The Complete Valuation Playbook for Game Development Businesses

A data-driven guide to how game development studios are valued in today’s M&A market - and the practical steps founders can take in 6-12 months to increase multiples and buyer confidence.

If you are considering a sale in the next 1-12 months, valuation is not just a number - it is the story buyers believe about your future cash flows, your risk, and your ability to repeat success.

This guide is built for game development founders and CEOs. It uses real market data on how similar studios have been valued in acquisitions, plus what public game companies trade at, and then translates that into practical steps you can take before you go to market.

You will learn what game development businesses actually sell for, what drives higher vs lower multiples, how to self-assess where you likely sit, and what you can realistically improve in 6-12 months.

1. What Makes Game Development Unique

Game development looks like "software" from the outside, but buyers do not value it like SaaS. Most studios are valued as creative production businesses with uneven revenue, title risk, and big swings around launches.

Main types of game development businesses

Most privately held studios fall into a few buckets:

- AAA/PC-console developers (original IP & franchises) - premium or AA/AAA game development, sometimes with publisher funding, sometimes self-funded.

- Mobile-first free-to-play developers and publishers - live-ops, data-driven retention, heavy user acquisition (UA) and content cadence.

- Indie/portfolio publishers and developers - smaller teams, multiple titles, sometimes a publisher + dev mix.

- Co-development/services studios - QA, porting, co-dev, audio, art, engineering support. More "contract-like" revenue.

- Retro/remaster specialists - focused on classic IP restoration, remasters, and re-releases.

- Platforms/ecosystems - UGC, creator tools, marketplaces (a different world on valuation).

Unique valuation considerations

Buyers will always pressure-test:

- How much of your revenue is repeatable vs one-off (back catalog, DLC, live-ops, long-tail).

- Your "hit risk" - how dependent your results are on a single title landing.

- Where you sit in the value chain - own IP, license IP, work-for-hire, or platform economics.

- Capital intensity - how much cash and time it takes to ship your next meaningful release.

- Team dependency - whether the studio is a transferable machine or a founder-driven creative core.

Key risk factors buyers will always check

In game dev, the classic diligence checklist has a few sector-specific spikes:

- Pipeline risk - milestones, burn rate, probability-weighted delivery dates, and who is funding the runway.

- IP rights clarity - ownership, licensing restrictions, engine/tool dependencies, talent agreements.

- Live-ops capability - if you claim ongoing monetization, buyers will verify cadence and retention proof.

- Platform concentration - one storefront, one platform holder, one publisher relationship can be a valuation limiter.

- Quality and community risk - reviews, sentiment, and post-launch support expectations are real value drivers.

2. What Buyers Look For in a Game Development Business

Buyers pay for future outcomes, not past effort. In game development, that means they care about whether your studio can reliably produce revenue-generating titles without blowing up budgets, timelines, or team morale.

The universal basics still matter

Even in a creative industry, the basics drive outcomes:

- Scale - bigger, proven revenue bases are easier to underwrite.

- Growth - expanding audiences, rising monetization, or an increasing release cadence.

- Profitability - or at least a credible path to it.

- Clean financial reporting - clear title-level P&Ls, capitalization policies, and revenue recognition.

Game dev-specific buyer priorities

This is where deals diverge:

- IP control and monetization options - buyers pay more when IP can be reused (sequels, DLC, licensing).

- Back catalog durability - revenue after launch is often the difference between a studio and an asset.

- Production reliability - buyers love studios that hit milestones and ship with predictable quality.

- Talent and culture stability - key creatives staying matters, but buyers also want depth beyond 2-3 stars.

- Distribution leverage - strong publisher relationships, platform-holder connections, or owned channels.

How private equity thinks about game studios

Private equity (PE) buys businesses with a plan to sell them later - usually in 3-7 years.

What that means for you:

- Entry multiple vs exit multiple: PE wants to buy at a sensible price and sell at a similar or higher multiple later. They worry if your revenue is too "spiky" because exit buyers discount uncertainty.

- Who they can sell to later: strategics (publishers, platform-adjacent groups), larger PE funds, or a public listing in some markets.

