The Complete Valuation Playbook for Cooling and Refrigeration Solutions Businesses

A practical guide to how cooling and refrigeration businesses are valued and what drives high multiples.

If you run a privately held Cooling & Refrigeration Solutions business and you may sell in the next 1-12 months, valuation is no longer something to think about at the very end. This sector is seeing steady consolidation from strategics, selective appetite from private equity, and a clear split between businesses that look like scalable service platforms and those that look like lower-multiple project contractors.

This playbook is built to help you understand what businesses in this sector actually sell for, what separates high-multiple outcomes from average ones, and what you can still improve in the next 6-12 months before going to market.

The goal is not to pretend there is one exact number for your company. It is to show you the valuation logic buyers use, so you can see where your business fits and how to push it toward the top of the range.

1. What Makes Cooling & Refrigeration Solutions Businesses Unique

Cooling & Refrigeration Solutions is not one simple industry. It includes several business types that buyers value differently: engineered refrigeration and cold-chain equipment makers, commercial refrigeration integrators, HVAC and refrigeration installation and maintenance contractors, parts and equipment distributors, and niche specialists such as monitoring, controls, or refrigerant lifecycle services.

That matters because two businesses with the same revenue can deserve very different valuations. A company that mainly passes through equipment and wins one-off installation jobs will usually trade very differently from a company with recurring maintenance contracts, strong service margins, and a reputation for solving technically difficult cooling problems.

Buyers also know that this sector sits at the intersection of product, project execution, field service, and compliance. They will want to understand how much of your revenue comes from equipment resale, how much comes from labor and service, how sticky your maintenance base is, and whether your work is repeatable or heavily dependent on a few senior people.

The core risks are also sector-specific. Buyers will always check customer concentration, exposure to construction cycles, refrigerant regulation risk, warranty and call-back history, reliance on a few project managers or engineers, service technician depth, margin volatility on fixed-price jobs, and how much of your backlog is real versus hopeful pipeline.

2. What Buyers Look For in a Cooling & Refrigeration Solutions Business

At the simplest level, buyers care about four things: how fast you are growing, how profitable you are, how predictable your revenue is, and how risky the business feels. In this sector, that last point matters a lot. A business with modest growth but strong recurring maintenance and mission-critical customer relationships can be more attractive than a faster-growing business built on lumpy, low-margin project work.

Strategic buyers usually look for one of three things. First, they may want geographic expansion, especially if you have a strong local service footprint. Second, they may want technical capability, such as industrial refrigeration, natural refrigerants, controls, remote monitoring, or cold-storage design expertise. Third, they may want customer access in attractive end markets like food retail, cold storage logistics, pharmaceuticals, healthcare, data centers, or industrial processing.

Private equity buyers look at the business through a slightly different lens. They ask what multiple they are paying today, what multiple they might sell at in 3-7 years, and what they can improve in the meantime. They will think hard about whether your business could later be sold to a larger strategic buyer, a larger private equity fund, or used as a platform for add-on acquisitions.

They also look for clear value creation levers. In this sector, those often include raising service contract attach rates, professionalizing pricing, increasing maintenance renewals, expanding parts and aftermarket revenue, cross-selling into adjacent cooling needs, reducing project execution mistakes, and adding tuck-in acquisitions to widen territory or technical depth.

How private equity really thinks

A private equity buyer does not just ask, "Is this a good business?" They ask, "Can this become a better and more sellable business by the time we exit?" If your company already has recurring revenue, clean reporting, second-line management, and a credible expansion path, it is much easier for them to underwrite a strong return.

If instead the business depends on you personally, has unclear segment reporting, and swings sharply with project timing, they will either lower price, add earn-outs, or walk away.

3. Deep Dive: Recurring Service Revenue vs Project Revenue

In Cooling & Refrigeration Solutions, one of the biggest valuation questions is whether buyers see your company as a project contractor or as a service platform.

