The Complete Valuation Playbook for Energy Management Businesses

A data-driven guide to how energy management businesses are valued and what drives high multiples.

If you are thinking about a sale in the next 1-12 months, valuation is not just a finance question. It is a strategy question. In energy management, buyers are active, the market is still consolidating, and the gap between a premium asset and an average asset can be very wide even when revenue is similar.

This playbook is built to help you understand three things: what energy management businesses actually sell for, what drives higher versus lower multiples, and what you can realistically do over the next 6-12 months to improve your position before going to market.

The numbers below are based on the source set you provided, combined with practical M&A judgment from how buyers usually assess businesses in this sector. The goal is not to predict one exact price. It is to show you how buyers think.

1. What Makes Energy Management Unique

Energy management is not one neat category. It includes software platforms for utilities and buildings, connected asset and IoT platforms, demand response and virtual power plant software, building and industrial controls, advisory and consulting firms, efficiency retrofit providers, and project-led interconnection or infrastructure delivery businesses.

That matters because buyers do not value all of these the same way. A software-led platform with recurring subscriptions, deep integrations, and a real role in operating energy assets will usually be valued very differently from a project-led installer, an EPC-style contractor, or a consulting-heavy business. The headline phrase "energy management" hides very different revenue quality.

There are also sector-specific issues buyers always check. They want to know whether your product is embedded in customer operations, whether savings claims are real and provable, whether your contracts renew, whether your integrations are hard to rip out, and whether your revenue depends on a handful of customers, policy incentives, or one-off projects.

In this sector, valuation is shaped by a few recurring questions:

- Are you software, services, projects, or some mix of all three?

- Are you mission-critical to customer operations, or nice-to-have?

- Are your economics recurring and visible, or lumpy and forecast-driven?

- Are you reducing real operational risk, or mainly selling labor?

Those questions carry more weight here than in many other industries.

2. What Buyers Look For in an Energy Management Business

At a basic level, buyers look for the same things they look for in most deals: revenue scale, growth, gross margin, EBITDA, customer retention, and a believable path to future growth. But in energy management, they look at those through a very specific lens.

First, they care about revenue quality. A buyer will usually pay more for contracted software, long-term monitoring, data subscriptions, or recurring optimization services than for hardware resale, implementation fees, engineering projects, or one-time audits. Two companies can both have USD 10m of revenue, but if one is 80% recurring software and the other is 70% project work, the market will not value them the same way.

Second, they care about operational importance. If your platform helps control loads, manage distributed assets, automate billing or customer operations, or keep critical systems compliant and secure, you sit closer to the customer's "must keep running" layer. Buyers like that because it creates stickiness and makes replacement painful.

Third, they care about proof. In this sector, founders often tell a strong story about decarbonization, optimization, flexibility, or energy savings. Buyers still want evidence. They want to see retention data, contract length, net revenue expansion, deployment depth, reference customers, installed base, margin by product line, and a clear explanation of what part of the value chain you actually own.

Private equity buyer thinking

Private equity buyers are usually asking three simple questions.

The first is entry price versus exit price. If they buy you at a healthy multiple today, they need a clear reason why someone else will pay a similar or better multiple in 3-7 years. That means they care a lot about whether you can become a more software-like, more recurring, more scalable business over time.

The second is resale path. They want to know who buys this business after them. A larger software platform? A strategic automation player? A larger PE-backed platform? In rare cases, a public market story? If there is no obvious next buyer, valuation usually suffers.

The third is value creation. PE buyers will think about price increases, cross-sell, upsell into the installed base, operational efficiency, tuck-in acquisitions, and professionalizing the sales engine. In energy management, they especially like businesses where service relationships can be turned into software subscriptions or long-term monitoring contracts.

3. Deep Dive: Control Layer + Recurring Revenue vs Project Tool + Services Revenue

One of the biggest valuation questions in energy management is this: are you part of the customer's operating system, or are you mainly a project vendor?