- Levers they expect to pull:

- Stabilize revenue via live-ops, DLC, and portfolio expansion

- Improve margins through production discipline and shared services

- Add bolt-ons (small studios, service teams, IP libraries)

- Build repeatable pipeline governance, not hero-based delivery

3. Deep Dive: Recurring Revenue vs Hit-Driven Revenue - The Single Biggest Multiple Driver

If there is one valuation question that shows up again and again in game development, it is this:

How much of your revenue is repeatable and predictable - and how much depends on your next launch landing perfectly?

In the data, you can see why this matters. Segments with stronger ongoing monetization and operator-style economics often support higher valuation outcomes than pure project-based development, because buyers can underwrite them with more confidence.

Why buyers care so much

Buyers are not allergic to hit-driven upside - they just hate not knowing what they are buying.

Predictability shows up as:

- A back catalog that keeps selling without heroic marketing spend

- Live-ops content cadence that retains and monetizes players

- DLC and expansions with known conversion patterns

- Multiple titles contributing meaningfully, not one title carrying the studio

How this factor shows up in market outcomes

Private market precedent deals show higher EV/Revenue for mobile casual/puzzle developers (average ~6.0x, median ~6.3x) than co-dev/services studios (average ~1.0x, median ~1.1x). That spread reflects how buyers price "repeatable operator economics" vs "contract margin businesses." (Both can be great businesses - they are just valued differently.)

Similarly, AAA/PC-console developers (original IP & franchises) show a wider range (average ~4.0x, median ~4.7x EV/Revenue), reflecting that some studios have de-risked monetization and others are still heavily dependent on a few big launches.

How you move from lower-value to higher-value profile

You do not need to transform into a mobile F2P machine to improve predictability. The goal is to reduce "single title dependency" and increase the share of revenue that persists.

Practical moves buyers recognize:

- Strengthen post-launch monetization: DLC plans, seasonal content, expansions

- Build a measurable community engine: wishlists, Discord, creator programs, retention KPIs

- Create a portfolio: even 2-3 smaller releases that contribute steady cash can change the underwriting

- Add selective services work to smooth the troughs (without becoming a pure services shop)

Mini-table: lower-value vs higher-value profile

4. What Game Development Businesses Sell For - and What Public Markets Show

The cleanest way to think about valuation is this:

- Private deals show what buyers actually paid for similar assets.

- Public multiples show what the market thinks comparable businesses are worth today.

- Your valuation usually lands somewhere in between, adjusted for your scale, growth, risk, and scarcity.

The numbers below are illustrative benchmarks - they are not a pricing promise.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions dataset, the overall average and median EV/Revenue is ~3.4x, with overall EV/EBITDA ~14.2x. But the spread by business model is meaningful.

Here are the clearest "like-for-like" group signals:

A few patterns to internalize:

- Mobile casual/puzzle and retro/remaster models tend to hold higher revenue multiples because the cash flows are easier to predict and monetize repeatedly.

- Services studios can have very respectable EBITDA multiples when margins are strong, but revenue multiples stay lower because growth is more people-dependent.

- AAA/PC-console can be premium, but the range is wide because buyers are underwriting execution risk as much as past performance.

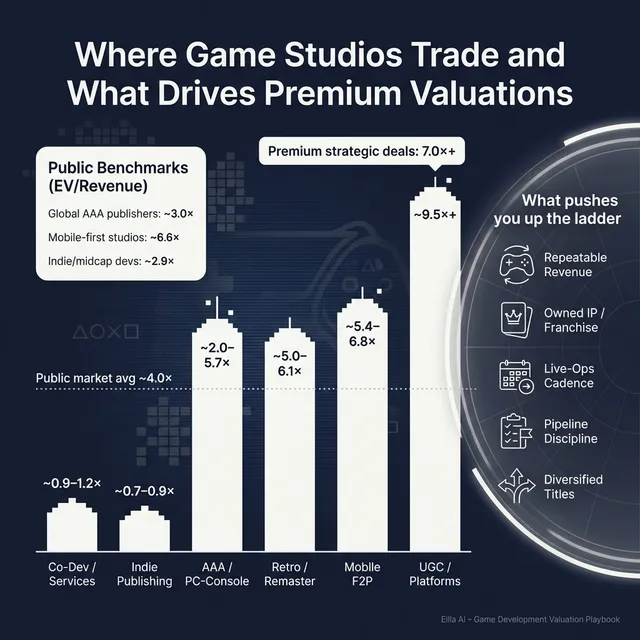

4.2 Public Companies

Public markets are noisy, but they give you a reality check. Across the public group dataset, the overall average EV/Revenue is ~4.0x and overall average EV/EBITDA is ~14.6x.

