The Complete Valuation Playbook for Eye Care Businesses

A practical, data-driven guide to how eye care businesses are valued - and what drives premium vs average multiples.

If you are considering selling your eye care business in the next 1-12 months, valuation should not be treated as a mystery or a one-line rule of thumb. In eye care, the gap between an average outcome and a premium outcome can be very large - even for businesses with similar revenue.

That matters even more now because eye care sits in the middle of several active buyer themes: healthcare consolidation, growing demand for outpatient and surgery-led care, continued interest in specialty healthcare platforms, and strong long-term demand driven by aging populations, refractive demand, and chronic eye disease. At the same time, buyers are more selective than they were in easier capital markets. They want quality, not just growth.

This guide is built to help you understand what eye care businesses actually sell for, what drives higher and lower multiples, where your business may fit, and what you can realistically improve in the next 6-12 months before going to market.

1. What Makes Eye Care Businesses Unique

Eye care is not one single business model. Buyers will value an ophthalmology hospital group very differently from an optical retail chain, a diagnostics platform, a lens manufacturer, or an ophthalmic device company. Even within provider businesses, there is a major difference between a cataract-heavy ambulatory surgery model, a general clinic model, and a tertiary referral center handling more complex cases.

For privately held eye care businesses preparing for sale, the most common models are usually one of four types:

- Ophthalmology clinic and surgery networks

- Mixed eye care groups with consultations, diagnostics, and procedures

- Optical retail and primary eye care businesses

- Eye care-adjacent platforms such as diagnostics, software, workflow, equipment, or products

What makes valuation in this sector distinctive is that buyers do not just look at revenue size. They look at revenue quality. In eye care, that means asking questions such as: how much of your revenue comes from repeatable consultations versus one-time procedures, how dependent are you on a few surgeons, how much of your earnings come from high-value procedures, and how scalable is the operating model across locations?

There is also a strong clinical layer to buyer diligence. In many sectors, buyers mainly worry about financial performance. In eye care, they also worry about clinical reputation, doctor retention, patient outcomes, referral patterns, utilization of expensive equipment, payor mix, and regulatory compliance. A business can look good on headline revenue and still trade lower if the clinical engine is fragile.

Three risk areas buyers almost always examine are concentration, dependency, and consistency. Concentration means too much revenue from one doctor, one site, or one referral source. Dependency means the business relies too heavily on a founder-surgeon. Consistency means the business needs to show stable procedure volumes, stable margins, and repeatable patient demand - not a few great months followed by volatility.

2. What Buyers Look For in a Eye Care Business

At a high level, buyers want the same basic things they want in any attractive business: scale, growth, profit, and predictability. But in eye care, those ideas get translated into very specific questions. Is the revenue mix weighted toward higher-value procedures? Are surgeons and optometrists likely to stay? Does each location have room to increase utilization? Are patients and referring doctors loyal to the platform, or to one individual clinician?

They will usually focus first on six core areas:

- Revenue scale and growth trend

- EBITDA margin and cash conversion

- Procedure mix and revenue quality

- Doctor bench strength and retention

- Site-level performance consistency

- Exposure to reimbursement, regulation, or consumer demand swings

In plain terms, buyers pay more when the business feels durable and expandable. A business with several productive sites, a broad doctor base, good surgery volumes, and clear systems for referral management feels much safer than a business where one star surgeon drives everything and the back office is still founder-led.

They also care about the model underneath the headline revenue. A surgery-led eye care business with strong utilization of operating theaters or ambulatory surgical capacity will often get more attention than a consultation-heavy business with limited procedure conversion. That is because procedures usually create higher revenue per patient visit, better operating leverage, and a stronger platform story for future expansion.

How private equity buyers think about your business

Private equity buyers usually ask three simple questions. First, what are they paying today? Second, what can they improve over the next 3-7 years? Third, who can they sell to later?