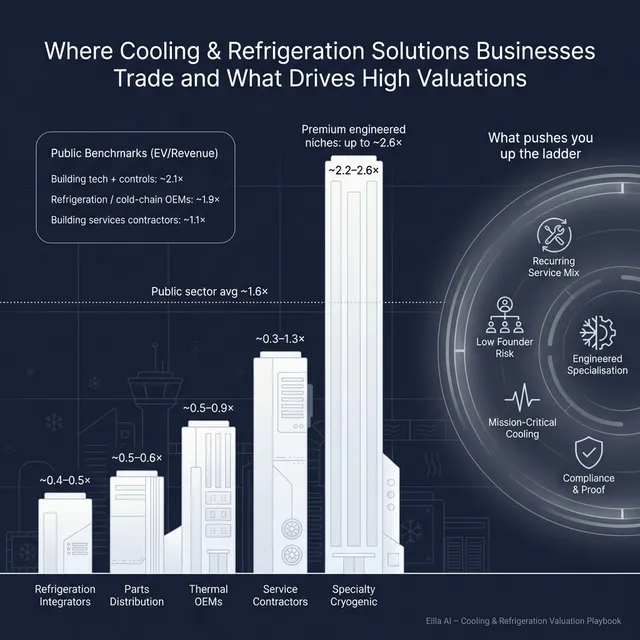

The source data points in that direction very clearly. Private transactions for mechanical and HVAC building services and O&M businesses tend to cluster around roughly 0.3x to 1.3x revenue, while commercial refrigeration integrators in the data sit lower, around 0.4x to 0.5x revenue. By contrast, higher-quality outcomes in and around the sector usually show up where the business has stronger engineering content, better margins, or some form of recurring or usage-like revenue.

Why do buyers care so much? Because project revenue resets every quarter. You have to win it again. It can be delayed, repriced, or canceled. It is also more exposed to labor execution risk and input-cost surprises. Service revenue, especially preventive maintenance, uptime contracts, monitoring, and recurring compliance work, behaves more like an annuity. Buyers trust it more, lenders support it more, and investors pay more for it.

This does not mean project work is bad. In fact, project work is often how you win the customer in the first place. The problem is when the install job ends and there is no long-tail relationship. The best-valued businesses in this sector use projects to create future service, parts, retrofit, and monitoring revenue.

There is a second layer here: whether your work is truly engineered or mostly labor-led. Buyers will pay more for businesses that solve difficult cooling problems, standardize designs, understand compliance, and operate in demanding environments. They pay less for businesses that look interchangeable with other local installers.

If your business looks more like the left column today, the path forward is usually practical, not magical. Increase maintenance attach on every install. Track renewal rates by customer cohort. Separate equipment resale from labor and service in your reporting. Package remote monitoring, emergency response, compliance checks, and energy optimization into contracted offerings. These changes do not turn you into software, but they do move you toward more trusted earnings.

4. What Cooling & Refrigeration Solutions Businesses Sell For - and What Public Markets Show

Here is what the data actually shows: most private-market revenue multiples in this sector are not sky-high. The median private transaction multiple in the dataset is about 0.6x revenue, even though the average is distorted upward by a few obvious data anomalies and specialty outliers. Public-company averages are also mixed, with the overall public set averaging about 1.6x revenue and 19.1x EBITDA, but the median public revenue multiple is only about 1.0x.

The right way to read that is simple. Cooling & Refrigeration Solutions businesses can absolutely sell for attractive values, but buyers are selective. The market rewards quality, differentiation, and recurring economics. It does not give blanket premiums just because a business operates in cooling, HVAC, or cold chain.

4.1 Private Market Deals (Similar Acquisitions)

The most relevant private deals for many founder-owned businesses in this sector are service and installation companies, system integrators, and smaller specialty product businesses. Those deals mostly land below 1.0x revenue, unless the company has a more engineered product mix, very strong margins, or a niche specialty position.

The strongest private-market message in your source set is that business model matters more than broad industry labels. A contractor or service operator is usually valued on a lower revenue multiple than an engineered specialist. And where the data appears to show an extreme premium, the underlying numbers often look messy or inconsistent - which is itself a lesson for founders: unclear financials do not create premium value, they destroy credibility.

These ranges are illustrative, not a formula. A recurring-service-heavy refrigeration business with a strong end-market niche can reasonably sit above the middle of the contractor range. A low-margin installer with weak reporting can fall below headline numbers very quickly.

4.2 Public Companies

Public markets give a useful reference point, but not a direct price tag. As of late 2025, public companies around this sector traded very differently depending on where they sat in the value chain.

