The Complete Valuation Playbook for IT Infrastructure Management Businesses

A data-driven playbook showing what IT infrastructure management businesses actually sell for and what drives high multiples.

If you run an IT Infrastructure Management business - an MSP, system integrator, cloud ops provider, or infrastructure-focused security services firm - you are likely operating in a market that is consolidating fast. Strategic buyers want scale, coverage, and capabilities. Private equity wants recurring revenue and clean operations they can grow and resell.

This playbook is built for founders and CEOs considering a sale in the next 1-12 months. It will show what similar businesses actually sell for, decode what drives higher vs lower multiples, and give you a practical self-assessment plus a 6-12 month action plan. The numbers below are illustrative ranges based on the provided deal and public comps data - not investment advice or a formal valuation.

1. What Makes IT Infrastructure Management Unique

IT Infrastructure Management is one of the most “real world” corners of tech. Buyers like it because customers rarely turn it off. But buyers also discount it because it can look like a people-heavy services business unless you prove otherwise.

The main business types buyers see

Most privately held companies in this space fall into a few recognizable profiles:

- Managed IT services (MSP) and infrastructure ops: monitoring, patching, endpoint management, backup, helpdesk, network management, hybrid cloud ops.

- Systems integration and infrastructure projects: migrations, data center work, network refreshes, Microsoft stack implementations, cloud transitions.

- Managed security overlays: managed detection/response partners, SOC services, compliance, security engineering attached to infra delivery.

- Infrastructure software and tooling (less common in private IT infra management): monitoring, configuration/integrity tools, automation, infra-as-code platforms.

Unique valuation considerations

Valuation in this sector hinges on a few “buyer reality checks” that don’t matter as much in pure software:

- Recurring revenue quality matters more than revenue level. A USD 10m MSP with long-term managed contracts can be worth more than a USD 15m project shop with lumpy work.

- Gross margin tells the truth. If a big chunk of revenue is hardware resale or pass-through licenses, the revenue multiple will compress.

- Delivery capacity is a constraint. Growth is often limited by hiring and utilization, not demand. Buyers pay up when you can scale delivery without quality breaking.

- Customer concentration is common. A few big accounts can drive a lot of revenue, which can cap valuation if retention risk is high.

Key risk factors buyers will always check

In diligence, sophisticated buyers tend to obsess over:

- Contract terms and renewals: are SLAs multi-year, or can customers walk quickly?

- Churn and “silent churn”: customers staying but shrinking spend.

- Vendor dependency: one hyperscaler, one security vendor, one distributor relationship.

- Security and liability posture: incident history, insurance, tooling maturity, response process.

- People risk: does the business run on 2-3 key engineers (or the founder)?

2. What Buyers Look For in an IT Infrastructure Management Business

Buyers are not buying “IT services.” They’re buying a predictable stream of cash flow with manageable risk, plus a platform they can scale.

The basic fundamentals still matter

Even in infrastructure services, buyers anchor on:

- Scale: revenue size matters, but quality matters more.

- Growth: consistent growth is rewarded; flat or declining growth gets discounted.

- Profitability (EBITDA): EBITDA is the proxy for cash generation and operational maturity.

- Customer retention: “Do customers stick around and buy more over time?”

The sector-specific nuances that swing outcomes

Where IT infrastructure management gets judged differently:

- Recurring vs project mix: managed services revenue is valued more highly than one-off projects.

- Gross margin mix: high-margin managed services gets rewarded; low-margin resale drags multiples.

- Operational maturity: ticketing discipline, standardized SLAs, reporting, security controls, and clear service catalogs signal “institutional readiness.”

- Evidence of value delivered: uptime metrics, time-to-resolution, compliance outcomes - buyers love measurable outcomes, not anecdotes.

How private equity thinks about your business

Private equity (PE) buyers usually run the same mental model:

- Entry multiple vs exit multiple: they care what they pay today and what they can sell it for in 3-7 years.

- Exit options: who buys later - a bigger MSP platform, a larger IT services group, or a strategic buyer that needs your capabilities?

