The Complete Valuation Playbook for Healthcare Consulting Businesses

A data-driven guide to how healthcare consulting businesses are valued and what drives high multiples.

If you run a privately held healthcare consulting business and you are thinking about a sale in the next 1-12 months, the biggest risk is not “getting a bad multiple.” It’s misunderstanding what buyers are actually paying for in this sector - and leaving value on the table because you did not package your business the way buyers evaluate it.

Healthcare consulting is in a very “buyer-sensitive” moment: payers and providers are under margin pressure, regulation keeps shifting, and strategic buyers are consolidating capabilities in data, workflows, and operational execution. That makes some consulting businesses feel indispensable - and others feel like interchangeable labor.

This playbook is built from real market data in the sources you provided (private deal multiples, public trading multiples, and observed premium/discount drivers), plus practical M&A pattern recognition. You’ll see what businesses like yours sell for, what pushes multiples up or down, and a simple self-assessment + 6-12 month action plan to move toward a premium outcome.

1. What Makes Healthcare Consulting Unique

Healthcare consulting is not valued like “general consulting” because healthcare has three features that change buyer behavior:

- Regulation and reimbursement drive demand. In many industries, consulting is discretionary. In healthcare, projects often become “must do” because rules change, audits happen, reimbursement models shift, and national or regional programs roll out.

- Outcomes matter more than slides. Buyers reward firms that can prove they reduce cost, improve throughput, improve quality measures, or help clients pass regulatory gates - because those outcomes tie directly to dollars and risk.

- Trust and access are real assets. Long-standing relationships with payers, providers, government agencies, and key vendors can create a moat. But buyers will stress-test whether that trust sits in the firm or in the founder’s personal network.

Main business models inside healthcare consulting

Most privately held healthcare consulting businesses fall into a handful of “valuation profiles”:

- Project-led advisory (strategy, ops improvement, revenue cycle, digital transformation, regulatory programs)

- Managed services / BPO-like delivery (ongoing operations, reporting, compliance monitoring, program management)

- Specialized regulatory and market access (submissions, audits, validation, evidence packages, payer/provider contracting)

- Data and workflow enablement (HIE work, interoperability, analytics implementation, care management operations)

- Hybrid consulting + “accelerators” (templates, toolkits, automation scripts, lightweight software, dashboards)

Unique valuation considerations

- Recurring vs one-off revenue matters more than “brand.” A consulting firm with the same revenue can sell for very different prices depending on how predictable that revenue is.

- Delivery model quality becomes a valuation driver. Buyers want to know if results require elite, expensive people - or if you can deliver consistently with a repeatable method.

- Healthcare compliance creates both risk and moat. If you’re embedded in regulated workflows (payer/provider programs, national systems, regulated data flows), buyers can pay up - but they will also diligence security, privacy, and contractual liabilities aggressively.

Key risk factors buyers will always check

- Customer concentration and contract structure (Do you depend on 1-2 clients? Do you have multi-year MSAs or only SOWs?)

- Reliance on the founder / a few rainmakers (Would revenue drop if 1-2 people left?)

- Proof of impact (Can you tie your work to measurable outcomes or just “deliverables”?)

- Data handling and compliance posture (HIPAA/GDPR-like obligations, security controls, incident history, subcontractor risk)

- Margin resilience (Can margins hold if utilization dips or if wages rise?)

2. What Buyers Look For in a Healthcare Consulting Business

Buyers generally fall into two camps:

- Strategic buyers (healthtech platforms, payers, provider services groups, CROs, IT services firms expanding healthcare)

- Private equity (platform and add-on buyers who want predictable cash flow and a clear path to scale)

Both types care about fundamentals - but in healthcare consulting, a few sector-specific items often dominate the decision.

The “core” buyer checklist (in plain English)

- Predictable revenue: multi-year contracts, renewals, retainer-like structures, recurring managed services.

