The Complete Valuation Playbook for Legal Tech Businesses

A practical guide to how Legal Tech companies are valued today and what drives premium multiples.

If you are a founder or CEO of a Legal Tech business thinking about a sale in the next 1-12 months, valuation is not just about growth. It is about how a buyer sees the durability of your revenue, how deeply your product sits inside legal workflows, and how much risk they believe they are taking on.

That matters more right now because Legal Tech is being pulled in two directions at once. On one side, buyers want software that reduces legal labor, supports compliance, and becomes part of daily workflow. On the other, they are more disciplined than they were a few years ago about paying premium multiples for tools that feel replaceable, services-heavy, or loosely positioned.

This playbook is built to help you make sense of that. It shows what Legal Tech businesses actually sell for, explains what pushes valuations up or down, gives you a practical way to assess where your company sits today, and lays out what you can do in the next 6-12 months to improve the outcome.

1. What Makes Legal Tech Unique

Legal Tech is not one single category. It includes law-firm workflow software, document drafting and review tools, eDiscovery and litigation platforms, legal research and regulatory content businesses, contract and agreement tools, secure collaboration and data room platforms, and adjacent legal services models. Buyers do not value all of those the same way.

What makes Legal Tech different is that the best products sit inside high-stakes workflows. If your product touches document creation, transaction execution, litigation review, board governance, diligence, or compliance, mistakes are costly for the customer. That usually leads to lower churn, stronger pricing power, and more buyer interest than a general productivity tool with similar features.

Business model matters a lot here. Buyers will separate recurring software revenue from services revenue very quickly. A business with subscription revenue, high gross margins, strong renewal rates, and low implementation burden will usually command a better multiple than one with the same revenue but a heavier mix of custom work, managed services, or one-off project fees.

Customer type also changes valuation. Law firms, in-house legal teams, compliance teams, financial institutions, and regulated enterprises all buy differently. Enterprise customers can support larger contracts and better retention, but they also create longer sales cycles and higher diligence requirements. SMB-focused businesses can grow faster, but buyers may worry more about churn and competitive pressure.

There are also Legal Tech-specific risks buyers always examine. They will look at data security, privilege and confidentiality handling, AI reliability, integration into systems like Microsoft, iManage, NetDocuments or CLM stacks, customer concentration, and whether your product is genuinely embedded in workflow or simply used by a few champions.

2. What Buyers Look For in a Legal Tech Business

At the most basic level, buyers care about scale, growth, margins, and predictability. A business growing well with recurring revenue and healthy margins is easier to underwrite than a flat business with lumpy project work. But in Legal Tech, those basics are only the start.

Buyers also want to know how essential your product is. If customers use you every day to draft, review, collaborate, manage evidence, run diligence, or satisfy compliance requirements, that is a very different value story from a tool used occasionally for convenience. The more your software becomes part of the operating system of legal work, the more valuable it tends to be.

They will also test how sticky your customer base really is. Do customers renew because your product is deeply embedded, or because switching has simply not risen to the top of the list yet? Are you winning budget from mission-critical spend, or from innovation budgets that can disappear quickly? Buyers pay more for businesses that can answer those questions with evidence.

Product breadth matters too, but only when it is coherent. A buyer likes a platform that covers several connected steps in a workflow - for example drafting, collaboration, approval, deal room, audit trail, and secure sharing. They do not like a pile of unrelated features with weak adoption.

How private equity buyers think

Private equity buyers care about your entry price, but they care just as much about their exit path. They are asking: if we buy this business now, who will want it in 3-7 years? That next buyer could be a larger software platform, a strategic acquirer in legal or compliance, another private equity firm, or in rare cases the public market.

They also think in terms of levers. Can they increase prices without breaking retention? Can they cross-sell into a broader customer base? Can they improve sales efficiency, reduce services dependency, or complete add-on acquisitions around the core platform? If those levers are visible, your business becomes more attractive even before they are fully pulled.

Private equity also cares about whether your multiple today can still make sense later. If they pay a healthy multiple for a Legal Tech business, they need confidence that the company can grow into it through stronger revenue, better margins, and a clearer strategic position by the time they sell.

3. Deep Dive: Is Your Product Infrastructure - or Just a Tool?

One of the biggest valuation questions in Legal Tech is simple: does your product feel like infrastructure inside a legal workflow, or does it feel like a useful but replaceable tool? The data strongly suggests this distinction matters.