On the way in, they care about the entry multiple - the price they pay today compared with your revenue or EBITDA. On the way out, they care about the exit multiple - what a larger buyer may pay later. If they think your business can become a regional or national platform, add sites, recruit more clinicians, standardize pricing, improve scheduling, increase procedure conversion, and build a stronger management team, they may accept a fuller price today.

They also think hard about the next buyer. That future buyer could be a larger private equity fund, a strategic operator expanding geographically, or in some cases a listed healthcare platform. If your business looks like something that can become part of a larger eye care network, that helps. If it looks too small, too founder-dependent, or too messy to integrate, that hurts.

In eye care, the common private equity value levers are usually clear: add locations, improve doctor productivity, lift theater or equipment utilization, increase higher-value procedure mix, improve revenue cycle management, centralize back office work, and acquire smaller practices onto a common platform. Buyers are not paying for today alone. They are paying for what they believe they can build from it.

3. Deep Dive: Procedure Mix and Clinician Dependence

One of the biggest valuation questions in eye care is this: are you selling a real platform, or are you selling access to one or two high-performing doctors? That difference matters because buyers want earnings they can count on after closing.

The data supports the idea that healthcare provider assets command better valuations when they combine strong cash flow with a structure that a buyer can control and scale. In the precedent transaction set, the provider example with the clearest premium logic involved strong EBITDA margins and explicit governance control, which helped justify the valuation narrative. That logic matters in eye care too. If a buyer believes your platform can keep producing after the founder steps back, value increases.

Why do buyers care so much about procedure mix? Because procedure-led revenue is often the economic engine of eye care. Cataract surgery, refractive procedures, glaucoma procedures, retina work, premium lens upsell, and certain diagnostics can create a much richer revenue base than routine consultations alone. A business with healthy consult volumes but weak procedure conversion may look busy without being especially valuable.

Why does clinician dependence matter just as much? Because procedure mix only has value if it is durable. If 45% of EBITDA comes from one surgeon and there is no long-term retention plan, no second line of leadership, and no proof that patients and referrals belong to the platform, buyers will discount the business. They are buying future cash flow, not your past effort.

A useful way to frame it is this:

If your business looks more like the left column today, the fix is rarely a dramatic pivot. Usually it is about making the platform less personal and more repeatable: recruit and retain more clinicians, professionalize referral management, track consult-to-procedure conversion by doctor and site, improve utilization of surgical capacity, and reduce reliance on one name.

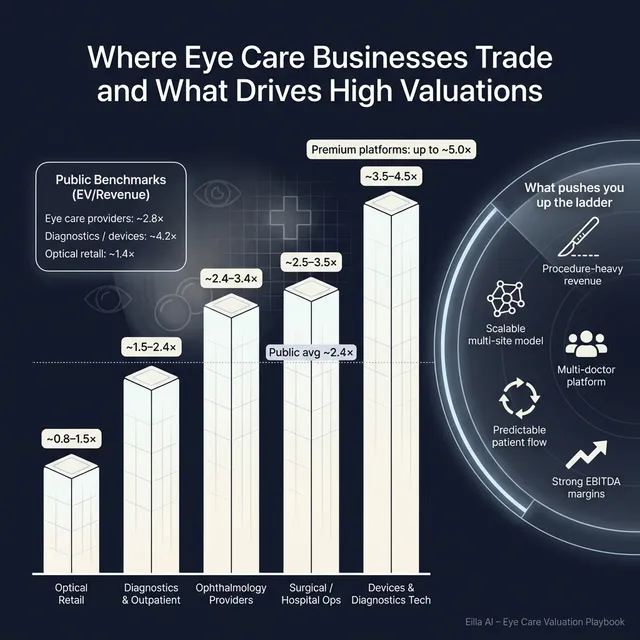

4. What Eye Care Businesses Sell For - and What Public Markets Show

Here is the clearest way to read the market data: eye care valuation ranges are wide because the sector includes very different business models. Provider networks, surgery-led operators, optical retail, diagnostics, products, and devices do not trade the same way. Even within provider businesses, quality differences matter a lot.