- Clear positioning: a defined niche where you are “known for something” (not “we do everything for everyone”).

- Proof you create economic value: reduced denials, faster throughput, better quality metrics, audit readiness, improved medical-loss ratios, etc. (This is a premium driver in the data - buyers pay up when you reduce care friction and improve payer-provider economics.)

- A delivery engine: repeatable playbooks, templates, QA, training, project governance, and a bench that does not collapse when one person is out.

- Margin profile that makes sense for services: buyers accept services margins, but they dislike volatility and surprise write-offs.

Industry-specific nuances buyers care about

- Embeddedness in regulated workflows: When your work becomes part of how a payer/provider operates (or how a government program runs), you become harder to replace. The sources highlight premiums for assets embedded in national/regional systems and regulated workflows.

- “Proximity to data” without owning software: Even if you do not sell software, buyers like consulting firms that sit close to healthcare data flows and can enable analytics, reporting, and interoperability - because that can be cross-sold into a broader platform strategy.

- Operational stickiness: Managed services with SLAs, clear ROI, and renewal behavior are valued differently than pure project work. The sources explicitly flag managed services and measurable ROI as a premium driver.

- Security and compliance credibility: In healthcare, one weak link in subcontractors or data handling can kill enthusiasm late in diligence.

How private equity thinks about it (without the jargon)

Private equity is usually asking:

- “What multiple am I paying today, and can I sell it later at the same or higher multiple?” If your revenue is lumpy and founder-driven, PE fears they will have to sell it later as a lower-quality asset.

- “Who will buy this in 3-7 years?” The best answer is: a larger healthcare services platform, a payer/provider services buyer, or a scaled tech-enabled healthcare operations player - not “maybe someone will like it.”

- “What levers can we pull?”

- Turn one-off projects into recurring programs

- Raise prices where outcomes are proven

- Cross-sell adjacent offerings into existing clients

- Add bolt-on firms to expand capability or geography

- Improve utilization and delivery efficiency without hurting quality

If you want PE interest, you need to show a believable path from “services firm” to “services platform with recurring engines.”

3. Deep Dive: The Biggest Valuation Nuance in Healthcare Consulting - Repeatability and Embeddedness

Here’s the question that quietly drives a large part of valuation dispersion in this sector:

Are you selling “expert hours,” or are you selling a repeatable operating capability that becomes part of the client’s workflow?

Two firms can both be “healthcare consulting,” both have USD 10m revenue, and still land in very different valuation outcomes because buyers are buying risk-adjusted future cash flow, not your past projects.

How this shows up in the data

In the sources, deals and premiums cluster around businesses that are:

- Plugged into regulated data and workflows, where acquirers can integrate them into existing payer/provider platforms and monetize at scale (a premium driver explicitly called out).

- Embedded in national or system-level pathways, where regulatory approvals and ecosystem embedding create a moat (another explicit premium driver).

- Able to prove they reduce care friction and improve economics, not just complete tasks (explicit premium driver).

Even when the asset is not “software,” the market rewards stickiness - especially when it looks like ongoing operations rather than episodic consulting.

Why buyers care (in simple terms)

- Repeatability lowers delivery risk. If your success relies on a few brilliant people improvising, buyers see fragility.

- Embeddedness lowers churn risk. If you sit in the operational “spine” of a program (SLAs, reporting cadence, compliance cycles), replacement is painful.

- It creates cross-sell value. Strategics pay more when they can plug your capability into a broader platform (data + workflow + services).

How to move from lower-value to higher-value

You do not need to become a software company in 12 months. You do need to package your services so buyers perceive you as a durable operating asset.

A simple way to think about it:

Practical moves that help (and come up again in Sections 6, 9, and 11):

- Convert your best engagements into managed services with SLAs.

- Build repeatable playbooks and QA so delivery is consistent.

- Track outcomes in a way a buyer can diligence (before/after metrics, benchmarks, case studies).

