The Complete Valuation Playbook for Data Management Businesses

A practical guide to how data management businesses are valued and what drives high multiples.

If you are a founder or CEO of a privately held data management business and you may sell in the next 1-12 months, valuation should not be a mystery. In this market, buyers are still paying strong prices for the right assets - but they are much more selective about what they pay up for.

That matters in data management because this sector covers very different businesses under one label. A cloud-native platform with sticky recurring revenue is valued very differently from a services-heavy data integration firm, an industrial telemetry business, or a geospatial data platform with project-based delivery. The labels can sound similar. The valuation outcomes often are not.

This playbook is built to help you understand what data management businesses actually sell for, what pushes multiples up or down, where your company may fit, and what you can realistically do in the next 6-12 months to improve the outcome.

1. What Makes Data Management Unique

Data management is not one single business model. In practice, the sector includes several different types of companies:

- Software-first platforms for data cataloging, observability, governance, lineage, digital twins, and operational visibility

- Edge-to-cloud and industrial data platforms that sit between sensors, assets, workflows, and enterprise systems

- Data engineering, analytics consulting, and managed services firms that help customers implement and operate data infrastructure

- Vertical data businesses built around regulated, infrastructure, utility, geospatial, or industrial use cases

That mix matters because buyers do not value all revenue the same way. A dollar of recurring software revenue with strong gross margin, low churn, and deep integration into customer workflows is usually worth much more than a dollar of project revenue that must be resold every quarter.

Another sector-specific issue is that buyers often care less about the broad phrase "we help companies use data better" and more about your exact place in the stack. Are you the system of record? The governance layer? The analytics layer? The integration layer? The managed services wrapper? The closer you are to a mission-critical workflow, the more strategic you look.

Buyers also spend a lot of time checking risks that are especially important in data management. These usually include customer concentration, dependence on a few technical staff, implementation-heavy delivery, unclear product versus services mix, weak data security controls, limited auditability, and customer value that is hard to prove. In regulated or infrastructure settings, they also check whether your product is truly hard to replace or just technically interesting.

2. What Buyers Look For in a Data Management Business

At a basic level, buyers still care about the classic four things: scale, growth, margin, and predictability. A bigger company with faster growth, higher gross margin, and more recurring revenue will almost always attract more interest than a smaller, flatter, more project-led business.

But in this sector, buyers also look closely at how your revenue is produced. They want to know whether you are really a software business, or whether software is only one part of a delivery model that still depends on custom work, implementation, hardware, or ongoing services. Founders often describe their business as "platform-led." Buyers test whether the numbers actually support that story.

They also care about customer dependence and stickiness. If your software is deeply embedded in data pipelines, governance workflows, field operations, utility systems, or industrial environments, switching becomes painful. That makes your revenue more valuable. If customers can replace you with a larger vendor, a systems integrator, or an in-house team without much disruption, multiples usually fall.

Strategic buyers and private equity buyers often look at the same business through slightly different lenses.

How strategic buyers think

Strategic buyers ask questions like these: Does this fill a product gap? Does it help us sell into a new customer set? Does it improve our data governance, compliance, workflow depth, or industrial edge capabilities? Can we cross-sell this into our installed base?

That is why some companies get paid for as "missing puzzle pieces." Even when they are not yet highly profitable, buyers may pay a premium if the asset completes a broader platform and unlocks enterprise adoption.

How private equity thinks

Private equity buyers are more likely to ask: If we buy this today, who do we sell it to in 3-7 years? Can we grow revenue faster? Can we improve pricing? Can we cross-sell? Can we reduce delivery cost? Can we add smaller acquisitions around it?

They are also very aware of entry multiple versus exit multiple. If they buy at a high multiple, they need a believable path to grow into that valuation. In data management, that usually means pushing the company toward more recurring revenue, cleaner product packaging, better customer retention, stronger margins, and a broader buyer universe for the next sale.

3. Deep Dive: Productized Platform Revenue vs Services-Heavy Delivery

This is one of the biggest valuation dividing lines in data management. Two companies can both say they "manage enterprise data," yet one sells like a software platform and the other sells like a consulting business.

