The Complete Valuation Playbook for Learning Platforms Businesses

A practical, data-driven guide to how learning platform businesses are valued and what drives high multuples.

If you run a learning platform business and you are thinking about a sale in the next 1-12 months, valuation becomes less about what you feel your company is worth - and more about how buyers will underwrite risk and believe the next 3-5 years will play out.

This playbook is built for learning platform founders, using real patterns from precedent transactions and public market multiples in and around EdTech. It will (1) show what comparable businesses actually sell for, (2) decode the few drivers that consistently move multiples up or down, and (3) give you a practical self-assessment and a 6-12 month action plan to improve outcomes.

A big reason to focus on valuation now: learning platforms are in a buyer-led market where procurement scrutiny is higher, budgets are tighter, and consolidation is real. That cuts both ways - weaker businesses get punished, but differentiated, mission-critical platforms can still command premium outcomes.

1. What Makes Learning Platforms Unique

Learning platforms look like “software,” but buyers rarely value them like generic SaaS.

Most learning platform businesses fall into a handful of archetypes, each with different valuation logic:

- Institutional platform SaaS - LMS/LXP, student engagement, scheduling, records, compliance tooling.

- K-12 curriculum + adaptive learning - content plus platform, often tied to outcomes, district procurement cycles, and renewal dynamics.

- Assessment, exams, proctoring, smart campus infrastructure - workflow + integrity + compliance, often high-stakes and embedded.

- Online course marketplaces and credentials - two-sided content aggregation, creator/institution supply, demand generation, churn dynamics.

- Student support and tutoring platforms - consumer or hybrid models, higher marketing spend, more churn sensitivity.

- Publishing and content rights businesses - content libraries, distribution, renewals, and sometimes heavy legacy revenue.

Why this matters: two learning companies can both have “USD 10m revenue” and be valued wildly differently depending on recurring revenue quality, procurement stickiness, gross margin profile, and how exposed they are to cyclicality (budgets, enrollment, regulation, platform shifts).

Buyers will always pressure-test a few sector-specific risks:

- Budget and procurement risk: long sales cycles, RFPs, delayed decisions, and “nice-to-have” cuts.

- Implementation and services drag: even “software” learning platforms can be services-heavy in delivery, onboarding, content migration, and support.

- Outcome and compliance exposure: if you touch grading, exams, credentialing, or data privacy, buyers will scrutinize reliability and compliance hard.

- Content rights and partnerships: content licensing terms, renewal rights, and the durability of distribution relationships.

- Platform dependency: reliance on app stores, search, third-party content, LTI integrations, or a single ecosystem partner.

2. What Buyers Look For in a Learning Platforms Business

At a simple level, buyers pay for three things:

- Durable revenue - customers keep paying and expand over time

- A credible path to profit - or profit today

- Strategic usefulness - the buyer can grow it faster inside their platform than you can alone

In learning platforms, the “durable revenue” test is more specific than in generic SaaS. Buyers will zoom in on:

- Recurring mix and renewal mechanics: subscription or contracted recurring revenue tends to be valued more than one-time content sales or project-based services.

- Customer stickiness: integrations into core workflows (rosters, gradebooks, ID systems, content distribution, assessments) make switching painful.

- Cohort health: do newer customer cohorts churn less? expand more? require less support?

- Gross margin quality: many learning platforms have content, services, or support costs that cap margins. Buyers pay up when margins are structurally strong or clearly improving.

They also care about where you sit in the learning stack:

- System of record vs add-on: if you are the workflow “hub” (or tied to it), you are harder to replace.

- Data and insights: analytics that actually change decisions (student success, retention, outcomes, compliance) are more valuable than dashboards nobody uses.

How private equity thinks about you

Private equity (PE) buyers typically ask: “If we buy at X, can we sell at a higher multiple in 3-7 years?”

They focus on:

- Entry multiple vs exit multiple: they want to buy at a reasonable price and sell to a larger buyer later (bigger PE fund, strategic acquirer, or public market).

- Repeatable levers:

- Pricing and packaging (especially seat-based and tiered plans)

- Expansion into adjacent modules (assessment, engagement, analytics, content)

- Professionalizing sales (pipeline discipline, segmentation, partner channels)

- Improving delivery efficiency (reducing services burden)

- Bolt-on acquisitions (smaller tools to widen the suite)

Your job in a sale is to make those levers feel realistic and already underway, not hypothetical.

