The Complete Valuation Playbook for Industrial Machinery Businesses

A data-driven guide to how industrial machinery businesses are valued and what drives high multiples.

If you own an industrial machinery business and are thinking about selling in the next 1-12 months, valuation matters now more than ever. The market is still active, but buyers have become more selective. They are paying up for businesses with a strong installed base, recurring service revenue, niche engineering know-how, and exposure to attractive end markets like energy efficiency, technical gases, cold-chain infrastructure, and selected energy-transition applications.

This guide is built to help you understand what industrial machinery businesses actually sell for, what drives higher and lower valuation multiples, and what you can still improve before going to market. The numbers here are based on the transaction and public-market data you provided, combined with practical M&A logic from this sector.

1. What Makes Industrial Machinery Businesses Unique

Industrial machinery is not one single business model. The sector includes compressed-air and flow equipment makers, refrigeration and cold-chain equipment suppliers, power and energy equipment providers, industrial gas and cryogenic systems businesses, and service-led installers, integrators, and aftermarket support companies. Two companies can both call themselves "industrial machinery" and still deserve very different valuations.

That is because buyers do not just look at revenue size. They look at what kind of revenue you have. A business that mainly resells equipment on one-off projects usually gets valued very differently from a business with a sticky installed base, recurring parts and service revenue, proprietary engineered systems, and strong margins.

Another reason this sector is unique is that reliability matters as much as growth. In software, buyers often focus heavily on growth. In industrial machinery, they also care about whether your products are mission-critical, whether downtime is expensive for the customer, whether your equipment requires ongoing service, and whether the customer is likely to keep buying parts, upgrades, or maintenance.

Buyers will also always check a few sector-specific risks:

- customer concentration, especially if a few OEMs, EPCs, distributors, or plant operators drive most sales

- project lumpiness and long sales cycles

- exposure to cyclical industries such as construction, general manufacturing, or oil and gas

- warranty risk, field-failure risk, and service quality

- dependence on a founder for sales, technical design, or customer relationships

- supply-chain risk, including key components, castings, motors, electronics, and long lead times

- margin quality, especially if revenue looks healthy but installation, customization, or service delivery eats the profit

In plain English: industrial machinery valuation is not just about how much you sell. It is about how defensible, repeatable, and profitable those sales are.

2. What Buyers Look For in an Industrial Machinery Business

Most buyers start with a few obvious questions. How big is the business? Is revenue growing? Are margins healthy? Is cash conversion solid? Is the customer base diversified? Those basics matter, but in industrial machinery they are only the starting point.

The next layer is installed-base quality. Buyers love businesses where equipment sold in prior years creates future revenue through spare parts, service contracts, maintenance, retrofits, monitoring, compliance checks, consumables, and efficiency upgrades. That kind of revenue is usually more predictable than new equipment sales and often carries better margins.

They also care about commercial positioning. Are you competing mostly on price, or do you win because your product solves a difficult engineering problem, lowers downtime, improves energy efficiency, handles safety-critical applications, or meets demanding customer specifications? The more your product is hard to replace, the more leverage you have in valuation.

End-market exposure matters too. Buyers will look at where demand comes from. Exposure to cold-chain, food processing, technical gases, specialty process industries, regulated environments, and selected energy-transition themes often gets more attention than pure exposure to general industrial capex cycles. A business tied to customers' "must-have" operating needs usually gets viewed more favorably than one tied mostly to discretionary expansion projects.

What private equity buyers are thinking

Private equity buyers usually ask three simple questions.

First, what price are they paying today, and what price might they sell for later? If they buy at a full multiple, they need a believable plan to grow earnings enough to still make a good return.

Second, who could buy the business from them in 3-7 years? That might be a larger strategic buyer, a larger private equity firm, or occasionally a public listing, though that is less common for smaller industrial machinery businesses.

Third, what levers can they pull after buying? In this sector, that often means:

- raising prices where the product is mission-critical

- growing aftermarket and service revenue

- improving sourcing and operations

- adding bolt-on acquisitions

- cross-selling into adjacent product lines or geographies

- professionalizing sales, reporting, and management depth

So when a private equity buyer studies your business, they are not only valuing what you are today. They are valuing what they can turn you into.

3. Deep Dive: Why Aftermarket and Service Mix Can Change Valuation So Much

In industrial machinery, one of the biggest valuation questions is this: are you mostly selling equipment once, or are you building a machine-plus-lifecycle revenue model?

