The Complete Valuation Playbook for Lab Software and Automation Businesses

A data-driven guide to how lab software and automation businesses are valued and what drives high multiples.

If you run a lab software and automation business and are thinking about a sale in the next 1-12 months, valuation is no longer something to leave until the last minute. Buyer appetite is still there, but it is more selective than it was during the peak market years. Strategic acquirers and private equity firms are still paying strong prices for the right assets - especially when the business is embedded in customer workflows, has sticky revenue, and solves expensive operational problems inside labs, diagnostics, or bioprocessing environments.

This playbook is built to help you answer three practical questions. First, what do businesses like yours actually sell for? Second, what pushes a valuation toward the top or bottom of the range? Third, what can you do in the next 6-12 months to improve the outcome before you go to market?

1. What Makes Lab Software and Automation Businesses Unique

Lab software and automation is not one simple category. It usually includes a mix of businesses such as lab workflow software, LIMS-connected products, robotic sample handling, automated quality control tools, lab process monitoring, custom automation systems, instrument control software, and integration-heavy engineering businesses that sit between hardware, software, and regulated lab operations.

That mix matters because buyers do not value all of these models the same way. A pure software product with recurring subscription revenue will usually be valued differently from a custom automation integrator. A business with proprietary robotics, software, consumables, and service contracts will usually be valued differently from a project-led engineering company that gets paid mostly for one-off builds.

The biggest valuation challenge in this sector is that many businesses look "software-enabled" without actually being software-like from a buyer's point of view. Buyers will ask very quickly: how much of revenue is recurring, how much is project-based, how dependent is delivery on your engineering team, and how easy is it to scale without adding headcount in step with revenue?

There are also sector-specific checks that come up again and again:

- regulatory and validation risk

- integration depth with customer systems such as LIMS, MES, ERP, or instrument stacks

- installed base and serviceability in the field

- dependence on a few large pharma, biotech, academic, or diagnostic customers

- backlog quality and project margin consistency

- exposure to capex cycles, grant cycles, or funding swings in biotech and life sciences

In other words, buyers are not only buying growth. They are buying confidence that your revenue, margins, and customer relationships will survive after the founders leave.

2. What Buyers Look For in a Lab Software and Automation Business

At a basic level, buyers care about the same big things they care about in most deals: revenue scale, growth, gross margin, EBITDA, customer concentration, and how predictable next year's numbers look. But in this sector, those factors are filtered through one important question: are you selling a repeatable product, or are you re-engineering the solution every time?

That is why two lab automation businesses with the same revenue can get very different valuations. One may be seen as a scalable platform with recurring software, upgrades, validation services, and a growing installed base. The other may be seen as a skilled engineering shop that happens to work in laboratories.

Strategic buyers usually focus on where your business fits inside their existing offering. They ask:

- does this add a missing capability?

- does it deepen our position in a valuable workflow?

- can we sell this to our installed base?

- can we attach service, consumables, software, or validation revenue after the acquisition?

Private equity buyers ask a slightly different version of the same question. They care about whether the business can be improved and sold again in 3-7 years at a similar or higher multiple. That means they look hard at:

- recurring revenue growth

- margin expansion potential

- pricing power

- cross-sell opportunities

- international expansion

- add-on acquisitions

- management depth below the founder

How private equity thinks about your business

A private equity buyer is usually trying to buy at one multiple and sell later at the same or a better one. So they will ask who the next buyer could be. That might be a larger PE fund, a strategic acquirer, or in rare cases a public listing candidate.

They also want clear "value creation levers" after closing. In this sector, those often include raising prices on service contracts, increasing software attachment rates, standardizing more of the product line, cross-selling into adjacent lab workflows, improving procurement, or acquiring smaller complementary companies.

If your business is too custom, too founder-dependent, or too hard to scale, PE may still be interested - but the price usually reflects that extra risk.

3. Deep Dive: Repeatable Platform Revenue vs Custom Project Revenue

This is one of the most important valuation questions in the entire sector. Many lab automation businesses sit somewhere in the middle: they have real technical IP, real software, and strong customer relationships, but a meaningful share of revenue still comes from bespoke projects, engineering time, and customer-specific deployment work.

The data strongly supports the idea that buyers pay more when they believe earnings are durable and repeatable. One of the clearest patterns in the transaction set is that some businesses earn premium EBITDA outcomes not because they look like high-growth SaaS, but because buyers trust the stability of the earnings stream. In other words, buyers often reward dependable service, upgrade, validation, and aftermarket revenue more than they reward a vague "software story."

