The Complete Valuation Playbook for GovTech Businesses

A practical guide on how GovTech businesses are valued and what drives high multiples.

If you run a private GovTech business and are thinking about a sale in the next 1-12 months, valuation is not just a finance question. It is a market positioning question. The same USD 10m revenue business can be worth very different amounts depending on how buyers see its product fit, revenue quality, implementation risk, and role inside the government software stack.

This is a useful time to think about valuation because GovTech is still consolidating. Strategic buyers are building broader workflow suites, private equity remains active in software, and buyers are looking hard at assets that help public agencies automate work, stay compliant, and operate with fewer people. But they are also selective. In GovTech, quality matters more than headline growth alone.

This playbook shows what GovTech businesses actually sell for, what tends to push valuations up or down, how to roughly self-assess where your business sits today, and what you can realistically do in the next 6-12 months to improve the outcome.

1. What Makes GovTech Unique

GovTech is not one thing. It includes core public administration software such as ERP, tax, records, permitting, case management, grants, and benefits systems. It also includes workflow and low-code tools used by public agencies, data and reporting platforms, document and information management, and more specialized software in areas like health and social services, compliance, inspections, and procurement.

That matters because buyers do not value all of these businesses the same way. A recurring software platform embedded in a local government's daily workflows will usually be valued very differently from a business that looks more like a project-based systems integrator, even if both serve the public sector. In GovTech, who pays you, how sticky you are, and how much of your revenue is truly repeatable are central valuation questions.

The sector also has structural features that make valuation different from generic software. Sales cycles are longer. Procurement rules matter. Winning the customer is hard, but once you are embedded, switching can be painful. That can create strong retention and long customer lives - but only if your implementation model, support model, and product quality actually hold up.

Buyers will always look closely at a few GovTech-specific risks. They will ask how concentrated your revenue is across agencies and contracts. They will look at how dependent growth is on a few procurements landing on time. They will test whether your software is truly mission-critical or whether it is a layer that could be replaced. They will also examine integration depth, data security, compliance posture, and how much key customer knowledge sits in the founder's head.

In plain English: GovTech can be very attractive because customers tend to stay, contracts can be long, and the software often sits close to important public workflows. But the sector is also unforgiving if your growth depends on a handful of slow-moving deals, custom work, or founder relationships that do not transfer.

2. What Buyers Look For in a GovTech Business

At the simplest level, buyers look for four things: scale, growth, profitability, and predictability. Scale matters because bigger businesses usually feel less risky. Growth matters because buyers want future upside. Profitability matters because it shows the business can convert revenue into cash. Predictability matters because that is what lets a buyer underwrite the return.

In GovTech, those basics are filtered through a different lens. Buyers care less about whether you can tell a broad software story and more about whether your product is truly embedded in public-sector operations. They want to know whether your software helps agencies run important workflows - such as finance, records, permitting, inspections, case handling, or reporting - and whether replacing you would be difficult and disruptive.

They also care about revenue quality. A business with recurring subscription revenue, annual renewals, multi-year contracts, and strong customer retention will get more attention than one with lumpy implementation work and one-off projects. Services revenue is not bad, especially in GovTech where onboarding and integration are often required, but buyers usually prefer services that support software adoption rather than services that are doing the real work of the business.

Customer profile matters too. A company selling to dozens or hundreds of agencies is usually easier to value than one relying on two or three large contracts. Buyers will look at whether you serve municipalities, counties, central government, schools, public health agencies, or quasi-public entities - and whether that customer mix creates stability or concentration risk.

PE buyer thinking in simple terms

A private equity buyer usually thinks in a more mechanical way than a strategic buyer. They ask what they are paying today, what they can improve over the next 3-7 years, and who they can sell the business to later.

They care about entry multiple versus exit multiple. If they buy your company at a high price, they need a believable plan to grow revenue, improve margins, make acquisitions, or strengthen the product so they can sell it later at an equal or better multiple. They will also think about the next buyer: will this eventually be attractive to a larger software group, a bigger private equity fund, or a strategic acquirer building a broader GovTech suite?