By segment, the averages and medians show how investors price different business models (as of mid/end-2025 data):

How to use this as a private founder:

- Treat public multiples as a reference band, not your price tag.

- Adjust down for smaller scale, more concentration, weaker margins, less proven monetization.

- Adjust up (sometimes) for scarcity - if you own a rare IP or a uniquely valuable team in a hot niche, strategics can pay above what public comps imply.

5. What Drives High Valuations (Premium Valuation Drivers)

Premium outcomes are not random. They usually have a simple story: buyers can underwrite growth and durability, and they can see multiple ways to win.

Based on the observed premium drivers in the deal data, plus what consistently matters in game M&A, the big themes are:

5.1 Scale with proven live-ops economics

In mobile free-to-play, premium outcomes are strongly associated with scale plus retention proof, often paired with earnouts that pay for future performance. When cohorts, monetization, and content cadence are measurable, buyers are willing to pay more because growth is not just a pitch - it is a model.

Founder translation: if you can show that players stick, spend, and return as you add content, buyers see a machine, not a gamble.

5.2 IP and franchise leverage with strong gross margins

Premium deals cluster where studios own or control enduring IP and monetize it across multiple channels: direct sales, DLC, remasters, licensing, and sometimes events. This reduces hit risk because a franchise can keep paying you even when new releases slow down.

Founder translation: "We ship good games" is not the premium story. "We own a franchise that can generate revenue repeatedly" is.

5.3 High-margin, contract-backed co-development capability

For services and co-dev studios, premium outcomes show up when the business has:

- repeat AAA clients

- visible backlog

- strong EBITDA margins

- consistent delivery record

Founder translation: buyers pay more when they believe revenue will still exist next year even if one client pauses.

5.4 Niche focus with strong profit conversion

Some studios do not need mega-scale to be valuable. If you have a clear niche, loyal demand, and disciplined cost control, you can produce strong EBITDA on modest revenue. In the data, niche-focused studios with strong revenue-to-EBITDA conversion supported low double-digit EBITDA multiples in acquisitions.

Founder translation: you do not need to be the biggest studio - you need to be predictably profitable in a lane you can own.

5.5 Performance-aligned earnouts that signal growth visibility

Earnouts are not just a legal structure - they are a pricing tool. In the data, several premium deals used earnouts tied to multi-year revenue and EBITDA targets. That usually happens when the buyer sees upside but wants to pay for it as it arrives.

Founder translation: earnouts can increase headline valuation if you have measurable milestones and a credible plan to hit them.

5.6 High-margin licensing and media adjacencies

When IP extends into merchandise, animation, books, or other media, buyers often price the business more like an IP platform than a single studio. This compresses hit risk and improves margin durability.

Founder translation: if your IP can live outside the game, you are selling more than a product - you are selling an asset with multiple revenue doors.

5.7 The boring stuff that still matters

Even the best creative story gets discounted if fundamentals are messy:

- clean title-level reporting

- consistent KPIs and dashboards

- diversified revenue sources

- leadership bench beyond the founder

- clear contracts, IP ownership, and employee agreements

6. Discount Drivers (What Lowers Multiples)

Lower multiples are usually not punishment - they are math. Buyers reduce price when they see uncertainty, concentration, or hidden cost.

Here are the most common valuation drag factors in game development:

6.1 Single-title dependency with no back catalog

If most value depends on one upcoming launch, buyers treat your revenue like a risky forecast, not a stable base. That typically pushes you toward the low end of comparable ranges.

6.2 Weak proof of retention and monetization

If you claim live-ops potential but cannot show retention curves, spending behavior, or content cadence outcomes, buyers assume "unproven" and price accordingly.