In the transaction set, the strongest EBITDA outcomes show up in businesses sitting inside regulated, high-cost-of-failure workflows like governance, board processes, due diligence, and compliance. That pattern tells you buyers are willing to pay more for earnings when they believe revenue is durable and the product has real pricing power. By contrast, more generic document and workflow businesses often settle into lower revenue multiples.

Why do buyers care so much about this? Because infrastructure-like products are harder to rip out. They tend to sit on sensitive data, become part of process controls, connect into several systems, and matter to multiple stakeholders. That lowers churn risk and raises strategic value. A point solution may still grow well, but it is easier for a buyer to imagine competitive pressure, budget cuts, or replacement.

Security and compliance proof is part of the same story. In Legal Tech, strong certifications and defensible controls are not just nice badges. They can shorten procurement, reduce buyer diligence anxiety, and open larger enterprise accounts. That is especially important if you sell into law firms handling sensitive matters, regulated companies, or board-level workflows.

If your business looks more like a tool today, the goal is not to reinvent the company overnight. The goal is to prove deeper workflow importance. That can mean showing high user dependence, stronger renewal behavior, more embedded integrations, cleaner compliance proof, and better evidence that your product drives part of the customer's core operating process.

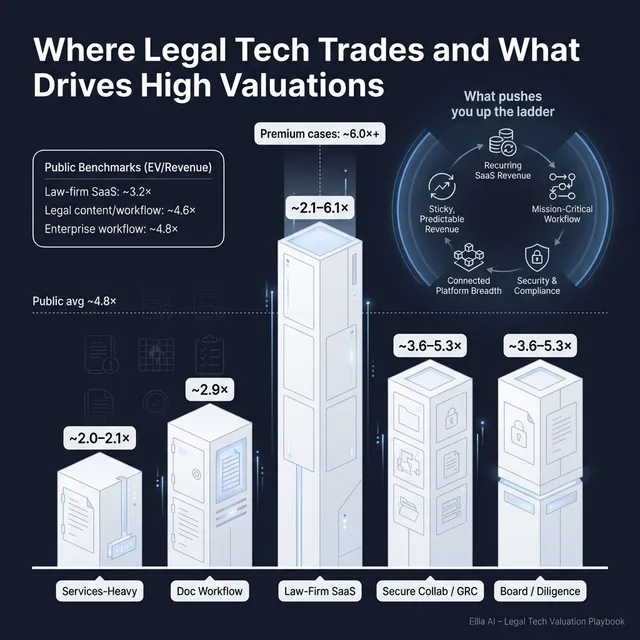

4. What Legal Tech Businesses Sell For - and What Public Markets Show

The data shows a wide valuation spread across Legal Tech and adjacent workflow software. That is normal. Buyers are not paying one category multiple for all businesses called "Legal Tech." They are paying based on business model quality, workflow criticality, customer stickiness, and how strategic the asset feels in a broader platform.

At a high level, the private transaction set is lower than the public market set, which is exactly what you would expect. Public companies have more scale, more liquidity, broader investor visibility, and often stronger balance sheets. Private companies usually trade at a discount unless they are scarce, highly strategic assets.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions provided, the overall average private EV/Revenue multiple is about 2.9x and the median is about 2.1x. On EV/EBITDA, the average is about 9.3x and the median is about 9.2x. That is the broad backdrop, but the mix matters.

The more attractive private outcomes tend to appear in secure collaboration, governance, diligence, and compliance-oriented software - especially where the business has strong margins and sits in a mission-critical workflow. More services-led and non-software-heavy models tend to cluster lower. Small capability acquisitions can sometimes price higher on revenue, but those are not the right benchmark for most founder-owned businesses preparing for sale.

These ranges are illustrative, not automatic. A sub-USD 10m revenue business with high gross margin, strong retention, and clear strategic fit can outperform the average. A larger business with weak positioning, heavy services, or customer concentration can still land near the low end.

4.2 Public Companies

The public company set provides a broader reference band. Across the full sample, the overall average EV/Revenue is about 4.8x and the median is about 3.4x. Average EV/EBITDA is about 24.4x and the median is about 18.9x. This snapshot reflects public trading levels around mid-to-late 2025.