- Levers they expect to pull (in plain English):

- Raise prices on underpriced contracts and reduce unprofitable work

- Standardize service delivery to improve margins

- Cross-sell security, cloud management, and compliance services

- Do add-on acquisitions to grow faster and build coverage

- Improve sales process and reduce founder dependence

If your business already looks “platform-like” (repeatable delivery, strong recurring mix, clear KPIs), PE can justify paying more because they can see the path to a higher-value resale.

3. Deep Dive: The Valuation Nuance That Matters Most - Revenue Quality vs Revenue Volume

In IT infrastructure management, two companies can have the same revenue and wildly different valuations. The biggest driver is usually revenue quality - how predictable, contractual, and high-margin your revenue is - not just the top line.

Why this matters in the data

In the provided valuation logic example for a services-led MSP/system integrator profile, the defensible comp band converges around ~0.8–1.6x EV/Revenue for a small regional services firm at USD 10m revenue, assuming no clear evidence of software-like margins or strong productization. That range is anchored by both public and private “services-ish” comps and is explicitly sensitive to recurring mix and margin structure.

Why buyers care (in human terms)

Buyers are buying future cash flows. A contract that renews annually with clear SLAs and embedded services is “easy to underwrite.” A project pipeline is not.

Buyers pay more when:

- your customers are unlikely to leave quickly,

- your gross margin is strong and stable,

- your service delivery is standardized enough to scale without chaos.

How to move from “lower-value” to “higher-value” in 6-12 months

This is often achievable without reinventing the company:

- Convert “best effort” support into tiered managed offerings with SLAs, pricing ladders, and measurable outcomes.

- Reduce pass-through revenue as a share of total, or at least separate it cleanly in reporting so buyers don’t penalize the whole business.

- Lock in longer-term commitments where appropriate (even if pricing stays similar) to improve predictability.

4. What IT Infrastructure Management Businesses Sell For - and What Public Markets Show

Here’s the key framing: private deal multiples reflect what real buyers paid, while public multiples reflect what the stock market is willing to pay for larger, more liquid, and often more diversified companies. Your valuation usually lives below public comps - unless you have scarce, highly strategic capabilities.

4.1 Private Market Deals (Similar Acquisitions)

Across the provided precedent transactions data, the group averages show:

- Overall private deals: ~2.6x EV/Revenue and ~28.1x EV/EBITDA (average/median reported).

- Managed IT Infrastructure & Cybersecurity Services (MSPs and system integrators): ~1.7x EV/Revenue (average) and ~1.5x (median); EV/EBITDA shows a wide spread with ~23.4x average and ~12.0x median.

That “wide EV/EBITDA spread” is real: small services businesses with modest EBITDA can produce very high EV/EBITDA on paper, especially when buyers are paying for strategic fit, future growth, or scarcity of talent rather than current profit.

A founder-friendly way to interpret this: most MSP/SI deals cluster around mid-single-digit to low-double-digit EBITDA multiples in the middle of the market, and around ~1-2x revenue when the business is services-led. Premium outcomes exist, but they usually require a clear “why us” story (specialization, sovereign credentials, IP, or platform-like recurring revenue).

These are illustrative. Your outcome depends on growth, margin, recurring mix, contract structure, and risk profile.