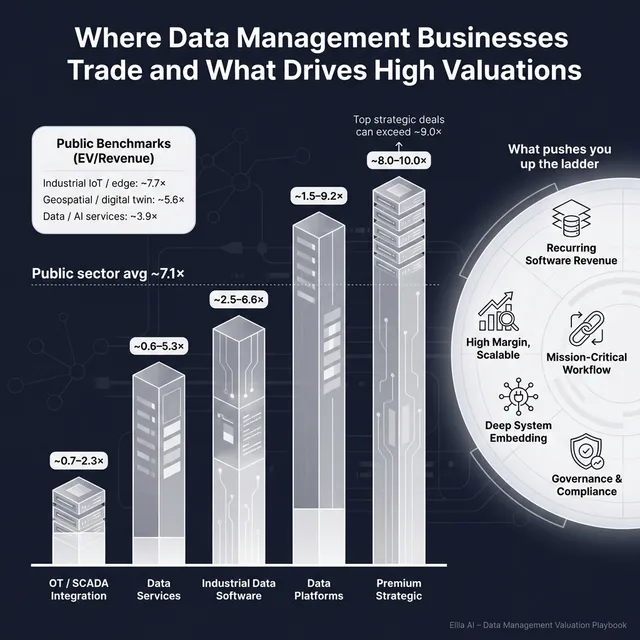

The source data makes this pretty clear. Software-first data and observability assets can achieve much stronger revenue multiples than services-led analytics and implementation businesses. Private software-first examples in the dataset range from under 1.0x at the weak end to above 9.0x at the strong end, while services-led deals are generally much lower on revenue multiples and depend more on EBITDA quality.

Why buyers care is simple. Productized software revenue is more scalable. Once the platform is built, adding more customers should not require hiring in a straight line. Services-heavy revenue is different. Every new customer may need more people, more custom work, more implementation effort, and more delivery risk. That limits operating leverage and makes future margin expansion less certain.

This does not mean services are bad. In many data management businesses, services are what help win customers, integrate systems, and deepen relationships. But buyers want to see services supporting the product - not carrying the whole company. If services are too large a share of revenue, or every deployment looks custom, buyers start to worry that your software is less repeatable than the pitch suggests.

A second nuance inside this same theme is governance and compliance. The source data shows that software assets tied to governance, lineage, compliance, and enterprise-grade controls can command standout revenue multiples even before they are highly profitable. Buyers may see those features as essential to completing a broader data stack.

A simple way to think about it is this:

If your business looks more like the left side today, the best move is not a total reinvention. It is to make the product story more real in the numbers: separate software from services, standardize onboarding, reduce custom work, tighten packaging, and show that more of next year's growth can come without adding delivery headcount at the same pace.

4. What Data Management Businesses Sell For - and What Public Markets Show

The data shows a wide spread, which is exactly what founders need to understand. This is not a sector where one headline multiple tells the story. The gap between lower-quality and higher-quality assets is large because buyers care deeply about business model quality, mission-critical value, and growth durability.

The overall source set shows public companies averaging about 7.1x EV/Revenue and 19.5x EV/EBITDA, with medians of about 4.0x and 18.4x. Private transactions are lower on average, at roughly 3.2x EV/Revenue and 15.2x EV/EBITDA, with medians around 2.3x and 15.0x. That is a useful anchor: private companies usually do not sell at public-market prices unless they are truly exceptional or strategically scarce.

4.1 Private Market Deals (Similar Acquisitions)

In the private deal data, the strongest revenue multiples tend to appear in software-first assets with strategic relevance - especially governance, observability, and specialized domain software. Services-led and systems-integration-heavy businesses generally trade lower on revenue multiples, though solid EBITDA can still support attractive EBITDA multiples.

That pattern matters because many privately held data management companies are hybrids. They may have real software value, but also carry implementation, services, or integration work that drags down how buyers underwrite the revenue base.

A few takeaways stand out from the private comps. First, software-first assets can get paid very well when they solve a hard problem inside a larger buyer's platform. Second, strong profitability can support a premium EBITDA outcome even when revenue multiples look modest. Third, businesses that depend on engineering projects, integration work, or custom delivery usually sit lower unless there is a very clear strategic reason for a buyer to stretch.

These ranges are illustrative, not a price list. Your actual outcome depends on your growth, margin, retention, customer quality, product depth, and buyer fit.

