The Complete Valuation Playbook for Legal Tech Businesses

A data-driven guide to how Legal Tech businesses are valued today and what drives high multiples.

If you are a Legal Tech founder thinking about a sale in the next 1-12 months, valuation is not just a number - it is a story the market believes. And in Legal Tech right now, buyers are paying very different prices for businesses that look similar on the surface.

This playbook is built from what the data actually shows in Legal Tech deals and public comps, plus how strategic buyers and private equity (PE) teams really underwrite risk in this sector. You will see what Legal Tech businesses sell for, what drives higher vs lower multiples, a worked example on a fictional USD 10m revenue company, and a practical self-assessment + action plan.

1. What Makes Legal Tech Unique

Legal Tech is not one industry - it is a set of product categories that sit in very different parts of the legal workflow. Buyers value each category differently because the underlying “stickiness” (how hard you are to replace), customer budgets, and risk profile are different.

The main Legal Tech business types you see in the market:

- Law firm workflow and drafting software - document drafting, clause libraries, knowledge management, practice workflow, Word-based tools.

- Corporate legal ops platforms - e-billing, matter management, spend management, vendor management, budgeting and accruals.

- Research and information platforms - legal research, regulatory content, tax and compliance knowledge products.

- eDiscovery and legal data processing - collect, process, review, and analyze litigation data at scale.

- Agreement and content management adjacencies - e-signature, contract lifecycle management (CLM), enterprise content/document management.

- Tech-enabled services - translation, managed review, and other services supported by software.

Why valuation is different here than in “generic SaaS”:

- Trust and risk tolerance are unusually high bars. Legal work carries privilege, confidentiality, regulatory risk, and reputational exposure. Buyers discount anything that looks unsafe or unreliable, even if growth is good.

- Workflow embed matters more than features. In Legal Tech, the highest outcomes show up when your product becomes part of the system people run daily work through (approvals, spend controls, matter records), not a tool they “sometimes” use.

- Procurement cycles can be slow - but retention can be fantastic. That creates a valuation split: buyers pay up for proven enterprise adoption, and discount “promising but early” adoption heavily.

- AI creates both tailwinds and landmines. AI can expand product value fast, but it also raises buyer questions around data rights, model risk, hallucinations, and defensibility.

Key risk factors buyers will always check (and price accordingly):

- Data security posture (SOC 2/ISO, audit trails, access controls), and how you handle client confidential data.

- Accuracy and reliability of AI outputs, plus legal disclaimers and human-in-the-loop design.

- Customer concentration (one big firm or one big corporate legal department can make your revenue fragile).

- Evidence of “stickiness”: renewals, expansion, usage, and integrations that make switching painful.

- Services dependency (implementation, customization, managed work) that caps margins and scalability.

2. What Buyers Look For in a Legal Tech Business

Most buyers - strategic acquirers and PE - start with the basics, then quickly move to Legal Tech specifics.

The obvious stuff still matters

- Scale and growth: faster growth expands the buyer pool and supports higher multiples.

- Recurring revenue: buyers pay more when most revenue repeats automatically (subscriptions) vs being “re-sold” every year.

- Gross margin: software-like margins signal scalability. Services-heavy revenue usually lowers multiples.

- Retention: if customers renew and expand over time, buyers underwrite a longer payback and pay more.

Legal Tech nuances buyers care about

- Who pays and why: budgets are different for law firms vs in-house legal teams vs compliance buyers. Corporate legal ops budgets can be more “operational and durable” than innovation budgets.

- Where you sit in the workflow: tools that control spend, approvals, matter data, signing, or compliance gates tend to be more “must-have” than tools that only accelerate drafting.

- Integration footprint: if you plug into DMS, practice management, billing, identity, e-signature, and collaboration tools, you become harder to replace.

- Defensibility in an AI world: buyers want to know what you have that a big platform cannot copy quickly - proprietary datasets, workflow data, distribution, integrations, domain tuning, or compliance-grade architecture.