That matters because some founders try to frame their business as a software platform when the financial profile says otherwise. Buyers usually see through that quickly. If your gross profit depends on custom engineering on every deal, or if delivery risk changes project to project, buyers will pull the multiple back toward an engineering or systems integrator benchmark rather than a pure software benchmark.

A more valuable profile usually looks like this:

The good news is that you do not need to become a pure SaaS business to improve valuation. You just need to move buyers toward believing that more of your revenue is repeatable, supportable, and scalable. In practice that can mean standardizing hardware modules, packaging implementation into defined offerings, selling annual software support, creating validated templates for common use cases, and proving that your installed base generates follow-on revenue.

If your business looks more like the left column today, the valuation goal for the next 6-12 months is not a total reinvention. It is to show that a bigger share of revenue can behave like an annuity rather than a one-time engineering event.

4. What Lab Software and Automation Businesses Sell For - and What Public Markets Show

Here is what the data actually shows. Private market deals in and around lab software, lab automation, lifecycle services, engineered systems, and adjacent automation tend to price well below the biggest public life science tools companies. That is normal. Public companies are larger, more diversified, more liquid, and usually have broader product sets and stronger aftermarket economics.

So public multiples are useful as reference points, but not as direct price tags for a privately held founder-owned business.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions provided, the overall average private market multiple is about 2.8x revenue and the median is about 1.7x revenue. Where EBITDA is disclosed, the overall average is about 7.8x EBITDA and the median is about 5.9x EBITDA.

But that overall average hides an important split. Services-heavy, distribution, and project-led businesses often transact around the low-to-mid part of the range. More strategic, scarcer, or more productized assets can move much higher - sometimes dramatically higher - especially when the buyer is underwriting unique capability rather than current profitability.

A few practical lessons come out of this. First, the headline highest revenue multiples in the dataset should be treated carefully. Some very high observations appear tied to scarce strategic capabilities or noisy underlying financials, not to ordinary sale processes. Second, the most relevant range for many privately held lab automation businesses is often not the flashy outlier - it is the tighter middle band where both revenue and EBITDA logic line up.

That is especially true for businesses with decent margins but a meaningful project component. In those cases, buyers often price off earnings durability, backlog quality, installed base, and repeatability more than off a "software category" label.

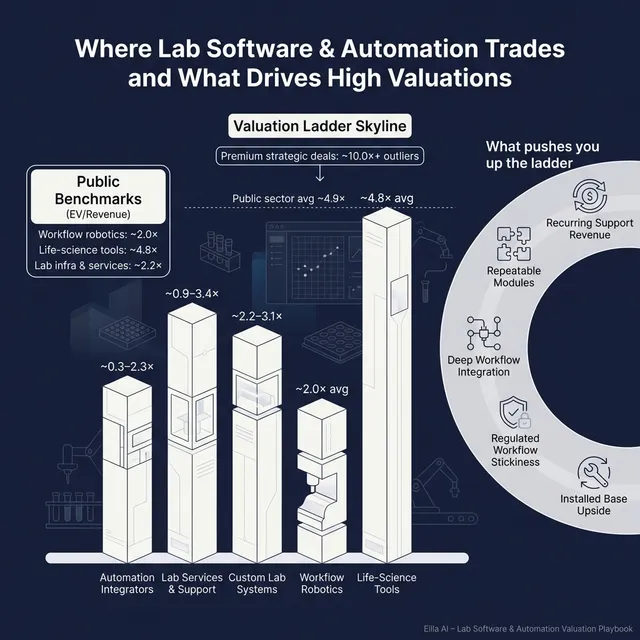

4.2 Public Companies

As of mid-to-late 2025, the public comp set provided shows an overall average of about 4.9x EV/Revenue and 25.6x EV/EBITDA, with medians of about 3.3x EV/Revenue and 20.1x EV/EBITDA. Those numbers are much higher than private deal averages, but again, these are larger and more scalable businesses.

At the segment level, the pattern is intuitive. Broad life science tools and analytical instrumentation businesses tend to trade above many smaller automation or project-led businesses because they have scale, recurring consumables, service revenue, global distribution, and better margin profiles. Lab automation and workflow robotics companies generally trade in a lower but still meaningful range. Infrastructure, fit-out, and services tend to trade lower unless there is something unusually strong about growth, market position, or margin quality.

*Averages are directionally useful, but some subgroup EBITDA averages are distorted by a few unusual data points and should be treated with caution.

The right way to use public multiples is as a valuation reference band. They can help show what high-quality, scaled, more liquid businesses in adjacent spaces trade for. But your private company will usually be adjusted downward for smaller size, customer concentration, lower liquidity, and greater founder dependency.