The levers they expect to pull are usually practical. Price increases where contracts are underpriced. Better cross-sell across modules. Cleaner go-to-market. Lower implementation drag. Better reporting and KPI discipline. Tighter cost control. In some cases, add-on acquisitions that expand geography, product scope, or customer access.

A strategic buyer, by contrast, may pay more if your software fills an important product gap, deepens its reach into government customers, or creates strong cross-sell opportunities into its installed base.

3. Deep Dive: Productized Platform vs Services-Heavy GovTech

This is one of the biggest valuation questions in GovTech because many businesses sit somewhere between software company and specialist delivery partner. Buyers know public-sector software often needs implementation, configuration, data migration, training, and ongoing support. The question is not whether services exist. The question is whether the software is leading the relationship - or whether services are.

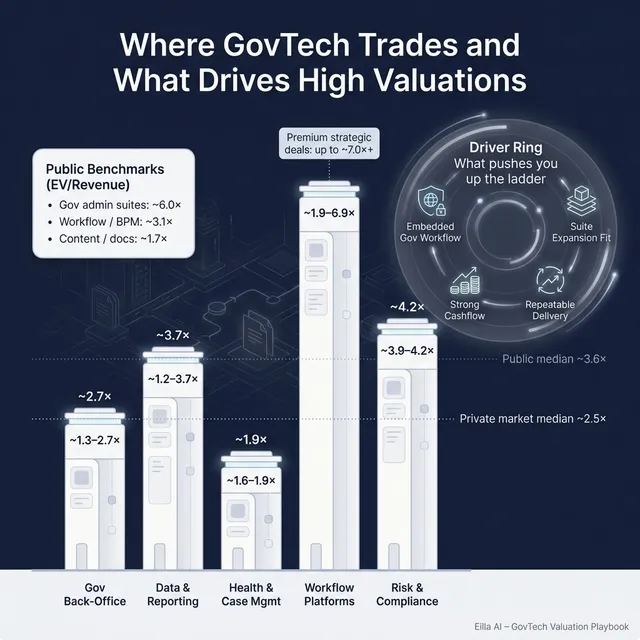

The market data strongly points to this distinction. The worked valuation logic in your sources narrows the most relevant range for a small GovTech workflow and data platform to about 1.9x to 4.2x revenue, with caution around pushing above roughly 4.0x without clear evidence of exceptional growth, retention, or gross margin. That logic reflects a real pattern: smaller private GovTech and workflow businesses can command good valuations, but services intensity and implementation dependence often cap how far buyers are willing to stretch.

Why do buyers care so much? Because a product-led business scales better. If new customers can be deployed with repeatable workflows, standard integrations, and a defined support model, a buyer sees margin expansion and easier growth. If every new customer requires a semi-custom build, heavy founder involvement, and long delivery cycles, the buyer sees execution risk and a harder path to scaling.

This also affects how buyers think about revenue quality. Software revenue feels durable when the product is embedded and supportable by a broader team. Services-heavy revenue feels less durable if it depends on custom work, specific people, or a project pipeline that must constantly be refilled.

The good news is you do not need to become a pure horizontal SaaS company to improve your profile. In GovTech, some services are normal and even valuable. What buyers want to see is a business where services help land and expand the software, not a business where software is just an excuse to sell services.

If your business looks more like the left side today, the path forward is practical. Standardize implementations. Package modules more clearly. Separate recurring support from project work. Track gross margin after delivery costs. Show buyers that new customers are getting easier to deploy, not harder.

4. What GovTech Businesses Sell For - and What Public Markets Show

The most useful way to think about valuation is to combine two lenses. First, what similar private businesses have sold for. Second, what relevant public software groups trade at. Private deals are usually more relevant for a smaller private GovTech company, while public trading levels help set the outer boundaries of what the market considers attractive or expensive.

