The Complete Valuation Playbook for Digital Health Businesses

A practical guide to how digital health businesses are valued and what drives high multiples.

If you are thinking about selling your digital health business in the next 1-12 months, your valuation will not be decided by a single “market multiple.” It will be decided by how buyers translate your specific risk profile - clinical, regulatory, reimbursement, data privacy, integration, and retention - into what they are willing to pay today.

This playbook is built to be practical. It shows what similar digital health businesses have actually sold for, explains what drives higher vs lower multiples, and gives you a simple self-assessment and a 6-12 month action plan to improve your outcome.

1. What Makes Digital Health Unique

Digital health sits in an awkward-but-valuable middle zone: it is software, but it touches clinical decisions, patient outcomes, sensitive data, and regulated workflows. Buyers therefore value it differently than generic SaaS.

The main types of digital health businesses (and how they monetize):

- Virtual care and chronic condition management - often PMPM (per member per month), employer/payer contracts, or provider networks (telehealth + coaching/programs).

- Provider enablement platforms - workflow software for practices and hospitals (EHR/EMR adjacencies, patient flow, patient engagement); usually subscription + implementation.

- Remote patient monitoring and device-enabled care - hardware + software + services; revenue mix can include device sales, recurring monitoring fees, and reimbursement-driven RPM revenue.

- Digital therapeutics (DTx) and SaMD (software as a medical device) - regulated software with evidence requirements; monetization can be enterprise licensing (life sciences partnerships) and/or reimbursement-linked programs.

- Life sciences software and clinical trials tech - tools that sell into pharma/biotech (trial operations, real-world data platforms); typically contract-based with longer cycles and higher compliance burden.

- Services-heavy digital health integrators - implementation, compliance, analytics, and engineering services that support regulated healthcare and life sciences buyers.

Unique valuation considerations buyers will price in:

- Regulatory credibility (what you can safely claim, what your product is cleared/validated for, and what could go wrong).

- Clinical proof and outcomes (or at least a believable pathway to proof).

- Reimbursement dependence (how much of your revenue relies on policy or billing codes staying favorable).

- Data risk (privacy/security posture, breach history, and how defensible your controls are).

- Integration friction (EHR, payer systems, device stacks, identity, workflow adoption).

- Retention and utilization (do patients or clinicians actually keep using it?).

Key risk factors buyers will always check:

- Whether you are truly “software” (repeatable product) or mostly “people” (services delivery).

- Whether growth is durable without constant new pilots.

- Whether your revenue is contractually recurring (or at least predictable).

- Whether you can survive diligence around security, privacy, and clinical/regulatory documentation.

2. What Buyers Look For in a Digital Health Business

Think of buyers as trying to answer one question: “If we own this, will it keep growing without blowing up?” Their valuation is their best guess at risk-adjusted future cash.

The obvious factors still matter

- Scale: More revenue usually means more credibility and more buyer options.

- Growth: Buyers pay up for momentum - but only when it looks repeatable.

- Gross margin: Software-like margins give buyers confidence they can grow profitably.

- Profitability (or a clear path): In the digital health deal data, the most “premium” outcomes show up more clearly on EV/EBITDA (earnings multiples) than on revenue multiples. In other words, buyers are rewarding cash flow quality. (More on this later.)

Digital health nuances that matter more than in normal SaaS

- Who pays (employer, payer, provider, pharma, patient) and how stable that payer is.

- Proof and trust (clinical validation, regulatory posture, security credentials).

- Adoption: You can sell it, but can customers implement and expand it?

- Workflow criticality: Tools that sit in daily workflows tend to retain better.

- Evidence and outcomes: Even if not “fully proven,” buyers want credible signals: engagement, adherence, reduction in avoidable costs, or improved operational throughput.

How private equity buyers think (in plain English)

A financial sponsor is underwriting a 3-7 year story:

- Entry price vs exit price: They ask “If we buy at X, can we sell later at X or higher?”

- Who could buy it later: Larger strategics, larger PE funds, or sometimes public markets.