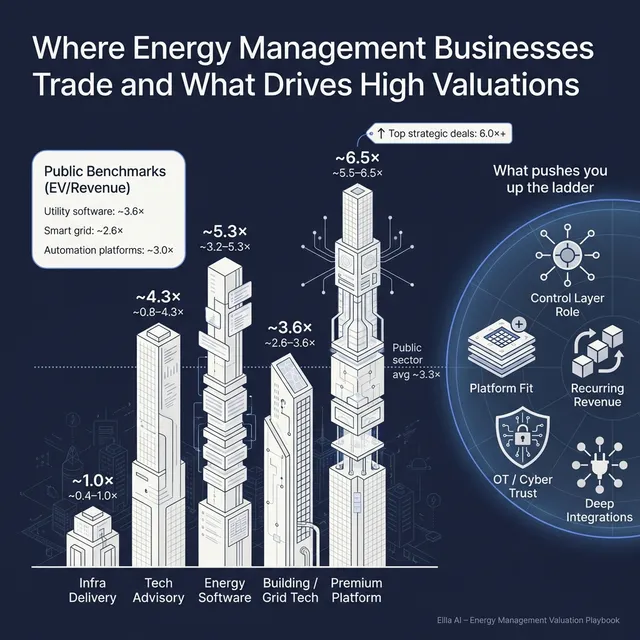

The data strongly supports this distinction. In your source set, the strongest software-led outcomes came from businesses with high recurring revenue or a clear platform role. One software asset with very high annual recurring revenue relative to total revenue sold on a meaningfully higher software multiple. The premium drivers also point in the same direction: buyers pay attention to control-plane leverage, end-to-end platform logic, and recurring software revenue.

By contrast, project-heavy and services-heavy businesses usually traded much lower. In the precedent transaction set, the overall average was 1.7x revenue and the median was 0.9x. That sounds low until you realize the data mixes software assets with EPC, consulting, retrofit, and project delivery companies. Once you separate those categories, the picture changes a lot.

Why do buyers care so much about this distinction? Because recurring revenue is easier to underwrite. It is more visible, more financeable, and usually more scalable. And if your system controls or coordinates energy flows, connected devices, or critical operations, the buyer is not just buying revenue - they are buying a position inside the customer's workflow that is harder to remove.

A simple way to think about it:

If your business looks more like the left side today, the goal is not to reinvent the company overnight. The goal is to move one step right. That could mean turning monitoring into a subscription, separating implementation from software fees, standardizing contracts, deepening integrations, or proving that your platform affects real operating decisions rather than just reporting after the fact.

4. What Energy Management Businesses Sell For - and What Public Markets Show

Here is what the data actually shows. The biggest mistake founders make is grabbing one attractive software multiple and assuming it applies to the whole sector. It does not. In energy management, the valuation spread is wide because the business models are wide.

The better way to use valuation data is to compare yourself to the right operating model first, then adjust for growth, margin, customer quality, and strategic value.

4.1 Private Market Deals (Similar Acquisitions)

The private transaction data shows a clear split between software-led assets and service or project-led assets. The software-led energy management and connected asset platforms in your source set support the best multiples. Project delivery, EPC, interconnection, and implementation-heavy businesses generally trade much lower. Services and advisory firms sit in the middle, but only reach stronger outcomes when they offer specialist expertise that reduces real risk for customers.

The overall private deal set averaged 1.7x revenue with a 0.9x median. But that overall number hides the more useful pattern: software-like assets can command materially higher revenue multiples than services-heavy or project-heavy peers.

A few practical takeaways stand out. First, earnouts are common in this sector. That usually means buyers see upside, but they also see uncertainty. Second, premium service outcomes are possible, but only when the service is specialized enough to reduce technical, quality, compliance, or supply-chain risk. Third, software stories only get software multiples when the buyer believes the revenue really behaves like software.

These ranges are illustrative, not a formal valuation. Your exact outcome depends on how your business actually looks in a buyer's model.

4.2 Public Companies

Public markets provide a useful reference point, but not a direct price tag for private companies. As of mid-to-late 2025, the overall public comp set in your source data traded at about 3.3x EV / Revenue on average, with a 2.4x median, and about 24.1x EV / EBITDA on average, with a 15.2x median.

For energy management founders, the most relevant public buckets are utility software, smart grid platforms, building and industrial automation platforms, and services-led digital transformation firms. Hardware-heavy metering, OEM, and utility generation businesses are useful context, but they are usually less relevant unless your model is similarly capital-intensive or product-hardware-heavy.

