The Complete Valuation Playbook for Elevator and Escalator Solutions Businesses

A practical guide to how elevator and escalator businesses are valued and what drives high multiples.

If you own an elevator and escalator solutions business and are thinking about a sale in the next 1-12 months, valuation is not just about your revenue size. In this sector, buyers look very closely at the mix of maintenance, repair, modernization, installation, route density, safety record, contract quality, and how dependent the business is on a small number of people or accounts.

That matters even more today because the sector is still shaped by steady consolidation, aging installed equipment, growing modernization demand, and buyer preference for dependable service revenue over one-off project work. In plain English: buyers still like the space, but they do not value every elevator business the same way.

This guide is built to help you understand what elevator and escalator businesses actually sell for, what separates higher-multiple businesses from lower-multiple ones, how to roughly assess where your company fits, and what you can do in the next 6-12 months to improve the outcome.

1. What Makes Elevator & Escalator Solutions Businesses Unique

Elevator and escalator solutions businesses sit in a very specific corner of the built-environment market. They are not pure construction companies, and they are not pure manufacturers either. Most private businesses in this sector are some combination of maintenance, repair, callout service, modernization, and installation, with the mix varying a lot from company to company.

That mix matters because recurring maintenance revenue is usually worth more than project-heavy installation revenue. A buyer will usually pay more for a business with a large base of contracted maintenance units, predictable service calls, and recurring modernization opportunities than for one that relies mostly on winning new installation jobs each quarter.

There are several main business types in this market. First are OEM-like businesses that manufacture, install, service, and modernize equipment. Second are independent, multi-brand service and modernization contractors. Third are parts and component suppliers. For most privately held founder-owned businesses coming to market, the closest valuation lens is usually the independent service and modernization contractor model, not the global OEM model.

The sector also has risks that buyers always check. Safety and regulatory compliance are at the top of the list. After that come technician availability, dependence on key supervisors, concentration in a few major property managers or developers, exposure to cyclical new construction, and the quality of maintenance contracts. In this industry, a customer list is not enough - buyers want to know how durable that revenue really is.

2. What Buyers Look For in a Elevator & Escalator Solutions Business

At the simplest level, buyers care about four things: how predictable your revenue is, how profitable the work is, how risky the operation feels, and how much upside they can see after closing. Revenue size and EBITDA matter, but in this sector they are only part of the story.

For an elevator and escalator business, the first question is usually: how much of revenue comes from maintenance and service agreements versus one-off projects? A contracted maintenance base gives buyers confidence. It creates visibility, supports technician planning, and often feeds repair and modernization work later. That is very different from a business that has to re-win revenue every month.

The second question is quality of earnings. Buyers will look at gross margin by service line, technician productivity, callback rates, emergency callout mix, pricing discipline, and whether EBITDA is real or propped up by underpaying the owner, delayed hiring, or unusually low overhead. In other words, they are asking whether current profit can hold up after the sale.

The third question is customer and route quality. A business with dense routes, long-standing customer relationships, multi-year service agreements, and a healthy mix of commercial, institutional, residential, and public-sector accounts often feels more valuable than a scattered book of smaller jobs across a wide geography. Density lowers service costs and improves customer response time.

How private equity buyers think

Private equity buyers usually look at your business through a three-part lens. First, what price do they have to pay today? Second, what can they improve over the next 3-7 years? Third, who can they sell it to later?

That future buyer could be a larger strategic acquirer, a bigger private equity-backed platform, or sometimes another sponsor. To make that work, PE firms usually want to see levers they can pull: annual price increases on maintenance contracts, cross-sell of repairs and modernization, add-on acquisitions in nearby markets, stronger purchasing, tighter scheduling, or better branch-level reporting.

They also care about the gap between entry and exit quality. A business that already has clean reporting, low customer churn, strong margins, and a professional management team may be easier to buy, but it also needs a believable growth path. A business with some messiness can still be attractive, but only if the buyer believes the fixes are achievable and worth the risk.

3. Deep Dive: Why Maintenance Contract Quality and Installed-Base Density Matter So Much

In this industry, not all recurring revenue is equal. Two businesses may both say that maintenance is 60% of revenue, but one can be far more valuable than the other. The difference often comes down to contract quality and installed-base density.