The public and private data together suggest that founder-owned eye care provider businesses should not expect one universal sector multiple. Instead, you should think in bands shaped by business model, margin, growth, and risk. Public markets provide the outer reference points. Private transactions show what buyers have actually paid in similar healthcare settings.

4.1 Private Market Deals (Similar Acquisitions)

The precedent transaction data provided is broader healthcare rather than pure eye care only, but it is still useful because it shows how buyers price provider businesses, software-like healthcare assets, and more services-heavy healthcare businesses. Across the full precedent set, the average EV/Revenue multiple is 2.6x and the median is 2.4x. Average EV/EBITDA is 23.6x, but the median is only 9.6x, which tells you a few high outliers are pulling up the average.

That matters because many eye care founders hear a big number and assume it applies to them. In reality, ordinary provider and services businesses tend to cluster far closer to the low-to-mid single-digit revenue multiple range, while software-like or highly recurring assets can price materially above that. For an eye care clinic or surgery platform, buyers will usually anchor closer to provider and operator logic than software logic.

The pattern is simple. Buyers pay more when the asset has either strong provider economics with control and integration potential, or software-like recurring revenue with high visibility. They pay less when revenue is less predictable, more project-based, lower-margin, or harder to scale.

These ranges are illustrative, not a promise. A highly attractive eye care business can outperform them. A smaller or riskier business can fall below them.

4.2 Public Companies

The public market set is especially useful here because it includes several eye care-related categories: ophthalmology provider networks, ophthalmic surgical devices, diagnostics, optical retail, vision correction manufacturing, and ophthalmic therapeutics. As of mid to late 2025, the overall public comp set in the materials shows an average EV/Revenue multiple of 4.7x and a median of 2.4x, plus an average EV/EBITDA multiple of 15.1x and median of 9.4x.

But the averages hide big variation. Ophthalmology provider networks and eye hospitals show a very wide spread, from below 1.0x revenue at the low end to more than 7.0x at the high end. That tells you the market sharply distinguishes between lower-growth or lower-confidence operators and scaled, profitable, premium-positioned providers. Meanwhile, surgical devices and premium optical product platforms can trade at higher revenue multiples when growth, margins, or intellectual property are strong.

A few clear patterns come through. Provider businesses can trade very well, but only when they combine scale, credibility, and strong profitability. Optical retail tends to trade lower because it is often more consumer-facing, more promotion-sensitive, and less clinically differentiated. Diagnostic and device businesses can trade higher when they have stronger gross margins, better growth, or product defensibility.

Founders should use public multiples as reference bands, not direct price tags. A private company is usually smaller, less liquid, more concentrated, and less diversified than a listed business, so the multiple often needs to be adjusted downward. But public comps still matter because they shape buyer thinking. They tell buyers what larger platforms are worth, which affects what they can rationally pay for smaller add-ons or new platforms.

At the same time, private assets can sometimes justify stronger-than-expected pricing when they are scarce, highly strategic, or clearly platformable. That is especially true when multiple buyers can see a path to building a broader eye care network around the asset.

5. What Drives High Valuations (Premium Valuation Drivers)

Premium valuations do not happen because a founder tells a great story. They happen when the buyer sees lower risk, better economics, and a clear path to future value creation. In the data provided, the clearest premium themes are recurring revenue visibility, strong margins, control rights, and structures that let buyers pay up while protecting downside.

5.1 Strong margins and real cash flow

Buyers pay more for eye care businesses that convert revenue into healthy EBITDA. In provider models, strong margins suggest the business has good doctor productivity, efficient scheduling, healthy procedure economics, and cost discipline. In practical terms, buyers feel more comfortable paying up when they believe the earnings are real and repeatable.

