The Complete Valuation Playbook for Door Products and Services Businesses

A data-driven guide to how Door Products & Services businesses are valued and what drives high multiples.

If you own a Door Products & Services business and you may sell in the next 1-12 months, valuation is not just a finance exercise - it is a strategy exercise. In this sector, buyer appetite is shaped by consolidation, tighter construction markets in some regions, growing interest in safety and access control, and a clear divide between commoditized product businesses and more defensible, service-linked platforms.

This playbook is built to help you understand what Door Products & Services businesses actually sell for, what drives higher or lower multiples, and what you can still improve before going to market. The goal is simple: give you a practical, data-based framework you can use now.

1. What Makes Door Products & Services Businesses Unique

Door Products & Services is a broad category, and that matters for valuation. At one end, you have manufacturers of fire-rated doors, steel doors, shutters, gates, interior doors, frames, and related products. At the other end, you have access control and door automation businesses, distributors and installers, and service-heavy companies that maintain, inspect, or upgrade door and entry systems over time.

That mix creates a major valuation gap inside the sector. A business that mainly sells physical products into one-off projects will usually be valued differently from a business that combines products with installation, maintenance, inspections, compliance support, or electronic access solutions. Buyers do not just ask, "What do you sell?" They ask, "How replaceable are you, and how much of the customer relationship do you own?"

Cost structure is another big sector-specific issue. Many door businesses carry meaningful exposure to raw materials, labor, freight, project execution, and installation quality. So buyers pay close attention to gross margin, pricing discipline, supplier dependence, rework risk, and the ability to pass through cost inflation.

There are also sector-specific risks that show up again and again in diligence. Buyers will check product certification, fire and safety compliance, warranty claims, installation quality, concentration by contractor or distributor, exposure to cyclical new-build construction, and whether your revenue depends on one-off projects or has recurring service elements.

In simple terms: this is not a sector where revenue alone tells the story. Buyers care about where your business sits on the spectrum between product manufacturer, project contractor, and embedded building access partner.

2. What Buyers Look For in a Door Products & Services Business

Most buyers start with the basics: revenue scale, growth, EBITDA, gross margin, cash generation, and management quality. But in this industry, those basics are filtered through a more specific question: does your business look like a durable building systems company, or a harder-to-scale project and product supplier?

Scale matters because it reduces risk. Larger businesses usually have broader customer bases, more stable operations, deeper management teams, and better purchasing leverage. Smaller owner-led businesses can still attract strong interest, but buyers will discount for key-person dependence, limited systems, and narrower capacity.

Buyers also care about customer type. Revenue tied to regulated, high-consequence applications - such as fire-rated environments, healthcare, industrial safety, critical infrastructure, and secure access - tends to be more attractive than purely price-driven standard product sales. Not because it is automatically high margin, but because switching costs, certification, and approval requirements can make the business harder to displace.

Another major factor is revenue quality. If a meaningful share of revenue comes from maintenance, inspection, replacement parts, upgrade cycles, service contracts, or repeat specification work, buyers are more comfortable underwriting future cash flow. If revenue is mostly one-off, tender-based, and won on price, valuation usually stays closer to the low-to-middle part of the range.

How private equity thinks about your business

Private equity buyers usually think in three time frames at once. First, what are they paying to buy you today? Second, what can they improve over the next 3-7 years? Third, who will buy the business from them later?

That means they care about entry multiple versus exit multiple. If they buy a door business at a solid multiple, they need to believe they can sell it later to a larger strategic buyer or a bigger private equity firm at the same or better multiple. That only works if the business becomes more scalable, more diversified, more profitable, and more system-like over time.

The levers they usually look for in this sector are straightforward: bolt-on acquisitions, stronger pricing, more service revenue, cross-selling into the installed base, better procurement, better branch economics, improved sales coverage, and cleaner reporting. They also want to see a believable path from "door seller" to "building access and lifecycle solution provider."

3. Deep Dive: Product-Only Revenue vs Lifecycle Revenue

One of the biggest valuation questions in this sector is whether your business stops at the product sale or stays involved across the life of the opening. That sounds simple, but it often separates average outcomes from premium ones.

The source data shows that the strongest premium narratives appear when a company helps an acquirer build a broader building access or safety suite. That means hardware plus systems plus services - not just physical doors or shutters. Deals with this kind of adjacency are attractive because buyers can cross-sell, bundle more products, and capture a larger share of customer spend.