Within that, law-firm-focused Legal Tech and legal workflow software trades around the low-to-mid 3x revenue range on average in this set, though outcomes vary widely depending on growth and profitability. Legal and regulatory information platforms trade higher on average because they often combine mission-critical content, strong renewal patterns, and durable margins. Adjacent enterprise workflow and automation platforms can trade at even richer levels, but those are usually larger and broader businesses, so they should be treated as directional reference points rather than direct comps.

*Approximate averages based on the available public sample.

Here is the practical takeaway. Public multiples are not your sale price. They are a reference band. Buyers will usually adjust them downward for smaller scale, lower growth, customer concentration, weaker margins, and private-company illiquidity.

That said, public comps still matter because they shape buyer psychology. If your business looks like a smaller version of a durable public workflow platform, that can support a stronger valuation narrative. And in some cases, a scarce private asset with strategic importance can trade above what a simple public-to-private discount would suggest.

5. What Drives High Valuations (Premium Valuation Drivers)

The data points to a clear idea: buyers pay up when they believe your revenue is durable, your product is hard to replace, and your earnings quality is real. In Legal Tech, that usually shows up through a handful of recurring themes.

Mission-critical workflow position

Businesses embedded in workflows where failure is costly tend to get better valuation outcomes. That includes board processes, diligence, governance, compliance, litigation review, and core drafting or transaction workflows. Buyers pay more because these products are harder to cut from budget and harder to replace.

For founders, this means your story should not be "we help legal teams work better." It should be "we sit inside a process the client cannot afford to get wrong."

Breadth across connected workflows

A broader platform can command more value when the modules are truly connected. Buyers like businesses that can expand from one use case into adjacent tasks in the same workflow because that raises wallet share and strengthens retention.

For example, it is more valuable to cover secure collaboration, approvals, due diligence, and auditability in one connected experience than to offer a few disconnected productivity features. The key is real adoption, not a long feature list.

Security and compliance proof

In Legal Tech, security posture is often a buying requirement, not a marketing extra. Clear certifications, strong controls, documented governance, and evidence of secure handling of confidential data can reduce friction in procurement and lower perceived risk in diligence.

This matters even more if you sell to Am Law firms, financial institutions, listed companies, or regulated enterprises. A buyer will pay more for a business that already clears those gates.

Strong software economics

High gross margin and healthy EBITDA margins tell buyers that your business is truly software-led rather than software wrapped around expensive services. In the data, some of the most attractive EBITDA outcomes come from businesses with strong margin profiles even at modest scale.

For a founder, that means buyers care about the shape of your revenue, not just the size of it. Two companies at the same revenue can be valued very differently if one converts revenue into cash earnings much more cleanly.

Clear strategic fit for specific buyers

Premium outcomes often happen when the buyer can immediately see how your business fits into their platform. That could mean cross-selling your product into their installed base, filling a workflow gap, strengthening a compliance offering, or deepening relationships with legal or regulated customers.

Founders often undersell this. You are not only selling a company. You are selling a reason why a specific buyer should care now.

Predictable revenue and low customer regret

Premium buyers like evidence that customers stay, expand, and rely on the product over time. Strong logo retention, good net revenue retention, multi-year contracts, usage depth, and expansion into more teams or matters all support that.

In simple terms, buyers care about whether your customers stick around and pay more over time. That is one of the cleanest signs that your product matters.

Clean operation and leadership readiness

Not every premium driver is sector-specific. Clean financial reporting, clear monthly KPIs, a strong second layer of management, low founder dependence, and a believable growth plan all increase buyer confidence. Buyers pay more when they feel they are stepping into a controlled business rather than a heroic founder story that depends on one person.

6. Discount Drivers (What Lowers Multiples)

The low end of the market usually comes from a handful of predictable problems. None of them are fatal on their own, but together they can drag a business well below the headline ranges founders hear about.

The biggest discount driver is weak positioning. If your product looks like generic document tooling, a narrow point solution, or an add-on that is nice to have rather than essential, buyers will not underwrite premium durability. The multiple falls because the revenue feels easier to replace.

A heavy services mix is another common issue. If implementation, support, managed review, or custom work makes up too much of the revenue, buyers start to question whether they are buying software economics or people-heavy delivery. That usually lowers both the revenue multiple and the earnings multiple.

Low quality retention also hurts. High churn, short contracts, low product usage, or expansion that depends only on new sales rather than existing customers signals that your revenue may not be durable. Buyers will often react more strongly to this than founders expect.