The headline lesson from the source data is straightforward. Private GovTech and adjacent workflow deals most often sit in the low-to-mid single digit revenue multiple range, while public software groups can trade materially higher depending on scale, growth, margins, and strategic positioning. That does not mean your business should be priced off public market averages. It means public comps are a reference point, not a price tag.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions provided, the overall average was 3.4x EV/Revenue and the median was 2.5x EV/Revenue. On EBITDA, the overall average was 23.2x and the median was 12.7x. That already tells you something important: there are some premium outcomes, but the center of the market is more modest than many founders expect.

For the most relevant private segments, the worked valuation logic points to these 25th-75th percentile ranges. Public sector back-office and government financial software sits around the lower end of the set, while workflow, compliance, and certain integration-ready platforms can pull higher. The broad pattern is that buyers pay more when the product is mission-critical, scalable, and useful as a bolt-on to a larger suite - and less when growth is slower, services are heavier, or revenue quality is less obvious.

A few patterns matter. First, very high headline multiples can be misleading when the target is tiny. One deal in the data reached 19.0x revenue, but on a very small revenue base, where even a modest purchase price can inflate the multiple. Founders should not treat those outliers as normal clearing prices. Second, strong EBITDA margins can support better EBITDA multiples even when revenue multiples look only moderate. In other words, some buyers pay for cashflow quality, not just growth.

These ranges are illustrative, not definitive. Your exact valuation will depend on customer stickiness, implementation burden, concentration, growth, margins, and how strongly a buyer sees you as a strategic fit.

4.2 Public Companies

The public market data is useful mainly as context. Across all public companies in the data, the average was 9.2x EV/Revenue and the median was 3.6x EV/Revenue. The average is lifted by some very large or unusual names, so the median is often the more realistic anchor for founders. On EBITDA, the overall average was 28.3x and median 16.2x.

For GovTech-relevant public groups as of mid-to-late 2025, core public administration software generally trades above many smaller vertical software businesses, while workflow, content, and information management names sit in more moderate bands. Large horizontal software platforms can trade well, but they are not clean comparables for a smaller private GovTech company because scale, liquidity, and margin profile are completely different.

*This segment is not a clean anchor for small private GovTech companies because the dataset includes extreme outliers.

The public market tells founders three practical things. First, scaled, profitable, sticky public-sector software can command strong valuations. Second, most smaller private companies should expect some discount versus public comps because they are less liquid, less diversified, and riskier. Third, scarce assets can still punch above their size if they clearly strengthen a larger buyer's product suite or government footprint.

So use public multiples as a valuation band, not a promised outcome. In most cases, a small private GovTech business should be marked below public peers for size, concentration, and execution risk. In some cases, a highly strategic asset can narrow that gap or even outperform what the basic numbers suggest.

5. What Drives High Valuations (Premium Valuation Drivers)

The source data shows that premium outcomes in GovTech and adjacent workflow software do not come from one thing alone. They usually come from a combination of strategic fit, credible growth, strong economics, and lower integration risk. Here are the themes that matter most.

A. You expand a buyer's platform into a new workflow

This is one of the clearest patterns in the deal data. Buyers paid up when a target helped extend an existing software suite into a useful adjacent workflow or vertical. In practice, that means your company is not just a standalone tool - it helps a larger buyer sell more modules, deepen customer relationships, or become harder to replace.

Why buyers pay more: the value to them is bigger than your standalone profits. They may see cross-sell into their installed base, faster product expansion, or a chance to own a broader workflow.

Examples founders can relate to:

- You sit next to budgeting, permitting, payments, inspections, or records in a way that naturally expands a larger public-sector platform.

- Your software plugs into common government systems and can be attached to a broader suite.

- You have repeatable modules that could be sold into the buyer's existing agency customers.

B. Your revenue has visible upside, and buyers can underwrite it

Several deals in the source set used earn-outs or performance hurdles. That often means the buyer believed there was real upside, but wanted some protection around timing or delivery.

Why buyers pay more: if they see believable growth after closing, they may support a higher headline price. In GovTech, that can be especially relevant where procurement cycles are slow but the pipeline is strong.

Examples:

- You have signed contracts that are still ramping.

- You have a clear expansion path from one agency department into others.

- Your pipeline includes realistic cross-sell or rollout opportunities rather than speculative logos.