The data points in that direction. The strongest public independent maintainer in the set trades well above broader service peers, while lower-valued field-service and facilities-style businesses tend to have thinner margins and less obvious defensibility. The message is clear: buyers pay more when maintenance revenue is not just recurring in theory, but durable, profitable, and hard to dislodge.

Why do buyers care so much? Because a dense, well-managed maintenance base does three things at once. It stabilizes revenue, improves technician productivity, and creates a built-in pipeline for repairs and modernization. If your technicians can service more units in tighter territories with fewer windshield hours and faster response times, your revenue quality improves and your cost structure gets better too.

Contract quality matters just as much as contract count. Buyers want to know whether agreements are annual or multi-year, how often prices are reset, whether cancellation terms are loose, how many units are loss-making, and whether service levels are consistently met. A large maintenance book with weak pricing and poor margins can actually hurt value.

Founders can move from the lower-value profile to the higher-value profile over time. The practical steps are straightforward: clean up unprofitable contracts, tighten service-level tracking, raise prices where justified, improve route density, and build better visibility by customer, unit, and technician.

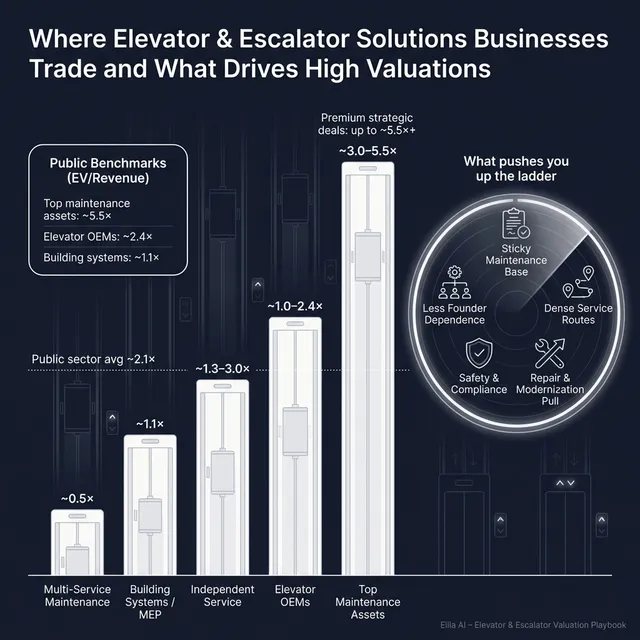

4. What Elevator & Escalator Solutions Businesses Sell For - and What Public Markets Show

The market data does not support one single valuation number for this sector. It supports a range, and that range is wide because business models vary so much. A field-service maintenance contractor, an OEM-like business, a component supplier, and a broader building-services company do not trade alike.

The right way to use the data is to start with the closest business model matches, then adjust for size, growth, profitability, recurring revenue, and risk. For most privately held elevator and escalator solutions businesses, the most relevant reference points are independent maintenance and modernization contractors, plus selected technical services and facilities-engineering businesses.

4.1 Private Market Deals (Similar Acquisitions)

The private deal data shows an overall average of about 1.3x revenue and 7.5x EBITDA, with medians of about 0.4x revenue and 6.2x EBITDA. But those overall figures mix together very different business types, including lower-margin building services and more strategic product-led deals. For elevator-related founder-owned service businesses, that overall average is only a starting point.

The more relevant private comparisons split into two broad groups. First are field-service, lifting, and specialty service businesses, where one directly relevant service-style deal was around 2.3x revenue. Second are broader engineering and lifecycle service businesses, where deals were much lower on revenue - roughly 0.2x to 0.4x revenue and around 6.2x to 11.0x EBITDA in the disclosed examples. That tells founders something important: in services, EBITDA often gives a clearer read than revenue multiples alone.

A practical interpretation is this: if your business is mainly maintenance, repair, modernization, and service, buyers will usually anchor on earnings quality first and revenue quality second. If margins are modest and the business looks like a general contractor with some service work, multiples tend to compress. If the business has a real contracted maintenance base, dense routes, strong safety positioning, and clear modernization pull-through, it can move toward the better end of the range.

These ranges are illustrative, not a price tag. Your exact outcome will depend on your service mix, margin quality, growth, customer stickiness, and the kind of buyer you attract.