Security, compliance, and AI risk can also lower value quickly. If you sell into sensitive legal workflows but cannot clearly explain your controls, model governance, hallucination safeguards, or data handling posture, buyers see future customer risk and diligence risk at the same time.

Customer concentration matters too. A few large customers can look attractive until a buyer asks what happens if one leaves. The same goes for channel dependence, founder-led sales dependence, or one key integration partner driving too much of the business.

Finally, messy reporting is a valuation killer. If you cannot cleanly separate recurring revenue from services, show cohort behavior, track margin by revenue type, or explain why revenue converted into EBITDA the way it did, buyers will assume the risk is higher than it may actually be.

7. Valuation Example: A Legal Tech Company

Let’s turn the data into a practical example. The company below is fictional. The revenue number is fictional. The valuation range is illustrative only. It is meant to show how valuation logic works, not to provide investment advice or a formal valuation.

The setup

Assume a fictional company called LexBridge. It sells document collaboration and drafting workflow software to mid-sized and large law firms. It has USD 10m of annual revenue, mostly subscription-based, with good gross margins and moderate profitability. It is not an early-stage startup, so no startup premium is applied.

The comps-based logic from the data points to a core EV/Revenue range of roughly 2.6x to 5.0x on USD 10m of revenue for a mature Legal Tech business anchored to law-firm-focused LegalTech SaaS and content/document collaboration benchmarks. That implies an enterprise value range of roughly USD 26m to USD 50m.

Step 1: How the logic works

First, you start with the most relevant private and public reference points. In this case, that means law-firm workflow software, legal document collaboration, and adjacent content/document platforms.

Second, you narrow the range based on company quality. If the business has decent recurring revenue and reasonable product-market fit but lacks strong premium drivers, you stay inside that core band. If it has several strong premium drivers - such as excellent retention, deeper workflow embedment, stronger enterprise security proof, and platform breadth - you can justify moving toward or slightly above the top of that band.

Third, you test the downside. If the business has weak retention, heavy services, product overlap with more generic tools, or concentration risk, the realistic valuation can slip below the core band.

Step 2: Applying it to LexBridge

Assume LexBridge has these characteristics:

- USD 10m revenue

- 85% recurring software revenue

- Strong gross margins

- Solid retention, but not best-in-class

- Good law-firm customer base

- Some services tied to onboarding and custom templates

- Clean financial reporting

- No major customer concentration

- Reasonable security posture, but not standout enterprise proof assets

That would likely place the business somewhere in the core range, rather than the premium edge.

What would create the premium scenario?

LexBridge might push into the premium scenario if it also had:

- Very strong retention and expansion inside existing firms

- Clear proof that it sits in daily, mission-critical workflows

- Enterprise-grade security and compliance credentials

- Stronger EBITDA conversion

- A broader connected workflow story beyond a single feature

- Obvious strategic relevance to a likely buyer set

What would create the discounted case?

It could fall toward the lower end if:

- Services made up too much of revenue

- Customers saw it as optional productivity software

- Churn was creeping up

- Reporting was weak

- The business depended too heavily on the founder or a few large customers

- The product had weak differentiation versus larger platforms

The main lesson is simple. Two Legal Tech companies with the same USD 10m of revenue can reasonably be worth very different amounts. Revenue gets you into the conversation. Quality, durability, and strategic value determine where you land.

8. Where Your Business Might Fit (Self-Assessment Framework)

A good self-assessment is not about flattering yourself. It is about identifying what buyers will actually care about and deciding where the biggest gains can still be made before a sale.

Score each factor from 0 to 2:

- 0 = weak or missing

- 1 = acceptable but not strong

- 2 = clearly strong

How to interpret your score

8-10 points: You are closer to the premium end of the range. That does not guarantee a premium valuation, but your business likely checks many of the boxes buyers pay for.

5-7 points: You are in fair-market territory. This is where many good businesses sit. A few focused improvements in the next 6-12 months could matter a lot.

0-4 points: You are likely at risk of being valued below the headline multiples you see in the market. The good news is that this usually means there is clear work to do before launching a process.

Use this framework honestly. The point is not to produce a number. The point is to see which gaps have the biggest payoff if fixed before a sale.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often start a process before the numbers are clean, before the story is clear, and before the likely buyer list has been built properly. That usually leads to reactive answers, weaker buyer confidence, and lower offers.