That said, there are cases where a private asset can punch above what you might expect. If your business is strategically scarce, deeply embedded in valuable workflows, and clearly expands a buyer's market reach or product set, a strategic buyer may pay closer to a public-style premium than a normal private market comparison would suggest.

5. What Drives High Valuations (Premium Valuation Drivers)

The premium drivers in this sector are not mysterious. Buyers pay more when they believe your revenue is durable, your role in the workflow is hard to replace, and your business can do more inside their hands than it could on its own.

5.1 Durable earnings, not just a growth story

One of the clearest patterns in the deal data is that premium outcomes are often expressed through EBITDA multiples rather than flashy revenue multiples. That usually happens when a buyer trusts the staying power of earnings - repeat service revenue, upgrade cycles, validation work, compliance-driven stickiness, and installed-base support.

Why buyers pay more:

- they can underwrite cash flow with more confidence

- they see lower downside risk after closing

- they believe the business can support debt or fund further growth

Practical examples:

- annual software support tied to deployed systems

- recurring validation, maintenance, calibration, or compliance services

- upgrade revenue from an installed base rather than constant new-logo dependence

5.2 Strategic scarcity

Some assets attract premium pricing because they fill a gap a buyer cannot easily build on its own. In the data, the highest revenue-multiple outliers look more like strategic tuck-ins for scarce capability than standard operating-company valuations.

Why buyers pay more:

- the asset unlocks a missing product line

- it accelerates entry into an attractive lab workflow

- it expands the buyer's addressable market quickly

Practical examples:

- proprietary automation in a fast-growing sample prep or bioprocess workflow

- unique instrument-control software with deep regulatory credibility

- a rare technical capability that strengthens a larger platform

5.3 Installed base and aftermarket economics

A large installed base matters because it can create annuity-like revenue through support, service, parts, software updates, consumables, and future system expansions. Buyers love that because it lowers customer acquisition friction and increases lifetime value in plain English: once the customer is in, there are more ways to keep earning revenue.

Why buyers pay more:

- recurring gross profit is usually higher quality than project revenue

- switching costs rise once your system is embedded

- follow-on sales are cheaper than winning new accounts

Practical examples:

- field service contracts

- software licenses or update subscriptions attached to existing machines

- modular system expansions sold into existing customers

5.4 Mission-critical workflow position

The closer you are to a workflow that directly affects throughput, quality, compliance, or release timing, the more valuable you become. Buyers pay more for products that customers cannot easily live without.

Why buyers pay more:

- mission-critical tools are harder to displace

- price increases are easier to hold

- customer relationships are more resilient in budget cuts

Practical examples:

- systems tied directly to sample integrity, QC release, chain of custody, or regulated documentation

- automation that reduces operator error in high-cost lab environments

- software that becomes the control layer between instruments and lab operations

5.5 Clean data and credible numbers

This sounds basic, but it matters a lot. The deal set includes examples where noisy or odd margin data can distort apparent valuation. Sophisticated buyers will normalize quickly. Sloppy reporting does not create a premium - it usually damages trust.

Why buyers pay more:

- cleaner financials shorten diligence

- confidence reduces the need for holdbacks and earn-outs

- it makes your growth and margin story believable

Practical examples:

- clear split between product, software, services, and pass-through revenue

- backlog reported in a way that matches actual conversion and margin

- accurate gross margin by business line

5.6 Management depth and transferability

If the business still depends on you for sales, architecture, delivery, and customer rescue, buyers worry. If there is a credible second layer of leadership, the business becomes easier to own and easier to finance.

Why buyers pay more:

- transition risk falls

- integration becomes easier

- buyers can scale the business faster

Practical examples:

- a clear commercial lead, engineering lead, and operations lead below founder level

- documented customer handoffs

- less founder involvement in day-to-day delivery

6. Discount Drivers (What Lowers Multiples)

Most low-end deals are not caused by one catastrophic problem. They usually happen because buyers see too many reasons to discount certainty.

The most common discount driver in this sector is revenue that looks less repeatable than the founder thinks it is. If a large share of sales comes from custom projects, one-off builds, or customer-specific engineering work, buyers worry about forecasting, margin variability, and how much growth really depends on adding more engineers.

Another major issue is heavy use of earn-outs or contingent consideration. In the transaction data, milestone-heavy structures often show up when buyers are not fully comfortable with forecastability. That does not always mean the asset is weak. It does mean the buyer wants risk-sharing built into the price.