4. What Healthcare Consulting Businesses Sell For - and What Public Markets Show

This section is intentionally data-first. The numbers below are not a price tag for your company - they are reference bands. Your actual multiple moves based on predictability, margin quality, concentration, and how “embedded” you are.

4.1 Private Market Deals (Similar Acquisitions)

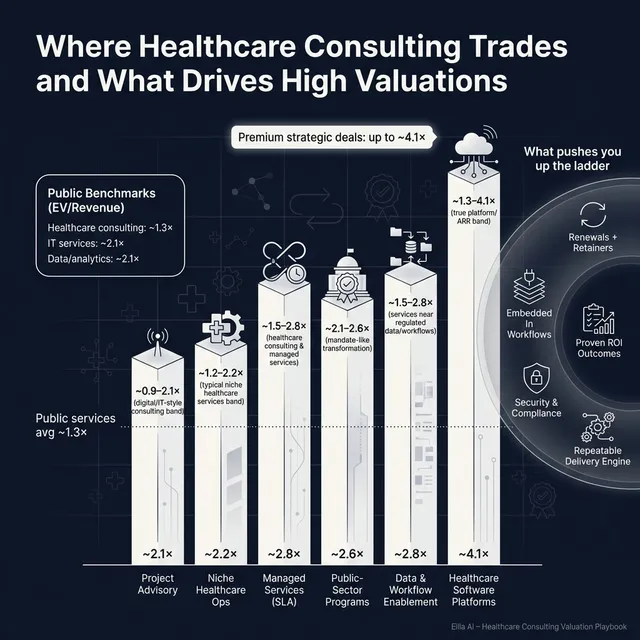

Across the precedent transactions provided, the overall average precedent EV/Revenue is ~2.7x, with meaningful variation by segment. For healthcare-focused consulting and managed services (non-software), the group averages are around ~2.2x EV/Revenue (median ~1.9x). EV/EBITDA averages are higher but skewed by mix and outliers (average ~29.9x, median ~12.1x), which is why many founders find revenue multiples easier to anchor on when EBITDA is volatile.

A practical takeaway: quality healthcare consulting assets that look “platform-like” often trade closer to ~1.5x-2.6x revenue, while more commodity or less predictable services can drift toward the low end of public services trading bands.

Illustrative private deal bands from the provided precedent groups:

These are illustrative ranges pulled from the data you supplied, not guarantees.

4.2 Public Companies

Public markets are a reference point for private valuation, but they are not a direct translation. Public multiples reflect scale, liquidity, and investor sentiment.

From the public multiples table you provided (as of mid/end 2025 in your instructions):

- Healthcare-focused consulting & federal/public health services trade around ~1.3x EV/Revenue on average (median ~1.4x) and ~9.8x EV/EBITDA on average (median ~9.5x).

- General IT services & digital transformation trade around ~2.1x EV/Revenue on average (but median ~1.2x) and ~13.6x EV/EBITDA on average (median ~9.0x).

- Healthcare data/analytics platforms trade higher at ~2.1x EV/Revenue (avg/median ~2.1x) and ~12.0x EV/EBITDA (avg ~12.0x, median ~11.0x), reflecting more “asset-like” economics.

A clean way to view it:

How to use public multiples correctly

- Use public multiples as a reference band, not a direct “valuation calculator.”

- Private companies are usually adjusted down for smaller scale, customer concentration, weaker predictability, and founder dependency.

- Private companies can sometimes be adjusted up if they are scarce strategic assets (deeply embedded in regulated workflows, clear ROI, defensible niche) - which is exactly what the premium driver data points to.

5. What Drives High Valuations (Premium Valuation Drivers)

The market does not pay premium multiples because you are “in healthcare.” It pays premiums when your business feels hard to replace, predictable, and strategically useful to a buyer.

Below are the premium drivers in your sources, grouped into practical themes, with added sector context.