There are two important cautions here. First, public companies are usually much larger, more diversified, and more liquid than private businesses. That means founders should use these figures as a reference band, not as proof of what a buyer must pay.

Second, public multiples still need adjustment. Smaller businesses are usually adjusted down for scale, concentration, and execution risk. But scarce assets can sometimes push above the normal private range if a buyer sees strategic value, especially if your platform sits in a control layer, has strong recurring revenue, and can be used to cross-sell into an installed base.

5. What Drives High Valuations (Premium Valuation Drivers)

The data points to a handful of themes that move energy management businesses toward the top of the range.

5.1 You sit in the control layer, not just the reporting layer

Buyers pay more when your product helps orchestrate, control, or automate energy assets and workflows across a real installed base. The premium driver here is not just "software." It is software with operational authority.

That is why buyers get interested in businesses tied to telemetry, SCADA, distributed energy orchestration, device connectivity, or billing and customer operations. These systems are painful to replace once embedded.

Examples founders can relate to:

- Your platform dispatches or coordinates loads, batteries, EV charging, or flexible devices.

- You are integrated into utility or building operations, not just producing monthly reports.

- Removing your software would disrupt compliance, billing, control, or uptime.

5.2 Your revenue behaves like software

The cleanest premium signal in the source set is recurring revenue quality. High ARR, multi-year contracts, strong renewals, and predictable expansion inside the customer base all support better valuations.

Buyers are not just paying for current revenue. They are paying for confidence that the revenue will still be there after the deal closes. That confidence rises when the contracts are recurring and the product is embedded.

Examples:

- A customer signs a three-year monitoring and optimization contract rather than a one-off implementation.

- Software fees are separated clearly from services fees.

- Existing customers add more sites, assets, or modules over time.

5.3 You fit into a larger platform strategy

Several deals in the source set were clearly framed as part of building an end-to-end platform. Buyers like assets that can widen their product suite, deepen their customer relationships, and create cross-sell.

This matters especially in energy management because the value chain is fragmented. A buyer may already have controls, field services, analytics, billing software, or industrial communications. If your business fills a missing piece, that can improve your valuation even when your current scale is modest.

Examples:

- You connect building controls with energy analytics and sustainability reporting.

- You bridge device data with customer billing or optimization workflows.

- You can be bundled with a larger buyer's installed base.

5.4 You reduce technical and operational risk

Premium service valuations are possible when the service itself is a de-risking layer. In the source set, scaled technical advisory with a deep engineering bench achieved a much better outcome than typical consulting.

In energy management, risk reduction matters. Buyers pay more for businesses that help customers avoid operational failure, poor-quality deployments, compliance problems, cybersecurity issues, or bad equipment decisions.

Examples:

- You provide highly technical engineering oversight rather than generic consulting.

- Your team is trusted to sign off on performance-critical work.

- You have a strong record in regulated, industrial, or utility environments.

5.5 You have OT/IT and cybersecurity credibility

The source data also highlights OT/IT convergence and cybersecurity as a valuation accelerant when it is real and proven. This is especially true in utility and industrial environments where failure is not just inconvenient - it is costly and risky.

This does not mean buyers will pay more just because cybersecurity is on a slide. It means they may pay more if you can show real deployments, certifications, resilient architecture, and a history of operating in sensitive environments.

Examples:

- You have referenceable deployments in utility or industrial settings.

- Your product architecture is designed for secure field connectivity.

- Cybersecurity is built into the offering, not bolted on in marketing language.

5.6 Clean basics still matter

Founders sometimes focus so much on strategic positioning that they forget the obvious. Buyers still pay more for clean financials, diversified customers, strong gross margins, low churn, a capable leadership bench, and a business that can run without the founder in every room.

These things do not sound exciting, but they directly affect deal confidence. Deal confidence affects price.

6. Discount Drivers (What Lowers Multiples)

Lower valuations usually come from some combination of weak revenue quality, weak visibility, and weak trust.

The biggest discount driver is project-heavy revenue. If your sales depend on one-off installations, custom engineering jobs, or a backlog that has to be constantly refilled, buyers will usually pay less. That does not make the business bad. It just makes future revenue harder to underwrite.