4.2 Public Companies

Public markets as of mid-to-end 2025 show a similar pattern: business model matters more than the label on the door. Across the full public set, average trading levels were about 2.1x revenue and 16.3x EBITDA, with medians of about 1.3x revenue and 9.0x EBITDA. But those broad figures again mix OEMs, maintenance contractors, building-services companies, and related equipment businesses.

The strongest public valuation in the directly relevant maintenance category comes from the independent maintainer group, where the standout player trades around 5.5x revenue and 24.8x EBITDA. That is far above most general building-services peers and reflects scale, growth, and very strong margins. By contrast, elevator OEMs in the data mostly sit closer to roughly 1.0x-2.6x revenue and around 8.6x-14.2x EBITDA, with a few outliers. Broader facilities and building engineering businesses generally trade lower on revenue, often around 0.1x-2.5x, depending on profitability and quality.

For founders, the lesson is simple. Public multiples are useful reference bands, not direct sale prices. A small private company should usually trade below the best public comparables because it is smaller, less liquid, and often riskier. But a scarce, highly strategic private asset with a strong installed base and obvious buyer synergies can sometimes punch above where a generic service business would trade.

You should use public multiples in two ways. First, as a reality check on what the market rewards. Second, as a reminder that buyers adjust down for smaller scale, weaker margins, lower growth, or customer concentration. The reverse can also be true: if your business is rare, strategic, and clearly better than typical peers, the public market is not necessarily your ceiling.

5. What Drives High Valuations (Premium Valuation Drivers)

Higher valuations in this sector usually come from a combination of revenue quality, defensibility, and buyer-specific strategic value. It is rarely one single metric.

A large, sticky maintenance base

Buyers pay more for businesses where maintenance revenue is truly recurring and hard to replace. In this sector, that usually means a meaningful base of contracted units, low churn, predictable renewal patterns, and a history of turning maintenance relationships into repairs and modernization work.

A founder-friendly way to think about this is simple: buyers want to see that your customer book behaves like an asset, not a monthly sales challenge.

Safety-critical positioning with real service reliability

The source data highlights a recurring pattern around safety, compliance, and rapid response. Businesses positioned around safety-critical work and 24/7 responsiveness can earn better outcomes when that positioning translates into real customer stickiness, pricing power, and dependable service revenue.

That only works when it is measurable. If you can show response times, uptime, low claims, strong renewal rates, and low customer losses, buyers are more likely to believe your premium story. If it is just marketing language, they will treat it as table stakes.

Strong, repeatable profitability

The data also shows that even in service-heavy businesses, margins matter a lot. Buyers do not automatically pay premium multiples for maintenance services. They pay more when they believe your margins are real, repeatable, and not vulnerable to labor shortages, underpricing, or owner heroics.

In practice, that means showing clean branch economics, disciplined pricing, route efficiency, and stable labor performance. If your profit comes from cutting corners or deferring investment, buyers will discount it.

Strategic scarcity

The highest revenue-multiple outcome in the private set came from a product-led deal where the buyer likely cared more about strategic fit than current earnings. The same idea can apply in elevator and escalator services when a business offers something scarce: a dense installed base in an attractive region, access to a hard-to-penetrate customer segment, a strong modernization niche, or a credible platform for further acquisitions.

This is where deal narrative matters. Instead of presenting your business as "a solid maintenance contractor," the better framing might be "a hard-to-replicate regional installed-base platform with strong modernization pull-through."

Scale and service breadth

The premium EV/EBITDA example in the data came from a large, diversified lifecycle services business. Scale can create better customer retention, wider service capability, improved purchasing, and more resilience when one end market softens.

You do not need to be huge to benefit from this. Even a smaller founder-owned business can improve its valuation by expanding from pure reactive maintenance into a fuller lifecycle offer: inspection support, planned repair, modernization, monitoring, and selected adjacent services that make the customer relationship deeper.

Clean operation and deal readiness

Some premium drivers are not glamorous, but they still matter. Buyers pay more when your financials are clean, customer contracts are organized, margins are reported by service line, and there is a management team beyond the founder. A business that feels easy to diligence often gets better offers than one with similar economics but messy information.