4.2 Public Companies

Public markets give a useful reference point, but not a direct sale price. As of mid to late 2025 in the source set, the highest trading categories tend to be software-led businesses with stronger growth narratives, higher gross margins, and clearer strategic positioning. Hardware-heavy, services-led, or project-led models trade lower.

For a founder, the most useful public comparison is not "what is the highest multiple in the whole dataset?" It is "which public segment looks most like my business model, my margin profile, and my growth story?"

*Based on the smaller subset of companies in the source data that disclosed EBITDA multiples.

The public market spread is the main lesson. Some software-led businesses trade at very high revenue multiples because investors believe growth will stay strong and margins can scale. Others trade much lower because revenue quality is weaker, growth is slower, or the model depends more on projects, hardware, or field work.

For private founders, public multiples are best used as an upper and lower reference band. In most cases, you should expect a private valuation to be adjusted down for smaller scale, lower liquidity, higher customer risk, or weaker margins. The exception is when your asset is scarce, strategically important, and fills a clear gap for a buyer that can pay for that value.

5. What Drives High Valuations (Premium Valuation Drivers)

The source data points to several themes that consistently support stronger valuations. Some are specific to data management. Others are simply what sophisticated buyers always pay more for.

5.1 You solve a mission-critical problem, not a nice-to-have one

Buyers pay more when your platform sits inside an essential workflow. That can mean data governance, lineage, compliance, operational visibility, asset monitoring, or a system that helps customers avoid risk, downtime, or regulatory pain.

The key question is whether customers truly depend on you. A dashboard that is useful but optional is not valued the same way as a system that feeds decisions, compliance, or day-to-day operations.

5.2 You are a missing product piece for a bigger platform

One of the clearest premium patterns in the source data is when a target fills a missing capability inside a larger software stack. Governance, auditability, lineage, policy control, and other "enterprise readiness" features can be worth a lot because they help a bigger acquirer sell a more complete platform.

In practical terms, this means buyers may pay up if you help them answer a question like: "How do we make our broader platform enterprise-grade?" That logic can matter even if your current profitability is still developing.

5.3 High gross margin with a believable path to operating leverage

Buyers do not just want growth. They want growth that can become cash flow. High gross margin matters because it suggests incremental revenue can turn into profit over time.

That is why a software-led business with strong margins and improving efficiency often attracts more interest than a low-margin company growing at the same speed. Buyers are underwriting the future shape of earnings, not only today's revenue.

5.4 Deep customer embedding and hard-to-replace deployments

Premium outcomes often show up where the product is operationally embedded. This is especially true in industrial, infrastructure, utility, and regulated environments where the software is tied to real workflows, field operations, or risk management.

If replacing your product would require retraining teams, changing processes, revalidating systems, or passing new approvals, your revenue becomes more durable. Durable revenue gets paid for.

5.5 Regulatory and compliance relevance

The source data suggests that regulatory friction can actually support valuation when it signals a real barrier to entry. In other words, if your product operates in a sensitive environment where approvals, security standards, or national-interest rules matter, buyers may view that as evidence that the business is not easy to replicate.

That only helps if you can prove it. Founders should be able to show where their product has passed security reviews, compliance checks, customer qualification hurdles, or deployment standards.

5.6 Clean recurring revenue, diversified customers, and a real management bench

These are not glamorous, but they matter in every sale. Buyers pay more for revenue they can trust. They also pay more when the business is not dependent on one customer, one founder, or one technical leader.

Examples founders can relate to include:

- Multi-year customer relationships with good renewal history

- Clear split between software subscriptions and services

- No single customer dominating revenue

- A product and engineering organization that does not depend on one person

- Financial reporting that lets buyers understand gross margin, churn, and cohort behavior quickly

6. Discount Drivers (What Lowers Multiples)

A lot of founders focus on headline multiples and miss the real question: why do some companies land at the low end of the range? Usually it is not because the sector is weak. It is because the buyer sees risk, complexity, or weak revenue quality.

The first common discount is services-heavy revenue disguised as software. If a large share of growth still depends on custom implementation, consulting, or manual delivery, buyers worry about scalability. This is one of the biggest reasons data businesses trade below the best software comps.