For founders, this can show up in ways that feel operational rather than financial:

- Well-utilized procedure rooms and equipment

- Good staffing ratios

- Healthy consult-to-procedure conversion

- Strong pricing on premium procedures or lenses without excessive discounting

5.2 A platform the buyer can control and scale

One of the strongest valuation themes in the source data is strategic control. Buyers are more willing to pay up when they are not just buying a profit stream, but a base they can expand. In eye care, that usually means a multi-site platform, or a strong first site with a model that can be replicated.

This is why governance, management depth, and standardized operations matter. If a buyer can centralize scheduling, marketing, procurement, finance, referral management, and doctor recruitment across a platform, the asset becomes more valuable than a single clinic with good numbers.

5.3 Recurring or visible revenue

The source data shows that healthcare software businesses with explicit recurring revenue disclosure can support stronger valuation logic. Eye care providers are not software businesses, but the principle still matters: visibility gets rewarded.

In eye care, visibility can come from things like:

- Repeat diagnostics and follow-up pathways

- Long-standing referral relationships

- Predictable procedure demand

- Corporate contracts or institutional channels

- Membership, care plans, or subscription-like optical relationships where relevant

The more buyers can underwrite next year's revenue with confidence, the more aggressive they can be on price.

5.4 High gross margin and attractive revenue quality

The data also shows that high gross margin models generally have more room to support stronger revenue multiples. In eye care, that does not mean gross margin alone is enough. One source example showed that high gross margin without scale, growth, or profit still did not produce a premium revenue multiple.

That is the key lesson. Buyers do not pay a premium for one good metric in isolation. They pay a premium when several attractive features line up at once: solid margin, good growth, clear demand, and credible scalability.

5.5 Earnout-friendly growth narrative

The source data shows earnouts being used where buyers see upside but want protection. That often supports stronger headline valuations than a pure cash deal. In eye care, earnouts are common when growth depends on future site openings, surgeon recruitment, new service lines, or hitting procedure targets.

This matters because founders sometimes reject earnouts on principle. That can be a mistake. A well-structured earnout can help bridge value gaps if your business is clearly improving but the trailing numbers do not yet fully show it.

5.6 Clean company fundamentals

Even when not stated directly in the data, the same rules apply in almost every good sale:

- Clean financials

- Consistent reporting

- Predictable KPIs

- Diversified revenue

- Low founder dependency

- Strong second-line management

These are not glamorous, but they often determine whether you land in the top third of the range or the middle.

6. Discount Drivers (What Lowers Multiples)

The low end of the valuation range usually has a logic behind it. It is rarely random. Buyers discount businesses when they see fragility, volatility, or too much work needed after closing.

One obvious discount driver is weak visibility. If your revenue is hard to forecast, heavily dependent on ad hoc demand, or unclear by service line, buyers get cautious. A consultation-heavy model with uneven procedure flow often trades worse than a business with a more stable clinical and surgical engine.

Another discount driver is high dependence on one founder, one surgeon, one site, or one referral channel. In eye care, this is a major issue. A business can look very profitable on paper and still get marked down if the buyer thinks the economics leave with one individual.

The source data also shows that high gross margin alone does not guarantee a strong valuation. One high-margin service asset still traded at only about 1.3x revenue because profitability was negative and the scaling story was weak. That is a useful warning for eye care founders who assume a premium patient experience or premium pricing alone will lift value.

Other common discount drivers include:

- Low or inconsistent EBITDA margins

- Underutilized equipment or facilities

- Messy site-level performance

- Poor doctor contracts or weak retention tools

- Regulatory, licensing, or compliance gaps

- Heavy exposure to lower-quality reimbursement

- Limited management depth below the founder

The good news is that many discount drivers are fixable. Buyers will forgive imperfections more easily when they see the issue clearly measured, openly explained, and already being improved.

7. Valuation Example: A Eye Care Company

Let us make this concrete with a fictional business.