5.1 Strategic fit in regulated data and workflows

The clearest premium pattern in the sources is when the buyer can plug the asset into an existing payer/provider platform, reduce care friction, and monetize data/workflows at scale.

What this means for a consulting business:

- Buyers pay more when you have repeatable integration patterns with payers/providers, HIEs, and regulated programs.

- If your work consistently touches “regulated workflows” (interoperability, reporting mandates, compliance cycles), it feels less optional.

Practical examples:

- You have a repeatable approach to interoperability or HIE operations that multiple systems use.

- Your team is known for making “regulatory + workflow” programs actually work end-to-end.

5.2 National/system embedding as a moat

Your sources highlight “national system embedding and regulatory approvals as moat” as a premium driver. In plain English: if you are integral to a major system’s care pathways, you become difficult to displace.

How consulting can emulate this (without owning a national platform):

- Become the default implementation partner for a recurring compliance or reporting program.

- Own reference architectures, compliance accelerators, or standardized operating models that clients treat like a de facto standard.

5.3 Measured outcomes - reducing care friction and improving economics

Premium buyers want proof that you improve throughput, adherence, gaps in care closure, audit outcomes, or payer/provider economics. The sources make this explicit: premiums hinge on provable improvements, and value can be captured through performance-based or ongoing operational contracts.

Practical examples:

- You can quantify denial reduction, faster scheduling, lower leakage, improved quality scores, or audit pass rates.

- You moved from “project completed” to “metric moved.”

5.4 Managed services with measurable ROI (stickiness)

The premium driver list calls out “embedded BPO/managed services with measurable ROI.” Even when multiples in individual examples are not always sky-high, the principle matters: managed services reduce perceived risk and increase predictability.

Practical examples:

- You run ongoing reporting/compliance operations with SLAs and renewals.

- You operate a program office or analytics ops team that clients renew annually.

5.5 Margin resilience and recurring economics

The premium driver list highlights high gross margins and defensible recurring economics as supportive of premium outcomes. For consulting, the path is usually:

- Productize what you do (templates, automation, training, QA)

- Increase the recurring portion of revenue (retainers, managed services)

- Reduce delivery volatility (less rework, fewer write-offs)

5.6 Scale and diversification (but niche dominance can substitute)

The data includes examples where large diversified platforms command strong strategic value because cross-sell and risk dispersion are real. But small firms can still win premium outcomes if they dominate a regulated niche with repeatable programs and reference clients.

“Always matters” premium basics (even if boring)

- Clean financials and clear revenue recognition

- Diversified customer base and strong retention

- A leadership bench that is not founder-only

- Clear KPIs: pipeline, backlog, utilization, gross margin by service line, renewal rates if applicable

6. Discount Drivers (What Lowers Multiples)

Discounts usually come from one simple fear: future cash flow is less certain than it looks. Here are the most common issues that push you toward the low end of ranges.

6.1 Revenue fragility

- High customer concentration (one client drives too much revenue)

- Lumpy project mix with limited backlog or renewals

- Short-term SOW cycles where work must be re-won every quarter

How to mitigate: build multi-year MSAs, convert repeat work into managed services, and document backlog and renewal behavior.

6.2 Founder dependence and key-person risk

If the founder is the primary seller, relationship owner, and delivery lead, buyers apply a discount or require earnouts because they fear the business will shrink after close.

Mitigation: formalize sales process, distribute relationships, build a delivery leadership layer, and show wins sourced by others.

6.3 Delivery and margin volatility

- Unpredictable utilization

- Frequent write-offs

- Weak scoping discipline

- Margin swings by quarter that cannot be explained

Mitigation: tighter scoping, standard templates, better project governance, and service-line margin reporting.

6.4 Compliance and data risk

Healthcare diligence is unforgiving. Weak security practices, unclear subcontractor controls, or messy data-handling processes can slow or kill a deal.

Mitigation: tighten policies, document controls, and show evidence (training logs, access controls, incident response).

