The Complete Valuation Playbook for Manufacturing Technology Businesses

A practical guide to how manufacturing technology businesses are valued and what drives high multiples.

If you are a founder or CEO of a privately held manufacturing technology business and you may sell in the next 1-12 months, valuation should not be treated like a mystery or a guessing game. In this sector, the spread between an average outcome and a great one can be very wide - even for businesses with similar revenue.

That is especially true now. Manufacturing technology is attracting steady buyer interest because industrial companies still need better automation, planning, visibility, quality control, and plant-level software - but buyers have also become much more selective about what deserves a true software multiple versus what is really a project business in disguise.

This playbook is built to help you see what manufacturing technology businesses actually sell for, what drives higher and lower multiples, where your business may sit on that spectrum, and what you can realistically do over the next 6-12 months to improve the outcome.

1. What Makes Manufacturing Technology Unique

Manufacturing technology is not one single category. It includes software-led manufacturing ERP and planning tools, factory digitization platforms, industrial analytics, OT and control system integration, industrial vision and sensing systems, digital twin and engineering platforms, and workflow tools that help factories run better. Some businesses are true software companies. Others are really engineering or integration firms with software wrapped around them. That difference matters a lot in valuation.

The biggest reason this sector is unique is that buyers are not only asking, "How fast are you growing?" They are also asking, "Where do you sit in the manufacturing stack?" A company that becomes part of daily factory decision-making - scheduling, throughput, quality, maintenance, line performance, traceability, or plant visibility - is usually worth more than a company that sells one-off projects or custom engineering hours.

Another important difference is that manufacturing technology often lives in a harder operating environment than general business software. Buyers know factory deployments can involve long sales cycles, integration work, plant-level change management, cybersecurity concerns, hardware dependencies, and slower customer adoption. They pay more when you have already solved those problems in a repeatable way.

The main risk factors buyers always check in this sector include:

- how much of revenue is recurring software versus services or hardware

- how hard deployments are, and whether implementations consume too much margin

- whether your product is truly mission-critical or just "nice to have"

- customer concentration, especially if a few large manufacturers drive most revenue

- integration risk with ERP, MES, SCADA, PLC, and plant systems

- whether your product can scale across sites, plants, and geographies

- whether ROI is measurable and easy for customers to understand

In plain English: buyers want to know whether you built a scalable product, or whether they are really buying a team of smart people who need to keep doing custom work forever.

2. What Buyers Look For in a Manufacturing Technology Business

At the most basic level, buyers care about the same things they care about in other deals: revenue scale, growth, profitability, gross margin, retention, and quality of management. But in manufacturing technology, those basics are filtered through one bigger question: is this business product-led enough to scale, or is it still too dependent on bespoke delivery?

Strategic buyers usually look for one of three things. First, they may want a missing product capability, such as planning optimization, plant analytics, machine vision software, or industrial data connectivity. Second, they may want access to a customer segment or manufacturing vertical where you already have credibility. Third, they may want a platform extension that helps them cross-sell into their installed base.

Private equity buyers usually look at the same business with a slightly different lens. They care about whether the company can grow fast enough after acquisition, whether margins can improve, and who they could sell it to later. If they buy at a full price today, they need confidence that a larger buyer in 3-7 years will still pay well.

How private equity thinks about your business

A private equity buyer usually asks four practical questions.

First, if they buy you at today's multiple, can they grow the business enough that the exit still works later? That means they care deeply about recurring revenue, retention, upsell, pricing power, and how repeatable customer acquisition is.

Second, who is the likely next buyer? In manufacturing technology, that could be a larger strategic software company, an automation platform, an industrial OEM with digital ambitions, or a bigger private equity-backed software group.

Third, what levers can they pull? Common levers include price increases, better sales discipline, cross-sell into adjacent modules, international expansion, acquisitions of smaller point solutions, and reducing low-margin service work.

Fourth, how much risk is buried inside delivery? If growth depends on long custom projects, heavy founder involvement, or constant on-site engineering, the buyer will usually lower the multiple because scale is harder than the revenue line suggests.