Assume NorthStar Eye Centers is a fictional regional eye care company with USD 10m of revenue. It operates two surgery-capable sites and one consultation-heavy satellite clinic. Its revenue mix is 55% cataract and refractive procedures, 25% diagnostics and consultations, and 20% optical and ancillary services. The company and the revenue figure are fictional, and the valuation below is illustrative only - not investment advice or a formal valuation.

How the logic works

The cleanest way to value a business like this is to start with the most relevant public and private reference points. For a provider-led eye care business, the best anchors in the source materials are ophthalmology provider networks and broader hospital or surgical facility operators - not biopharma, not high-growth medtech, and not software.

The source logic for a real provider example at a much larger revenue base used a lower-to-mid provider multiple range of roughly 1.0x to 1.65x revenue. That makes sense for a stable clinical services asset without obvious software-like growth characteristics. For a smaller private business, you would usually begin around that zone unless the company has unusually strong quality markers.

Then you adjust. If the business has premium features - strong EBITDA margins, diversified clinicians, high procedure mix, good growth, and real expansion potential - the multiple can move up. If it has weaknesses - founder dependence, inconsistent site output, thin management, or messy numbers - the multiple moves down.

Applying the logic to the fictional company

For NorthStar Eye Centers, let us assume the base profile is decent but not perfect:

- Good procedure mix

- Solid local reputation

- Reasonable margin profile

- Some founder dependence

- Still room to professionalize reporting and management

That would support a base case somewhere around the core provider band.

What could justify each scenario?

A discounted case might apply if the founder performs most of the high-value procedures, one site carries most of the profit, reporting is weak, and growth has flattened. Buyers would worry that the platform is less transferable than it appears.

A base case fits a business with sound operations, acceptable margins, decent procedure demand, and a credible transition plan. This is where many solid eye care businesses would likely land.

A premium case becomes more credible when several strengths stack together: strong multi-doctor bench, stable growth, high procedure utilization, clean data by site and service line, attractive margins, and visible room to add locations or clinicians. In that situation, buyers are not just valuing today's earnings - they are valuing a platform.

The main lesson is simple: two eye care businesses with the same USD 10m revenue can be worth very different amounts. Revenue gets you into the conversation. Quality determines where in the range you land.

8. Where Your Business Might Fit (Self-Assessment Framework)

This is not a scientific valuation model. It is a practical way to pressure-test how buyers are likely to see your business today. Score each factor from 0 to 2:

- 0 = weak

- 1 = acceptable

- 2 = strong

Be honest. The goal is not to flatter yourself. The goal is to identify where improvements will move value most.

A more detailed version might look like this:

A rough interpretation:

- 14-18 points: You are closer to premium territory

- 9-13 points: You are likely in fair-market range

- 0-8 points: You may want more preparation before selling

This is not about pride. It is about identifying the few improvements that can change buyer confidence the most.

9. Common Mistakes That Could Reduce Valuation

The first big mistake is rushing the sale. Many founders decide to sell after a strong quarter or a moment of fatigue, then go to market before the numbers, story, and process are ready. That almost always weakens leverage. Buyers can tell when a process is improvised.

The second is hiding problems. In healthcare deals, issues almost always surface in diligence - doctor concentration, compliance questions, site profitability problems, billing weakness, equipment underutilization, disputes, or inconsistent KPIs. If buyers discover a problem late that should have been disclosed early, trust drops and valuation usually drops with it.

The third is weak financial records. If you cannot clearly show revenue by site, by service line, by doctor group, and by margin contribution, buyers will assume the risk is higher than it may actually be. This is especially painful because many of these issues can be improved in 6-12 months with better reporting, clearer revenue recognition, cleaner add-backs, and more disciplined KPI tracking.