How PE buyers think (in plain English)

PE usually asks: “If we buy at X, can we sell at a higher multiple later?”

- Entry multiple vs exit multiple: They care about what they pay now, and what a future buyer might pay in 3-7 years.

- Who they can sell to later: A larger PE fund, a strategic consolidator (big legal publisher, enterprise software platform), or occasionally the public markets.

- The levers they expect to pull:

- Price increases (if you have strong ROI and low churn)

- Cross-sell to adjacent buyer portfolios

- Reduce services burden and improve gross margin

- Improve sales efficiency and repeatability

- Add bolt-ons (small acquisitions) if the category lends itself to consolidation

If your business cannot credibly support those levers - or if revenue is “lumpy” and services-heavy - PE interest and valuation usually fall.

3. Deep Dive: Workflow Embed vs “Nice-to-Have” AI - The Biggest Multiple Split in Legal Tech

In Legal Tech, the single most important valuation question is often:

Are you embedded in a mission-critical workflow, or are you a productivity add-on?

This matters because buyers are not just buying revenue - they are buying how hard you are to replace.

In the deal data, the clearest premium example is a corporate legal ops platform deeply embedded in legal department spend workflows (e-billing, budgeting, accruals, vendor management). That level of embed showed up in a very high revenue multiple despite negative EBITDA, because it behaves like a system-of-record with high switching costs. Another example shows a premium for regulated KYC/AML signing workflows, where compliance creates “must-have” retention. These patterns are exactly what strategic buyers pay for - durable workflows, not novelty.

Why buyers pay more for workflow embed

- Lower churn risk: when your product is intertwined with approvals, billing, and record-keeping, replacing you is painful.

- Higher pricing power: if you govern spend or compliance, you can raise prices without losing customers.

- More expansion paths: embedded platforms can sell more seats, more matters, more modules, and more enterprise-wide adoption.

How to move from “tool” to “workflow anchor”

You do not need to rebuild your product. You usually need to move one level deeper into the operating system of legal work:

- Add structured approval flows, policy enforcement, and audit trails.

- Integrate into the systems customers already live in (DMS, billing, identity, e-signature, Microsoft ecosystem).

- Become the place where legal teams track work status, risk, and decisions - not just generate drafts.

Lower-value profile vs higher-value profile

If you recognize yourself on the left, your goal in the next 6-12 months is not “more AI.” It is more workflow ownership.

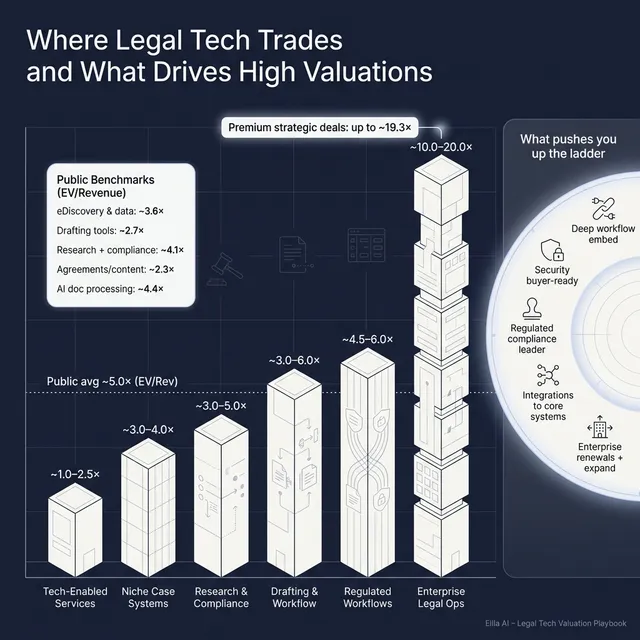

4. What Legal Tech Businesses Sell For - and What Public Markets Show

This section is intentionally factual: private deal multiples set the real-world clearing prices, and public comps set the reference band buyers use to sanity-check what they pay.