Other common discount drivers include:

- customer concentration, especially if one or two pharma or diagnostics accounts drive a big share of revenue

- weak backlog quality, where signed work does not reliably translate into margin

- lumpy project economics or frequent cost overruns

- low software attachment or weak monetization of the installed base

- founder dependence in sales, design, or key relationships

- poor segmentation of financials, making it hard for buyers to see what is really profitable

- exposure to volatile biotech funding cycles or delayed capital budgets

- limited regulatory depth if the buyer expects you to operate in validated or compliance-heavy workflows

There is also a more subtle discount driver: trying to claim a premium category without the numbers to support it. If you position the company as a software platform but buyers see a services-heavy integration business, the valuation usually drops fast. Mis-positioning hurts credibility.

The positive takeaway is that many of these issues can be improved before a sale. Even if you cannot change the whole business model in 12 months, you can make the economics, reporting, and buyer story much stronger.

7. Valuation Example: A Lab Software and Automation Company

Let’s turn the valuation logic into a worked example.

The company below is fictional. The revenue level is also fictional. This is not investment advice or a formal valuation. It is just a practical illustration of how buyers often think.

a) The fictional company

Assume a fictional business called NorthBridge Lab Automation.

NorthBridge designs and deploys automated lab workflow systems for pharma, diagnostics, and advanced research labs. It combines custom automation cells, workflow software, instrument integration, LIMS connectivity, and validation support. It has a growing installed base and some recurring software and service revenue, but it is still not a pure software company.

Assume:

- revenue: USD 10m

- EBITDA margin: 18%

- EBITDA: USD 1.8m

b) How the valuation logic works

The first step is not to grab the highest multiple in the market. It is to find the right peer set. For a business like this, the best comparison is usually not pure SaaS and not giant life science tools majors. It is a middle ground: custom lab automation, engineered systems, and workflow-driven businesses with some software but meaningful delivery content.

The source data suggests that for a profitable, established, mid-market lab automation business with an integration tilt, a sensible core revenue range is around 2.2x-3.1x revenue. That is also supported by the EBITDA cross-check, where a practical engineered-systems range of around 12x-17x EBITDA produces very similar results for the worked example logic.

That convergence is important. When revenue-multiple and EBITDA-multiple approaches point to roughly the same zone, the valuation case is usually more credible.

c) Applying that logic to NorthBridge

Base case

If NorthBridge is profitable, reasonably diversified, has a decent installed base, and some recurring support revenue - but still relies meaningfully on custom projects - the core range might look like this:

- Revenue approach: USD 10m x 2.2x-3.1x = USD 22-31m

- EBITDA approach: USD 1.8m x 12x-17x = USD 22-31m

That gives a practical base case enterprise value of roughly USD 22-31m.

Premium case

Now assume NorthBridge has several strong premium drivers:

- high customer retention

- clear repeatability in core system modules

- meaningful annual support and software revenue

- a strong installed base generating upgrades

- low founder dependence

- deep workflow relevance in compliance-sensitive environments

In that case, a strategic buyer may be willing to pay above the core range. The premium scenario might move toward 3.5x-4.5x revenue, implying:

- Revenue approach: USD 10m x 3.5x-4.5x = USD 35-45m

That is not the same as saying every premium-looking business will get that price. It means that when a buyer sees genuine strategic value and durable economics, the range can widen materially.

Discounted case

Now assume the opposite:

- a few customers dominate revenue

- backlog is hard to trust

- most deals are one-off custom projects

- margins swing from project to project

- the founder still drives sales and solution design

- recurring revenue is limited

In that case, the multiple may fall closer to 1.5x-2.0x revenue, implying:

- Revenue approach: USD 10m x 1.5x-2.0x = USD 15-20m

d) Summary table

The lesson is simple: two lab software and automation companies with the same USD 10m revenue can be worth very different amounts. The difference usually comes down to repeatability, risk, installed-base monetization, and how strategic the asset feels to the buyer.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as an honest self-check, not a vanity exercise. Score each factor from 0 to 2.

- 0 = weak / unclear

- 1 = decent but not strong

- 2 = clear strength

Scoring table

How to interpret the score

If your total score is in the top band, you are more likely to sit toward the premium end of the market. That does not guarantee a premium price, but it usually means your buyer story is stronger and your risk profile is lower.

If you score in the middle band, you are probably in fair-market territory. You can still get a good outcome, but process quality and positioning will matter a lot.

If you score in the lower band, that does not mean you should not sell. It means the biggest value gains are likely to come from fixing a few specific issues before going to market - especially around recurring revenue, financial clarity, and founder dependence.