Another common issue is mixed or muddy business models. If a buyer cannot quickly understand what portion of revenue is software, services, hardware, maintenance, and pass-through, they usually assume the worst. Confusion lowers confidence, and lower confidence lowers valuation.

Customer concentration also matters a lot in this sector. Many energy management businesses have a few large utility, real estate, industrial, or public-sector customers. If one contract represents too much revenue, the buyer will focus hard on renewal risk, procurement cycles, and relationship dependency.

Other common discount drivers include:

- Low or inconsistent gross margin

- Weak retention or no proof of contract renewals

- Founder-led sales with no repeatable commercial engine

- Heavy customization for every deployment

- Exposure to policy, subsidy, or procurement timing risk

- Hardware resale or pass-through revenue inflating top line

- Weak cybersecurity posture in operational environments

- Poor KPI reporting on sites, devices, users, or customer savings

Earnouts are also worth mentioning here. In your data, contingent consideration showed up across many deals. That tells you something important: buyers often use earnouts to bridge uncertainty. A big headline price with a large earnout is not the same thing as cash at close.

The good news is that many discount drivers are fixable. Better segmentation, better contracts, cleaner reporting, clearer product packaging, and stronger customer evidence can all improve how buyers view the same revenue base.

7. Valuation Example: A Fictional Energy Management Company

Let’s make this concrete with a fictional example.

Assume a fictional company called GridPilot, with USD 10m of annual revenue. GridPilot sells software to commercial and utility customers that helps monitor distributed assets, automate energy optimization, and connect field devices into customer operations. This company is fictional, the revenue figure is fictional, and the valuation ranges below are illustrative only. This is not investment advice or a formal valuation.

7.1 Step 1: Start with the right comp set

For a business like GridPilot, the right starting point is software-led energy management comps, not EPC, hardware-led metering, or consulting businesses.

The source logic points to three relevant anchors:

- Private software-led energy management platforms: about 3.2x-5.3x revenue

- Public utility CIS / billing software: about 3.6x revenue

- Public smart grid platforms: roughly 1.4x-3.6x revenue, but with wider variation and noisier profitability

Because GridPilot is software-led and sits somewhere between customer operations and distributed asset orchestration, the private software-led band is the most useful core anchor. The public utility software point supports the middle of that range.

7.2 Step 2: Build a core range

Using USD 10m of revenue:

- Lower core case: 3.2x revenue = USD 32m EV

- Upper core case: 5.3x revenue = USD 53m EV

That gives a sensible core valuation range of about USD 32m-53m for a software-led energy management asset with a credible platform story.

7.3 Step 3: Adjust up or down based on quality

Now we ask what kind of GridPilot this really is.

If GridPilot has strong recurring revenue, deep integrations, multi-year contracts, solid retention, and clearly acts as part of the customer's control layer, buyers may push it toward the top of the range or slightly above it.

If GridPilot is more implementation-heavy, has weak renewal evidence, depends on a few customers, or relies heavily on founder relationships, buyers will usually pull it down.

7.4 What this means for founders

Two energy management businesses with the same USD 10m of revenue can realistically be worth very different amounts. The difference usually comes down to revenue quality, customer stickiness, strategic position, and risk.

That is why valuation work is not just about picking a multiple. It is about understanding which version of your business the buyer sees.

8. Where Your Business Might Fit (Self-Assessment Framework)

A useful way to think about valuation is to score yourself honestly across three groups: high-impact factors, medium-impact factors, and bonus factors.

Give yourself:

- 0 if the factor is weak

- 1 if it is decent but not standout

- 2 if it is clearly strong

A practical scoring guide:

- 0-8 points: You are likely closer to the lower end of the range. That does not mean you should not sell, but it means preparation matters a lot.

- 9-15 points: You are in fair-market territory. A strong process and clear positioning can still make a big difference.

- 16-24 points: You are closer to premium territory, especially if the buyer universe includes strategic acquirers who value your platform fit.

The point of this exercise is not to flatter yourself. It is to identify which 2-3 improvements would have the biggest impact before a sale.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often wait until they are tired, distracted, or under pressure, then start a process before the numbers, story, and buyer list are ready. That usually leads to weak first offers and less leverage.