4.2 Public Companies

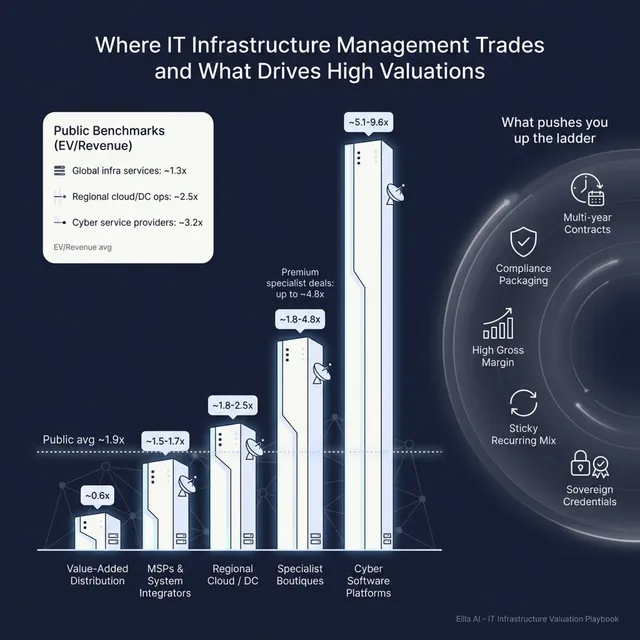

Public markets (as of mid-to-end 2025 in the provided dataset) show a clear segmentation:

- Global IT Infrastructure Managed Services & System Integrators: average ~1.3x EV/Revenue (median ~0.9x) and ~8.7x EV/EBITDA.

- Regional cloud & data center operators: average ~2.5x EV/Revenue (median ~1.8x) and ~15.9x EV/EBITDA (median ~12.5x).

- Cybersecurity-focused service providers (managed security, SOC/MDR): average ~3.2x EV/Revenue (median ~1.3x) with extremely high EV/EBITDA readings in the dataset (reflecting negative or near-zero EBITDA in some cases).

- Overall public set: average/median ~1.9x EV/Revenue and ~13.9x EV/EBITDA.

How to use these public multiples:

- Treat them as a reference band, not a price tag.

- Adjust downward for smaller scale, customer concentration, founder dependence, and messy financials.

- Adjust upward only if you have scarce, defensible differentiation (examples in the premium drivers section).

5. What Drives High Valuations (Premium Valuation Drivers)

Premium outcomes in this sector happen when buyers stop thinking “services firm” and start thinking “strategic control point,” “compliance engine,” or “platform-like recurring revenue.”

Below are the premium drivers observed in the data, grouped into founder-friendly themes, plus a few universal M&A drivers that always matter.

5.1 Compliance and regulated trust as a moat

Observed in premium outcomes tied to enterprise-grade governance and identity control points. The pattern is simple: when you sit in the middle of compliance, buyers pay more.

What this looks like in an IT infrastructure management business:

- Managed services packaged around compliance outcomes (audit-grade reporting, policy enforcement, identity management operations).

- Certifications and documented controls that reduce buyer fear.

- Strong enterprise references where compliance is the reason you won.

Practical example:

- Instead of “we run IT,” you sell “we keep you audit-ready with measurable controls, every month.”

5.2 Specialist positioning in high-demand ecosystems (Azure, ServiceNow, hyperscalers)

The data shows specialist cloud-platform boutiques can command higher outcomes than generic SIs when they have scarce expertise and repeatable delivery accelerators.

What buyers pay for:

- A clear niche: “We are the Azure GitOps/DevSecOps team” or “We are the ServiceNow implementation + managed services partner.”

- Proof of repeatable delivery: templates, automation packs, pre-built playbooks.

Practical example:

- If your proposal is faster and lower-risk because you have pre-built accelerators, buyers see margin upside and scalability.

5.3 Recurring managed security and platform-like services

Premium deal narratives in the data cluster around “sticky, recurring, high-margin managed offerings,” especially in security and integrity monitoring contexts.

What that means for you:

- Multi-year managed contracts

- Clear tiers and packaging

- Outcome reporting (time-to-detect, time-to-respond, patch compliance, vulnerability closure rates)

Practical example:

- A managed security add-on that is sold and delivered like a subscription (even if it’s still service-delivered) looks more “software-like” to buyers.

5.4 Sovereign and government-grade credentials

Where you have public sector exposure or data residency requirements, compliance barriers can act like a moat.

What buyers like:

- Government frameworks, data residency controls, security clearance capability, or sovereign cloud alignment.

- Documented renewals and long-term relationships.

Practical example:

- If your contracts are hard to replace due to certifications and procurement hurdles, buyers underwrite retention with more confidence.