Integrated building technology and controls businesses traded at the highest broad revenue levels in this set, around 2.1x revenue on average, helped by stronger software, controls, services, and lifecycle elements. HVAC OEMs also traded around 2.1x revenue on average, but with a lower median because the group includes both stronger premium manufacturers and more cyclical names. Refrigeration and cold-chain OEMs averaged around 1.9x revenue, while building services contractors were much lower on median, around 0.7x revenue, even though one high-flying outlier lifts the average.

* These EBITDA averages are influenced by outliers and should be read with caution.

For founders, public multiples are best used as guardrails. They show what larger, more diversified, often more liquid businesses are worth. Your private company will usually be adjusted downward for smaller size, customer concentration, weaker reporting, or less predictable earnings. Occasionally, a scarce and strategic asset can push above the normal private range - but that usually happens because it has a very specific niche, not because the seller wishes it into existence.

5. What Drives High Valuations (Premium Valuation Drivers)

High valuations in this sector usually come from a handful of recurring themes, not one magic metric.

5.1 Engineered specialization that is hard to replace

Buyers pay more when your business solves difficult problems, not when it simply supplies standard equipment and labor. The premium driver in the source data is engineered, specialty product or systems capability with defensible complexity. That can mean natural refrigerants, cold-room design, pressure or temperature-critical environments, compliance-heavy work, proprietary controls logic, or hard-to-replicate application know-how.

Why this matters is simple: if your work is difficult, customers switch less often and competitors are fewer. Buyers can underwrite better margins and stronger customer retention.

5.2 Recurring revenue that turns capex into ongoing spend

A business that makes money only when a customer buys equipment is less valuable than one that keeps getting paid to maintain uptime. Buyers like maintenance contracts, monitoring fees, emergency response retainers, refrigerant management programs, and long-term service agreements because they make revenue more visible.

The source material also highlights subscription-like models and remote monitoring as attractive narratives. You do not need to become a software company. You just need to show that a meaningful part of your revenue is contracted, renewable, and tied to operational continuity.

5.3 Attractive end markets with mission-critical cooling needs

Not all customer sectors are valued the same. Buyers are more excited by exposure to end markets where failure is expensive - pharmaceuticals, healthcare, cold-chain logistics, industrial processing, data centers, labs, and certain food environments. In these markets, uptime matters more, service quality matters more, and price is not the only decision factor.

That usually leads to better margins, more repeat business, and a stronger valuation story.

5.4 Proof, not storytelling

One of the strongest messages in your source set is that data quality matters. Some of the most extreme multiples in the raw deal list appear to reflect inconsistent or mis-scaled data, not true premium outcomes. In the real market, poor data does not help you. It creates doubt.

That means premium value comes from being able to prove your story. Clean segment reporting, service renewal data, backlog quality, gross margin by revenue type, technician utilization, and customer retention all matter because they let buyers trust the earnings.

5.5 Scalable footprint and repeatable operations

Buyers pay more when they believe the business can grow without breaking. A dense service footprint, multiple branches, strong dispatch and field operations, good training, and repeatable installation and maintenance processes all help. So does a professional management layer beneath the founder.

This is especially important for buyers who want to use your business as a platform. They need confidence that add-on acquisitions, territory expansion, or cross-selling can be integrated into a working operating model.

5.6 Management continuity and reduced key-person risk

Founders often underestimate this point. Buyers will pay more when they believe your engineers, project leaders, service managers, and customer relationships will still be there after closing. The source transactions show this clearly through retained founders, staged buyouts, and earn-outs tied to ongoing product or commercial performance.

A buyer does not want to acquire a cooling business and then discover the real value was sitting in the founder's phone.

5.7 Clean basics still matter

Even in a technical sector, the classic value drivers remain powerful: diversified customers, stable gross margins, predictable working capital, good cash conversion, clean financials, limited one-off adjustments, and a credible second line of leadership.

These do not create a premium story on their own. But without them, premium stories rarely survive diligence.

6. Discount Drivers (What Lowers Multiples)

Most disappointing outcomes happen for understandable reasons. Buyers are not trying to be cruel. They are pricing risk.

The biggest discount driver is when the business looks too project-led and too hard to forecast. If revenue depends heavily on winning the next installation job, margins swing by project, and service is a small add-on rather than a meaningful base, buyers will usually push toward the low end of the range.

Another major discount factor is when your company looks more like labor than intellectual property. Bespoke work sounds attractive, but if buyers conclude it is really custom field execution without proprietary know-how, they will underwrite you as a regional contractor, not as a specialty engineering asset.