The fourth is not running a structured, competitive process with an advisor. A well-run process creates buyer tension, better preparation, sharper materials, and better price discovery. Research and market practice consistently support the idea that a structured competitive process with an advisor can lead to meaningfully higher outcomes - often around 25% higher purchase prices than less organized, one-buyer discussions.

The fifth is telling buyers what price you want before the market has spoken. If you tell buyers you want USD 10m, many of them will not think, "What is this really worth to us?" They will think, "Can we get this done at USD 10.1m or USD 10.2m?" You kill the chance for real price discovery.

Two eye care-specific mistakes are especially common. One is failing to address founder-surgeon dependence before a sale. If the buyer thinks patients, referrals, and procedures are tied to you personally, value falls. The other is failing to explain procedure economics clearly. If buyers cannot see the difference between low-value visits and high-value surgical pathways, they may undervalue what is actually a strong clinical model.

10. What Eye Care Founders Can Do in 6-12 Months to Increase Valuation

10.1 Improve the numbers buyers care about

Start by making the business easier to understand. Build monthly reporting by location, service line, and doctor group. Track consult volume, procedure conversion, revenue per patient, utilization of key equipment or surgery capacity, and EBITDA by site if possible.

Look for margin improvements that are realistic within a year:

- Improve scheduling and theater utilization

- Reduce leakage between consultation and procedure

- Tighten staffing and procurement

- Review pricing on premium offerings

- Clean up billing and collections

You do not need a dramatic turnaround. Small, believable improvements often matter more than ambitious forecasts.

10.2 Reduce dependence on the founder

This is one of the highest-value moves in eye care. If too much depends on you, start changing that now. Recruit or elevate clinical leaders, professionalize site management, document workflows, and strengthen doctor retention agreements where appropriate.

Also work on making referrals belong to the platform rather than to one person. That means better CRM discipline with referring doctors, stronger patient communication systems, and clearer branding around the organization.

10.3 Strengthen revenue quality

Buyers like visibility. You can improve that by building more repeatable patient pathways, improving follow-up conversion, strengthening institutional referral channels, and stabilizing demand across sites. If optical, diagnostics, or post-op pathways improve retention and wallet share, show that clearly.

If you have a growing premium procedure mix, document it. If certain service lines are dragging margins, either improve them or explain why they matter strategically. Buyers do not mind complexity as much as they mind unexplained complexity.

10.4 Build the platform story

Even a smaller eye care business can earn a stronger multiple if it looks like a platform rather than a practice. That means showing:

- Repeatable site model

- Capacity for more clinicians or more procedures

- White space for add-on acquisitions

- Local brand strength

- Management depth beyond the founder

In practical terms, this means putting together a credible growth roadmap, not a fantasy. Buyers want to see what can realistically happen in the next few years.

10.5 Prepare for diligence before the sale starts

Get ahead of diligence now. Organize contracts, licenses, clinician agreements, site leases, referral data, compliance records, financial statements, and KPI dashboards. Identify issues early and decide how to explain them clearly.

A buyer is much more likely to hold price when they feel the business is well prepared, well understood, and honestly presented.

11. How an AI-Native M&A Advisor Helps

A modern sale process is no longer just about knowing a handful of buyers. An AI-native M&A advisor can expand the buyer universe dramatically - often to hundreds of qualified acquirers screened by deal history, strategic fit, financial capacity, and likely synergy. That broader reach matters because more relevant buyers create more competition, stronger offers, and better odds of closing even if one party drops out.

AI also speeds up the process. With AI-assisted buyer matching, outreach, preparation of marketing materials, and support through diligence, initial buyer conversations and first offers can often be reached in under 6 weeks. Speed does not replace judgment, but it does reduce wasted time and keeps momentum on your side.

The advantage is not AI alone. It is expert human advisory enhanced by AI. You still want experienced M&A advisors driving the process, framing the business correctly, pressure-testing the numbers, and negotiating with buyers. What AI changes is the depth, speed, and breadth of that work - giving you Wall Street-grade advisory quality without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.