5.5 Strategic integration value to a larger platform buyer

Premium outcomes also show up when a larger buyer can plug you into a bigger platform story - AI, automation, hybrid cloud operations, or enterprise security portfolios.

What you can do:

- Build co-sell motions with major vendors.

- Show pipeline sourced through vendor ecosystems.

- Demonstrate how your service “slots into” a bigger platform.

5.6 Universal premium drivers that still matter

Even in this niche, these basics can move you up the range:

- Clean financials and credible forecasting

- Diversified customer base

- Strong second-layer leadership (not founder-only)

- Low churn and strong net retention (customers expanding spend)

- Repeatable sales motion (not pure relationships)

6. Discount Drivers (What Lowers Multiples)

Discounts happen when buyers see risk they can’t price confidently, or when they fear your earnings will shrink after you leave.

6.1 Low-margin revenue and resale-heavy mix

If a big chunk of revenue is hardware or pass-through licensing, buyers will:

- value that portion at a much lower multiple, or

- ignore it and focus on gross profit instead of revenue.

If this is you, the fix is not “stop selling hardware.” It’s separate it clearly, show gross profit by line, and prove services drive value.

6.2 Weak recurring visibility

Short-term contracts, month-to-month arrangements, or informal renewals reduce predictability.

Buyers discount when they can’t answer:

- “What revenue is already contracted for the next 12 months?”

6.3 Customer concentration and key-person risk

Infrastructure management businesses often have a few large customers and a few critical engineers.

If losing one customer or one engineer breaks the business, buyers will:

- push for earnouts,

- retain more cash in escrow,

- or lower the headline price.

6.4 Lumpy project revenue and inconsistent delivery margins

Project work isn’t bad, but buyers will discount when:

- utilization is unstable,

- projects are priced inconsistently,

- margins swing wildly quarter to quarter.

6.5 Messy financial records and unclear KPIs

If you can’t quickly prove gross margin by service line, recurring revenue %, churn, and customer concentration, buyers assume the worst until proven otherwise.

7. Valuation Example: A Fictional IT Infrastructure Management Company

This is a worked example to show the logic. The company and numbers are fictional, and the valuation range is illustrative - not a formal valuation.

Step 1: The logic (in plain English)

- Identify whether you are being valued like services, managed services, or software/platform.

- Use public comps to set a broad reference range, but weight toward the segment that matches your reality.

- Use private deal ranges as the “real world anchor.”

- Adjust for premium drivers (recurring, compliance, specialization, sovereign credentials) or discount drivers (resale-heavy, low recurring, concentration, messy financials).

The provided sources’ valuation logic for a small regional services-led MSP/SI profile converges on ~0.8–1.6x EV/Revenue as a reasonable band for a USD 10m revenue business, with upside toward ~1.6–2.0x if you can prove high gross margin and strong recurring SLAs, and downside toward ~0.5–0.8x if revenue is pass-through heavy.

Step 2: Apply it to a fictional company

Meet NorthBridge Infrastructure Services:

- USD 10.0m LTM revenue (fictional)

- 35 employees

- 55% of revenue in managed services contracts, remainder in projects

- Gross margin 38% overall (services strong, some resale included)

- EBITDA margin 10%

- No sovereign/government specialization, but solid mid-market retention

Now apply scenarios:

Step 3: What this means for you

Two USD 10m revenue businesses can be worth USD 8m or USD 20m because buyers pay for confidence: confidence that revenue stays, margins hold, and the business scales without breaking.

If you’re selling in 1-12 months, your best ROI is usually not “grow revenue at all costs.” It’s improving revenue quality, proof, and risk profile.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this to get a rough sense of where you sit. Score each factor 0-2:

- 0 = weak / unclear

- 1 = decent

- 2 = strong / proven

How to interpret:

- High scores across High Impact: you’re closer to the top end of services-led ranges and you’ll attract more bidders.

- Mixed scores: you’ll likely land in “fair market” territory, and deal terms (earnouts, retention) matter a lot.