3. Deep Dive: Software-Led vs Services-Led - The Valuation Split That Matters Most

In manufacturing technology, one of the biggest valuation questions is simple: are you really a software company, or are you a services company with software attached? The data makes this point very clearly. The best private deal outcomes in the set go to software-led, high-margin, mission-critical optimization businesses. The weakest outcomes tend to cluster around services-heavy, legacy, low-tech, or non-core carve-out situations.

This matters because recurring software revenue is more scalable than project revenue. A buyer will pay more when the next USD 1 of revenue can be added without needing a matching increase in implementation hours, field engineering, or custom work. In this sector, that often separates a true platform from an integration-led business.

The private transaction data shows that many automation, engineering, and integration-led deals clear at low revenue multiples, often below 1.0x revenue. By contrast, the standout premium deal in industrial optimization reached roughly 11.0x revenue, supported by very strong profitability, high strategic value, and clear fit within the buyer's broader platform. That is the core lesson: software scarcity and proven economics create premium outcomes. "Industrial tech" by itself does not.

Buyers care because services-heavy businesses are harder to scale and easier to replace. They can be attractive businesses, but they usually trade more on EBITDA than on revenue. A software-led business with strong margins, low churn, and measurable plant ROI can support a much stronger revenue multiple because the buyer sees a larger long-term platform.

If your business looks more services-led today, the goal is not to pretend otherwise. The goal is to move steadily toward a better mix over time - more recurring licenses, more standard deployments, more reusable connectors, fewer one-off custom builds, and clearer proof that customers stay and expand.

A founder-friendly way to think about this is: every time you replace custom effort with repeatable product value, you make the business easier to buy and easier to scale.

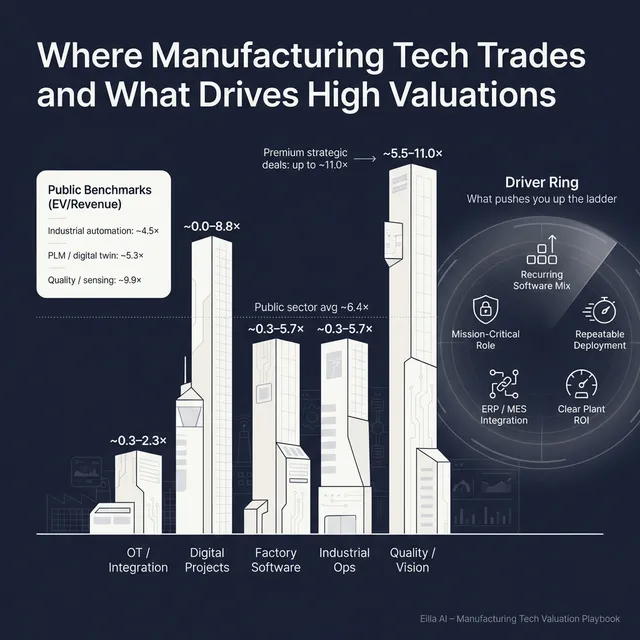

4. What Manufacturing Technology Businesses Sell For - and What Public Markets Show

The data shows a very wide range in manufacturing technology. That is normal for this sector because it includes very different business models under one label. Software-led industrial optimization, planning, and platform businesses can command materially higher multiples than engineering-led, integration-led, or consulting-heavy businesses.

So the right way to use market data is not to grab the highest number and call it your valuation. The right way is to identify which group your business actually resembles, then adjust for your scale, growth, margin quality, recurring revenue, and strategic fit.

4.1 Private Market Deals (Similar Acquisitions)

The overall private transaction dataset shows an average EV/revenue multiple of about 2.5x, but the median is only about 0.7x. That gap is important. It means a few premium software-like deals lift the average, while many real-world deals in services, integration, and lower-quality software clear at much lower levels.

The pattern is fairly consistent. Services-led automation, OT integration, and digital transformation deals often land below 1.0x revenue, while stronger software-led industrial optimization assets can move materially higher. The premium outlier in the set reached roughly 11.0x revenue, helped by around 40% EBITA margin, strategic fit, and clear evidence that the asset would be accretive for the buyer.