Messy reporting is another value killer. If you cannot reconcile revenue, backlog, service mix, gross margin by segment, or normalized EBITDA, buyers will assume the conservative case. That point is reinforced directly by the source data, where some apparent premium outcomes are undermined by unreliable underlying numbers.

Customer concentration also hurts. So does dependence on one founder, one estimator, one service manager, or one supplier. The same goes for weak technician retention, warranty leakage, and poor margin discipline on fixed-price jobs.

Sector-specific red flags include too much exposure to low-margin equipment pass-through, lack of documented refrigerant and regulatory compliance capability, and weak evidence that install customers convert into recurring service customers. These issues do not make a sale impossible, but they usually pull value down or shift more of the consideration into earn-outs and holdbacks.

7. Valuation Example: A Cooling & Refrigeration Solutions Company

Let’s turn the valuation logic into a practical example.

Assume a fictional company called NorthPeak Cooling Services. It is not a real business. Assume it has USD 10m of annual revenue, with a mix of commercial refrigeration installs, retrofit work, planned maintenance, emergency service, and some equipment resale. The valuation ranges below are illustrative only. They are not investment advice or a formal valuation.

Step 1: How the logic works

Start with the most relevant comparable set. For a founder-owned cooling and refrigeration business that is mainly design, install, service, and maintenance - rather than a branded OEM with proprietary products - the closest references are private contractor and O&M deals, plus public building-services and refrigeration service businesses.

The specific source logic you provided points to a defensible working range of about 0.65x to 1.20x revenue for a mature SME of this type. That sits above the weaker private contractor floor, but still below product-led or more scalable OEM-like multiples. In plain English: a good service-and-project operator can earn a decent premium to weaker contractors, but it usually should not be priced like a true manufacturing or technology platform unless it has much stronger differentiation.

Then adjust for the actual business profile. If the company has strong recurring maintenance, good margins, diversified customers, and clear technical specialization, it can push upward in the band. If it is equipment-heavy, founder-dependent, or lumpy, it drifts downward.

Step 2: Apply it to the fictional company

Assume NorthPeak has the following profile:

- USD 10m revenue

- 38% from recurring maintenance and service

- 42% from installation and retrofit

- 20% from equipment and parts resale

- Good regional reputation

- No proprietary product IP

- Solid but not elite reporting

- Moderate founder dependence

That profile supports a core range around the middle of the band.

What would justify the strong case?

A higher-end outcome would usually require several things to be true at once: strong maintenance attach rates, clear recurring revenue evidence, good gross margin discipline, attractive end-market exposure, low customer concentration, documented leadership beneath the founder, and a credible story that install work feeds durable service revenue.

What would justify the discounted case?

A lower result would be more likely if revenue is heavily project-based, equipment pass-through is high, gross margins are inconsistent, the founder owns most customer relationships, or financial reporting does not cleanly separate service from project economics.

The key lesson is simple: two Cooling & Refrigeration Solutions businesses with the same USD 10m revenue can rationally be worth very different amounts. Revenue size starts the conversation. Revenue quality decides where you land.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as a rough scoring tool, not a scientific test. Score each factor from 0 to 2.

- 0 = weak

- 1 = average

- 2 = strong

How to interpret your score

If you score mostly 2s in the high-impact rows, you are closer to the top of the realistic range for private businesses in this sector. If you are mostly 1s, you are likely in fair-market territory. If you are carrying several 0s in recurring revenue, concentration, founder dependence, or data quality, that usually means the business will be priced more conservatively unless you fix those issues before launch.

The point of this exercise is not to judge yourself. It is to show where the next 6-12 months can create the biggest payoff.

9. Common Mistakes That Could Reduce Valuation

Rushing the sale

Founders often decide to sell only after a hard year, a burnout moment, or an incoming approach. That is understandable, but it is expensive. If your numbers, segment reporting, customer story, and management plan are not ready, buyers will feel your lack of preparation and price accordingly.

Hiding problems

Do not do this. Buyers will find churn issues, margin leakage, warranty problems, contract weakness, compliance gaps, or customer concentration during diligence. When they discover a problem late that you did not disclose early, the issue is no longer just the problem itself - it becomes a trust problem, which is worse.

