The Complete Valuation Playbook for EdTech Businesses

A practical guide to how EdTech businesses are valued and what drives higher multiples.

If you are an EdTech founder thinking about a sale in the next 1-12 months, valuation is not just a finance exercise. It is the market’s judgment on your growth quality, your revenue durability, your customer stickiness, and how strategically useful your business looks to the next owner.

That matters even more in EdTech because buyers are selective. They do not value all revenue the same way. A compliance-heavy school software platform, a content-led learning business, an LMS, and an education IT reseller can all sit inside “EdTech” - but they can trade at very different multiples.

This playbook is built to help you understand what EdTech businesses actually sell for, what drives higher versus lower multiples, where your company may fit today, and what you can do over the next 6-12 months to improve the outcome.

1. What Makes EdTech Unique

EdTech is not one market. It includes school administration software, communication platforms, learning management systems, digital courseware, assessment and proctoring tools, tutoring and study platforms, education IT infrastructure, and services-heavy education support businesses. That matters because buyers do not apply one simple “EdTech multiple” across all of them.

The first big difference is revenue quality. Buyers usually pay more for recurring software revenue than for one-off content sales, hardware rollouts, implementation projects, or people-heavy services. In EdTech, many businesses have a mix of subscription software, services, content, onboarding, device sales, and support. That mix can move valuation a lot.

The second difference is customer behavior. In many sectors, small businesses can switch vendors quickly. In EdTech, switching can be slower because the product is embedded in workflows, academic calendars, student records, compliance processes, or teacher habits. When your software becomes part of how a school, university, or training provider actually operates, that tends to help valuation.

The third difference is procurement and risk. EdTech buyers look closely at long sales cycles, budget dependence, government exposure, data privacy, child safety, regulatory compliance, renewal patterns tied to school years, and whether usage is truly mandatory or just “nice to have.” A product that schools like is not the same as a product they cannot easily rip out.

2. What Buyers Look For in an EdTech Business

At a basic level, buyers still care about the usual things: revenue scale, growth, margins, cash generation, and whether customers stay. But in EdTech, they also care about where your product sits in the institution’s workflow.

If your business helps a school or institution manage records, scheduling, communication, payments, student data, compliance, or core teaching delivery, buyers usually view that as more valuable than a tool that sits on the edge of the workflow. Core systems are harder to replace. They are also more likely to expand across departments and campuses.

Buyers also pay close attention to revenue visibility. They want to know how much of your revenue repeats every year, how contracts renew, how much comes from upsells versus new logos, and whether customer demand depends on constant sales effort. A business with strong retention can be far more valuable than a faster-growing business with weak renewals.

Customer mix matters too. A business serving many schools, districts, institutions, or enterprise training customers is usually more attractive than one that depends on a few large contracts. Heavy concentration is a valuation risk. So is overdependence on one geography, one distributor, one curriculum partner, or one funding program.

How private equity thinks about your business

Private equity buyers usually ask a simple question: “If we buy this business now, who can we sell it to in 3-7 years, and why would they pay more than we paid?” That means they care a lot about entry multiple versus exit multiple.

They will look for clear value-creation levers. In EdTech, those often include raising prices carefully, improving renewal rates, cross-selling more modules into existing institutions, reducing services intensity, improving gross margin, expanding geographically, or making tuck-in acquisitions.

They also care about whether your business can become a platform. A single-product EdTech company can still sell well, but a multi-module company with room to add adjacent tools is often more interesting. That is especially true if the buyer can imagine selling the company later to a strategic acquirer, a larger private equity fund, or in some cases the public market.

3. Deep Dive: Why Revenue Quality Matters More Than Headline Growth in EdTech

Many founders focus first on top-line growth. That is understandable. But in EdTech, buyers often care just as much about the type of revenue you have as how fast it is growing.

The source data shows this clearly. Software-led education administration assets and high-margin digital learning businesses can achieve meaningfully better outcomes than infrastructure, hardware, or services-led businesses. The reason is simple: recurring software or content subscriptions are easier to scale, easier to forecast, and usually produce stronger margins over time. Services-heavy and rollout-heavy businesses may still be good companies, but buyers usually treat that revenue as less durable and less scalable.