C. Your business looks like software, not custom consulting

Even in GovTech, buyers reward repeatability. They want evidence that implementations follow a playbook, integrations are reusable, and support is manageable without founder heroics.

Why buyers pay more: repeatable delivery means lower risk and better future margins.

Examples:

- A standard onboarding method instead of reinventing each deployment.

- Product configuration replacing custom development.

- Clear support tiers and customer success processes.

D. You already produce attractive cashflow

The deal data shows several cases where buyers paid strong EBITDA multiples for workflow and compliance software with good margins. That tells founders an important truth: in GovTech, strong cashflow can be just as valuable as fast topline growth.

Why buyers pay more: profitable software gives downside protection. If growth slows temporarily, the buyer still owns a business that throws off cash.

Examples:

- Healthy EBITDA margins because delivery is efficient.

- Good gross margins after accounting for implementation and support.

- Low churn, so revenue does not need to be constantly replaced.

E. You have real public-sector moats

GovTech moats are often less flashy than consumer tech moats, but they can be powerful. They include procurement knowledge, agency credibility, trusted integrations, workflow embeddedness, domain expertise, and long-term customer relationships.

Why buyers pay more: these moats make revenue harder to disrupt and growth easier to repeat.

Examples:

- Deep integration into government data, identity, finance, or case systems.

- Products designed around actual public-sector workflows rather than adapted from private-sector tools.

- Strong references in a niche where trust matters, such as tax, social services, public health, or compliance.

F. Management continuity lowers execution risk

Founder reinvestment and post-deal continuity showed up in the data as a positive signal. This is especially important in GovTech, where relationships, procurement knowledge, and product know-how are often concentrated in a few people.

Why buyers pay more: if key people stay and remain motivated, the buyer is more confident the customer base and product roadmap will hold together after closing.

Examples:

- A founder willing to stay through transition.

- A second layer of leaders who can run delivery, product, and customer relationships.

- Commercial and technical knowledge spread across a team, not trapped in one person.

G. Clean fundamentals still matter

Not every premium driver is sector-specific. Clean financials, predictable recurring revenue, diversified customers, reliable KPI reporting, and a strong management bench all improve buyer confidence.

Why buyers pay more: certainty is valuable. Buyers pay better prices for businesses they can understand, diligence, and integrate without surprises.

6. Discount Drivers (What Lowers Multiples)

Discounts usually happen when a buyer sees risk, complexity, or weak transferability. Many founders focus on the headline multiple they want, but the real question is what gives a buyer the confidence to pay toward the top of the range - or the reasons to stay near the bottom.

A common discount in GovTech is heavy dependence on custom work. If every deployment is different, margins are hard to predict and growth is harder to scale. Buyers may still like the market and customer base, but they will usually underwrite you more like a services-led business than a software platform.

Another clear discount driver is revenue concentration. If one or two agencies or contracts make up too much of revenue, the buyer will worry about renewal, budget cycles, and procurement timing. The same is true if growth depends on a handful of large opportunities that have not yet closed. In GovTech, pipeline quality matters - but timing risk is real.

Small scale can also distort expectations. The data includes very high headline multiples on tiny revenue bases, but those are not safe benchmarks for most founders. Buyers know small businesses can be more fragile, more founder-dependent, and more exposed to delivery issues. If your revenue is modest and team depth is thin, the buyer will likely apply a size discount unless there is a very strong strategic reason not to.

Weak profitability or unclear delivery economics can lower value fast. If your gross margin looks good before implementation and support costs, but much weaker after, a buyer will catch that. If EBITDA is low because the model is genuinely inefficient rather than because you are investing for growth, they will likely mark the business down.

Other classic M&A discount drivers still apply:

- messy financial reporting

- unclear revenue recognition

- churn or low customer expansion

- weak product roadmap

- founder-centered customer relationships

- legal, security, or compliance gaps

- long implementation backlogs

- poor referenceability from customers

The good news is that many of these issues are fixable. A discount is not always a permanent label. Often it is a sign that the business needs better packaging, clearer metrics, or a few quarters of cleaner execution before going to market.