3. Deep Dive: The Highest-Impact Valuation Nuance in Learning Platforms - “Stickiness” Is Not a Vibe

In learning, “stickiness” is the difference between a buyer underwriting your revenue as durable - or treating it like it could disappear after the first renewal cycle.

In the data you provided, public market revenue multiples for many learning platform models are often modest (frequently around ~0.3x-2.0x EV/Revenue for several categories), while certain private-market outcomes for software-like institutional tools can land in materially higher bands (for example, an “Institutional EdTech Software” band of ~3.1x-5.4x EV/Revenue appears in the private comps). The gap is largely a bet on stickiness and future profit.

Why buyers care so much:

- Learning buyers (districts, universities, enterprises) can be slow to buy - but once embedded, they can be slow to switch.

- Switching costs are real when you touch identity, rosters, content, grades, exams, or reporting.

- Conversely, if you are “a tool teachers like” but not operationally embedded, budget tightening can kill you quickly.

A practical way to think about it:

How to move right (in 6-12 months):

- Integrate into systems of record (SIS/LMS/HRIS/SSO) and make those integrations measurable.

- Instrument adoption: show activity by role (admin/teacher/student), weekly active usage, and feature penetration.

- Prove renewal drivers: tie retention to specific outcomes or workflow reliance (not “we have good relationships”).

- Reduce friction: onboarding time-to-value, implementation hours, support tickets per account.

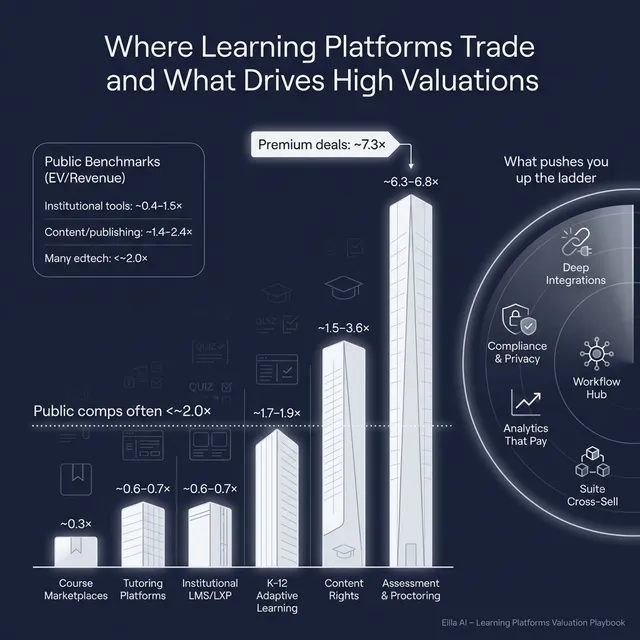

4. What Learning Platforms Businesses Sell For - and What Public Markets Show

The simplest truth: there is no single “learning platform multiple.” Multiples cluster by segment and by business quality.

The data you provided includes (1) precedent transactions with an overall average/median around 4.0x EV/Revenue and ~26.1x EV/EBITDA, and (2) segment-level ranges that swing widely. That spread is not noise - it reflects fundamentally different business models and risk profiles.

4.1 Private Market Deals (Similar Acquisitions)

Using the precedent transaction groupings in your sources, here are the headline patterns founders should take seriously (illustrative ranges, not a price tag):

A few important interpretations:

- Segment averages hide winners and losers. The K-12 and assessment categories show especially wide ranges in the underlying data, which usually means “quality matters a lot.”

- Services and distribution drag revenue multiples down. If revenue is not recurring or margin is structurally capped, buyers pay less per dollar of revenue.

- High-stakes workflows can command premiums. Assessment and compliance-related systems often have stronger “must-have” characteristics.

4.2 Public Companies

Public markets give you a reality check: what do investors pay for scaled learning businesses today?

From your dataset, many public learning-related companies trade at relatively modest EV/Revenue levels (often under ~2.0x), with exceptions and outliers. A few examples across categories in your list illustrate the spread:

- Some institutional platform and education software profiles cluster around ~0.4x-1.5x EV/Revenue.