Compliance and workflow depth amplify this effect. A school communication or administration platform that handles sensitive records, parent communication, timetabling, grading, or regulated data can become very sticky. That stickiness is not just about customer happiness. It is about switching pain. When a buyer believes your product is embedded and hard to replace, the business starts to look more like a durable software asset and less like a vendor relationship.

That is why high gross margin alone is not enough. The premium outcomes in the data appear where software economics are paired with recurring revenue density, workflow embedment, and believable retention. A founder saying “we are used by thousands of institutions” is not enough by itself. Buyers want to know how many of those institutions pay meaningfully, renew consistently, and buy more over time.

A useful way to think about it is this:

If your business looks more like the left side today, the goal is not to reinvent the company overnight. It is to move steadily rightward. That may mean packaging more of your offer into annual subscriptions, reducing custom work, tying the product more tightly into core school workflows, improving renewal discipline, and proving that customers expand after the first sale.

4. What EdTech Businesses Sell For - and What Public Markets Show

The data does not support one simple EdTech valuation rule. Private deals show a fairly wide range depending on business model, and public markets show the same thing. Software-led, sticky, higher-margin assets tend to sit higher. Hardware, services, and more volatile education models tend to sit lower.

The right way to use the data is not to hunt for one flattering multiple. It is to find the band that best matches your business model, margin profile, and buyer story.

4.1 Private Market Deals (Similar Acquisitions)

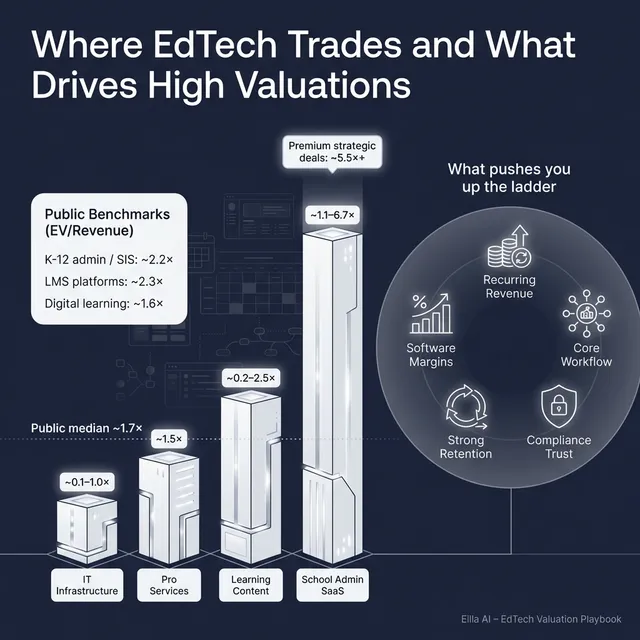

In the private market data, the overall average is about 1.7x EV/Revenue and the median is about 1.1x. But that headline number hides major variation. Education administration SaaS deals in the sample sit meaningfully above services-led and infrastructure-led transactions, while services-heavy and rollout-heavy deals cluster closer to low revenue multiples.

The most relevant signal for a typical software-led EdTech founder is that education administration SaaS assets in the source set show a broad range from roughly 1.1x to 6.7x revenue, with a more realistic practical middle band below that top end unless the asset has very strong recurring revenue, retention, and strategic value. Digital learning content and courseware deals in the sample are mixed - some sit in the low 1x to mid-2x range, while stronger or more strategic assets can clear higher levels. Infrastructure and systems integration deals are typically lower because the revenue mix is more operational and less software-like.

These are illustrative ranges, not a price list. A small but sticky vertical SaaS business can beat a larger but messier content or services business. Likewise, a software company with weak retention or heavy service delivery can still fall toward the low end.

4.2 Public Companies

The public market set is also very wide. Across the whole sample, the average EV/Revenue is about 10.3x, but the median is only about 1.7x. That tells you there are some very high outliers, so founders should not anchor on averages alone. The median is often more useful.

Looking by segment, public K-12 administration and communication platforms, learning platforms, and some digital learning assets often trade in the low-single-digit revenue range, while infrastructure and more operational businesses can be lower or more inconsistent. A few public names in assessment, AI-led learning, or niche strategic categories trade much higher, but those are not good default anchors for a private company.