- Low High Impact score: you may still sell, but you’ll want to fix the biggest risk flags first.

9. Common Mistakes That Could Reduce Valuation

9.1 Rushing the sale

If you go to market before your numbers and story are tight, buyers will anchor low and stay there.

9.2 Hiding problems

Every real issue surfaces in diligence. If you hide it, you don’t just lose value - you lose trust, and deals die from trust issues.

9.3 Weak financial records

This is fixable in 6-12 months more often than founders think:

- Separate pass-through vs services revenue

- Track gross margin by service line

- Track recurring revenue %, churn, customer concentration

- Make EBITDA credible and explainable

9.4 Not running a structured, competitive process with an advisor

A competitive process creates price tension. Research commonly cited in M&A practice suggests structured, advisor-led competitive processes can produce meaningfully higher outcomes - on the order of ~25% higher purchase prices versus negotiated one-off deals, largely because of better buyer reach and better price discovery.

9.5 Revealing what price you’re after too early

If you tell buyers “we want USD 10m,” many buyers will come back at USD 10.1m, USD 10.2m - instead of showing what they would truly pay. You kill price discovery.

9.6 Industry-specific mistake: blending resale revenue into “growth”

In this sector, “growth” that is mostly low-margin resale can make you look bigger but worth less. Buyers would rather see slower growth with improving services gross profit than fast growth with thin margins.

9.7 Industry-specific mistake: founder as the escalation path for everything

If customers or engineers escalate to you for delivery, pricing, or security decisions, buyers will either discount the price or force retention-heavy terms.

10. What IT Infrastructure Management Founders Can Do in 6-12 Months to Increase Valuation

Think in three buckets: improve the numbers, reduce buyer fear, and improve your “market story.”

10.1 Improve the numbers without a massive pivot

- Increase recurring revenue share: migrate “support-like” project work into managed plans.

- Improve gross margin clarity: separate pass-through revenue, report gross profit by service line.

- Normalize profitability: eliminate unprofitable contracts, re-price where value is obvious, reduce scope creep.

10.2 Improve revenue quality and predictability

- Standardize SLAs and tighten renewal process.

- Push toward annual or multi-year commitments where reasonable.

- Build a simple churn dashboard: logo churn, revenue churn, and expansion.

10.3 Build differentiation buyers will pay for

Based on premium patterns in the data:

- Pick a specialization lane (Azure ops, ServiceNow managed services, identity ops, compliance-driven managed security).

- Package accelerators and automation into your delivery - even small, practical tooling can change the buyer narrative from “people” to “process + IP.”

- Turn compliance into a product: audit-ready reporting, standardized controls, clear governance deliverables.

10.4 Reduce key-person risk

- Document delivery processes and escalation paths.

- Build a second layer of leadership and client ownership.

- Make sure top accounts have relationships with more than just the founder.

10.5 Prepare for diligence like a professional

- Clean customer list with revenue by customer and contract type

- Cohort view: new logos vs renewals vs expansion

- Clear explanation of any one-time spikes

- Security posture summary (controls, incident history, insurance)

11. How an AI-Native M&A Advisor Helps

Selling an IT infrastructure management business is not just “finding a buyer.” It’s running a process that creates competition, reduces uncertainty, and presents your business in the way buyers actually evaluate it.

An AI-native advisor can drive higher valuations through broader buyer reach by expanding the buyer universe to hundreds of qualified acquirers based on deal history, synergy fit, and financial capacity. More relevant buyers means more competition and stronger offers - and if one buyer drops late, you’re not stuck.

AI can also help you reach initial offers in under 6 weeks by accelerating buyer matching and outreach, speeding up marketing materials creation, and supporting diligence workflows so the process moves faster than manual-only approaches.

Finally, you still need human judgment. The best model is expert advisory enhanced by AI: experienced M&A advisors who know how to frame your story, defend your numbers, and run a credible process - with AI doing the heavy lifting behind the scenes. The goal is Wall Street-grade outcomes without traditional “bulge bracket” costs.

If you’d like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.