- Publishing/content and some scaled education businesses can be around ~1.4x-2.4x EV/Revenue.

- There are notable higher-multiple outliers in certain regions or special situations, but your source explicitly flags these as less reliable anchors for valuation.

For founders, the right takeaway is not “public says I’m worth 0.8x.” It’s this:

- Public multiples are a reference band - an upper and lower guardrail.

- Private buyers often pay more than public comps when the asset is scarce, strategic, and has clear synergies.

- But buyers also haircut private valuations for smaller scale, concentration risk, weaker margins, and unclear retention.

If you are preparing for a sale, your goal is to build a story where buyers believe you deserve a private-market strategic outcome - not a “small public comp” discount.

5. What Drives High Valuations

Your sources include “premium valuation driver” groupings where higher-quality learning platform businesses can achieve meaningfully stronger EV/Revenue outcomes (for example, a premium band for “Higher-Ed and K-12 Learning Platforms (SaaS LMS and Analytics)” around 7.3x EV/Revenue, and “Institutional EdTech Software” around ~4.1x EV/Revenue median). The common thread is not the label - it’s the underlying buyer conviction.

Below are the premium drivers that consistently show up in higher-multiple outcomes, grouped into practical themes.

5.1 Mission-critical workflow position

Buyers pay more when your platform is tied to workflows that cannot break:

- Enrollment, rosters, identity, content access, assessment integrity, reporting, compliance.

- “If this goes down, the institution cannot operate normally.”

Practical examples:

- You are integrated into core systems and replacing you would require months of reconfiguration.

- You own a workflow that administrators are accountable for (not just a teacher-level tool).

5.2 Demonstrated analytics monetization (not just dashboards)

Your source example logic explicitly credits analytics monetization as a premium factor - but only when it is real and repeatable.

Buyers pay more when:

- Analytics are packaged and sold (tiered plans, modules, seat add-ons).

- Analytics change decisions and outcomes (retention, interventions, credential progress, compliance).

Practical examples:

- You can show that accounts using analytics renew at higher rates or expand faster.

- You have a clear “data product” roadmap tied to monetization.

5.3 Breadth that enables cross-sell (suite advantage)

A suite can be a premium driver when it reduces churn and increases expansion:

- Multiple modules that share data, workflows, and buyers.

- Land with one pain point, expand into adjacent needs.

Practical examples:

- Starting in content distribution, expanding into engagement, then analytics.

- Starting in scheduling/records, expanding into compliance and reporting.

5.4 Strong unit economics and improving margins

Premium multiples are hard to justify if your gross margins are structurally capped and EBITDA is deeply negative.

Buyers pay more when:

- Gross margin is strong (or clearly improving) and services are not the main profit engine.

- You can show a believable path to profitability without “heroic” assumptions.

Practical examples:

- Implementation is standardized and largely repeatable.

- Support costs per customer are shrinking as you scale.

5.5 High-quality revenue: recurring, contracted, and resilient

This is the classic driver, but in learning it has extra nuance:

- Multi-year contracts, predictable renewals, and expansion.

- Low exposure to one-time content spikes or seasonal volatility.

Practical examples:

- Multi-year district or institutional agreements with standard renewal cycles.

- A meaningful percentage of revenue that renews with minimal selling effort.

5.6 Clean fundamentals that reduce buyer fear

Even great learning products get discounted if diligence reveals chaos.

Buyers pay more when:

- Financials are clean and consistent.

- Customer concentration is manageable.

- Security/privacy posture is credible for your customer type.

- You have a leadership bench beyond the founder.

6. Discount Drivers (What Lowers Multiples)

Discounts happen when buyers sense that revenue is fragile, margins are structurally weak, or risk is hiding in the corners.

Based on the patterns implied in your sources (including the example logic emphasizing discounts for negative EBITDA and sub-55% gross margins), the biggest discount drivers in learning platforms are:

6.1 Weak profitability story (or no believable path)

- Persistently negative EBITDA with no clear plan to improve.

- Gross margins that suggest the business is “content/services dressed as software.”

What to do:

- Show margin improvements already happening, not promised.

- Separate software revenue from services revenue and show software margin clearly.

6.2 Low stickiness and unclear retention drivers

- Churn that spikes after initial contracts.