- What levers they will pull:

- Raise prices where value is clear

- Improve retention and upsell

- Reduce services-heavy delivery costs

- Add bolt-on acquisitions

- Professionalize reporting, KPIs, and forecasting

If your business requires heroic effort from the founders to keep growing, PE will price that risk - or avoid the deal.

3. Deep Dive: Productized Software vs Services Mix - The Valuation Gravity in Digital Health

In digital health, one factor quietly explains a lot of valuation outcomes: how much of your business is a repeatable product vs bespoke services.

Why it matters: services-heavy models can grow fast early, but buyers worry about:

- Hiring constraints and delivery capacity

- Project overruns and client-specific dependencies

- Lower predictability and weaker margins at scale

The data hints at this “gravity.” Private digital health-related deals cluster mostly around ~1-6x EV/Revenue depending on segment, with regulated software-like platforms higher on average than compliance/engineering services. For example, precedent deals show average EV/Revenue of ~5.9x for regulated DTx/SaMD platforms vs ~3.0x for healthcare IT compliance/engineering services. (Those are averages - your outcome depends on your profile.)

Buyers will pay more when they believe your services are:

- A short-term implementation layer that shrinks over time, or

- A high-margin, repeatable “deploy-and-expand” motion attached to software

They will pay less when they believe services are the product.

A simple way to think about it:

If you look more like the left column today, the fix is not “stop services tomorrow.” The fix is to show credible movement: standardized packages, repeatable delivery, and expanding recurring revenue.

4. What Digital Health Businesses Sell For - and What Public Markets Show

Valuation is not one number. It is a range shaped by:

- Your segment (what you sell and to whom)

- Your business model (recurring vs project, software vs device vs services)

- Your risk profile (compliance, evidence, retention, reimbursement)

- Your profitability (or the believable path to it)

This section anchors you in two reference points:

- Private deals (what similar companies have been acquired for)

- Public comps (how public investors price categories as of mid/end 2025)

4.1 Private Market Deals (Similar Acquisitions)

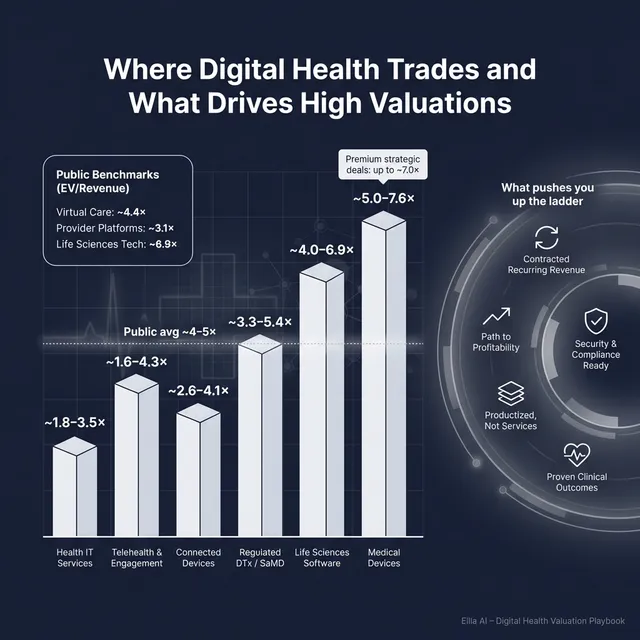

Across the precedent transactions provided, the overall average EV/Revenue is ~4.3x. Within that, there is meaningful variation by deal type and business model:

A few patterns worth translating into plain language:

- Recurring revenue helps. Where deals disclosed ARR or used ARR-linked earnouts, it signals buyers underwrote retention more confidently.

- Profitability can matter more than “digital health story.” Some deals show high EV/EBITDA multiples even when EV/Revenue is modest, indicating buyers paid for durable earnings power.

- Earnouts are common. They can boost headline value, but they also signal buyers want proof post-close rather than paying everything upfront.

These ranges are illustrative - not a promise. Your exact multiple depends on your risk, growth, margins, and deal tension.

4.2 Public Companies

Public markets give you a reality check. They are not your price tag, but they set reference bands and investor psychology.

