The Complete Valuation Playbook for Insurance Software Businesses

A practical guide to how insurance software businesses are valued and what drives high multiples.

If you run an insurance software business and may sell in the next 1-12 months, valuation is no longer something to think about only at the finish line. Buyer appetite is still real, but it is more selective than it was in peak SaaS markets. Strategic acquirers and private equity firms will still pay well for assets they believe are sticky, hard to replace, and positioned inside critical insurer workflows - but they are quicker to discount businesses that look services-heavy, hard to scale, or difficult to underwrite.

This playbook is built to help you answer three practical questions. What do insurance software businesses actually sell for? What pushes a company toward the top or bottom of the valuation range? And what can you do in the next 6-12 months to improve your odds of a stronger outcome?

1. What Makes Insurance Software Unique

Insurance software is not one single category. Buyers usually break the space into a few buckets: core systems such as policy administration, claims, and billing; claims workflow and automation tools; fraud, risk, and decisioning platforms; and distribution or ecosystem software that helps carriers, brokers, or partners sell and service policies more efficiently.

That matters because buyers do not value all of these businesses the same way. A system that sits at the center of claims or policy operations often gets more credit than a tool that is useful but easier to swap out. A recurring software platform with high gross margins also gets valued differently from a business where a large part of revenue comes from implementation projects, BPO-like delivery, or manual service work.

Insurance is also a market where switching is painful. That can be good for valuation when your product is deeply embedded, but it also means buyers spend a lot of time checking whether your software is truly part of the customer’s day-to-day operations or just sitting on the edge. They will ask how your product connects to policy, billing, claims, underwriting, document management, payments, and repair or service networks.

The sector also has risks that are more specific than in generic vertical SaaS. Buyers will check regulatory exposure, data security, claims accuracy, fraud handling, auditability, integration risk, implementation timelines, and whether your product performance holds up across lines of business. In insurance software, a flashy demo matters far less than proof that the platform works in live production for demanding customers.

2. What Buyers Look For in an Insurance Software Business

At the highest level, buyers still care about the basics: revenue scale, growth, gross margin, EBITDA, retention, and how predictable next year’s revenue looks. But in insurance software, those basics are filtered through one more question: how essential are you to the insurer’s workflow?

If you help a carrier or MGA run a mission-critical process - such as claims handling, policy changes, underwriting decisions, repair coordination, or compliance-heavy administration - buyers tend to view your revenue as more durable. If you mainly sell one-off projects, custom builds, or advisory-heavy deployments, they will usually treat the business as less scalable and lower quality, even if current revenue looks healthy.

They also look closely at the revenue model. Subscription revenue usually gets the most credit. Transaction-based revenue can also be attractive if volumes are stable and margins are strong. But buyers will pull valuation down when too much revenue depends on implementation, change requests, outsourced operations, or heavy support that grows in line with headcount.

Customer quality matters too. A founder often focuses on logos, but buyers care even more about customer behavior. Do clients renew? Expand? Add product modules? Roll the platform out across more claims teams, regions, or business lines? A small customer base with deep product usage can sometimes be more valuable than a larger customer count with weak adoption.

How private equity thinks about your business

Private equity buyers usually look at your company through two lenses at once. First, what entry valuation can they justify today? Second, who can they sell the business to in 3-7 years, and at what likely multiple?

That means they care not only about where you are now, but also about the future exit story. Can the business become a larger platform? Can it add modules, raise prices, expand internationally, or buy smaller tuck-ins? Could the next buyer be a strategic acquirer, a larger private equity fund, or in rare cases a public market story?

They will also ask what levers they can pull after closing. Common ones include price increases, cross-sell into existing customers, reducing services reliance, improving delivery efficiency, building a stronger sales engine, or consolidating adjacent products. If the only growth plan is "keep doing more of the same," private equity will be more cautious.

3. What Buyers Look For in an Insurance Software Business

Strategic buyers and financial buyers often want the same things, but for different reasons. Strategic buyers may pay more if your product fills a gap in their suite, gives them access to a new carrier segment, or deepens their position in claims, underwriting, or policy operations. Financial buyers focus more on whether the business can compound value over a hold period.