7. Valuation Example: A GovTech Company

To make the valuation logic concrete, here is a fictional example. The company below is fictional, and the USD 10m revenue figure is fictional. The valuation ranges are illustrative only. They are designed to show how buyers think, not to provide investment advice or a formal valuation.

Step 1: Start with the right comp set

Assume CivicFlow, a fictional GovTech company, sells workflow and reporting software to local and regional government agencies. It helps automate permitting, internal approvals, case routing, and performance reporting. It has meaningful recurring software revenue, but also some implementation and integration work.

The right valuation approach is not to compare CivicFlow to giant horizontal software companies. It is to anchor on the most relevant public and private groups from the source data:

- private GovTech back-office deals

- private workflow platform deals

- private data and analytics software deals

- public GovTech core administration and workflow software groups

The worked logic in the source material narrows the most defensible range for a small GovTech workflow and data platform to roughly 1.9x to 4.2x revenue. That range makes sense because it captures the strengths of the category - sticky workflow software, public-sector fit, possible strategic adjacency - while acknowledging the limits of smaller scale and likely implementation intensity.

Step 2: Apply the logic to the fictional company

Assume CivicFlow has:

- USD 10m revenue

- strong customer retention

- a recurring software core

- some services tied to implementation

- good public-sector references

- moderate growth

- decent, but not elite, margins

A reasonable base case would be somewhere in the middle of that narrowed band. If the business looks productized, has diversified customers, and clearly fits into a larger acquirer's suite, it could move toward the upper end. If it relies heavily on custom work, is concentrated in a few agencies, or lacks clean metrics, it could fall toward the lower end.

Step 3: What changes the outcome

Here is how two USD 10m GovTech businesses end up with very different values.

A lower-end case might have:

- customer concentration

- services-heavy delivery

- limited management depth

- weak visibility into retention and expansion

- implementation bottlenecks

A premium case might have:

- highly repeatable deployments

- strong recurring revenue mix

- embedded integrations into government systems

- evidence of module expansion or cross-sell

- good EBITDA margins and clean reporting

- obvious fit for a larger strategic platform

That is the real lesson for founders. Revenue size matters, but it is not the whole story. In GovTech, the quality of the revenue and the strategic usefulness of the product often matter just as much.

8. Where Your Business Might Fit (Self-Assessment Framework)

The goal of this framework is not to produce a fake precise number. It is to help you honestly assess whether your business looks closer to the low end, middle, or high end of the market.

Score each factor from 0 to 2:

- 0 = weak

- 1 = mixed

- 2 = strong

Self-assessment table

How to interpret the score

As a rough guide:

If you score in the lower band, that does not mean you should never sell. It means buyers will likely focus on risk and push for protection, lower headline multiples, or earn-outs. If you score in the middle, you probably have a marketable asset but need a strong process and good positioning. If you score near the top, you are much more likely to create tension among buyers and pull valuation upward.

Use this exercise honestly. The point is not to flatter yourself. The point is to identify the few improvements that would have the biggest impact before going to market.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders sometimes decide to sell, pull a few numbers together, and start taking meetings. That usually leaves value on the table. Buyers pay more when the financials are clean, the story is clear, and the process is run with discipline.

Another major mistake is hiding problems. In M&A, problems nearly always surface in diligence. If you have customer concentration, churn issues, delivery delays, pricing problems, or security gaps, those issues are usually manageable if framed honestly and addressed early. They become much more damaging when discovered late because trust collapses.

A third mistake is weak financial records. This is especially costly when you could fix the issue within 6-12 months. Many GovTech companies can improve valuation just by cleaning up revenue reporting, separating software from services revenue, tracking cohort retention, measuring gross margin properly, and showing which parts of the business are actually improving.

A fourth mistake is running an unstructured sale process. A structured, competitive process with an advisor usually leads to better outcomes because more buyers see the opportunity, the positioning is tighter, and tension is created between bidders. Research commonly shows that a competitive process with an advisor can lift purchase price meaningfully - often by around 25% - versus a weak one-on-one negotiation.