A few practical takeaways come from that table. First, headline category labels do not tell you much by themselves. Second, the market pays very differently for recurring, software-led industrial value versus labor-heavy delivery. Third, in this sector, premium outcomes usually need either true product scarcity or a very clear strategic role inside a larger platform.

These are illustrative ranges, not a formal valuation opinion. Your actual outcome depends on who the buyer is, what they believe they can do with the asset, and how competitive the sale process is.

4.2 Public Companies

Public market trading multiples provide a useful reference point, but they are not your private valuation. Most public companies in and around this space are larger, more diversified, more liquid, and more mature than private founder-owned businesses. Their multiples set the edges of the map, not the final answer.

As of mid to late 2025, the public set shows a broad overall average of about 6.4x EV/revenue and a median of about 3.6x. The average EV/EBITDA is around 37.1x, with a median of about 18.2x. But again, the spread is huge, because different subsegments trade very differently.

* These averages are heavily influenced by outliers and should be treated cautiously.

Here is how to interpret that. Public markets tend to reward scale, strong margins, durable product value, and mission-critical position in the workflow. Industrial sensing and software-enabled quality platforms can trade very well because they sit close to production, quality, and throughput. Large industrial automation platforms also trade well because they combine sticky installed bases with embedded software and strong customer relationships.

Private founders should use these public numbers as reference bands. In most cases, you should adjust downward for smaller scale, lower growth, customer concentration, limited management depth, and private-company risk. In special cases, you may argue upward if your asset is genuinely scarce, highly strategic, and clearly fits into a larger buyer platform.

5. What Drives High Valuations (Premium Valuation Drivers)

The data points to a simple truth: buyers pay up when a manufacturing technology business looks scarce, scalable, and strategically important. The premium is not just about growth. It is about confidence that growth is durable and that the product matters enough to justify continued investment.

5.1 Mission-critical product value

If your product sits close to the core economics of a factory - throughput, scheduling, yield, quality, downtime, traceability, labor efficiency, or production visibility - buyers tend to care more. They know that manufacturers do not easily rip out systems that improve these outcomes.

A good example is software that helps a plant make better scheduling decisions, improve line performance, or reduce scrap in a measurable way. That is very different from a generic dashboard or a nice reporting layer. The closer you are to decisions that save money every day, the stronger your valuation story.

5.2 Software-like economics

The premium outcomes in the data are tied to software-like economics: high margins, scalable deployment, and a product that does not require endless custom work. Buyers pay more when the business can grow without adding delivery complexity in the same proportion.

In practical terms, that means standardized onboarding, reusable integrations, remote deployment where possible, and customer success that scales. If your gross margin improves as you grow, buyers notice.

5.3 Clear and quantified customer ROI

Manufacturing buyers are often skeptical by nature. They want proof. So do acquirers. A business that can show measurable ROI - reduced downtime, fewer defects, higher throughput, lower energy use, better schedule adherence, faster root-cause analysis - is easier to underwrite.

This is especially powerful when you can show the value in customer language, not software language. For example: "our customers reduce quality escapes by 18%" is more valuable than "we provide real-time analytics."

5.4 Platform fit and ecosystem position

Some of the strongest outcomes happen when a buyer sees exactly where the target fits in its own platform. That might mean connectors into ERP, MES, SCADA, historians, PLCs, CMMS, quality systems, or engineering workflows. It might also mean the target is OEM-agnostic and can sit across different installed bases.

Buyers pay more when they can see the cross-sell path clearly. If they already own the customer relationship and your product adds a missing capability, your value becomes strategic, not just financial.

5.5 Strong margin trajectory and operating leverage

Even when revenue multiples are not spectacular, buyers still reward improving earnings quality. The data shows that businesses with improving margin structure and operating leverage can support stronger EBITDA-based outcomes because buyers believe forward earnings are becoming more dependable.

For founders, this means valuation is not only about current margins. It is also about showing that margins are moving in the right direction for the right reasons - better product mix, more repeatable delivery, smarter implementation, and healthier pricing.