In both cases, buyers want proof that your product solves an expensive problem. In this sector, that usually means one of four things: lower loss adjustment expense, faster claims resolution, better underwriting decisions, reduced fraud, or lower operating cost inside the insurer. The clearer that value is, the easier it is for a buyer to defend a stronger price internally.

They also care about implementation reality. Insurance software can look like SaaS in the pitch deck but feel like consulting once a buyer gets into diligence. If every new customer requires major custom work, long deployment cycles, and heavy founder involvement, that will hurt valuation even if customers love the product.

A business with moderate growth but strong retention, predictable renewals, and clear workflow ownership can still attract strong interest. Buyers know insurance is a conservative market. They do not need every company to grow like a venture-backed startup. But they do need confidence that revenue is durable and the product has earned a long-term place in the stack.

What strategic buyers want

Strategic acquirers often look for one of three things: a missing module, a stronger position in a valuable workflow, or a new data asset. If your product plugs directly into claims, policy, billing, or underwriting, the strategic value can be much higher than what simple financial metrics suggest.

They also think about cross-sell. If your software can be sold into an existing carrier customer base, or if your customers could adopt the buyer’s other modules, that can increase tension in a sale process. Founders sometimes underestimate how much value can sit in that distribution overlap.

What private equity wants

Private equity tends to like insurance software when it sees recurring revenue, a clear vertical niche, and room to professionalize the business. They ask whether the current multiple can expand later, whether EBITDA can improve, and whether the company could become a platform for consolidation in a fragmented part of the market.

They also underwrite downside carefully. If growth slows, can the business still generate cash? If a large customer leaves, is the company still resilient? If the product is good but the operating model is messy, PE may still buy it - but usually at a price that reflects the cleanup work ahead.

4. Deep Dive: Are You Truly Embedded in the Insurance Workflow - or Just Adjacent?

This is one of the biggest valuation questions in the sector because it sits underneath many of the premium and discount patterns in the data. Buyers pay more for software that is deeply tied into insurer workflows, harder to remove, and clearly part of how work gets done every day.

The source data points in that direction. The strongest premium themes are tied to mission-critical workflow integration, decisioning, and software that becomes a system of record or system of execution. That includes core insurance software, claims process tooling, and platforms with credible data and decisioning value. In plain English: the closer you are to the real operating engine of the insurer, the better.

Why do buyers care so much? Because embedded software is hard to rip out. It touches claims files, policy data, workflows, SLAs, compliance steps, and customer service. Once a carrier or administrator has trained teams, integrated systems, and built internal processes around your platform, switching costs go up. That makes revenue more durable and makes the asset easier for a buyer to underwrite.

The opposite profile is a product that sounds useful but is not truly required. If customers can use your tool only occasionally, or if it depends on manual exports, side workflows, or a lot of human intervention, buyers worry that budget pressure or a broader platform vendor could push you out. The same issue shows up when revenue looks like software on the surface but depends heavily on custom delivery.

If your business looks more like the lower-value profile today, you usually do not need a complete reinvention. You need evidence of deeper workflow ownership. That can come from better integrations, more modules used by each customer, product usage data, stronger renewal history, clearer ROI proof, and less reliance on founder-led configuration.

A practical goal over the next year is not just to say your product is mission-critical, but to prove it. Show that insurers run real work through the platform, that it connects to other systems, that customers expand over time, and that results improve because of your software.

5. What Insurance Software Businesses Sell For - and What Public Markets Show

The first thing to know is that the data is not perfectly clean. Public market comps cover a wide mix of software, analytics, claims-related services, distribution platforms, and adjacent financial software. Private transaction data is thinner and more deal-specific. That means no founder should treat any single number as a price tag.

Still, the pattern is useful. Pure software and analytics businesses generally trade higher than claims-heavy service models. Embedded, workflow-critical platforms tend to earn better valuation support than businesses that depend on brokerage economics, outsourced delivery, or manual service layers.