- Usage that looks good in demos but weak in real adoption.

What to do:

- Build renewal playbooks, adoption measurement, and proof of value.

- Tie product usage to renewal and expansion outcomes.

6.3 Services-heavy delivery and custom work

- Too much revenue depends on projects, customization, or founder-led relationships.

- Implementation requires large bespoke effort per customer.

What to do:

- Productize onboarding.

- Standardize integrations.

- Reduce the “hours per deployment” metric.

6.4 Concentration and procurement fragility

- One customer, one district, one country, or one channel drives too much revenue.

- Revenue depends on a single partnership or platform relationship.

What to do:

- Diversify pipeline.

- Build second and third channels.

- Document partner terms and renewal protections.

6.5 Compliance, security, and data risk

In learning, buyers fear reputational blow-ups:

- Privacy violations, insecure student data handling, weak security controls.

- Regulatory uncertainty in certain markets.

What to do:

- Make security and privacy diligence-ready.

- Have policies, audits, and incident response documented.

7. Valuation Example: A Learning Platforms Company

This is a worked example to show how valuation logic works in practice. The company and numbers below are fictional (including the USD 10m revenue figure), and the valuation range is illustrative - not investment advice or a formal valuation.

Step 1: The plain-English valuation logic

A buyer (or advisor) typically does this:

- Pick the right “reference sets”

- Public comps for a reality check (often lower, more conservative).

- Private precedent deals for what strategics/PE have actually paid.

- Choose a base multiple range

- In your sources, a conservative anchor for mixed learning software/content businesses often clusters around ~0.6x-1.5x EV/Revenue in public markets.

- Private-market outcomes for “Institutional EdTech Software” show a higher band (roughly ~3.1x-5.4x EV/Revenue in the data).

- The real question becomes: how much of that private “software band” do you deserve?

- Adjust up or down based on drivers

- Premiums for stickiness, analytics monetization, cross-sell suite, and credible path to profit.

- Discounts for negative EBITDA, weak gross margins, heavy services mix, and fragile retention.

- Sanity-check

- Does the result make sense versus both public comps and private comps?

- Is the story credible in diligence?

Step 2: Apply it to a fictional company

Meet Northbridge Learning, a fictional business:

- USD 10m revenue (fictional)

- Sells to higher-ed and vocational institutions

- Product: student engagement + content access + analytics module

- Revenue mix: mostly subscription, some implementation services

- Gross margin: mid-50s and improving

- EBITDA: slightly negative today, but improving due to reduced implementation hours per deployment

- Strength: cross-sell across modules, deep integrations with institutional systems

- Weakness: still proving long-term renewal expansion across cohorts

A simple way to frame valuation scenarios (illustrative):

Why the base case looks like that:

- It matches a logic pattern in your sources where a realistic private-market band for institutional software can land around ~3.0x-5.5x for a software-led learning platform, especially when cross-sell and analytics are present, even if profitability is not perfect yet.

What would push Northbridge toward the premium case:

- Strong evidence that renewals are durable (low churn, stable cohorts).

- Analytics is clearly monetized and driving retention/expansion.

- Gross margin keeps improving and EBITDA path is credible within 12-24 months.

What would push it into the discount case:

- Services become the hidden engine of revenue.

- Renewals rely on relationships rather than embedded workflows.

- No believable profitability path without cutting growth.

Step 3: What this means for you

Two learning platforms with the same revenue can be worth 2x apart because buyers are pricing confidence, not just today’s revenue.

If you want a higher multiple, your goal is to make the buyer’s job easy:

- “This revenue will stick.”

- “Margins will improve predictably.”

- “This platform is strategically valuable in a portfolio.”

8. Where Your Business Might Fit (Self-Assessment Framework)

This is a quick self-check to estimate whether you are closer to the low, mid, or high end of your segment’s valuation range.

Score each factor 0 / 1 / 2:

- 0 = weak or unclear today

- 1 = decent but inconsistent

- 2 = strong and provable in data

How to interpret your total (very roughly):

- High scores: you are more likely to be valued toward premium private-market outcomes in your segment.

- Middle scores: you can still sell well, but expect buyers to negotiate hard around risk.

- Low scores: you may still exit, but you should consider a 6-12 month “value build” plan before running a process.