This matters because the data strongly suggests that service-led and integrator-type businesses tend to trade at much lower revenue multiples when they are project-heavy, local, and less differentiated. In the precedent transaction data, industrial services and systems integrators show a median EV/Revenue of about 0.6x. Meanwhile, specialty engineered businesses with stronger margins, proprietary know-how, or mission-critical products can attract meaningfully better outcomes, especially on EBITDA multiples.

Buyers care because aftermarket revenue is usually stickier than original equipment sales. Once your equipment is installed, the customer often prefers the same supplier for service, replacement parts, upgrades, controls integration, and troubleshooting. That lowers customer churn, smooths revenue, and makes the business less dependent on landing the next big project.

It also improves earnings quality. A business with modest top-line growth but strong gross margins on service, controls, retrofits, remote monitoring, and parts may be worth more than a faster-growing business that mainly pushes low-margin hardware through one-off projects. That is why buyers often focus hard on service attachment rate, installed base, spare-parts revenue, warranty history, and contract renewal behavior.

If your business looks more like the lower-value profile today, you can still move it in the right direction before a sale.

The practical goal is not to reinvent the company in six months. It is to prove that your customer relationships do not end when the machine ships.

4. What Industrial Machinery Businesses Sell For - and What Public Markets Show

The first thing to understand is that there is no single "industrial machinery multiple." The data shows a wide spread depending on whether a business is a scaled OEM, a specialty gas or cryogenic platform, a refrigeration or cold-chain equipment maker, or a service-heavy integrator.

The second thing to understand is that public-company multiples are useful reference points, but private companies usually trade below them unless there is something special about the asset. Smaller size, customer concentration, lower margins, less diversified channels, and founder dependence usually push private valuations down. Scarcity, proprietary know-how, and strong strategic fit can push them up.

4.1 Private Market Deals (Similar Acquisitions)

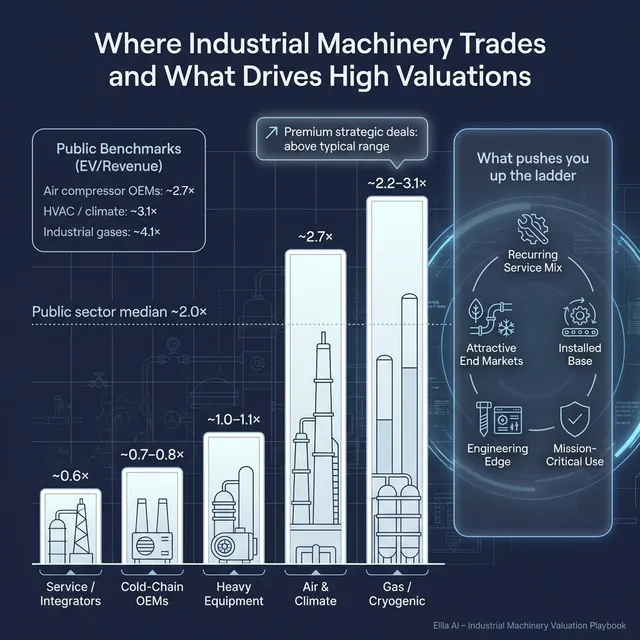

In the private deal data, the clearest pattern is that standard industrial equipment, refrigeration, and integration businesses often transact around modest revenue multiples. Industrial refrigeration and cold-chain equipment OEM deals average about 0.8x EV/Revenue, with a median around 0.7x. Heavy industrial equipment OEM deals sit around 1.0x to 1.1x EV/Revenue. Industrial gas, cryogenic, and hydrogen systems deals are higher on average at about 3.1x EV/Revenue, but that is pulled up by a few premium growth or technology-led outcomes.

That spread matters. It tells you that buyers are not rewarding "industrial" exposure by itself. They pay more when the target has real technology differentiation, specialty applications, attractive end markets, or unusually strong margin structure. Otherwise, the market often values these businesses much more conservatively than founders expect.

A founder should read those ranges as illustrative, not automatic. The same USD 10m revenue business could be worth very different amounts depending on whether it is mostly resale and installation work, or a sticky specialty platform with strong margins and clear strategic value.

4.2 Public Companies

Public markets, as of mid to late 2025, show a similar pattern. Scaled, high-quality industrial platforms with better margins, broader distribution, and stronger aftermarket economics trade at higher multiples than smaller or more commoditized players. Across the whole public set, the average EV/Revenue is about 3.4x and the median is about 2.0x. Average EV/EBITDA is about 19.4x, with a median of about 14.5x.