6. Discount Drivers (What Lowers Multiples)

Most lower-multiple outcomes are not caused by one fatal flaw. They are caused by a stack of smaller concerns that make a buyer cautious.

The first common discount driver is too much exposure to one-off installation or project work. Installation can be valuable, but if the business relies heavily on construction cycles and re-winning jobs rather than contracted service revenue, buyers will view cash flow as less predictable.

The second is weak profitability or margins that buyers do not trust. In this sector, modest EBITDA margins often pull a business closer to general technical services or facilities contractors rather than premium maintenance specialists. If profit is inconsistent, branch reporting is weak, or technician labor is not well controlled, buyers will underwrite conservatively.

Another frequent discount is customer concentration. If a few building owners, property managers, developers, or public contracts make up too much of revenue, buyers worry about what happens after closing. The same applies if the founder personally owns most of those relationships.

Route sprawl is another hidden value killer. A service business with technicians driving all over a large geography may show decent revenue but weak service economics. Buyers notice this quickly because it hurts margins, response time, and future scalability.

A few more red flags tend to drag value down:

- poor documentation of maintenance agreements

- high callback or claim rates

- weak safety systems

- dependence on one or two technical leaders

- outdated ERP or service software

- aggressive revenue recognition

- too much working-capital volatility

- unresolved legal, licensing, or compliance issues

The good news is that many of these issues can be improved before a sale. A discount driver is not necessarily permanent. It is often a sign that preparation work has not been done yet.

7. Valuation Example: A Elevator & Escalator Solutions Company

To show how the logic works, let’s use a fictional company called Summit Vertical Services. This is not a real company, and the numbers below are illustrative only. Assume Summit generates USD 10m of revenue and is an established independent, multi-brand elevator business focused on maintenance, repair, modernization, and selected installation work.

Step 1: Start with the right comparison set

Because Summit is a service-led independent contractor, the best starting point is not the large OEM group and not the parts manufacturers. The closest references are independent maintenance and modernization businesses, plus field-service and technical-services companies with similar labor and contract dynamics.

The source data’s worked example for a real service-led lift contractor pointed to a defensible EV range of roughly USD 14m-22m on USD 22.8m revenue, using an EBITDA-based approach as the main anchor. The reason was straightforward: revenue multiples were too wide and too distorted by business-model differences, while EBITDA multiples better reflected real profitability for a smaller contractor.

Step 2: Build a core range

In the source example, the company had EBITDA of about USD 2.0m on USD 22.8m revenue, or an EBITDA margin of about 8.6%, and the narrowed range was based on roughly 7.0x-11.0x EBITDA. That produced the USD 14m-22m range.

For Summit, let’s assume a similar margin profile: USD 10m revenue and USD 0.9m EBITDA, or roughly 9% EBITDA margin. Applying the same logic gives a sensible core range.

Step 3: Adjust up or down based on business quality

If Summit has a strong contracted maintenance base, good route density, low customer churn, clean financials, and clear modernization pull-through, it can move toward the upper end of the range. If instead it has scattered routes, weak contract terms, customer concentration, or margin quality concerns, it can move lower.

Here is a simple worked example:

Assuming EBITDA of USD 0.9m, that means:

- Discounted case: about USD 5.0m-5.9m

- Core case: about USD 6.3m-8.1m

- Premium case: about USD 9.0m-9.9m

This example shows why two elevator businesses with the same revenue can be worth very different amounts. The gap usually comes from revenue quality, contract quality, route density, customer diversification, and how believable the earnings are. This is not investment advice or a formal valuation - it is just a practical illustration of how buyers often think.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple way to use this playbook is to score yourself honestly across the factors that most affect value. Give each factor a score of 0, 1, or 2.

- 0 = weak / unclear

- 1 = decent but not standout

- 2 = strong and well-supported

A rough way to interpret the score:

- 18-24: closer to premium territory

- 11-17: fair market range

- 0-10: likely more work needed before selling

This is not meant to produce a precise valuation. It is meant to help you see where the biggest gains are. In this industry, a few high-impact improvements usually matter more than many minor ones.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders sometimes go to market before the numbers, contracts, and deal story are ready. Buyers then fill in the gaps with caution, and caution usually means a lower offer.