Why do buyers care so much about this? Because lifecycle revenue is usually stickier than project revenue. A one-time sale can be rebid. A maintenance relationship, inspection schedule, approved supplier status, or installed-base upgrade cycle is much harder to dislodge. It also creates better visibility and often supports stronger margins over time.

In practical terms, a lower-value profile usually looks like this: you manufacture or distribute products, you win jobs largely on price, and your relationship with the customer fades after installation. A higher-value profile looks different: you install, inspect, maintain, repair, upgrade, or support compliance around the opening over multiple years.

Lower-value vs higher-value profile

If your business looks more like the left column today, the path upward is usually not a huge reinvention. It often means building service contracts, formal inspection programs, parts and repair offerings, stronger installed-base records, or partnerships with access control and building services providers. You do not need to become a software company. You do need to become harder to replace.

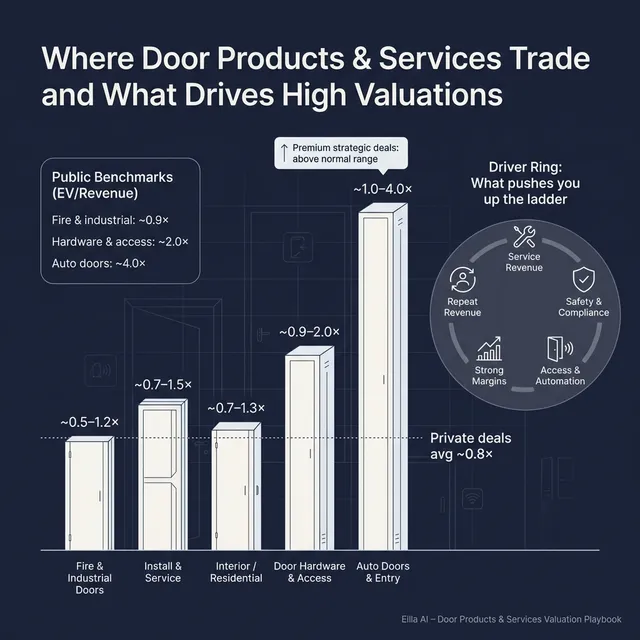

4. What Door Products & Services Businesses Sell For - and What Public Markets Show

Here is what the data actually shows: most public door-related building product businesses trade at relatively modest revenue multiples, and private deal multiples are usually lower still unless there is something strategically special about the target. That should be reassuring, not discouraging. It means you should think in terms of a sensible valuation range shaped by your specific profile - not chase a headline number from a very different business model.

4.1 Private Market Deals (Similar Acquisitions)

The private transactions in the source set point to a market where many door and adjacent building product businesses sell around 0.7x to 0.9x revenue, with EBITDA multiples often in the high-single-digit range when profitability is solid. The overall precedent transaction averages are about 0.8x EV/Revenue and 8.4x EV/EBITDA, with medians of about 0.7x and 8.6x respectively.

But the range matters more than the average. Product-led door and millwork manufacturers sit around the high-0.x revenue range in the data, while distributors and installers can range from the mid-0.x area to around 1.5x depending on scale, geography, and channel position. Service-led fire and security integrators often trade on lower revenue multiples, but can still achieve healthy EBITDA multiples if the earnings base is strong and recurring.

A simple reading of the private data is this: buyers pay more when the business gives them a broader solution, recurring pull-through, or access to a stronger channel position. They pay less when revenue is project-heavy, margins are thin, or the business looks easy to replicate. These ranges are illustrative, not a direct price tag for your business.

4.2 Public Companies

The public market data gives a useful reference band, especially for mid-to-late 2025. Across the full public set, the average EV/Revenue is about 1.6x and the median is about 0.9x. Average EV/EBITDA is about 15.0x, while the median is about 7.4x. That gap between average and median tells you something important: a few stronger, more strategic, or more scalable businesses pull the average up, while most companies trade in more ordinary territory.

Looking by segment, access control and door hardware businesses generally trade better than pure door manufacturing because they often have stronger margins, more differentiated products, and in some cases a technology or service angle. Fire-rated and industrial door manufacturers mostly cluster below 2.0x revenue, often much lower. Automatic doors and building entry systems can trade better when they combine product with maintenance or automation. Interior and wood-based door product companies are more mixed, with weaker performers dragging down the group and select premium names sitting well above the median.