But the more useful way to look at public markets is by subgroup. Industrial air compressor OEMs average about 2.7x revenue and 18.6x EBITDA. HVAC, climate, and cold-chain solution providers average about 3.1x revenue and 23.1x EBITDA. Industrial gases producers and distributors average about 4.1x revenue and 17.2x EBITDA. Engineering contractors and system integrators trade much lower on revenue, at around 0.8x on average.

The right way to use public multiples is as a reference band, not a direct price tag for your company. If you are smaller, less diversified, or less profitable than public peers, buyers will usually adjust down. If you have a scarce capability, strong installed base, high service attachment, and strategic relevance, buyers may pay above where a plain-vanilla private comp would suggest.

In other words, public comps help frame the ceiling and the direction of travel. They do not tell you your exact sale price.

5. What Drives High Valuations (Premium Valuation Drivers)

The data points to a handful of repeat patterns behind premium outcomes. These are the things that move a business toward the top end of the range.

5.1 Exposure to attractive long-term end markets

Buyers pay more when they believe your market will grow faster than the average industrial market for years, not just quarters. In the data, the clearest examples come from hydrogen, specialty gas handling, carbon capture, energy efficiency, clean mobility, and selected cold-chain or thermal-management themes.

Why buyers care: they are not just buying current earnings. They are buying future demand.

What this looks like in practice:

- your equipment supports hydrogen, cryogenic, technical gas, or decarbonization applications

- your products help customers lower energy use or meet sustainability targets

- you sell into markets with regulatory or infrastructure tailwinds

The key is credibility. Buyers pay for real exposure, not just ESG language in a slide deck.

5.2 Defensible engineering or technology differentiation

The strongest premiums in your data show up where the target had hard-to-replicate know-how - patented purification, hydrogen process technology, gas analysis, specialty cryogenic systems, or highly engineered solutions.

Why buyers care: if your product is hard to copy, the customer is less likely to switch on price alone.

Examples founders can relate to:

- patented or proprietary subsystem designs

- specialized controls, monitoring, or safety features

- an engineered solution that solves a difficult application better than generalist competitors

- a product that is deeply embedded in the customer's process or compliance environment

Remote monitoring and analytics can help, but only if they clearly improve retention, service revenue, uptime, or pricing power. A dashboard by itself is not a moat.

5.3 High-margin specialty mix

Some businesses do not look expensive on revenue, but they still command strong EBITDA multiples because the earnings are good. The data shows better outcomes where the target had a specialty mix, better gross margins, and solid EBITDA conversion.

Why buyers care: quality of earnings matters more than headline revenue.

Examples:

- high-margin parts and service tied to a large installed base

- specialty engineered modules rather than commodity hardware

- instrumentation, analysis, controls, or safety-critical components with pricing power

- recurring maintenance and retrofit work that is less competitive than new-build projects

5.4 Strong strategic fit for a larger consolidator

A recurring theme in the data is that industrial buyers pay better prices when the target fills a product gap, adds a new capability, extends geography, or creates cross-sell opportunities. That is classic strategic value.

Why buyers care: the business may be worth more inside their platform than it is on a standalone basis.

What that can mean for you:

- your product line plugs into a larger OEM's installed base

- your service team helps a buyer expand lifecycle revenue

- your capability opens a new customer segment or end market

- your engineering know-how shortens the buyer's product roadmap

This is why good sale processes matter. The "right" buyer may value your business very differently from the "first" buyer.

5.5 Recurring and visible revenue

This is not unique to industrial machinery, but it matters a lot here. Buyers pay more when they can see next year's revenue before the year starts.

Why buyers care: predictability lowers risk.

Examples:

- service contracts

- inspection and maintenance agreements

- consumables and replacement parts

- monitoring subscriptions tied to uptime or performance

- framework agreements with repeat customers

5.6 Clean operating discipline

Even a strong industrial business can lose value if the numbers are messy. Clean financial statements, clear margin reporting by product and service line, usable KPIs, and a management team that can run the business without the founder all increase buyer confidence.

Why buyers care: trust lowers deal friction. Less friction usually means better price and better terms.

6. Discount Drivers (What Lowers Multiples)

The low end of the valuation range is usually not caused by one dramatic flaw. More often, it comes from a stack of smaller risks that make buyers cautious.

The first major discount driver is a project-heavy revenue mix with weak repeatability. If too much revenue comes from one-off equipment sales, custom jobs, or irregular installations, buyers worry about future revenue visibility. That often pushes them toward lower revenue multiples.

The second is low earnings quality. A business can have decent revenue but still attract a lower valuation if gross margins are inconsistent, warranty costs are unpredictable, installation overruns are common, or service work is not priced properly. Buyers are quick to discount revenue that does not convert into durable profit.