A fifth mistake is revealing what price you want too early. This kills price discovery. If you tell buyers you want USD 10m of enterprise value, many will simply cluster around that number with offers like USD 10.1m or USD 10.2m instead of showing what they might really pay in a competitive process.

There are also GovTech-specific errors. One is failing to explain procurement timing clearly. Buyers who do not know your space may treat pipeline timing as weakness unless you help them understand the normal budget, approval, and implementation cycle. Another is failing to distinguish product IP from customer-specific customization. In GovTech, buyers need to know what is transferable, scalable product - and what is just custom work dressed up as software.

10. What GovTech Founders Can Do in 6-12 Months to Increase Valuation

You do not need a total reinvention before a sale. In most cases, valuation improves when you make the business easier to understand, easier to underwrite, and easier to scale.

A. Improve the numbers buyers care about

Start by separating recurring software revenue from implementation, support, and other services. Track gross margin more accurately, including delivery costs. Show retention clearly. Build a simple monthly dashboard that covers bookings, renewals, churn, expansion, average contract value, and revenue by customer.

If margins are improvable, take the easy wins. Reprice underpriced contracts where you can. Tighten delivery scope. Reduce custom work that does not lead to repeatable product value. Buyers notice improvement trends even before they are fully mature.

B. Make the business look more productized

Document your implementation process. Standardize integrations where possible. Package modules clearly. Show that each new customer does not require a fresh invention.

This matters because it moves you toward the part of the market that gets credit for repeatability and scale. Even modest progress here can change how buyers frame the business.

C. Strengthen your strategic story

Map where your product sits in the public-sector workflow. Which systems do you connect to? Which adjacent modules could a buyer cross-sell? Why are you hard to rip out once installed?

Do not just say you are "innovative." Show why your software matters in the stack. Buyers pay more when they can easily explain the strategic fit to their own board or investment committee.

D. Reduce concentration and transfer risk

Try to broaden the customer base if concentration is high. If that is not realistic in 6-12 months, at least show a credible plan and frame concentration honestly. Build deeper relationships below the founder level. Make sure customer knowledge, product knowledge, and procurement knowledge are shared across the team.

If a buyer thinks the business walks out the door with one founder or one salesperson, value goes down. If the business looks transferable, value improves.

E. Prepare for diligence before the process starts

Clean up contracts. Organize security and compliance documents. Make sure revenue recognition is explainable. Prepare a clear customer list, churn history, pipeline summary, and product roadmap.

This reduces friction and supports confidence. Many good businesses lose momentum in diligence not because the company is bad, but because the company is not ready.

F. Consider how to use earn-outs intelligently

If your pipeline is strong but timing is uncertain because of procurement cycles, a well-structured earn-out may help bridge valuation gaps. That is not always ideal, and cash at close is usually better, but in GovTech it can be a practical way to monetize future wins buyers believe in but do not want to fully prepay for.

The key is not to let the earn-out hide a weak base valuation. It should reward real upside, not replace value that should have been paid upfront.

11. How an AI-Native M&A Advisor Helps

A good exit is not just about finding one interested buyer. It is about running a process that creates competition, keeps momentum, and positions your business in the strongest possible way. That is where an AI-native advisor can change the outcome.

First, AI expands buyer reach. Instead of relying on a narrow list of obvious acquirers, an AI-native process can identify hundreds of qualified buyers based on deal history, product fit, likely synergies, financial capacity, and other signals. More relevant buyers usually means more competition, stronger offers, and a better chance the deal actually closes if one bidder drops out.

Second, AI speeds up the front end of the process. With AI-driven buyer matching, faster creation of marketing materials, and better support during diligence, initial conversations and first offers can often be reached in under 6 weeks. That does not mean the whole deal closes instantly. It means the process gets to market faster and with more precision.

Third, the best AI-native firms combine software with real advisory judgment. You still want experienced human M&A advisors running the process, shaping the narrative, and negotiating with buyers. The benefit is that AI makes that advisory work broader, faster, and more scalable - giving you Wall Street-grade preparation and buyer coverage without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.