As of mid to late 2025 in your source set, the public market picture looks roughly like this:

* Based on companies in the sample with usable EBITDA multiples.** Strongly skewed by extreme outliers, so not a reliable anchor for ordinary private company valuation.

The practical takeaway is simple. Public multiples are a reference band, not your sale price. Private companies are usually adjusted downward for smaller scale, lower liquidity, weaker margins, less predictable governance, and higher customer concentration. But great private assets can sometimes push upward if they are scarce, highly strategic, or create a clear acquisition opportunity for a larger buyer.

5. What Drives High Valuations (Premium Valuation Drivers)

The best EdTech valuations usually do not come from one magic metric. They come from a pattern: strong recurring revenue, clear workflow importance, healthy margins, believable retention, and a story a buyer can underwrite.

5.1 Mission-critical workflow position

Buyers pay more when your product sits close to the institution’s daily operating system. In EdTech, that often means communication, scheduling, records, curriculum management, grading, compliance, assessments, or core course delivery.

A product that helps schools “work” tends to be valued more highly than a product that simply helps them “experiment.” The closer you are to core operations, the harder you are to replace.

5.2 Compliance and data trust

The source data points to compliance-grade data handling as an important positive factor, especially where records, privacy, and regulated workflows matter. In school and education contexts, that can create real switching costs.

Buyers like businesses that reduce customer risk. If your platform is trusted with sensitive student data, institutional records, or regulated communications, you are not just selling software - you are selling trust and continuity.

5.3 High gross margin with a believable path to more EBITDA

Premium outcomes in the data tend to cluster around businesses with software-like economics. High gross margin signals that the business can scale without adding cost in a straight line.

But buyers want more than margin on paper. They want a believable path from gross profit to EBITDA. That means disciplined hiring, controlled service costs, and proof that each additional dollar of revenue carries better economics than the last.

5.4 Real recurring revenue, not just repeat customers

There is a big difference between “customers often come back” and “customers are contractually recurring and renew predictably.” Buyers pay more for the second one.

In practice, that means annual subscriptions, multi-year contracts, usage patterns that survive budget cycles, and evidence that customers stay on the platform rather than rebuying only when they have a specific need.

5.5 Institutional scale and distribution reach

The data suggests buyers value scaled institutional reach, especially when it is hard to replicate. A broad footprint across schools, districts, universities, or training providers can become strategically important.

But buyers will test the quality of that footprint. It is not enough to say you serve thousands of institutions. They will ask how many are paying, how much they pay, how deeply they use the product, and how often they renew.

5.6 Earn-out readiness and measurable growth story

Some of the premium patterns in the data involve earn-outs or contingent value tied to ARR growth. That tells you something important: buyers will often pay more when growth is measurable and they can protect themselves if it does not show up.

For founders, this means clean KPI reporting matters. If you can show recurring revenue, renewal rates, expansion revenue, implementation timelines, and cohort behavior clearly, buyers are more willing to stretch.

5.7 The basics still matter

Founders sometimes skip over the fundamentals because they sound boring. They are not boring to buyers.

Clean financials, low customer concentration, clear revenue recognition, consistent sales reporting, a strong leadership bench, and a business that does not depend entirely on you all help move a company toward the top end of the range.

6. Discount Drivers (What Lowers Multiples)

The lowest valuations in EdTech usually happen when buyers see uncertainty, not just weak growth. They discount what they cannot trust, what they cannot forecast, and what they think will be hard to improve.

A common discount driver is a messy revenue mix. If too much of your revenue comes from services, device resale, implementation work, one-off content projects, or custom development, buyers will often treat the business as less scalable. That does not make it unattractive. It just makes it harder to award a premium software multiple.

Another major issue is weak retention or shallow product embedment. If customers can leave easily after the first year, or if the product is not tightly woven into school workflows, buyers worry that growth must constantly be repurchased through sales and marketing.

Thin gross margins also hurt. The source data shows that services and infrastructure-heavy businesses often trade at much lower revenue multiples than software-led models. If you need a lot of people, support, or implementation effort to deliver each sale, buyers will assume margin expansion is harder.