The second is weak proof of differentiation. If you claim AI, analytics, observability, or data management capabilities but cannot show a unique dataset, strong product depth, meaningful switching costs, or clear customer outcomes, buyers often compare you to lower-multiple peers rather than higher-multiple category leaders.

Another discount driver is poor profitability without a clear story for improvement. The source data shows that loss-making companies can still get strong revenue multiples, but only when buyers see a strategic reason or a believable operating leverage story. Losses by themselves do not create a premium.

Other common discount drivers include:

- Customer concentration

- Churn or weak expansion within the customer base

- Founder dependence in sales, product, or delivery

- Security, compliance, or data-governance gaps

- Unclear product versus services economics

- Slowing growth at the wrong moment in the sale process

- Messy financial records and weak KPI reporting

There are also comp-quality issues. The source data itself shows that inconsistent disclosure around a deal can create valuation noise. In real sale processes, buyers notice the same thing inside your business. If your story, metrics, and legal structure are not clean, they discount what you say.

7. Valuation Example: A Data Management Company

Let’s make this real with a fictional company.

Assume a fictional business called NorthRiver Data Systems, with USD 10m of annual revenue. It sells a cloud-based data management platform to industrial and infrastructure customers. The company has strong software characteristics, but some edge integration and deployment work still comes with larger contracts. This company is fictional, and the valuation below is illustrative only - not investment advice and not a formal valuation.

a) How the logic works

The right way to think about valuation here is to start with the closest public and private comparison groups, then narrow to the business model that best fits. For this kind of company, the most relevant comp groups are usually software-led data platforms, industrial IoT / edge-to-cloud platforms, geospatial or digital twin platforms, and selected private software-first data deals.

The source data shows why founders need judgment. Very high public multiples do exist, but they often belong to companies with stronger scale, faster growth, category leadership, or a more purely software-driven model. On the other hand, services-heavy and project-led businesses trade much lower. So the goal is to find the range that best matches the company you actually have, not the one you wish you had.

In the worked logic provided in the source set, a software-led edge-to-cloud platform with USD 10m revenue supported a defendable range of roughly 6.5x-10.0x EV/Revenue, or USD 65m-100m EV, because it sat closer to the higher-quality software side of the sector than the services side. That is not a sector-wide average. It is a profile-specific range for a relatively attractive software-led asset.

b) Applying that logic to the fictional company

For NorthRiver Data Systems, I would frame the valuation like this:

c) What would justify each case?

Discounted case - USD 30m-45mThis is where the company would land if buyers decide it is more services-heavy than it first appears, growth is slowing, customer concentration is high, or the edge deployment work makes the model feel less scalable.

Core case - USD 65m-80mThis fits a business that is clearly software-led, has strong gross margins, good retention, real customer embedding, and a believable path to improved profitability. This is the range that follows the worked logic in the source data most closely.

Premium case - USD 80m-100mThis requires more than just good software. Buyers would need to see strategic scarcity: governance and compliance relevance, deeper regulatory or infrastructure defensibility, very sticky customer workflows, or a clear product gap that the acquirer needs to fill.

The main lesson is simple: two companies can both have USD 10m of revenue and still be worth very different amounts. In data management, the spread is driven by revenue quality, product depth, strategic fit, and how much of the future value a buyer believes is already visible.

8. Where Your Business Might Fit (Self-Assessment Framework)

You can use the framework below to judge where your company roughly sits today. Score each factor from 0 to 2.

- 0 = weak or not yet proven

- 1 = decent but mixed

- 2 = clearly strong

Be honest. The point is not to give yourself a high score. The point is to see where improving one or two factors could move valuation materially.

How to interpret the score

8-10 pointsYou are closer to the premium end of the valuation range. That does not guarantee a premium outcome, but it means the business likely has several of the features buyers compete for.

5-7 pointsYou are probably in the fair-market middle. A good process can still produce a strong result, but buyers will likely focus on a few obvious risks or limitations.

0-4 pointsYou may still be sellable, but the business is more likely to price off weaker comps unless you improve a few key drivers before going to market.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often go to market before the numbers are clean, before the story is clear, and before they have framed the business the way buyers actually think about it. That usually leads to discounting, not speed.