4.1 Private Market Deals (Similar Acquisitions)

From the precedent deals provided, Legal Tech software outcomes span a wide range. A key point: the highest private multiple in the data is not explained by profitability - it is explained by enterprise workflow embed and strategic fit.

- AI-enabled legal ops / workflow platforms can see very high revenue multiples when they are deeply embedded and strategic to a consolidator’s suite (example shown at ~19.3x revenue even with negative EBITDA).

- Regulated workflow platforms (like signing + KYC for AML-regulated onboarding) show solid but more “platform-normal” multiples (example around ~5.5x revenue).

- Smaller niche workflow systems serving public sector or specialized case management can transact in the low single-digit revenue multiple range (example around ~3.2x revenue).

Here is a founder-friendly way to think about the private ranges implied by the deal set:

These are illustrative, not promises. The same “category” can trade very differently based on growth, retention, customer concentration, and how strategic you are to a specific acquirer.

4.2 Public Companies

Public markets provide a reality check and a starting reference point. The grouped public multiples in the data show (as of mid-to-late 2025) that Legal Tech-adjacent software clusters generally trade around ~5.0x EV/Revenue overall and ~21.5x EV/EBITDA overall, but segment differences matter.

Public group averages from the data:

How to use public multiples (correctly)

- Treat public comps as reference rails, not a price tag.

- Private businesses usually trade at a discount to public multiples for smaller scale, less liquidity, and higher customer concentration risk.

- But private businesses can trade at a premium when they are scarce strategic assets (for example: a system-of-record legal ops platform that a consolidator needs now).

Your job is to help buyers justify where you sit relative to those rails.

5. What Drives High Valuations (Premium Valuation Drivers)

Based on the deal patterns and buyer behavior, premium outcomes in Legal Tech usually come from a few repeating themes.

5.1 Deep workflow embed creates switching costs

When your product runs legal operations (billing, budgeting, approvals, matter financials), buyers see durability. One deal in the data paid a very high revenue multiple despite negative EBITDA because the product was deeply embedded in enterprise legal ops workflows and behaved like a system-of-record.

Practical examples:

- You control invoice approval workflows and outside counsel budgets.

- You are where matters are tracked and reported, not just a reporting layer.

- You own audit trails and policy enforcement.

5.2 Strategic fit with consolidators and distribution machines

Large information-services and legal publishing platforms pay up when your product extends their suite into adjacent workflows they can cross-sell. The premium is not just your standalone revenue - it is your impact on their installed base.

Practical examples:

- You can show pilots or co-sell motions with a larger platform.

- Your product increases average revenue per customer inside an acquirer’s base.

- Your integrations make you “native” to their ecosystem.

5.3 Category leadership in regulated workflows

Regulated workflows create “must-have” retention and pricing power. In the data, a regulated signing + KYC workflow business with strong gross margins was acquired at a solid revenue multiple, reflecting compliance-driven stickiness.

Practical examples:

- You provide jurisdiction-specific compliance checks and auditable outputs.

- You offer policy gates and approvals that legal teams must follow.

- You can pass security reviews quickly and repeatedly.

5.4 Platform feel: modular product + ecosystem extensibility

Buyers pay more when they believe you are a platform, not a point solution. This does not require being huge - it requires a modular roadmap and ecosystem connectors.

Practical examples:

- A clear module path: intake -> analysis -> drafting -> negotiation -> post-sign monitoring.

- Connectors to Microsoft, DMS, practice management, CLM, billing.

- Partner ecosystem or marketplace motion, even early.

5.5 Rapid growth with improving profitability trajectory

In enterprise Legal Tech, buyers can tolerate negative EBITDA if growth is strong and losses are shrinking. The premium deal example in the data explicitly showed improving EBITDA trajectory alongside fast revenue growth.

Practical examples:

- Cohort retention is strong and expansion is real.

- Gross margin is high and trending up.

- Services are shrinking as a percent of revenue.

5.6 “Boring but important” trust builders

These are not glamorous, but they move deals:

- Clean financials and clear revenue recognition.