6.5 “Commodity positioning”

If your pitch sounds like “we do healthcare consulting” rather than “we solve X regulated problem with a repeatable method,” buyers treat you like a staffing firm with a healthcare wrapper.

Mitigation: sharpen positioning and prove outcomes.

7. Valuation Example: A Healthcare Consulting Company (Fictional)

This example is designed to show the logic - not predict your price.

The fictional company

HarborBridge Health Consulting (fictional)

- USD 10.0m last-twelve-month revenue (fictional)

- 40 people

- Mix: 65% payer/provider operations + compliance programs, 35% project advisory

- 30% of revenue on multi-year managed services with SLAs; remainder project-based

- Solid delivery playbooks; still somewhat founder-led in sales

- No standalone SaaS product, but has internal accelerators and templates

Step 1: Build a defensible base multiple range (using the source logic)

From your provided valuation logic for a niche healthcare consulting/services firm at USD 10m revenue, a defensible range was ~1.2x-2.2x EV/Revenue (implying USD 12-22m EV). That range was built by triangulating:

- Public healthcare consulting services trading bands roughly ~0.7x-1.6x revenue, with services clusters often around ~1.0x-1.6x

- Private healthcare consulting/managed services transactions that cluster higher, roughly ~1.5x-2.6x for higher quality assets

- A cap on upside when there is no true software/ARR (so you do not borrow SaaS multiples)

This is a good “base-case logic” for many sub-USD 20m revenue healthcare consultancies.

Step 2: Apply scenarios to HarborBridge (USD 10m revenue)

How to interpret these:

- Discounted case (1.0x-1.4x): This is what happens if revenue is mostly one-off projects, client concentration is high, and the founder is essential to winning and delivering work.

- Base case (1.2x-2.2x): Matches the source logic - a niche healthcare services firm with credible differentiation but limited recurring “operating asset” features.

- Premium-leaning case (2.0x-2.6x): This becomes realistic when you can prove a meaningful share of revenue is multi-year, renewal-driven managed services, and your offering is embedded in regulated workflows with measurable ROI (which aligns with the premium drivers in the source set).

Step 3: What this means for you

Two healthcare consulting firms with the same USD 10m revenue can be worth 2x+ apart because buyers are not paying for your revenue - they are paying for how durable and transferable that revenue is.

This is why “make the number bigger” is not the only path to value. Often, the fastest multiple lift comes from:

- increasing predictability (recurring/managed services),

- reducing key-person risk,

- and documenting outcomes.

Disclaimer: this is not investment advice or a formal valuation. It’s a worked example to show how buyers think.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as a quick, honest tool to estimate whether you are closer to the low, middle, or high end of typical healthcare consulting valuation bands.

Score each factor 0 / 1 / 2:

- 0 = weak or not present

- 1 = partially true

- 2 = clearly true and provable

How to interpret your score

- High band: Most high-impact factors are 2s. You are closer to “platform-like services,” which tends to push you toward the upper end of private ranges.

- Middle band: Mixed 1s and 2s. You can sell, but valuation is sensitive to deal process quality and story.

- Lower band: Several 0s on high-impact factors. You may still transact, but improving predictability and reducing key-person risk often pays off more than chasing growth at any cost.

9. Common Mistakes That Could Reduce Valuation

9.1 Rushing the sale

If you start a process before your numbers and story are ready, you force buyers to assume risk. In healthcare, assumed risk becomes discounts, holdbacks, and earnouts.

9.2 Hiding problems

Issues will surface in diligence. When buyers discover surprises, they do not just re-price - they lose trust. Trust loss kills deals.

9.3 Weak financial records (fixable in 6-12 months)

Common pain points:

- messy project accounting

- unclear revenue recognition

- no service-line margin view

- inconsistent utilization reporting

These are not “finance problems.” They are buyer-confidence problems.