6.3 Unclear IP ownership or licensing constraints

Anything fuzzy around IP rights creates deal friction. Buyers either demand strong reps and warranties (and holdbacks), or they discount.

6.4 Customer or partner concentration

A single publisher relationship, a single platform, or one outsized contract can be a hidden risk. The business may still sell well - but multiples often compress because revenue feels fragile.

6.5 Cost structure that is hard to flex

Studios with high fixed costs and limited ability to scale down between releases scare buyers. They worry about funding the gap if a title slips.

6.6 Team fragility and key-person risk

If success depends on 2-3 individuals who might leave after a sale, buyers will bake that risk into price and structure (earnouts, retention packages, escrow).

6.7 Messy financial records

If your numbers are hard to trust - inconsistent capitalization policies, unclear allocation across projects, limited forecasting - buyers assume there are problems they have not found yet.

7. Valuation Example: A Game Development Company

This is a worked example to show the logic - not investment advice and not a formal valuation.

The fictional company

"Northstar Forge" (fictional) is a privately held PC/console game development studio:

- Revenue: USD 10.0m (fictional)

- Team: ~250 employees

- Business model: premium PC/console development, mix of original IP and publisher-funded work

- Current reality: project-based economics, early back catalog, limited licensing revenue today

Step 1: Pick the right valuation yardstick

If you do not have stable, meaningful EBITDA (common in studios investing ahead of launches), buyers often anchor on EV/Revenue for studios like yours. That is consistent with how comparable developer assets are referenced in the provided market logic.

Step 2: Narrow to a credible multiple band

Using the most relevant private and public comp signals for PC/console developers:

- Public developer clusters support a practical band roughly ~1.5x-4.0x EV/Revenue depending on IP traction and margins.

- Private AAA/PC-console developer deals show a broader band, roughly ~2.0x-5.7x EV/Revenue, reflecting that some assets have premium IP or de-risked economics.

For a USD 10m revenue studio without proven licensing or scaled live-ops, a reasonable core range is often around ~2.0x-4.5x EV/Revenue (illustrative).

Step 3: Apply base, premium, and downside scenarios

What would justify each?

- Discounted case: one-title dependency, weak milestone confidence, unclear IP rights, messy reporting, or heavy cash burn with limited runway.

- Core range: credible pipeline, some back catalog, strong team, clear contracts, and believable next release plan.

- Premium case (harder, but possible): owned IP with demonstrated traction, high-margin monetization, clear expansion path (DLC/sequels), or a niche where you are a scarce asset.

What this means for you

Two studios can both have USD 10m in revenue and be worth very different amounts. Buyers are not paying for your current revenue line - they are paying for their confidence that revenue can repeat and expand without blowing up risk.

If you want to change your valuation, you usually do it by changing underwrite-ability: repeatability, proof, and reduced downside.

8. Where Your Business Might Fit (Self-Assessment Framework)

This is a simple way to sanity-check where you might land in the valuation spectrum. Score each factor 0-2:

- 0 = weak / not proven

- 1 = decent / partial

- 2 = strong / well-proven

Scoring table

How to interpret your score (roughly)

- 16-22: closer to premium outcomes - buyers can underwrite you with confidence.

- 10-15: fair market - good business, but some risks will cap multiples.

- 0-9: likely discounted - you may want to fix key risks before running a process.

The goal is not to "score high." The goal is to identify the 2-3 items where improvement will most directly change buyer confidence.

9. Common Mistakes That Could Reduce Valuation

9.1 Rushing the sale

A rushed process usually produces one or two lukewarm offers and little leverage. In game dev, a rushed sale is extra dangerous because buyers need time to diligence pipeline, IP rights, and retention metrics.

9.2 Hiding problems

Problems always surface in diligence: a delayed milestone, an IP ambiguity, a team retention risk, a weak title-level P&L. If buyers feel surprised, they do not just reduce price - they start to doubt everything else you say.

9.3 Weak financial records

This is one of the highest ROI fixes in 6-12 months. Game studios often have messy allocation across projects, inconsistent capitalization policies, and unclear revenue timing. Buyers discount uncertainty because it feels like risk.