*These averages are skewed by high-multiple outliers and should be interpreted carefully.

The right way to use public multiples is as a reference band, not a formula. Public companies are usually larger, more diversified, better capitalized, and more liquid than private founder-owned businesses. So private company valuations are often adjusted downward for smaller scale, narrower management depth, higher customer concentration, and greater cyclicality.

That said, the public market can also show you where valuation can go if your business has scarce strategic value. If you combine strong margins, recurring service revenue, regulated applications, and a broader building access proposition, you may deserve to be judged against the stronger part of the sector - not the commoditized part.

5. What Drives High Valuations (Premium Valuation Drivers)

The source data shows a clear pattern: premium outcomes in this space do not come from being "a door company" alone. They come from being more strategic, more embedded, and more profitable than a standard product business.

5.1 Broader building access and safety positioning

Buyers pay more when your business helps them offer a fuller solution. That could mean combining doors with access control, automation, maintenance, inspections, compliance support, or adjacent safety systems. In the data, the clearest premium stories show up where buyers can bundle products and services and deepen customer wallet share.

A founder-friendly way to think about this: if your business sits in the middle of the customer relationship, buyers see more future upside. If you are just one purchased component, they see less.

5.2 Exposure to regulated and high-stakes applications

Businesses tied to fire safety, critical infrastructure, healthcare, secure facilities, or other approval-heavy environments can attract premium attention - but only when that exposure is real and defensible. Buyers want proof that you are not just certified, but actually embedded in markets where compliance matters and approved supplier status narrows competition.

Examples include repeat specification into regulated buildings, audited certifications, framework wins, and reference projects where failure is not an option. Those things make a business harder to replace.

5.3 Strong gross margin and improving EBITDA margin

Premium valuation always comes back to economics. Buyers can accept moderate growth if margins are strong and improving. They struggle to justify a premium for businesses with weak gross margin, inconsistent pricing, or poor conversion from revenue to EBITDA.

In this sector, that often means buyers like businesses with a healthy mix of engineered products, customized work, aftermarket revenue, or service support - not just commodity product volume. If your margin profile suggests resilience through cycles, buyers will notice.

5.4 Repeatability and visibility of revenue

A business with recurring inspection schedules, maintenance contracts, replacement parts revenue, or repeat spec-in wins usually gets better valuation conversations than one relying entirely on fresh project bidding every quarter. Buyers do not need perfect recurring revenue. They need evidence that revenue repeats for structural reasons.

For example, a business serving hospitals, schools, industrial sites, or managed property portfolios may have stronger visibility than a business living job-to-job in the new-build residential channel.

5.5 Scaled trust and operational maturity

Long operating history, strong brand reputation, broad references, deeper management, and reliable delivery all reduce buyer fear. In the source data, scaled incumbents benefit from confidence around continuity and integration. Smaller businesses can still do well, but they must replace scale with some other kind of confidence - niche leadership, unusually high margins, or a very defensible customer position.

5.6 Clean fundamentals still matter

Even in a strategic deal, buyers pay more for clean financials, diversified customers, stable leadership, clear KPIs, and credible forecasting. These are not glamorous premium drivers, but they often make the difference between a buyer stretching and a buyer getting cautious.

6. Discount Drivers (What Lowers Multiples)

The low end of the valuation range usually has a clear logic behind it. Buyers are discounting risk, not being irrational.

The first discount driver is commoditization. If your products are easy to compare, easy to substitute, and won mainly on price, buyers will not assume strong long-term pricing power. That pushes valuation down even if revenue is respectable.

The second is project dependence without enough repeat business. If revenue resets every year, backlog is thin, and there is little service or maintenance follow-on, buyers will underwrite more volatility. They may still buy the business, but usually at a lower multiple.

Small scale can also drag valuation down. A business with USD 10m or USD 15m of revenue may be healthy, but if too much sits with the founder, one plant, one sales leader, one supplier, or a few customers, buyers apply a risk discount. In this sector, small scale often means limited operating leverage too.