9.4 No structured, competitive sale process

A structured, competitive process (with an advisor) typically produces meaningfully higher purchase prices - often cited around ~25% uplift because it creates real competition and better positioning. If you run a quiet, single-buyer process, you usually get “that buyer’s price,” not “the market price.”

9.5 Telling buyers what price you want (too early)

If you say, “I’m looking for USD 10m,” you just anchored the entire process. Buyers will cluster offers around that number (USD 10.1m, USD 10.2m) instead of telling you what they would actually pay in a competitive environment. Let the market speak first.

9.6 Healthcare-specific mistake: selling “activity” instead of “impact”

In this sector, buyers pay for outcomes and embeddedness. If your materials highlight work performed rather than value created (audit risk reduced, revenue leakage fixed, throughput improved), you look commodity.

9.7 Healthcare-specific mistake: under-preparing for data/compliance diligence

Even consulting firms get hit with deep questions on data handling, subcontractors, and security controls. If you cannot answer cleanly, deals slow down or price down.

10. What Healthcare Consulting Founders Can Do in 6-12 Months to Increase Valuation

This is the practical “multiple lift” plan. Think in three tracks: improve predictability, reduce risk, and sharpen the story.

10.1 Increase revenue predictability (highest ROI)

- Turn repeat project work into annual programs with clear scope and renewal.

- Introduce managed services tiers with SLAs (even if small at first).

- Build a renewal cadence: QBRs, KPI reporting, structured upsell paths.

- Track and report backlog and “contracted future revenue” like a metric you manage weekly.

Why it matters: this directly aligns with the premium patterns around embedded managed services and measurable ROI.

10.2 Productize delivery to lift margins and reduce volatility

- Create standard playbooks, templates, and QA gates for your top 2-3 offerings.

- Build a training path so new hires deliver consistently by month 2-3, not month 12.

- Fix scoping: define what is in/out, how change orders work, and who approves scope creep.

Why it matters: premium outcomes correlate with margin resilience and defensible recurring economics.

10.3 Reduce founder dependence (make the business transferable)

- Assign relationship owners beyond the founder for every top account.

- Build a simple, repeatable sales process: ICP, pipeline stages, win/loss, proposal templates.

- Put a “second line” in place for delivery leadership.

Buyers are buying the future. They want to know it survives leadership transition.

10.4 Prove outcomes in buyer-friendly language

- Pick 5-8 case studies and quantify outcomes:

- cost avoided, denials reduced, audit risk reduced, throughput improved, time-to-compliance shortened

- Standardize a before/after ROI narrative.

- Where appropriate, pilot performance-based elements (even small) to demonstrate confidence.

This ties directly to the premium driver around reducing care friction and improving economics.

10.5 De-risk compliance and security (do not leave this to diligence)

- Document data flows, access controls, subcontractor governance, incident response.

- Tighten contractual language and ensure you can explain obligations clearly.

- Prepare a “diligence-ready” folder with policies, evidence, and key contracts.

11. How an AI-Native M&A Advisor Helps (Soft CTA)

Selling a healthcare consulting business is not only about finding “a buyer.” It’s about finding the right set of buyers who value your niche, running a process that creates competition, and presenting your business in a way that reduces perceived risk.

An AI-native M&A advisor helps in three practical ways:

First, higher valuations through broader buyer reach. AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, synergy fit, financial capacity, and other signals. More relevant buyers means more competition, stronger offers, and more options if one buyer drops.

Second, initial offers in under 6 weeks. AI-driven buyer matching and outreach, faster creation of process materials, and structured support through diligence can compress timelines compared to manual-only processes - without sacrificing buyer quality.

Third, expert advisory enhanced by AI. You still need experienced human advisors to run the process, protect leverage, and frame the story credibly. The AI layer improves speed and coverage, while experts ensure the positioning, materials, and negotiation speak the buyer’s language - delivering Wall Street-grade advisory quality without traditional bulge bracket costs.

If you’d like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.