The real purpose of this exercise is to identify where one point of improvement can have the biggest payoff.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often decide to sell after a good year and assume the market will fill in the gaps. It usually does not. If your numbers are not clean, your segmentation is weak, and your growth story is not supported by evidence, buyers will either lower price or shift more of it into earn-outs.

Another major mistake is hiding problems. Margin issues, customer concentration, delayed projects, product gaps, or compliance issues almost always surface in diligence. Once buyers feel something was hidden, trust drops and so does value.

Weak financial records are also costly. In this sector, it is not enough to show top-line revenue and one EBITDA number. Buyers want to see what portion of revenue is software, service, product, spare parts, validation, and pass-through. They want to understand gross margin by line, backlog quality, and whether recurring revenue is truly recurring. Many founders can improve this meaningfully within 6-12 months.

A fourth mistake is not running a structured competitive process with an advisor. Good research and real-world deal experience both point in the same direction: a well-run competitive sale process with a capable advisor often leads to meaningfully higher outcomes, sometimes around 25% higher purchase price, because it improves buyer tension, market positioning, and negotiating leverage.

Another costly mistake is telling buyers what price you want too early. Once you say, for example, that you want USD 10m of enterprise value, many buyers will anchor right around that number. They may come back at USD 10.1m or USD 10.2m instead of showing you what they would actually pay in a competitive process. That kills price discovery.

Two sector-specific mistakes are especially common here. The first is overstating how "software-like" the business is when the revenue is still mostly project-led. The second is under-monetizing the installed base - meaning you have systems in the field, but no strong maintenance, upgrade, data, or software revenue attached to them. Buyers notice both immediately.

10. What Lab Software and Automation Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work is not cosmetic. It is about making the business easier to understand, easier to believe, and easier to scale.

10.1 Improve the numbers

Start by cleaning up financial reporting. Split revenue into logical buckets such as software, equipment, engineering services, validation, maintenance, consumables, and pass-through. Track gross margin by line. Show backlog clearly. Make it easy for a buyer to see what is recurring, what is project-based, and what has the best economics.

If you can improve margin consistency, do it. Even modest gains matter if they show the business is becoming more disciplined and repeatable.

10.2 Increase recurring revenue quality

You do not need a massive pivot to improve valuation. Focus on practical steps:

- put annual support contracts in place where they do not exist

- package software updates and support into standard renewals

- create paid validation, maintenance, and optimization offerings

- turn one-time customizations into reusable modules

This helps move the business closer to the higher-value profiles seen in the market.

10.3 Strengthen the installed-base story

Document how many systems are live, where they are, which customers they sit with, and what follow-on revenue they have generated. If you have weak service attachment today, fix that. Buyers are much more comfortable paying up when they see a real aftermarket opportunity rather than just one-off project history.

10.4 Reduce key-person risk

Push customer ownership, technical architecture, and delivery leadership below founder level. Build a visible second layer. Buyers do not need you to disappear before a sale - but they do need proof the business can run without you being in every critical decision.

10.5 Make the commercial story sharper

Be specific about the workflows you win in and why. "We automate labs" is too broad. "We reduce manual error and release delays in sample preparation and QC workflows for regulated pharma labs" is much better. Clear positioning helps buyers see strategic fit faster.

10.6 Fix obvious valuation drags early

If customer concentration is high, try to diversify before launch. If one project type has weak margins, reprice it or narrow the scope. If your reporting is messy, clean it now rather than during diligence. If recurring revenue exists but is not tracked properly, fix the KPI reporting before buyers arrive.

The point is not perfection. It is momentum. Buyers pay more when they can see that the business is becoming more durable, more scalable, and less risky.

11. How an AI-Native M&A Advisor Helps

Selling a business is not just about finding one buyer. It is about creating the right market around your company. An AI-native M&A advisor can expand the buyer universe from a short manual list to hundreds of qualified acquirers screened for deal history, strategic fit, synergies, and financial capacity. More relevant buyers usually means more competition, stronger offers, and a better chance the deal still closes if one buyer drops out.

Speed matters too. With AI helping match buyers, build outreach, prepare materials, and support diligence, the process can move much faster than a traditional manual-only approach. In many cases, that means initial conversations and first offers can be reached in under 6 weeks.

The model works best when AI supports, rather than replaces, experienced human advisors. You still want seasoned M&A professionals shaping the story, preparing buyer-ready materials, framing the business the right way, and negotiating with credibility. The difference is that AI helps deliver Wall Street-grade process quality without traditional bulge-bracket cost and friction.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.