5.1 Private Market Deals (Similar Acquisitions)

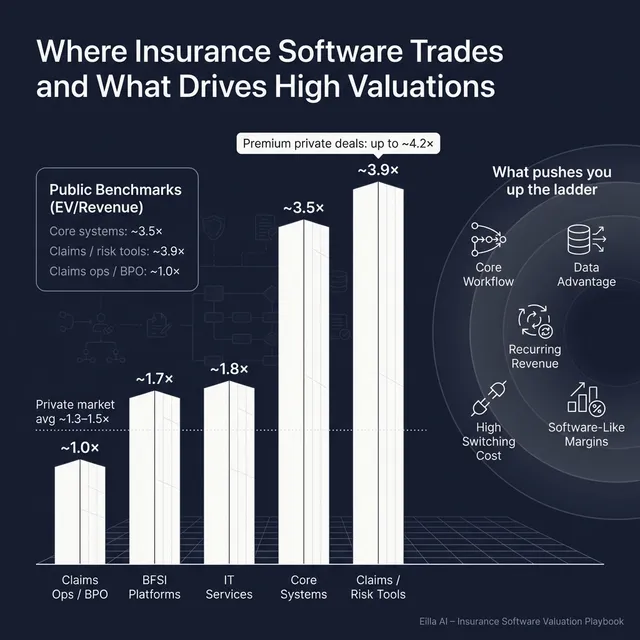

The private deal data in the source set suggests that smaller, privately held insurance software assets usually trade below headline public SaaS levels. The clearest direct benchmark for insurance core systems and claims or policy administration software vendors is around 1.3x EV/Revenue in the precedent set. Adjacent insurance comparison and marketplace businesses show around 2.1x EV/Revenue and 8.6x EV/EBITDA when they are profitable and operationally efficient.

That does not mean every insurance software company is worth 1.3x revenue. It means smaller private deals often reflect size discounts, limited competition, earnouts, customer concentration, services mix, or uncertainty around growth. In practice, better private software assets can move above those averages, but buyers usually need a reason: stronger recurring revenue, better margins, clearer workflow ownership, or real strategic fit.

These ranges are illustrative, not definitive. A high-quality private asset can trade above them, and a weaker business can fall below them.

5.2 Public Companies

Public markets set a broader reference band, and as of late 2025 the spread is wide. Insurance core systems software companies in the data trade at around 3.5x average EV/Revenue with very high average EBITDA multiples, reflecting how public investors reward scale, mission-critical software, and long-term contract durability. Insurance claims, risk, and fraud analytics platforms trade at around 3.9x average EV/Revenue and 11.7x average EV/EBITDA.

By contrast, claims management, TPA, and BPO-like models trade much lower at around 1.0x average EV/Revenue and 8.0x average EV/EBITDA. That is a useful reminder that once a business starts to look more like labor-backed delivery than software, the market values it differently. Adjacent BFSI and low-code platforms sit around 1.7x EV/Revenue and 8.7x EV/EBITDA, which provides a reasonable middle ground for software with less obvious insurance-specific scarcity.

One category needs caution: digital insurance distribution and ecosystem platforms show 12.1x average EV/Revenue, but the median is only 0.8x. That tells you the average is heavily distorted by outliers. For most founders of insurance software businesses, that is not the cleanest benchmark set.

The right way to use public multiples is as a reference band, not a direct answer. Most private companies deserve some discount to public peers because they are smaller, less liquid, more customer-concentrated, and usually have less proof around growth and management depth.

That said, public comps still matter because they shape buyer psychology. If your business looks like a mini version of a mission-critical software platform with strong retention and good gross margins, buyers can justify paying closer to the software side of the range. If it looks more like services or operational outsourcing wrapped in software, they will usually anchor much lower.

6. What Drives High Valuations (Premium Valuation Drivers)

Higher valuations usually come from a handful of themes working together. One premium factor alone rarely gets the job done. Buyers pay up when the story, the numbers, and the risk profile all point in the same direction.

1. You sit inside a mission-critical insurer workflow

This is the most important driver in the source data. Platforms tied to policy administration, claims execution, underwriting decisioning, or tightly integrated operating workflows tend to get more respect because replacing them is hard and risky.

In practical terms, buyers pay more when your software is not just a reporting layer or bolt-on utility. They want to see that claims handlers, adjusters, underwriters, or operations teams rely on your system to complete real work every day.