As of mid/end 2025 (based on the provided public multiples), average EV/Revenue by segment looks roughly like this:

One important caution: the dataset includes ultra-high EV/Revenue prints (28x, 100x+) that appear to be micro-cap anomalies and are not reliable anchors for a typical private, loss-making digital health business.

How to use public multiples as a founder:

- Treat public comps as reference rails, not direct pricing.

- Adjust downward for smaller scale, less liquidity, higher customer concentration, or more regulatory/reimbursement risk.

- Adjust upward only when you are scarce and strategically critical (or when you run a competitive process that forces strategic buyers to stretch).

5. What Drives High Valuations (Premium Valuation Drivers)

Here is what the deal data and buyer behavior consistently reward in digital health. These are the traits that pull you toward the top end of your segment range.

5.1 Trust and de-risking (security, privacy, compliance)

Security and compliance credentials (ISO 27001, SOC, HIPAA/GDPR/HITRUST-aligned programs) show up as buyer “de-riskers.” In the provided deal notes, these attributes supported dealability - they reduced diligence friction and made it easier for buyers to focus on growth rather than hidden risk.

Practical examples:

- You can pass a security review without weeks of scramble.

- You have clear policies, audits, and documentation.

- You can sell to enterprise healthcare and life sciences buyers faster.

Important nuance from the data: compliance alone did not create 10x+ revenue multiples. It protects downside. The premium emerges when compliance is paired with recurring revenue and/or strong margins.

5.2 Contractual recurring revenue (and clear proof of it)

Buyers pay more when they can underwrite retention. In the dataset, recurring revenue shows up via ARR disclosure and earnouts pegged to recurring targets. That is a signal buyers are anchoring value to contracted economics, not hope.

Practical examples:

- Multi-year agreements with auto-renewal.

- Expansion revenue (customers pay more over time).

- Clear cohort retention and renewal history.

5.3 Profitability and “cash-flow quality”

A key observation in the premium driver notes: the truly “premium” outcomes in this set show up more on EBITDA multiples than on revenue multiples. Buyers will often pay up for predictable earnings, especially when growth is steady rather than explosive.

Practical examples:

- You can grow without burning cash every quarter.

- Your gross margin is high and stable.

- Services do not eat your software margin.

5.4 Productized delivery economics (software-like gross margin)

Some targets show very high gross margins (90%+) and improving EBITDA margins - the “permission slip” buyers need to believe operating leverage is real. But the data also warns: high gross margin alone is not sufficient for a high revenue multiple if growth, market size, or strategic scarcity is limited.

Practical examples:

- Implementation is standardized.

- Support costs do not rise linearly with revenue.

- You can onboard customers quickly and predictably.

5.5 Scale and diversification (less single-thread risk)

Scale and multi-geo footprint can support higher underwriting confidence, especially for sponsors. More broadly in digital health, buyers pay more when risk is not concentrated in:

- One customer

- One channel partner

- One reimbursement code

- One product line

5.6 A credible “why this buyer” strategic narrative

This is not fluff. Buyers pay more when the asset is clearly strategic:

- Fills a product gap in their platform

- Creates cross-sell into their installed base

- Strengthens their data moat or workflow position

- Reduces their regulatory exposure or time-to-market

The best outcomes are usually a mix of: de-risked trust + predictable revenue + a strategic reason to own you now.

6. Discount Drivers (What Lowers Multiples)

Most valuation disappointments come from a small set of predictable buyer fears. Here are the common ones in digital health - and what they signal.

6.1 Revenue that looks recurring but behaves like projects

If renewals are shaky, contracts are short, or customers churn after pilots, buyers will treat your revenue as lower quality - even if you call it subscription.

What improves it:

- Longer contract terms, clearer renewal processes, stronger expansion motion.

6.2 Services-heavy delivery that does not scale

If revenue growth requires proportional hiring, buyers worry about margin ceilings and execution risk. This pulls you toward IT services-style multiples, which are generally lower than productized software.

What improves it:

- Standardized implementation, packaged offerings, and a clear plan to increase recurring mix.

6.3 Weak evidence of outcomes or ROI

Digital health is crowded. Buyers want proof that you move a metric someone cares about:

- cost reduction

- better adherence

- reduced hospitalizations

- improved throughput

- clinician time saved

What improves it:

- A small set of credible case studies with measurable outcomes, not just testimonials.