Weak margins or unstable margins are another common problem. If cost inflation, installation issues, or discounting regularly erode gross margin, buyers lose confidence fast. Door businesses are often judged harshly when the margin story is unclear because buyers know project execution can hide problems until diligence.

Other common discount factors include customer concentration, warranty claims, inconsistent certification records, weak ERP or reporting systems, poor backlog visibility, and overexposure to cyclical construction end markets. None of these automatically kills a deal. But each one pushes you toward the lower end unless you show a credible fix.

A final discount driver from the data is lack of strategic adjacency. If you are a straightforward manufacturer without service pull-through, strong compliance positioning, or system-level relevance, buyers tend to value you closer to traditional building products ranges rather than the better parts of access, safety, or automation.

7. Valuation Example: A Door Products & Services Company

Let us make this concrete with a fictional example.

Assume a fictional company called NorthGate Door Systems. It is a privately owned business with USD 10m of annual revenue. It manufactures and installs fire-rated steel doors, security shutters, and specialty access products for commercial and light industrial buildings. It also has a growing maintenance and inspection offering. This company is fictional, and the valuation ranges below are illustrative only - they are not investment advice or a formal valuation.

7.1 Step 1 - How the logic works

The most relevant starting point is the core peer set for fire-rated, security, and industrial door manufacturers. In the source materials, that group supports a reasonable public reference band of about 0.5x to 1.2x revenue for typical players, with the worked logic suggesting a defensible starting valuation range of around USD 5m to USD 12m on USD 10m of revenue.

Then you cross-check against broader building products, residential/interior door companies, and private door and millwork transactions. That helps you avoid overrelying on one group and also filters out obvious outliers. The source logic does exactly that and lands on a more practical defended range of about USD 7m to USD 15m, or 0.7x to 1.5x revenue, for a smaller physical building-products company with some differentiated features.

From there, you adjust for premium and discount drivers. If the business has strong margins, real compliance defensibility, recurring service pull-through, and customer diversification, it can move toward the upper part of the band. If it is small, founder-dependent, margin-pressed, and project-heavy, it likely stays near the lower end.

7.2 Step 2 - Apply the logic to NorthGate Door Systems

Assume NorthGate has the following profile:

- USD 10m revenue

- Good reputation in fire-rated and secure commercial openings

- 20% of revenue from maintenance, inspections, and replacement work

- Gross margin above a basic commodity manufacturer

- No single customer over 12% of revenue

- Founder still active, but with a credible operations leader in place

That is better than an ordinary small product business, but not a full premium platform. A sensible conclusion would be:

7.3 What would create the discounted case?

If NorthGate were heavily reliant on one contractor, had weak margin control, little service revenue, limited certifications, and most commercial relationships ran through the founder, buyers would likely anchor closer to USD 7-9m.

7.4 What would create the premium case?

If NorthGate had a strong installed base, formal inspection and maintenance contracts, repeat wins in regulated sectors, cleaner data on backlog and service attach rates, and clearer evidence of margin resilience, a buyer could justify USD 14-15m.

The bigger point is this: two door businesses with the same USD 10m revenue can be worth very different amounts. Revenue gets you onto the field. Revenue quality, margin profile, and strategic position determine where you land on it.

8. Where Your Business Might Fit (Self-Assessment Framework)

Here is a simple way to pressure-test your likely position in the valuation range. Score each factor as:

- 0 = weak

- 1 = acceptable

- 2 = strong

Be honest. The point is not to flatter yourself. The point is to identify what is holding your valuation back.

How to interpret your score

- 0-8 points: You are likely closer to the lower end of the valuation spectrum. A sale is still possible, but preparation could materially improve outcome.

- 9-15 points: You are in fair-market territory. With a good process and a strong story, you should be able to defend a solid range.

- 16-24 points: You are moving toward premium territory. Buyers are more likely to see strategic upside, not just current earnings.

The most useful part of this exercise is usually not the total score. It is seeing which one or two factors are stopping you from moving up the curve.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders sometimes go to market before the numbers are organized, before the growth story is clear, or before customer and margin trends are easy to explain. Buyers then fill in the gaps with caution, and caution usually lowers value.

Another major mistake is hiding problems. If there are margin issues, a customer concentration problem, warranty exposure, certification gaps, or a weak manager under the founder, it will come out in diligence. When buyers discover problems late, value often drops twice - once for the issue itself and again because trust is damaged.