Weak financial records

This one is especially avoidable. Many cooling businesses can materially improve sale readiness in 6-12 months just by cleaning up revenue recognition, separating service from project and equipment revenue, tracking gross margin by segment, and normalizing owner-related expenses. Buyers cannot give you full credit for a strong business if the reporting does not prove it.

Running an unstructured process

A one-buyer conversation rarely produces your best outcome. Research on private-company sales finds that sellers using M&A advisers achieve significantly higher valuations on average, and lower-middle-market market data often summarizes that uplift at around 25%, largely because advisers widen the buyer pool and create competitive tension. (Harvard Law Forum)

Naming your target price too early

This mistake kills price discovery. If you tell buyers, "I want USD 10m," many will simply anchor around that number and come back at USD 10.1m or USD 10.2m instead of showing what they might actually pay in a competitive process. Let the market speak first.

Failing to show service conversion

This is a sector-specific issue. If you install systems but cannot show how many customers convert into maintenance, monitoring, parts, retrofit, or refrigerant-management revenue, buyers will treat each project as mostly one-time.

Not documenting technical and compliance know-how

If your real value comes from solving difficult refrigeration problems, energy efficiency, natural refrigerants, or uptime-sensitive environments, document it. Otherwise buyers may assume your work is more replaceable than it really is.

10. What Cooling & Refrigeration Solutions Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers care about most

Separate revenue into at least three buckets: service and maintenance, projects and installation, and equipment or parts pass-through. Track gross margin by each bucket. Show monthly recurring service revenue, renewal rates, emergency callout patterns, and the share of installs that convert into ongoing service.

If you can improve one thing operationally, improve attach and renewal. A buyer will care more about a clear rise in recurring service penetration than a vague story about future opportunity.

Improve the quality of earnings

Clean up one-off expenses, owner add-backs, inventory issues, and revenue timing. Build a twelve-month trailing KPI pack that includes backlog, win rates, service retention, customer concentration, technician utilization, gross margin by category, and top-customer trends.

The cleaner your reporting, the less buyers need to "haircut" the story for safety.

Reduce concentration and key-person risk

Move important customer relationships deeper into the team. Put written incentive plans in place for project managers, engineers, and service leaders. Show that quoting, operations, and customer retention do not all run through you.

If you are the founder, one of the most value-creating things you can do is make the business look more sellable without you.

Strengthen the recurring revenue base

Review every installed base customer and ask three questions: Do they have a maintenance agreement? Do they have monitoring or compliance service needs? Are you first call when something goes wrong? If the answer is no too often, you are leaving valuation on the table.

Bundle preventive maintenance, uptime response, refrigerant management, and energy optimization into clearer service programs. The goal is not just more revenue. It is more trusted revenue.

Sharpen your market positioning

Generalists usually get generalist multiples. If you have credibility in cold storage, food production, pharmaceuticals, healthcare, industrial refrigeration, or another high-value niche, make that positioning obvious in your materials and your metrics.

Buyers pay more when they can quickly understand why your company matters and why customers keep coming back.

Prepare a buyer-ready narrative

Your equity story should be short and believable. It should explain what you do, what share of revenue is recurring, where margins come from, why customers stay, why your niche matters, and what a buyer could do next. A strong narrative does not replace data. It makes the data easier to believe.

11. How an AI-Native M&A Advisor Helps

Most founders do not lose value because they built a weak business. They lose value because they run a narrow process, reach too few buyers, and let the market define the story before they do.

An AI-native M&A advisor changes that in a practical way. AI can expand the buyer universe from a short list into hundreds of qualified strategic and financial acquirers based on deal history, adjacency, financial capacity, geography, and likely synergies. That broader reach usually creates more competition, stronger offers, and better deal certainty because you are not dependent on one or two conversations.

It also speeds up the early stages of the process. AI-supported buyer matching, outreach, preparation of marketing materials, and diligence organization can help founders get to initial conversations and first offers far faster than a manual-only process - often in under 6 weeks in well-prepared situations.

The key point, though, is not automation by itself. It is expert advisory enhanced by AI. The best outcome still comes from experienced human M&A advisors who know how to frame the business, pressure-test the numbers, manage buyers, and negotiate terms. AI simply helps them do that with wider reach, better preparation, and less wasted time - delivering Wall Street-grade process quality without traditional bulge-bracket cost structures.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.