Losses are not always fatal, but unexplained losses are. Buyers can accept current losses if they believe they are temporary and tied to growth investment. They become much less comfortable when the business has no clear path to profitability, unclear pricing discipline, or rising operating costs without evidence of future leverage.

Other common discount drivers include:

- Customer concentration

- Founder dependence in sales, product, or relationships

- Unclear contract terms or weak renewal data

- Poor KPI tracking

- Heavy exposure to one budget cycle, one channel, or one government program

- Claims of “usage” or “institution footprint” without clear paid monetization

- Product sprawl with too much custom work and too little standardization

The good news is that many of these issues can be improved before a sale. Discount factors are often not permanent. They are frequently preparation problems.

7. Valuation Example: A Fictional EdTech Company

Let’s make this concrete with a fictional company.

Assume NorthBridge Schools, a fictional school communication and administration software company, generates USD 10m of annual revenue. This company and this revenue figure are fictional. The valuation ranges below are illustrative and designed only to show how the logic works - they are not investment advice or a formal valuation.

Step 1: Start with the right comp set

Because NorthBridge is a school-focused software platform with communication and admin workflows, the best starting point is not all of EdTech. It is the closer group of education administration SaaS and public K-12 administration / SIS-style businesses.

The source logic points to a broad public range of about 0.9x-5.9x revenue for the closest public category, and a private education administration SaaS range of about 1.6x-4.4x revenue as the more relevant central anchor. After filtering out less relevant categories like infrastructure rollouts, hardware-heavy businesses, and distorted outliers, the most defensible core range for a private company like this is roughly 2.5x-4.5x revenue.

Why not just use the highest public number? Because unless you have strong proof of premium drivers - such as high retention, strong gross margins, deep workflow embedment, and a credible margin story - it is too aggressive.

Step 2: Apply the logic to the fictional company

Now assume NorthBridge has these characteristics:

- Mostly recurring subscription revenue

- Good institutional retention

- Strong gross margins

- Moderate growth

- Limited but not perfect customer concentration

- Some implementation services, but software is the core offer

That points to a reasonable base case in the middle of the private SaaS range.

What would justify each case?

The discounted case is where the business has real weaknesses: lower retention, too much service revenue, unclear margins, customer concentration, weak financial reporting, or a product that is useful but not deeply embedded.

The base case is where most solid private EdTech software businesses land: good recurring revenue, decent growth, reasonable margins, sticky customers, and a believable buyer story, but not enough proof to justify a premium stretch.

The premium case is where you have several strong positives at once: high recurring revenue quality, excellent retention, strong gross margin, clear compliance or workflow moat, diversified customers, and a convincing path to stronger EBITDA. That is where buyers start to think they are not just buying revenue - they are buying a scarce strategic asset.

What this means for founders

Two EdTech businesses can each generate USD 10m of revenue and still be worth very different amounts. One may be worth USD 20-25m. Another may be worth USD 45-55m or more. The revenue number is the same. The quality of that revenue is not.

That is why valuation work matters. The multiple is where the story of your business gets converted into price.

8. Where Your Business Might Fit (Self-Assessment Framework)

A useful self-assessment is not about flattering yourself. It is about seeing where the biggest valuation gaps are.

Score each factor 0, 1, or 2.

- 0 = weak / missing

- 1 = acceptable but not great

- 2 = strong and well evidenced

A simple way to use it:

- 0-8 points: You are likely closer to the low end of the valuation range unless the asset is strategically unique.

- 9-16 points: You are probably in the fair market middle band.

- 17-22 points: You are moving toward premium territory if the data supports the story.

Do not overcomplicate this. The value of this exercise is that it tells you where improvement matters most. A founder with weak retention and messy revenue mix should not spend six months polishing branding. Fixing the core economics will move valuation more.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often start a process before the numbers, materials, and story are ready. That usually leads to weak first impressions, lower offers, and more buyer leverage later in diligence.

Another mistake is hiding problems. Buyers will find churn, weak contracts, margin issues, customer concentration, missing product usage data, security gaps, or inconsistent financials. If you disclose problems clearly and explain the fix, buyers can work with that. If they discover them late, trust falls and value usually falls with it.