Another major mistake is hiding problems. This always comes out later - in diligence, in customer calls, in code review, or in security review. Once trust breaks, value drops quickly. Buyers can live with issues they understand. They hate surprises.

Weak financial records also hurt more than many founders expect. In data management, buyers want to see clear separation of subscription revenue, services revenue, gross margin by line, churn, expansion, and customer concentration. If those are messy, buyers assume the business is riskier than it may really be.

A fourth mistake is running an unstructured sale process without an advisor. Good buyers rarely bid their highest price first. A structured, competitive process creates comparison, urgency, and real price discovery. Research and market experience often show that a well-run competitive process with an advisor can lead to meaningfully higher outcomes, often around 25% better than a weak process.

Another very common error is telling buyers the price you want before the market speaks. If you say you want USD 10m, many buyers will anchor just above that - maybe USD 10.1m or USD 10.2m - even if they might have gone much higher in a real competitive setting. You want buyers to show you what the asset is worth to them, not simply accept your opening anchor.

There are also a couple of sector-specific mistakes that matter in data management:

- Treating services revenue as if it deserves software multiples

- Underinvesting in governance, auditability, data security, and compliance proof before a sale

In this sector, those details directly affect whether buyers see a scalable platform or a riskier delivery business.

10. What Data Management Founders Can Do in 6-12 Months to Increase Valuation

You do not need a massive pivot to improve value before a sale. Most of the best moves are about sharpening the business you already have.

10.1 Improve the numbers buyers care about most

Start by separating software revenue from services revenue clearly. If onboarding, implementation, and custom work are mixed into one line, fix that. Buyers need to understand what part of the business is truly recurring and scalable.

Work on retention and expansion. Even a modest improvement in renewals or account growth can change how buyers think about durability. If customers are paying more over time and staying longer, that shows real product value.

Also tighten gross margin where you can. Reduce custom delivery work, standardize deployments, and make support more efficient. Buyers pay for the shape of future earnings.

10.2 Make the product story more believable

If you say you are a platform, prove it. Standardize packages, document integrations, shorten implementation time, and show repeatable deployment patterns across customers.

If governance, compliance, audit trails, lineage, or policy controls are important in your market, strengthen those areas. The source data suggests these features can matter a lot when they help a buyer complete a broader product stack.

10.3 Reduce obvious buyer risks

Cut customer concentration where possible. Build a stronger second layer of leadership. Tighten data security and document it well. Make sure key contracts, IP ownership, and employment matters are clean.

These may not feel like growth projects, but they can have a direct effect on valuation because they reduce reasons for buyers to retrade price later.

10.4 Build the right evidence before you sell

Track the KPIs buyers will ask for anyway: recurring revenue, gross margin, churn, net revenue retention if you have it, services mix, sales efficiency, customer concentration, and deployment time.

Also build a crisp narrative around your place in the market. Are you a governance layer, an observability platform, a vertical data system, an edge-to-cloud workflow engine, or a specialized industrial data asset? A clear answer helps buyers place you against better comps.

10.5 Prepare for a competitive process

The companies that get the best outcomes are usually prepared, not lucky. That means a clean financial pack, strong materials, a sharp list of likely buyers, and a process designed to create competition.

You do not need 24 months for that. But you do need enough time to fix the obvious issues, tell the story well, and show a credible forward path.

11. How an AI-Native M&A Advisor Helps

A strong exit is not only about having a good business. It is also about running the right process. An AI-native M&A advisor can expand the buyer universe far beyond the obvious names by identifying hundreds of qualified acquirers based on deal history, product fit, financial capacity, and likely synergies. More relevant buyers means more competition, stronger offers, and a better chance the deal still closes if one buyer drops out.

Speed also matters. With AI helping match buyers, build marketing materials, organize buyer outreach, and support diligence, founders can often get to initial conversations and first offers much faster than in a manual-only process. In many cases, that means initial offers in under 6 weeks.

The best version of this is not AI alone. It is expert human advisors using AI to make the process broader, faster, and sharper. That means experienced M&A professionals guiding positioning, preparing materials that speak the buyer's language, and framing the business in the most attractive strategic light - with AI doing the heavy lifting underneath. The result is Wall Street-grade advisory quality without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.