2. You have a real data advantage, not just an AI story

The data points also highlight a second premium theme: decisioning credibility. Buyers like platforms with proprietary data, better model performance, or measurable outcome improvements because that creates a moat that gets stronger over time.

For an insurance software founder, this means proving things like better fraud detection, better severity estimation, faster claims triage, lower leakage, or shorter cycle times. "We use AI" is not enough. Buyers pay more for "our data and models produce better outcomes that customers can measure."

3. Your revenue is recurring, sticky, and expands

Insurance software can be very sticky, which is good for valuation. Buyers like annual subscriptions, usage-based revenue with stable volumes, multi-year relationships, and evidence that customers stay and buy more over time.

A founder-friendly way to think about this is simple: buyers care about whether customers stick around, whether they add seats, modules, geographies, or business lines, and whether next year’s revenue is easier to predict than this year’s.

4. You show software-like economics, not services-like economics

Premium outcomes usually require more than good revenue. Buyers also want software-like gross margins, a delivery model that does not scale one-for-one with headcount, and signs of operating leverage over time.

This is one reason profitable marketplace or platform businesses can do well when EBITDA conversion is strong. If additional revenue drops through without needing a lot more people, buyers become more comfortable stretching on price.

5. There is a credible path to future growth

Some deals use earnouts because the buyer believes in the upside but wants proof before paying for all of it upfront. That can actually help unlock value when growth potential is real but still being demonstrated.

For founders, this matters because premium valuation is often about what the buyer believes can happen next. More carrier rollouts, broader repair-network coverage, better attach rates, stronger cross-sell, or product expansion into adjacent workflows can all support a better narrative.

6. The leadership team can carry momentum after closing

The source data also shows the importance of continuity. Buyers are more willing to pay well when they believe product leadership, customer relationships, and growth execution will survive the transaction.

That does not mean you need to stay forever. It means the buyer wants confidence that the business will not wobble the moment the deal closes. A strong second layer of management and a realistic transition plan can matter more than founders expect.

7. The company is easy to diligence

This is less glamorous, but it matters. Clean financials, clear revenue reporting, cohort data, customer metrics, implementation KPIs, security documentation, and a well-organized data room reduce buyer fear. Lower fear often means better offers.

A lot of valuation slippage happens not because buyers dislike the business, but because they cannot get comfortable quickly enough. The better prepared you are, the easier it is for a buyer to stretch.

7. Discount Drivers (What Lowers Multiples)

The businesses that trade at the low end usually have one thing in common: buyers are not sure the revenue is as strong, scalable, or defensible as management says it is. The discount is a risk adjustment.

The first common problem is a services-heavy revenue mix. If too much revenue comes from implementation, custom development, outsourced claims work, or support-intensive delivery, buyers worry that growth requires constant hiring. That tends to pull the business toward lower software-adjacent or services benchmarks.

The second issue is weak proof of stickiness. If you cannot clearly show renewals, product adoption, usage depth, or expansion, buyers will question whether your software is truly embedded. Insurance buyers are used to long relationships, so a thin retention story stands out quickly.

Customer concentration is another frequent discount. A founder may see one large customer as validation. A buyer may see the same customer as a valuation problem. The same applies when a few channel partners or carriers drive too much of the pipeline.

Another discount driver is long, custom, or fragile implementation. If every deployment looks like a fresh consulting project, it becomes harder for buyers to underwrite future growth. They will also discount the business if integrations are messy, deployment time is unpredictable, or success still depends too heavily on you personally.

In this sector, "AI without proof" is also a discount. Buyers hear many claims about automation, decisioning, and fraud detection. If you cannot back that up with proprietary data, measurable lift, or real customer outcomes, the AI story often gets treated as marketing rather than value.

Finally, messy company infrastructure lowers price. Weak financial records, unclear revenue recognition, poor KPI reporting, incomplete security documentation, unresolved legal issues, and founder dependency all make buyers nervous. These are fixable, but if left unaddressed they can push you down the range.

8. Valuation Example: A Fictional Insurance Software Company

Let’s make this concrete with a fictional example. Assume NorthPeak Claims Cloud is a made-up insurance software company with USD 10m of annual revenue. This is not a formal valuation and not investment advice. It is just a worked example to show how buyers often think.