Weak financial records are another common value killer. If you cannot clearly separate software revenue from services, show gross margins by revenue type, explain deferred revenue, or prove retention, buyers will assume the risk is higher than it may actually be.

A lack of a structured, competitive sale process can also cost you real money. A well-run process creates buyer tension, improves price discovery, and gives you options if one bidder fades. Market commentary cited by sell-side advisors regularly points to price improvements in the roughly 6%-25% range when sellers run a professional process rather than a one-buyer negotiation. (Aligned IQ)

Another avoidable mistake is telling buyers your target price too early. If you tell the market you want USD 10m of enterprise value, many buyers will simply work backward from that anchor. Instead of discovering what your business is truly worth to them, you may accidentally cap the process yourself.

Two EdTech-specific mistakes are especially common. First, founders overstate “institution footprint” without clearly showing paid penetration, active usage, and renewal quality. Buyers discount vague deployment claims very quickly. Second, founders leave product and compliance documentation messy - security, privacy, student data handling, and implementation standards are too important in EdTech to treat casually.

10. What EdTech Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers actually care about

Start by making the revenue mix cleaner and easier to understand. Separate recurring software revenue from services, implementation, hardware, content projects, and support. If you can reduce one-off revenue dependence and make subscription revenue a larger share of the mix, that usually helps.

Work hard on retention. Even modest improvements in renewal rates can matter because they change how buyers see future revenue. If you can show that customers stay, expand, and become more valuable over time, you move closer to the premium profiles in the data.

Protect gross margin. Reduce unnecessary custom work, standardize onboarding, and be careful about discounting. The more your model looks like software economics instead of custom delivery economics, the better.

Improve the story and reduce risk

Document where your product sits in the workflow. Make it easy for a buyer to see why replacing you would be painful. Show how your platform handles communications, records, scheduling, compliance, or teaching delivery in a way that matters every day.

Tighten your compliance narrative. In EdTech, data privacy and trust are not side issues. Prepare clear documentation on security practices, data handling, contracts, and regulatory alignment. That can reduce buyer fear and improve confidence.

Also reduce customer concentration where possible. If one or two customers dominate the business, try to broaden the base before launch. If you cannot, be ready with a clear explanation and renewal evidence.

Make the business easier to buy

Get your financials into shape. Buyers should be able to understand revenue by product, gross margin by line, renewal behavior, customer cohorts, and your path to EBITDA without guessing.

Build a stronger management bench. If the business depends too heavily on you, buyers will discount it. Delegating customer relationships, product leadership, and operating decisions before a sale can materially help.

Prepare your core sale materials early. That includes a clear equity story, a buyer list, KPI dashboards, and a data room that does not feel rushed.

Position for strategic upside, not just a clean exit

Think about who should buy your company and why. Is your product a natural add-on for a school software platform, an LMS, a digital learning company, or a broader vertical software buyer? The clearer that answer is, the better your process can be run.

If you have room for quick wins, focus on the ones buyers can understand fast: better renewals, stronger cross-sell, clearer module adoption, improved pricing discipline, less services drag, and cleaner reporting. Those are realistic within 6-12 months. A full strategic reinvention usually is not.

11. How an AI-Native M&A Advisor Helps

A strong M&A outcome usually comes from running a disciplined process across a broad buyer universe. An AI-native advisor can widen that buyer universe much more efficiently by identifying hundreds of relevant acquirers based on deal history, strategic fit, financial capacity, and likely synergies. More qualified buyers means more competition, stronger offers, and better odds of closing even if one bidder drops out.

AI also helps compress the timeline. Buyer matching, outreach support, process materials, and diligence preparation can all move faster when much of the heavy lifting is supported by technology. That can help founders get to initial conversations and offers in under 6 weeks, rather than drifting through a slow manual process.

The real advantage is not AI instead of humans. It is expert human advisors enhanced by AI. You still want experienced M&A professionals driving positioning, negotiation, buyer psychology, and process control. What changes is the speed, coverage, and precision. That can give founders Wall Street-grade advisory quality without traditional bulge bracket cost structures.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.