6.4 Reimbursement or regulatory single-point-of-failure

If your economics depend on one code, one payer policy, or a pending regulatory decision, buyers will price the fragility.

What improves it:

- Diversify reimbursement pathways, show resilience across payers/geographies, and document regulatory posture clearly.

6.5 Security/privacy gaps (or messy documentation)

In healthcare, diligence risk is valuation risk. If you cannot answer basic security questions cleanly, buyers either walk away or use it to reduce price and add holdbacks.

What improves it:

- Formal security program, audits, incident response, clean data flows, and documentation.

6.6 Customer concentration and channel dependence

If one customer or partner drives most bookings, buyers fear renegotiation risk. In healthcare, this is common (one health system, one payer, one pharma partner), and it is heavily discounted.

What improves it:

- Diversify logos, build direct demand, reduce “single-thread” dependencies.

7. Valuation Example: A Digital Health Company

This example is intentionally fictional. The company, the revenue level (USD 10m), and the valuation range are illustrative. The purpose is to show how buyers actually apply multiples.

Step 1: The logic

- Pick the right peer group: compare yourself to businesses with similar revenue quality and risk - not whatever has the highest multiple.

- Anchor to private comps first: private deals reflect how real buyers price risk.

- Use public comps as sanity checks: public multiples set the “mood,” but you adjust for being smaller and private.

- Choose a core multiple range based on:

- Segment (DTx/SaMD vs workflow SaaS vs device-enabled)

- Business model (recurring vs services)

- Profitability (or burn)

- Move up or down based on premium and discount drivers (recurring proof, compliance readiness, margins, concentration, etc.).

The provided worked logic suggests a core range like ~3.5x-7.0x EV/Revenue for an early-scale regulated digital health software business with a services component and negative EBITDA, anchored by private regulated software ranges (low end) and higher-quality life sciences software references (high end) - but capped due to services mix and losses.

Step 2: Apply it to a fictional company

Meet ClearPath Care, a fictional digital health business:

- USD 10.0m annual revenue (fictional)

- Hybrid model: regulated care pathway software + implementation services

- Revenue mix: 70% subscription, 30% services

- Gross margin: 65%

- EBITDA margin: -20% (still investing)

- Customers: mix of health systems and life sciences partners

- Good security posture (SOC 2 in progress, ISO-aligned controls), solid documentation

- Moderate concentration (top 3 customers = 45% of revenue)

Now apply three scenarios:

What creates the premium case?

- Clear ARR and renewal proof (customers stick and expand)

- Strong compliance posture that reduces buyer fear

- Productized implementation (services not a bottleneck)

- A believable path to profitability within 12-24 months

- Multiple motivated buyers (competition)

What creates the discounted case?

- Services creeping up toward “the product”

- Weak renewal history or pilot-heavy revenue

- Customer concentration that scares buyers

- Security/compliance gaps or unclear regulatory documentation

- No credible plan to reduce burn

Step 3: What this means for you

Two digital health businesses can both have USD 10m revenue and be worth very different amounts because buyers are not paying for revenue - they are paying for confidence in future, repeatable cash flow.

This is not investment advice or a formal valuation. It is a worked illustration of how buyers tend to think.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as a rough positioning tool. Score each factor 0-2:

- 0 = weak / unclear

- 1 = decent but improvable

- 2 = strong and provable

Self-assessment table

How to interpret your score (directionally)

- High band: You are closer to the top end of your segment range. You look “de-risked.”

- Middle band: Fair market outcome - good business, but some risk factors need proof.

- Low band: Expect discounts unless you fix a few specific issues before running a process.

The goal is not to “win the score.” The goal is to spot the 2-3 improvements that most directly reduce buyer fear.

9. Common Mistakes That Could Reduce Valuation

9.1 Rushing the sale

If you start the process before your numbers, story, and diligence materials are ready, buyers will control the timeline and the narrative. Rushed processes create one buyer, one offer, and little leverage.

