collapses and so does price - often late in the process.

- Weak financial records

- Inconsistent revenue recognition between projects and managed services, unclear gross margin by product, and missing KPI tracking (churn, net retention, ARPU) all create uncertainty and discounts.

- Skipping easy margin improvements

- Not cleaning up low-margin legacy contracts, bad vendor deals or unnecessary costs 6-12 months before sale means leaving "free EBITDA" on the table.

- Lack of a structured, competitive sale process with an advisor

- Research across M&A markets indicates that running a structured, competitive process with an advisor often leads to materially higher purchase prices (commonly cited numbers are around 20-25 percent uplift versus one-off, bilateral deals).

- Revealing the price you are "looking for" too early

- If you say "we’re hoping for around USD 10m", buyers will anchor around that and come back with USD 10.1m or USD 10.2m instead of what they might have otherwise offered. Let the market talk first.

- Over-investing in capex right before selling

- Building a new data center or buying a big GPU fleet without clear utilization can scare buyers and drag down valuation.

- Under-documenting security and compliance

- Many founders assume "we’re secure" is obvious. Buyers need evidence - certifications, policies, incident logs, audits. Without that, they assume more risk than they should.

Avoiding these mistakes does not guarantee a premium multiple, but it prevents avoidable discounts that can easily be in the high single or double-digit percentage range.

10. What Cloud Infrastructure Founders Can Do in 6-12 Months to Increase Valuation

You probably cannot completely reinvent your business before a sale, but you can make targeted moves that change how buyers see your risk, growth and quality.

Think in three buckets: improve the numbers, improve the narrative and risk profile, and improve the process.

a) Improve the numbers (within reason)

- Tidy up gross margin

- Re-price obviously underpriced contracts as they renew.

- Reduce low-margin hardware resale and push more managed services.

- Lift EBITDA quality

- Remove discretionary founder expenses that won’t continue post-deal.

- Be clear about what is truly one-off vs recurring cost.

- Focus on healthier growth

- Prioritize growth in segments with better margins and stickiness (for example, DRaaS and security-managed services) rather than low-margin projects.

b) Improve the narrative and risk profile

- Clarify your core positioning

- Are you a sovereign cloud partner for regulated sectors, a GPU cloud specialist, a secure M365 provider, or a general MSP? Pick a clear "headline" for buyers.

- Strengthen security and compliance story

- Close obvious gaps, run internal security reviews, and document how you operate.

- If practical, complete at least one key certification and ensure it’s valid during the sale process.

- Reduce visible concentrations

- Where possible, diversify by adding or growing a few more mid-size customers, especially before disclosing your top customer list.

c) Upgrade financial and operational transparency

- Clean up your financial reporting

- Provide at least 3 years of monthly P&L with split by product line and revenue type (recurring vs project).

- Track and report KPIs: churn, net retention, ARPU, gross margin, and revenue by vertical.

- Prepare a clear forecast

- Build a realistic 3-5 year plan with clear assumptions. Buyers are not expecting a crystal ball, but they do want to see structured thinking.

d) Get sale-ready on process

- Build a light data room early

- Even before you formally launch, organize contracts, policies, financials and key metrics in one place.

- Decide what type of buyer you want

- Strategic acquirer? PE platform? PE roll-up? This influences how you present the business and which metrics you stress.

- Line up advisors who understand cloud infrastructure

- Sector-specific advisors can better position your premium drivers and reach the right buyer universe.

When you tie these actions directly back to the premium and discount drivers we covered, you can see the valuation impact:

- Reducing churn and raising recurring revenue moves you toward backup/DRaaS and mission-critical managed services profiles.

- Strengthening security and sovereignty posture moves you toward PCG Cyber, Venn IT and BlakYaks-type outcomes.

- Cleaning financials and KPIs reduces "uncertainty discounts" during due diligence.

11. How an AI-Native M&A Advisory Helps

Running a high-quality sale process while also running your cloud infrastructure business is hard. An AI-native M&A advisor like Eilla AI combines experienced human bankers with AI systems that are built for exactly this kind of work.

1) Higher valuations through broader buyer reach

- AI can scan hundreds of potential buyers and investors based on:

- Past deal history.

- Technology and product fit.

- Financial capacity and strategic priorities.

- That means more of the right buyers around the table - not just the obvious local MSPs or one or two PE funds.

- More relevant buyers usually leads to more competition, stronger offers, and a higher chance the deal closes even if one party drops out.

2) Initial offers in under 6 weeks

- AI-driven matching and outreach can identify and prioritize top-fit buyers quickly.

- Drafts of key materials - teasers, information memoranda, management presentation decks - can be created and refined much faster than in a purely manual process.

- AI tools can also help structure your data room and support due diligence, reducing friction once buyers engage.

- The result: you can often get from "we’re ready to explore options" to initial conversations and offers in weeks, not many months.

3) Expert advisory, enhanced by AI

- You still get human M&A advisors with years or decades of experience in technology and cloud infrastructure.

- AI helps them:

- Benchmark your numbers against relevant cloud infrastructure comps.

- Craft a positioning that speaks the buyer’s language - whether they are a hyperscaler-focused strategic, a sovereign data center group, or a PE fund.

- Spot red flags early so you can address them before buyers see them.

- In practice, that means Wall Street-grade advisory quality, without the traditional bulge-bracket cost structure or slow, manual processes.

If you’d like to understand how an AI-native process could support your own exit - from testing the waters to running a full competitive sale - book a demo with one of Eilla AI’s expert M&A advisors. Even a short conversation can help you see where your cloud infrastructure business might realistically sit on the valuation spectrum, and what to focus on in the next 6-12 months to improve your outcome.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.