Another mistake is hiding problems. If churn is rising, margins are unstable, a major customer is at risk, or a product line is underperforming, it will usually come out in due diligence. When buyers discover issues late, they do not just reduce price - they reduce trust.

Weak financial records are another preventable problem. In this sector, buyers want a clean view of software revenue versus services, gross margin by line, recurring versus non-recurring revenue, customer concentration, and key operating KPIs. If those are messy, the buyer either discounts the deal or asks for protection.

Many founders also run a weak sale process. A structured, competitive process run with an advisor usually produces a meaningfully better outcome than a single-buyer conversation. Research and market evidence commonly show that competitive, advisor-led processes can improve purchase prices by around 25%, because they create real price discovery and pressure.

Related to that, founders often reveal what price they want too early. This is a mistake. If you tell buyers you are hoping for USD 10m of enterprise value, many of them will simply come back at USD 10.1m or USD 10.2m instead of showing you what they may have actually been willing to pay. You kill price discovery when you anchor too early.

A few industry-specific mistakes matter too:

- Packaging hardware pass-through or installation revenue as if it deserves software multiples

- Claiming a "platform" position without clear proof of integrations, usage, retention, or operational dependence

10. What Energy Management Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work usually falls into three buckets: improve the numbers, improve the story, and reduce buyer risk.

10.1 Improve the numbers buyers care about

Start by making revenue quality visible. Separate recurring software, maintenance, monitoring, implementation, hardware, and pass-through revenue. If possible, shift new contracts toward recurring fees and clearer gross margin.

Focus on retention and expansion. Renewals, contract extensions, more sites per customer, more devices per customer, and additional modules all matter. In this sector, a buyer will pay more for revenue that expands inside the installed base than for top-line growth built only on fresh projects.

Margin quality matters too. If you can reduce custom work, standardize deployments, price implementation properly, or improve support efficiency, that helps both EBITDA and confidence.

10.2 Improve the story buyers will underwrite

You need a simple answer to one question: why is this business strategically important?

Build the case that you are a control layer, a system-of-record, or a mission-critical workflow layer - if that is true. Show how the product affects customer operations, not just reporting. Show the cost and disruption of replacement. Show why more modules or sites can be sold into the same customer base.

Also tighten your customer proof. Good case studies in this market are very specific. They show savings, uptime, compliance, automation, faster billing, lower manual work, better dispatch, or lower energy spend. Vague ESG language is not enough.

10.3 Reduce the risks that scare buyers

Reduce concentration where you can. Renew key contracts early. Get reference customers lined up. Formalize cybersecurity, especially if you connect to operational environments.

Make the company less founder-dependent. Train a second layer of leaders. Put real cadence into sales, customer success, and product reporting. If all key relationships and product decisions still run through you, the buyer will worry about transition risk.

10.4 Prepare sale-ready materials before the process starts

Create clean monthly financials, a clear KPI pack, product and revenue segmentation, customer cohort analysis, and a credible 3-year growth story. Not a fantasy plan - a believable one.

This is also the right time to pressure-test your buyer narrative. A strategic utility software buyer, an industrial automation buyer, and a PE buyer may each value you for different reasons. The best process frames the business in the language each buyer cares about.

11. How an AI-Native M&A Advisor Helps

A strong outcome in this sector usually comes from buyer competition, good positioning, and fast, disciplined execution. That is where an AI-native M&A advisor can be genuinely useful.

First, AI can expand the buyer universe far beyond the usual shortlist. Instead of only contacting a handful of obvious names, it can help identify hundreds of qualified buyers based on deal history, strategic fit, product adjacency, financial capacity, and likely synergy logic. More relevant buyers usually means more competition, stronger offers, and a better chance the deal still closes if one buyer drops out.

Second, AI can speed up the process materially. Buyer matching, outreach support, marketing materials, and diligence preparation can all move faster, which means initial conversations and offers can often be reached in under 6 weeks rather than dragging into a slow manual process.

Third, the best AI-native firms still combine that speed with real human advisory. You want experienced M&A professionals running the process, framing the story, preparing the numbers, and speaking to buyers in a way that creates confidence. The advantage is getting Wall Street-grade advisory quality without the cost structure of a traditional bulge bracket bank.

If you'd like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.