Another major mistake is hiding problems. In elevator and escalator services, issues around safety incidents, contract losses, technician turnover, pricing problems, or customer concentration almost always surface in diligence. If they come out late, buyers lose trust and often retrade the deal.

A third mistake is weak financial records. If you cannot clearly show maintenance revenue, repair revenue, modernization revenue, installation revenue, gross margins by service line, and normalized EBITDA, you make it hard for buyers to underwrite your business confidently. Many valuation gains come from simply presenting the business more clearly.

A fourth mistake is running an unstructured sale process. Businesses that are marketed through a structured, competitive process with an advisor typically achieve meaningfully better outcomes than those negotiated with one buyer in isolation. Research and market practice consistently support the idea that a well-run competitive process can increase purchase prices by around 25% because it improves price discovery and negotiating leverage.

Another mistake is telling buyers the price you want too early. If you say you want USD 10m, many buyers will anchor around that and come back at USD 10.1m or USD 10.2m rather than telling you what the market might actually pay. Good sale processes let buyers show their hand first.

There are also industry-specific mistakes. One is failing to clean up unprofitable maintenance contracts before launch. Another is not documenting service quality well enough - response times, callback rates, inspection performance, and contract retention all matter in this sector, and weak reporting makes the business feel riskier than it may really be.

10. What Elevator & Escalator Solutions Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers care about most

Start by breaking your revenue into clear buckets: maintenance, repair, modernization, and installation. Then track gross margin and EBITDA contribution by each bucket. Buyers will value you better when they can see what part of the business is recurring, what part is project-based, and where the profit really comes from.

Review maintenance pricing contract by contract. In many founder-owned businesses, some long-standing contracts are simply underpriced. Fixing even a portion of those before a sale can materially improve EBITDA and strengthen your valuation narrative.

Improve the quality of the maintenance base

Focus on contract retention, pricing resets, and route density. If you can make your maintenance book more profitable and more geographically efficient, you improve both margin and defensibility at the same time.

Also look at how maintenance leads to repairs and modernization. Buyers like to see a clear ladder: maintain the unit, identify issues early, win repair work, then win larger modernization projects. That makes the customer relationship more valuable.

Reduce buyer risk

Document your safety systems, claims history, training standards, license compliance, and response-time performance. In this sector, lower perceived risk can matter almost as much as growth.

You should also reduce dependence on the founder. Push customer relationships, branch management, and estimating responsibility deeper into the team. A business that can run without the founder every day is easier to buy.

Improve the sale story

Founders often undersell what makes their business special. Build a clear story around your installed base, route density, modernization pipeline, customer retention, and regional position. Do not just say you are "full service." Show why your service model is durable and why a buyer could grow it.

This is also the time to prepare diligence materials early: contracts, customer schedules, technician data, financial normalization, equipment lists, safety records, and branch KPIs. The cleaner the process feels, the fewer excuses buyers have to chip price later.

Position for the right buyer type

Not every buyer will value the same strengths. A strategic buyer may care most about installed-base density, territory, and customer overlap. A private equity buyer may care more about add-on acquisition potential, management bench, and the ability to improve pricing and operating discipline. Understanding which buyers are likely to value your specific profile can make a major difference.

11. How an AI-Native M&A Advisor Helps

A modern sale process is no longer just about knowing a handful of buyers. An AI-native M&A advisor can expand the buyer universe from a short list to hundreds of qualified acquirers based on real signals like deal history, strategic fit, financial capacity, geography, and likely synergies. More relevant buyers means more competition, stronger offers, and a better chance your deal closes even if one buyer drops out.

It also speeds up the process. With AI helping buyer matching, outreach, marketing material preparation, and support through diligence, initial conversations and first offers can often be reached much faster than in a manual-only process - often in under 6 weeks. Speed matters because it keeps momentum high and reduces the risk of deal fatigue.

The best model is not AI alone. It is expert human advisors enhanced by AI. That means experienced M&A professionals running the process, shaping the deal story, preparing materials that speak the buyer’s language, and negotiating from a position of strength - while AI does the heavy lifting behind the scenes. The result is Wall Street-grade advisory quality without the cost structure and slowness of a traditional bulge-bracket approach.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.