NorthPeak sells claims workflow software to mid-sized insurers and TPAs. It has subscription revenue, some implementation revenue, decent customer retention, and integrations into claims and document systems. It is growing, but not at venture speed. It has a good product, but it is not yet a category-dominating asset.

Step 1: How the valuation logic works

First, you choose the right benchmark set. Because NorthPeak is software-led and sits in claims operations, the best public reference points are insurance core systems software and claims, risk, and fraud analytics platforms. Services and TPA-like comps are still useful, but mainly as downside checks if the business turns out to be more labor-heavy than management presents.

Second, you adjust for private company reality. Public markets in the source data show roughly 3.5x EV/Revenue for insurance core systems and 3.9x for claims and analytics platforms, but a private USD 10m revenue company usually deserves some discount for size, liquidity, concentration, and execution risk.

Third, you look at company-specific drivers. If NorthPeak has repeatable deployments, strong gross margins, real workflow embedment, and evidence customers rely on it every day, it can move toward the stronger end of the range. If it has weak retention proof, heavy services mix, or founder dependence, it drifts down.

The source example for a smaller, mature insurance technology provider with limited proof of premium drivers used a revenue-based range of roughly 0.9x to 2.4x. That logic is still useful here as a downside-to-base framework. For a somewhat larger and better-positioned fictional company at USD 10m revenue, it is reasonable to widen the range upward if the quality indicators are stronger - but still stay grounded below the highest public software multiples.

Step 2: Apply the logic to the fictional company

For NorthPeak, a sensible framework might look like this:

Why those ranges make sense

The discounted case fits a business that is clearly useful but still looks partly services-driven, has patchy retention evidence, longer custom implementations, or some concentration risk. This is the type of company buyers may compare against lower-quality software, IT services, or claims-related service models.

The core range fits a solid private insurance software business: recurring revenue is meaningful, gross margins are healthy, customers renew, the product is used in real workflows, and delivery is increasingly repeatable. This is where many good founder-owned companies should expect serious buyer discussions to start.

The premium case requires more than "good software." It usually means strong workflow embedment, clear switching costs, strong net revenue retention or module expansion, credible data or decisioning advantage, and a business model that looks increasingly software-like rather than service-like. It may also require strategic fit or a competitive process with multiple interested buyers.

What this means for founders

Two insurance software businesses can both have USD 10m of revenue and still be worth very different amounts. One might be worth closer to USD 12m, while another could support interest above USD 35m. The difference is not magic. It usually comes down to revenue quality, workflow ownership, growth credibility, margin structure, and buyer competition.

That is why preparation matters so much. You are not just trying to "hit a number." You are trying to make it easier for buyers to believe your business deserves the stronger end of the range.

9. Where Your Business Might Fit (Self-Assessment Framework)

A useful way to self-assess is to score yourself honestly across three groups of factors. Give each factor a score of 0, 1, or 2. Zero means weak. One means acceptable. Two means strong.

How to use it

Start with the high-impact factors first. Those usually have the biggest effect on valuation. Then look at medium-impact factors that shape buyer comfort. Finally, bonus factors can push a good business into a better outcome when the market is competitive.

A more detailed version looks like this:

Interpreting the total

If you score in the top band, you are closer to the premium part of the market and should think carefully about positioning and buyer tension. If you are in the middle band, you likely have a sellable business but may still have a few issues keeping you from the best outcomes. If you are in the lower band, the goal is not to panic - it is to identify which 2-3 fixes will move valuation the most before going to market.

The point of the exercise is not perfection. It is honesty. Most valuation improvements come from fixing a few important weaknesses, not trying to improve everything at once.

10. Common Mistakes That Could Reduce Valuation

The first big mistake is rushing the sale. Founders often decide to sell after a strong quarter, an inbound approach, or simple fatigue. But if your numbers, story, and materials are not prepared, the buyer ends up defining your business for you. That usually leads to a weaker first offer and less room to recover later.

The second mistake is hiding problems. Issues almost always come out in diligence - customer churn, contract quirks, implementation problems, security gaps, weak margins, disputed IP ownership, messy cap tables, or pipeline softness. When buyers find surprises late, they do not just lower price. They lose trust.