The point is not the number. The point is identifying the 2-3 improvements that will change buyer conviction the most.

9. Common Mistakes That Could Reduce Valuation

These are avoidable - and expensive.

9.1 Rushing the sale

If you sprint into market without clean numbers and a clear story, buyers will:

- assume risk

- demand discounts

- slow-roll you in diligence

A good process is built, not improvised.

9.2 Hiding problems

In a sale, issues always surface: churn pockets, implementation pain, customer disputes, security gaps.

If buyers discover surprises late:

- trust breaks

- value drops

- deals die

Owning problems early usually protects value.

9.3 Weak financial records

Learning platforms often have messy revenue classification (software vs services vs content), inconsistent margin reporting, and unclear cohort behavior.

Fixable, high-ROI improvements:

- Separate software revenue from services and content clearly.

- Track gross margin by product line.

- Build a simple KPI pack: retention, churn, expansion, adoption.

9.4 No structured, competitive process with an advisor

Founders often underestimate how much process design drives price.

Research and market evidence commonly show that running a structured, competitive process with an advisor can lead to meaningfully higher purchase prices - often cited around 25% - because you create competition and control narrative.

9.5 Revealing your price too early

If you tell buyers “I’m looking for USD 10m,” you kill price discovery.

Buyers will cluster offers just above your number (USD 10.1m, 10.2m) instead of showing what they would actually pay in a competitive process.

9.6 Learning-platform-specific mistakes

- Not being diligence-ready on data privacy/security (especially with student data). Even small gaps can spook serious buyers.

- Letting implementation become bespoke. Custom work can quietly turn a “platform” into a services company, and multiples follow that reality.

10. What Learning Platforms Founders Can Do in 6-12 Months to Increase Valuation

You do not need a massive reinvention. You need targeted moves that improve buyer confidence.

10.1 Improve the numbers buyers actually pay for

- Increase recurring mix: shift one-time revenue into subscriptions where possible.

- Reduce services drag: productize onboarding, standardize integrations, and measure implementation hours per deployment.

- Show gross margin improvement: even a few points of margin expansion, clearly explained, changes underwriting.

- Build a credible EBITDA path: not “we’ll cut costs after the sale,” but “here is what already changed and the next steps.”

10.2 Prove stickiness with evidence (not opinions)

- Build a renewal dashboard: logo retention, net retention (are customers spending more), cohort trends.

- Track adoption by role and by feature: admin usage, teacher usage, student usage.

- Tie adoption and outcomes to renewals: “accounts with X adoption renew at Y%.”

10.3 Make analytics and cross-sell real

If analytics and breadth are part of your story, treat them like products:

- Package analytics into tiers.

- Track attach rates and expansion revenue.

- Create simple case studies showing impact on decisions/outcomes.

10.4 De-risk the business for a buyer

- Reduce customer concentration if possible (or at least build pipeline depth to show it is declining).

- Document security/privacy posture: policies, controls, incident process, compliance artifacts.

- Strengthen leadership bench: buyers pay more when the business is not “founder-or-nothing.”

10.5 Prepare for a buyer’s diligence process

- Clean up revenue classification (software vs services vs content).

- Build a consistent monthly reporting rhythm.

- Create a simple data room structure early (contracts, KPIs, financials, product docs, security).

11. How an AI-Native M&A Advisor Helps

Most founders underestimate how much buyer reach and process quality drive valuation. The best outcome usually comes from getting the right story in front of the right buyers - and creating real competition.

An AI-native approach expands your buyer universe dramatically. Instead of relying on a short list of “who we know,” AI can map hundreds of qualified acquirers based on deal history, product adjacency, synergy signals, and capacity to do a deal. More relevant buyers creates more competitive tension - and gives you backup options if one buyer drops out.

AI also compresses timelines. With AI-driven buyer matching and faster creation of marketing materials and diligence support, it becomes realistic to reach initial conversations and offers in under 6 weeks, rather than dragging into a multi-month crawl.

Finally, you still want expert humans running the process. The strongest model is senior M&A advisors (who know how buyers think and how to negotiate) enhanced by AI for speed, coverage, and execution. The result is Wall Street-grade process quality without traditional bulge bracket costs.

If you’d like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.