9.2 Hiding problems

In M&A, problems do not stay hidden. They surface in diligence - security gaps, churn, weak margins, missing documentation. If you hide issues, you do not just lose price - you lose trust. Trust loss kills deals or shifts value into holdbacks and earnouts.

9.3 Weak financial records

Many digital health founders run lean finance teams. Buyers still expect:

- Clean revenue recognition logic (especially with services + subscription)

- Clear gross margin by product vs services

- Cohort retention, churn, and expansion data

- A forecast you can explain

If you cannot produce these cleanly, buyers price in uncertainty.

9.4 Not running a structured, competitive process with an advisor

A structured process (tight positioning, full buyer list, clear timeline, controlled data room) usually creates more competition and better terms. Research is often cited that running a competitive process with an advisor can drive meaningfully higher purchase prices - around 25% - because price discovery works better when multiple buyers are engaged.

9.5 Revealing what price you want too early

If you tell a buyer “we are looking for USD 50m,” you often cap your own upside. Many buyers will come back at USD 50.1m and call it done - even if they might have paid more. Your job is to let the market tell you what your business is worth through competing offers.

9.6 Digital health-specific mistake: confusing pilots with product-market fit

A pile of pilots can look like traction, but buyers care about renewals, expansion, and long-term utilization. If your revenue is mostly “new logos” but not “customers that stick,” expect discounting.

9.7 Digital health-specific mistake: underinvesting in security and documentation until diligence

In regulated healthcare, security posture and documentation are not “later problems.” If you scramble during diligence, buyers assume there are more issues you have not found yet.

10. What Digital Health Founders Can Do in 6-12 Months to Increase Valuation

You do not need a massive pivot. You need targeted moves that reduce buyer fear and increase buyer confidence.

10.1 Improve the quality of revenue (the biggest lever)

- Increase recurring mix: move services into packaged onboarding, and price software separately.

- Lock in longer contracts: even moving from 12 months to 24-36 months can change buyer perception.

- Prove renewals and expansion: build simple retention reporting and customer cohorts.

- Reduce concentration: if top customers dominate revenue, prioritize 3-5 new logos to dilute risk.

10.2 Make margins more “software-like”

- Standardize implementation playbooks and reduce bespoke work.

- Track gross margin separately for software vs services.

- Identify 2-3 delivery cost drivers and attack them (tooling, automation, repeatable integrations).

10.3 De-risk trust: security, privacy, compliance, regulatory posture

- Finish SOC 2 (or equivalent) and document controls.

- Create a clean “diligence binder” for privacy, security, and regulatory documentation.

- Make it easy for buyers to say: “This will pass our compliance review.”

10.4 Strengthen outcomes proof and ROI story

- Pick 2-3 measurable outcomes and standardize how you report them.

- Turn customer success into quantified case studies (time saved, adherence improvement, reduced costs).

- If reimbursement is part of your model, document the pathway and show resilience across payers.

10.5 Build a sale-ready narrative and team

- Reduce founder dependence with clear leadership ownership (sales, delivery, product, compliance).

- Create a clear story of “why us wins” in your category - not just features.

- Prepare buyer-ready materials: clean KPIs, customer segmentation, pipeline quality, churn and retention.

If you do only one thing: make your revenue look more predictable and your risk look more manageable. That is what pulls you up the valuation curve.

11. How an AI-Native M&A Advisor Helps

A strong exit outcome usually comes from two things: running a tight process and creating competition among buyers. An AI-native M&A advisor helps you do both at a higher speed and broader reach than manual-only approaches.

First, AI can expand the buyer universe beyond the obvious names. Instead of a short list, you can reach hundreds of qualified acquirers screened by deal history, fit, and financial capacity. More relevant buyers usually means more competitive tension, stronger offers, and a higher chance the deal closes even if one buyer drops.

Second, AI-driven matching and process execution can compress timelines. With faster buyer targeting, quicker creation of marketing materials, and more structured diligence support, initial conversations and offers can often be reached in under 6 weeks - especially when you are prepared.

Third, the best model is not “AI replaces bankers.” It is expert advisors enhanced by AI: sharper positioning, cleaner materials, better buyer coverage, and more disciplined process control - delivering Wall Street-grade quality without traditional bulge bracket costs.

If you would like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.