Weak financial records are another avoidable value leak. In this sector, buyers want to see revenue by product line, customer segment, project type, service vs product mix, gross margin trends, and normalized EBITDA. If your books blur those together, buyers assume risk and price accordingly. Often, 6-12 months is enough time to clean this up.

A lack of a structured, competitive sale process can also hurt price badly. Research across M&A markets consistently shows that a competitive process run by an advisor tends to produce meaningfully higher purchase prices - often around 25% higher - because more buyers see the deal, tension is created, and offers are tested against one another instead of negotiated in isolation.

Another common mistake is naming your price too early. If you tell the market you want USD 10m, many buyers will conveniently come back with USD 10.1m or USD 10.2m instead of telling you what they might really pay in a competitive situation. Good process creates price discovery. Early anchoring kills it.

There are also industry-specific mistakes. One is failing to document certifications, fire ratings, approvals, testing, and installation quality in a way buyers can diligence quickly. Another is failing to show installed-base and service opportunity clearly. If buyers cannot see the recurring potential in your business, they will value you like a one-time project supplier.

10. What Door Products & Services Founders Can Do in 6-12 Months to Increase Valuation

You do not need a total reinvention to improve valuation. In most cases, the biggest gains come from making your business easier to believe in.

10.1 Improve the numbers

Start by cleaning up reporting. Break revenue into clear buckets: product sales, installation, service, inspections, repairs, and parts. Show gross margin by line if possible. Track customer concentration, repeat revenue, backlog, and quote conversion. Buyers pay more when they can clearly see what they are buying.

Then focus on margin quality. Tighten pricing discipline, reduce rework, renegotiate key supply terms, and identify jobs or products that destroy margin. Even modest EBITDA improvement can change a buyer's confidence level materially.

10.2 Increase revenue quality

Look for realistic ways to add repeat revenue. That could mean annual inspection programs, service agreements, replacement parts programs, or planned upgrade cycles for existing installations. In this sector, even a modest increase in lifecycle revenue can improve the story significantly.

Also look at where your best repeat customers come from. If hospitals, schools, industrial clients, or property portfolios reorder more often, lean into those segments. A more repeatable customer base is usually worth more than just a bigger but more volatile one.

10.3 Reduce buyer fear

Build management depth so the company does not feel like a one-person show. Clean up supplier exposure. Document certifications, product testing, QA procedures, and warranty history. Make sure your sales pipeline and backlog are easy to understand.

If you have regulatory or compliance strengths, prove them with evidence. Buyers will not pay for "we think this matters." They pay for repeatable proof - framework wins, approved supplier status, audited credentials, and customer references in high-stakes applications.

10.4 Strengthen your strategic narrative

Think about how your business should be framed. Are you just a manufacturer, or are you a specialist in compliant building access? Are you just an installer, or do you own the lifecycle relationship around safety-critical openings? The story matters because it affects which buyers show up and what they think they can do with your business.

You should also map logical acquirers early. Some buyers will only see a steady building products company. Others may see channel expansion, product bundling, access-control adjacency, or service pull-through. The more clearly that fit is articulated, the stronger the process usually becomes.

10.5 Prepare for the process, not just the meeting

Create a real data room. Prepare normalized financials. Build a clean management presentation. Decide how you will explain cyclicality, margin changes, customer wins and losses, certifications, and service attach rates. The best sale outcomes are often won in preparation, not in negotiation.

11. How an AI-Native M&A Advisor Helps

A strong outcome in this sector usually comes from running a better process, not just telling a better story. That starts with buyer coverage. An AI-native M&A advisor can expand the buyer universe from a short manual list to hundreds of qualified acquirers, screened based on deal history, strategic fit, financial capacity, sector adjacency, and likely synergies. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes even if one buyer drops out.

Speed matters too. With AI helping on buyer matching, outreach, marketing materials, and diligence support, founders can often reach initial conversations and first offers in under 6 weeks. That does not mean cutting corners. It means reducing manual delay and moving faster with better information.

The human part still matters. The best outcomes come from expert M&A advisors who know how to frame a door business in language that buyers trust - supported by AI that improves precision, buyer reach, and execution speed. That combination can deliver Wall Street-grade advisory quality without the cost structure of a traditional bulge bracket bank.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.