The third is concentration risk. If one customer, one distributor, one end market, or one founder relationship drives too much of the business, buyers see fragility. In industrial machinery, this is especially common where the founder personally handles large accounts, technical problem-solving, and supplier relationships.

The fourth is commoditization. If the buyer concludes that your products are easy to substitute and that customers mainly choose on price, it becomes much harder to argue for a premium multiple. That is especially true for plain equipment distribution, low-spec integration work, or undifferentiated fabrication.

A few other common discount drivers:

- weak backlog quality or poor forecasting

- long lead times with limited pricing protection

- customer claims, product failures, or unresolved warranty issues

- margin leakage from too much customization

- no clear installed-base data

- poor documentation of service contracts or renewal history

- overdependence on cyclical sectors

- working-capital volatility, especially large inventory swings

None of these issues automatically kill a deal. But each one gives buyers a reason to pay less, add earn-outs, or retrade late in the process.

7. Valuation Example: A Fictional Industrial Machinery Company

To make the logic practical, here is a worked example using a fictional company. The company and the revenue figure are fictional, and the valuation range below is illustrative only. It is not investment advice or a formal valuation.

Let us call the company NorthPeak Process Systems. NorthPeak sells, installs, and services industrial compressors, gas-handling skids, and refrigeration support systems for manufacturing and food-processing customers. It also earns some recurring revenue from maintenance contracts, spare parts, and remote equipment monitoring, but it is still mainly an equipment-plus-service business, not a software company.

Assume NorthPeak has:

- USD 10.0m revenue

- USD 0.65m EBITDA

- 41% gross margin

- 6.5% EBITDA margin

- 35% of revenue from service, parts, and maintenance

- no major customer concentration, but still founder-led

Step 1: Choose the right comp set

The most relevant private reference points are not the large global OEMs. They are smaller industrial services, systems integrators, and equipment-plus-service businesses. In the source logic, that is why the most useful revenue range for a small, mature industrial machinery company was around 0.55x-0.75x revenue, with an EBITDA cross-check around 8.0x-12.0x.

That makes sense. NorthPeak is too small, too local, and too service-heavy to justify a public OEM-style 3x-5x revenue multiple. But it is also better than a distressed low-margin project shop because it has positive EBITDA, decent gross margin, and some recurring revenue.

Step 2: Apply the logic

Using the same framework, the math looks like this:

- Revenue method: 0.55x-0.75x on USD 10.0m revenue = USD 5.5m-7.5m

- EBITDA method: 8.0x-12.0x on USD 0.65m EBITDA = USD 5.2m-7.8m

Those two approaches point to a sensible core range of about USD 5.5m-7.5m.

Then you pressure-test the range.

If NorthPeak has stronger service attachment, better installed-base data, less founder dependence, and more specialty engineered content than first appears, the business could push above the core range. If the business is more project-heavy, has lumpy sales, or depends too much on equipment resale, it could fall below the core range.

Step 3: What founders should take from this

Two industrial machinery businesses with the same USD 10m revenue can be worth very different amounts. One may be worth USD 4m-5m because it is mostly low-margin project work with weak repeatability. Another may be worth USD 8m-11m because it has a sticky installed base, strong service economics, niche know-how, and real strategic relevance.

That is the real lesson. Revenue gets you into the conversation. Revenue quality determines where the conversation ends.

8. Where Your Business Might Fit (Self-Assessment Framework)

Here is a simple way to score your business. Give yourself a 0, 1, or 2 on each factor.

- 0 = weak

- 1 = fair

- 2 = strong

The point is not to flatter yourself. The point is to see where improvements could move valuation most.

A more detailed version looks like this:

How to interpret the score

- 14-18 points: you are closer to the premium end of the private market range

- 9-13 points: fair market profile, with room to improve before sale

- 0-8 points: likely lower-end valuation today unless a strategic buyer sees special value

Use the framework honestly. Most businesses are not weak everywhere. They are usually strong in a few areas and underprepared in a few others. That is good news, because the underprepared areas are often fixable.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often start the process before the numbers are clean, the growth story is clear, or the buyer list is thought through. That usually leads to a weaker first impression and less leverage later.

Another major mistake is hiding problems. If there are margin issues, customer disputes, warranty problems, or concentration risk, buyers will usually find them in diligence. When problems surface late, buyers do not just reduce price. They lose trust. And lost trust is expensive.

Weak financial records are another common issue. Many industrial machinery businesses can improve valuation simply by better separating product, service, and parts margins, cleaning up working-capital reporting, tightening revenue recognition, and showing the real economics of the installed base. If you have 6-12 months, this is often one of the highest-return areas to fix.