- Predictable renewals and renewal process discipline.

- A leadership bench beyond the founder.

- Low customer concentration and credible pipeline.

6. Discount Drivers (What Lowers Multiples)

Discounts happen when buyers see risk, volatility, or lack of proof. In Legal Tech, a few discounts are especially common.

6.1 You are a “tool,” not a workflow anchor

If customers use you occasionally, or your value is “nice-to-have,” buyers underwrite churn risk and price you lower.

What to improve:

- Build deeper workflow ownership (approvals, records, compliance gates).

- Move from “document creation” to “matter process control.”

6.2 Services-heavy revenue mix

If implementation, customization, or managed work is a large share of revenue, buyers assume:

- Lower gross margin

- Harder scaling

- Harder to transfer relationships post-acquisition

What to improve:

- Productize onboarding and implementation.

- Separate services revenue clearly and show a path to reducing it.

6.3 Weak proof of retention and expansion

Legal Tech buyers want evidence customers stick and expand. Without it, they discount growth as “fragile.”

What to improve:

- Track renewals, churn, net retention (do customers spend more over time?).

- Show usage data that correlates with renewals.

6.4 Customer concentration and “founder-dependent” revenue

A few big customers can make revenue look strong, but fragile. Same for founder-led sales.

What to improve:

- Add a sales leader or repeatable process.

- Diversify across customer segments, industries, or geographies.

6.5 AI risk and IP uncertainty

AI-native Legal Tech gets diligence scrutiny:

- Data rights (can you use customer data to train?)

- Security controls and model governance

- Accuracy and liability risk

What to improve:

- Document your data policies and model governance.

- Make security posture auditable and buyer-ready.

7. Valuation Example: A Legal Tech Company

This is a worked example designed to show the logic - not a formal valuation or investment advice.

Step 1: The valuation logic (plain English)

A practical way to value a privately held Legal Tech business is to “triangulate”:

- Start with public comps in the closest product clusters and take a conservative core band.

- Cross-check with private deal outcomes to understand what premiums are possible when strategic fit and workflow embed exist.

- Adjust up or down based on the premium and discount drivers: stickiness, growth, margins, services mix, and risk.

In the provided logic example, a sensible base band for an AI-enabled legal software platform without proven system-of-record embed was ~3.0x-5.0x revenue, with upside to ~6.0x when the story supports stronger buyer conviction.

Step 2: Apply it to a fictional company (USD 10m revenue)

Meet LexHarbor (fictional). LexHarbor sells an AI-assisted drafting and review product used inside Microsoft Word, plus light workflow features for approvals and clause libraries.

Assumptions (fictional):

- USD 10m last-twelve-month revenue, mostly subscription

- Some enterprise customers, but not yet fully embedded in legal ops systems

- High gross margin, limited services

- Good early retention, but expansion proof is mixed

Now apply the multiples:

Step 3: What this means for you

Two Legal Tech companies can both be at USD 10m revenue and still sell for dramatically different prices. The difference is rarely “better AI.” It is:

- how embedded you are,

- how predictable your renewals are,

- and whether buyers believe you can become a durable workflow platform.

If you want to move up the range, your roadmap and go-to-market should be designed to prove those things fast.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as a simple, honest internal tool. Score each factor 0 / 1 / 2:

- 0 = weak or unproven

- 1 = decent but inconsistent

- 2 = strong and well-documented

Self-assessment table

How to interpret your score (roughly)

- High score: you look like a premium asset - likely to attract strategics and top-tier PE.

- Middle score: you can still get a good outcome, but you need a crisp narrative and a competitive process.

- Low score: you may still sell, but expect lower multiples unless you fix a few big items first (often retention proof, concentration, or services mix).

The point is not perfection. The point is identifying the 2-3 improvements that move valuation the most.

9. Common Mistakes That Could Reduce Valuation

9.1 Rushing the sale

If you start a process before your numbers, story, and buyer list are ready, you usually get:

- fewer buyers engaged,

- weaker offers,

- and more re-trading later (buyers lowering price after diligence).