Another major mistake is hiding problems. Churn issues, weak cohorts, customer disputes, security gaps, or margin pressure almost always surface in diligence. If buyers discover them late, the damage is worse than if you disclosed them early with a plan. Trust is part of valuation.

Weak financial records are another avoidable problem. If you can improve revenue classification, separate recurring revenue from services, tighten gross margin reporting, and show better KPI tracking over the next 6-12 months, that can materially improve how buyers view the business. Messy numbers force buyers to be conservative.

A fourth mistake is running an unstructured process. In practice, a competitive sale process with an experienced advisor often leads to meaningfully better pricing - often around 25% higher than a one-buyer conversation - because it creates tension, improves positioning, and reduces the buyer's ability to anchor the deal on their terms.

Another common error is revealing the price you want too early. If you tell buyers you are hoping for, say, USD 40m, many of them will treat that as the target to barely beat. You lose price discovery. The market should tell you what your business is worth, not the other way around.

There are also Legal Tech-specific mistakes. One is failing to explain where AI actually helps and where guardrails exist. If your AI story sounds like marketing rather than controlled workflow improvement, buyers will worry. Another is failing to prove security maturity in a category where confidentiality is central. A weak security story can quietly reduce both buyer interest and valuation.

10. What Legal Tech Founders Can Do in 6-12 Months to Increase Valuation

You do not need a dramatic reinvention to improve valuation. In most cases, the best gains come from tightening the business you already have and making the value clearer.

Improve the numbers

Start by cleaning up revenue quality. Separate recurring revenue from services, track gross margin by revenue type, tighten monthly reporting, and make sure retention data is easy to show. If you can reduce low-margin services dependency or improve onboarding efficiency, do it.

Also look for realistic margin improvement. Buyers reward businesses that look like software, not software plus labor. Even modest improvements can matter if they prove better earnings quality.

Improve the durability story

Focus on retention, expansion, and product embedment. Reduce churn where possible. Push for wider seat adoption, deeper workflow usage, stronger integrations, and multi-year contracts where the market supports them.

If you can show that customers are using more of the product over time and relying on it in more sensitive workflows, you move closer to the businesses that earn stronger valuations.

Reduce buyer fear

Make security and compliance proof easy to diligence. Organize certifications, policies, governance materials, AI controls, incident history, and customer security documentation. Buyers pay more when risk feels knowable and manageable.

Also reduce key-person risk. If too much depends on you, build up the leadership bench, delegate customer relationships, and document core operating knowledge. That helps buyers believe the company can perform after closing.

Sharpen the strategic narrative

Build a clear answer to three questions: why do customers really buy us, why do they stay, and which buyer types would value this asset most? A strong process does not just describe the business. It frames the business in terms a buyer cares about.

For Legal Tech, that usually means showing where you sit in workflow, what adjacent expansion paths exist, and why your customer base or product position would matter to a strategic acquirer or private equity platform.

Prepare like diligence has already started

Create a clean data room. Fix contract issues. Review customer concentration. Make sure your KPIs tie to the valuation story. Prepare explanations for weaker areas rather than hoping they will not come up.

Founders who do this work before launching a process usually get a better result because buyers feel confidence earlier, ask better questions, and spend less time discounting risk.

11. How an AI-Native M&A Advisor Helps

A strong outcome usually comes from two things happening at once: the right buyers see the deal, and the company is presented in a way that makes those buyers compete. That is where an AI-native M&A advisor can have a real edge.

First, AI can expand the buyer universe far beyond the usual shortlist. Instead of approaching only a small set of obvious acquirers, an AI-native process can identify hundreds of qualified buyers based on deal history, strategic fit, product adjacency, financial capacity, and other signals. More relevant buyers means more competition, stronger offers, and a better chance the deal closes even if one buyer drops out.

Second, AI can speed up the early part of the process. Buyer matching, outreach support, preparation of marketing materials, and due diligence organization can all move faster, which means initial conversations and first offers can often happen in under 6 weeks rather than dragging out through a manual process.

Third, the best AI-native firms combine that speed with experienced human advice. You still want senior M&A advisors who know how to frame the business, pressure-test the numbers, handle buyer psychology, and run a disciplined process. The advantage is getting that expert advisory quality with AI enhancing the work behind the scenes, rather than paying traditional bulge bracket costs for a slower, more manual approach.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.