A lack of a structured, competitive sale process can also materially reduce value. In practice, research and deal experience both suggest that running a structured competitive process with an advisor often leads to meaningfully higher purchase prices - often cited at around 25% better than a single-buyer conversation - because it creates urgency, improves positioning, and gives buyers less room to anchor low.

A closely related mistake is telling buyers the price you want too early. If you tell the market you want USD 10m, many buyers will simply come back at USD 10.1m or USD 10.2m instead of telling you what they might really pay. That kills price discovery. A strong process is designed to let the market reveal value, not let the seller cap it.

Two sector-specific mistakes matter especially in industrial machinery. First, many founders fail to present the installed base as an asset. They talk about annual sales but not about how many machines are in the field, how many customers buy parts, what service renewal looks like, or how upgrades and retrofits create future revenue. Second, they under-document technical differentiation. If your edge lives only in the founder's head, buyers cannot value it properly.

10. What Industrial Machinery Founders Can Do in 6-12 Months to Increase Valuation

10.1 Improve the numbers buyers care about most

Start by making the economics visible. Separate equipment, service, parts, retrofit, and software or monitoring revenue. Show gross margin by line. Track EBITDA cleanly. Build monthly reporting that a buyer can follow without a long explanation.

Then focus on a few real operating wins:

- improve service pricing where you are undercharging

- reduce warranty leakage and job overruns

- tighten procurement and inventory management

- push low-margin custom work through stricter quoting rules

The goal is not financial engineering. It is showing that the business converts revenue into durable profit.

10.2 Increase recurring and visible revenue

You may not be able to change your whole model in a year, but you can improve revenue quality.

Practical moves:

- convert break-fix customers into service-contract customers

- package preventive maintenance into new equipment sales

- create standard spare-parts programs

- identify installed-base upgrade campaigns

- bundle monitoring or uptime services into annual agreements

Even modest progress here can change how buyers think about your business.

10.3 Reduce concentration and founder dependence

Map your top customers, suppliers, and technical dependencies. If too much sits with you personally, start moving relationships and know-how into the team now.

Useful actions:

- introduce a second commercial contact on key accounts

- document service and quoting processes

- make technical know-how reusable, not founder-only

- build a clearer sales pipeline and CRM discipline

A buyer pays more when the business can stand on its own.

10.4 Sharpen the strategic story

Industrial buyers do not just buy numbers. They buy narratives they believe.

Your story should answer:

- why customers choose you

- why they stay

- why margins are defendable

- which end markets are growing

- how your installed base creates future revenue

- which strategic buyers would care and why

If you have exposure to attractive themes like technical gases, energy efficiency, specialty process applications, cold-chain reliability, or compliance-critical systems, show it with customer evidence, not buzzwords.

10.5 Build proof of differentiation

If you have patents, certifications, proprietary designs, difficult application expertise, unusual service data, or strong field-performance records, organize them. Buyers rarely give full credit for differentiation they cannot see clearly.

Create simple evidence:

- case studies with uptime or energy savings

- renewal and repeat-purchase data

- service attachment data

- warranty and failure-rate data

- product or process certifications

- examples of hard-to-win applications you serve well

10.6 Prepare for diligence before the process starts

The best time to answer buyer questions is before they ask them. Start gathering:

- clean financials

- customer concentration analysis

- backlog and pipeline

- installed-base data

- service contract summary

- supplier concentration

- organization chart

- quality and warranty metrics

- capex and working-capital trends

Founders often think this is just admin work. It is not. Preparation affects value because it affects buyer confidence.

11. How an AI-Native M&A Advisor Helps

Selling an industrial machinery business is not just about finding one buyer. It is about finding the right buyers. An AI-native M&A advisor can expand the buyer universe to hundreds of qualified acquirers based on deal history, product adjacency, end-market overlap, synergy logic, financial capacity, and other real signals. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes even if one bidder drops out.

It also speeds up the process. With AI-driven buyer matching, faster preparation of marketing materials, better process coordination, and support during diligence, initial conversations and first offers can often be reached in under 6 weeks. That speed matters because momentum protects valuation.

The best version of this is not AI instead of human advice. It is expert human M&A advisors, enhanced by AI. You still want experienced advisors who know how to position an industrial machinery business, speak the buyer's language, run a competitive process, and manage tough negotiations. AI simply helps them do that with more market coverage, faster execution, and sharper targeting.

The result is a process that feels closer to Wall Street-grade advisory quality, but without traditional bulge-bracket costs. If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.