Simple improvements that matter:

- title-level revenue and cost breakdowns

- consistent treatment of dev costs

- clear headcount allocation by project

- KPI reporting for live titles (retention, monetization, engagement)

9.4 Not running a structured, competitive sale process with an advisor

A structured, competitive process typically produces meaningfully higher purchase prices - research often cites improvements around 25% when a professional advisor runs a competitive process instead of a single-buyer negotiation. The reason is simple: competition forces buyers to bid their true best offer.

9.5 Revealing what price you are after too early

If you tell a buyer you want "USD 40m," you usually destroy price discovery. Instead of learning what the market would pay, you invite offers of USD 40.1m and USD 40.2m. Your job is to let the market tell you what you are worth.

9.6 Industry-specific mistake: treating pipeline as "creative only"

Buyers love creativity. They also need governance. Studios that cannot explain milestones, burn, and delivery risk in a crisp way get discounted - even if the game looks great.

9.7 Industry-specific mistake: unclear IP chain of title

Especially with contractors, co-dev partners, licensed music, and engine terms, small paperwork gaps can become huge valuation problems late in diligence.

10. What Game Development Founders Can Do in 6-12 Months to Increase Valuation

You do not need a miracle. You need a plan that makes your business easier to underwrite.

10.1 Improve the numbers buyers trust

- Build title-level P&Ls and a consistent way to allocate shared costs.

- Produce a rolling 18-24 month forecast with milestone-linked assumptions.

- If you have live titles, formalize a KPI pack (retention, ARPDAU if relevant, churn, conversion, content cadence).

- Tighten working capital basics (collections, vendor terms) - buyers notice.

10.2 Increase repeatability without changing who you are

- If you are PC/console premium, strengthen post-launch monetization plans (DLC, expansions, live events).

- Build a back catalog strategy: remasters, bundles, platform ports, seasonal promos.

- Reduce single-title dependency by making sure at least two revenue sources exist (even if one is smaller).

10.3 De-risk pipeline and delivery

- Turn your roadmap into a buyer-friendly artifact: milestones, staffing plan, risks, mitigations.

- Show how you prevent overruns: gating decisions, scope discipline, external QA plans.

- If you rely on publisher funding, clarify the contract economics and downside scenarios.

10.4 Strengthen the IP story

- Clean up IP ownership: contractor assignments, licensing rights, trademark filings where appropriate.

- If your IP has any transmedia potential, document it: merch pilots, licensing inquiries, community signals.

- Create a simple narrative: what your IP is, who it resonates with, and why it can live beyond one title.

10.5 Build a team that looks transferable

- Put in place a leadership bench: production, tech, creative, live-ops (as relevant).

- Identify key retention risks and pre-plan incentives.

- Document processes so the buyer sees a studio system, not a studio personality.

10.6 Prepare for deal process mechanics

- Create a clean data room: contracts, HR, IP, financials, KPIs.

- Pre-empt buyer questions: platform concentration, publisher dependencies, engine/tool licenses.

- Build a buyer narrative that is honest about risks but clear about how they are managed.

11. How an AI-Native M&A Advisor Helps

Selling a game development business is not just finding "a buyer." It is finding the right set of buyers, running a process that creates competition, and packaging your studio in a way that makes risk feel manageable.

Higher valuations through broader buyer reach: AI can expand the buyer universe to hundreds of qualified acquirers by matching on deal history, synergy fit, financial capacity, and strategic intent. More relevant buyers means more competition, stronger offers, and more fallback options if one buyer drops - which increases the chance your deal actually closes.

Initial offers in under 6 weeks: AI-driven buyer matching, faster outreach, and streamlined creation of marketing materials can materially shorten the time from "we should explore a sale" to "we have real conversations and initial offers." Speed matters because momentum and competitive tension are value drivers.

Expert advisory, enhanced by AI: The strongest outcomes still require experienced human deal leadership - framing, negotiating, and running a tight process. AI strengthens that work by improving buyer targeting, tightening diligence preparation, and helping present your business in the buyer’s language with professional materials and clear metrics. The outcome is Wall Street-grade process quality without traditional bulge bracket costs.

If you would like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.