9.2 Hiding problems

Problems always surface in diligence. Hiding them destroys trust, increases legal risk, and gives buyers leverage to cut price.

Better approach:

- disclose issues early, with a remediation plan and evidence of progress.

9.3 Weak financial records

Many founders underestimate how much valuation is a “confidence game.” If your financials are messy, buyers assume other things are messy too.

Low-hanging improvements in 6-12 months:

- clean revenue recognition,

- clear separation of software vs services revenue,

- consistent KPI reporting (retention, churn, bookings, backlog),

- customer-level profitability visibility where possible.

9.4 No structured, competitive sale process

A structured competitive process is one of the few reliable ways to increase purchase price. Research often cited in M&A indicates that running a structured process with an advisor can drive meaningfully higher outcomes - commonly referenced around 25% higher purchase prices versus single-buyer negotiations.

9.5 Revealing your target price too early

If you tell buyers “we want USD 10m,” you usually get bids like USD 10.1m and USD 10.2m - not the real price they might have paid in competition. You kill price discovery.

9.6 Legal Tech-specific mistake: treating security as a checkbox

In Legal Tech, security posture is part of product quality. Weak security slows diligence, limits the buyer pool, and invites price cuts.

9.7 Legal Tech-specific mistake: selling “AI magic” instead of hard workflow ROI

Buyers pay for measurable outcomes: reduced spend leakage, faster cycle times, fewer outside counsel hours, better compliance. If your story is vague, buyers discount it.

10. What Legal Tech Founders Can Do in 6-12 Months to Increase Valuation

Think in three tracks: improve the numbers, reduce risk, and sharpen the narrative.

10.1 Improve the numbers buyers pay for

- Increase recurring revenue share: convert services or usage to subscription where realistic.

- Prove retention and expansion: create renewal discipline, track cohorts, and show customers paying more over time.

- Reduce services drag: productize onboarding, standardize integrations, and separate services reporting clearly.

- Show improving profitability trajectory: even if EBITDA is negative, demonstrate improving trend and gross margin strength.

10.2 Move deeper into workflow embed

- Add approvals, policy enforcement, matter-level tracking, audit trails.

- Build 3-5 integrations that customers actually use daily (not a long list of “possible” integrations).

- If you serve in-house teams, deepen into legal ops workflows: spend controls, vendor management, matter dashboards.

This directly aligns with premium patterns in the deal data where deep embed drove outsized outcomes.

10.3 Reduce buyer fear around AI and data

- Put your data rights, retention, and training policy in writing.

- Build a governance approach: accuracy testing, human review paths, logging, auditability.

- Make security buyer-ready: SOC 2/ISO progress, pen tests, access controls, incident response.

10.4 Tighten the sale narrative

- Define your category clearly (what you replace, why you win).

- Show ROI with real customer evidence (case studies, quantified outcomes, renewal behavior).

- Map strategic buyer fit: who benefits most, and how they can cross-sell you.

11. How an AI-Native M&A Advisor Helps

Selling a Legal Tech business is not just about finding “a buyer.” It is about finding the right buyers - the ones for whom your product is strategically urgent - and running a process that creates competition.

Higher valuations through broader buyer reach. AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, synergies, financial capacity, and other signals. More relevant buyers means more competition, stronger offers, and more options if one buyer drops out - which increases the chance the deal actually closes.

Initial offers in under 6 weeks. AI-driven buyer matching and connecting, faster creation of process materials, and structured diligence support can compress timelines dramatically compared to manual-only outreach - helping you reach real conversations and initial offers much faster.

Expert advisory, enhanced by AI. The best outcomes still require experienced human advisors who can shape the story, manage buyers, and negotiate terms. The AI advantage is leverage: faster analysis, stronger positioning, and better process discipline - with “Wall Street-grade” materials and credibility, without traditional bulge bracket costs.

If you would like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.