A third mistake is weak financial records. In insurance software, buyers want to understand recurring versus non-recurring revenue, services versus software mix, gross margin by revenue type, customer cohorts, renewal behavior, and implementation profitability. If you cannot show this clearly, your business will be valued more conservatively than it might deserve.

Another mistake is running an unstructured process. A structured, competitive sale process with a good advisor usually produces better outcomes than a one-buyer conversation. In practice, that can mean materially higher pricing - often around 25% better than a loosely run process - because competition improves leverage, tension, and price discovery.

A fifth mistake is telling buyers your target price too early. Once you say, "I’m looking for USD 20m," many buyers will simply anchor around that number. You kill price discovery. Instead of hearing what the market might really pay, you often end up getting narrow offers just above your own number.

There are also sector-specific mistakes. One is overselling AI without proof. Insurance buyers are used to bold claims. If you cannot show model performance, workflow adoption, or measurable claims or underwriting outcomes, the story falls flat. Another is underestimating implementation drag. If custom work, carrier integrations, and deployment timelines are more complicated than your materials suggest, buyers will find out and discount quickly.

11. What Insurance Software Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work usually falls into three buckets: improve the numbers, improve the risk profile, and improve the story buyers will tell themselves about your company.

Improve the numbers buyers care about most

Start by separating software revenue from services revenue clearly. If implementation is dragging down the valuation story, look for ways to standardize onboarding, reduce customization, and package more of the value into the product itself.

Track retention properly. Show logo retention, revenue retention, customer expansion, module adoption, and churn reasons. If you can improve renewals or expansion even modestly before a process, that often changes how buyers see the whole business.

Also work on gross margin clarity. In this sector, founders often know the business is good but do not present the margin story well. Make it easy for a buyer to see what part of the business is truly software-like.

Reduce the main risks

If customer concentration is high, try to reduce it before launch or at least show a credible path to doing so. If the founder is still in the middle of every product decision, sales call, or deployment issue, start delegating and documenting.

Tighten contracts, security materials, product documentation, and KPI reporting. A buyer will feel much better about stretching on price if diligence looks clean and controlled rather than chaotic.

If your implementations are long and variable, work on repeatability. A shorter, more predictable time-to-value helps both valuation and the quality of buyer interest.

Strengthen the strategic story

Map your product to the workflows that matter most. Show where you sit in claims, policy, billing, underwriting, fraud, or ecosystem coordination. The more clearly you can explain your role in the insurance operating stack, the easier it is for a buyer to see strategic value.

Build proof of measurable outcomes. Show faster claims resolution, lower fraud leakage, improved accuracy, lower operating cost, better throughput, or better customer experience. Buyers pay more for outcomes than features.

Highlight integrations, embedded usage, and expansion potential. If your customers tend to adopt more modules over time or expand across lines of business, make that central to your story.

Prepare the company for a real process

Get your materials in shape early: historical financials, forward projections, customer metrics, org chart, product roadmap, security and compliance materials, top customer summaries, and a clean explanation of the revenue model.

Then think carefully about buyer positioning. Not every buyer will value your business the same way. Some will see software. Some will see services. Some will see a gap in their product suite. Your job is to run a process that gets the story in front of the buyers most likely to value it properly.

12. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can improve outcomes first by widening the buyer universe. Instead of relying on a short list of obvious names, AI can help identify hundreds of qualified acquirers based on deal history, product fit, synergies, financial capacity, and buyer behavior. More relevant buyers usually means more competition, better offers, and more fallback options if one party drops out.

It can also compress timelines. With AI-driven buyer matching, faster outreach, faster creation of marketing materials, and better support through due diligence, it becomes possible to move from preparation to initial conversations and offers much faster than in a manual-only process. In many cases, initial offers can be reached in under 6 weeks.

The best version of this is not AI alone. It is expert human advisors, enhanced by AI. You still want seasoned M&A professionals running the process, framing the story, handling negotiations, and giving buyers confidence. What AI changes is the speed, breadth, and precision of execution - helping deliver Wall Street-grade advisory quality without the traditional bulge bracket cost structure.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.