5.6 Capability breadth - but only when it is hard to replicate

A broader stack can help if it is genuinely differentiated. For example, a business that combines OT, cybersecurity, cloud integration, and engineered controls in a way that is difficult to copy may attract strategic buyer interest even if revenue multiples stay modest.

But founders should be careful here. Capability breadth only helps when it increases strategic value. If breadth just means you do many custom things for many clients, it may actually confuse buyers and reduce the sense of product focus.

5.7 Clean fundamentals still matter

Even in a specialized sector, basic M&A quality drivers still matter a lot:

- clean financial records

- predictable recurring revenue

- diversified customers

- low churn

- strong leadership below the founder

- clear KPI reporting

- credible forecasts

- no hidden legal, security, or product issues

These do not usually create the whole premium by themselves. But without them, buyers often refuse to pay the top end.

6. Discount Drivers (What Lowers Multiples)

The businesses that sell at the low end of the range are usually not "bad businesses." More often, they are businesses with too much uncertainty, too little repeatability, or too much dependence on custom work. Buyers respond to that uncertainty by lowering the multiple.

The biggest discount driver in this sector is a services-heavy revenue mix. If the buyer believes revenue depends on implementation teams, custom engineering, and founder-led delivery, they will be reluctant to pay a high revenue multiple. They may still like the business, but they will value it more like a services firm than a software platform.

Another common issue is weak differentiation. In manufacturing technology, many companies sound similar at first glance: AI, IoT, visibility, analytics, smart factory, optimization. Buyers discount businesses that cannot clearly prove what makes them hard to replace. If your value story sounds generic, your multiple usually follows.

Low or unstable margins also hurt valuation. So do inconsistent growth, customer concentration, weak renewal data, and deployments that take too long or fail too often. A buyer will ask whether growth is really scalable, or whether the company is constantly re-earning every sale.

Other common discount drivers include:

- too much revenue from one customer, one plant group, or one channel partner

- unclear ROI or weak case studies

- product that still behaves like a custom project

- poor integration readiness with core factory systems

- founder dependence in sales, product, or delivery

- unclear cybersecurity posture in OT environments

- weak financial controls or poor revenue visibility

- large backlog of customer-specific customizations that complicate support

The good news is that many of these issues can be improved. Buyers do not need perfection. They need evidence that the risks are understood, managed, and shrinking.

7. Valuation Example: A Manufacturing Technology Company

To show how valuation logic works in practice, let us use a fictional company called ForgePath Analytics. This company is not real, and the revenue figure below is also fictional. The numbers are illustrative only - not investment advice and not a formal valuation.

ForgePath Analytics sells plant performance and production optimization software to mid-sized manufacturers. It integrates with ERP, MES, and machine data sources, gives supervisors and plant leaders live visibility into bottlenecks and losses, and helps customers improve throughput, scheduling, and quality. Revenue is USD 10.0m, with a mostly software-led model, moderate implementation work, and improving margins.

How the valuation logic works

Start with the most relevant private comparables. The most useful private anchor in the source data is the software-led industrial operations optimization group, where the observed range is broad, but the better software assets sit well above services-led automation and integration deals.

Then look at public companies as an upper reference band. Public software and industrial platform businesses in adjacent categories often trade around the mid-single-digit revenue multiple range, with some much higher. But a private company at USD 10m revenue does not deserve full public-market treatment. You discount for smaller scale, private-company risk, lower liquidity, and less proof.

That leads to a sensible core range. The source logic suggests 4.0x-7.0x revenue is defensible for a small, software-led manufacturing operations analytics platform at USD 10m revenue, assuming it is clearly more software-like than services-led, but not yet a fully proven category leader.

Applying that logic to the fictional company

For ForgePath Analytics, the right valuation depends on what the business actually looks like.

If the company has decent growth but still relies too much on implementation work, with some concentration risk and only moderate proof of retention, you are closer to the lower end of the range.

If the company has strong gross margins, repeatable deployment, sticky customers, clear ROI proof, and good integration fit with larger platforms, you move toward the middle or upper part of the range.

If the company also has strong expansion within existing customers, low churn, credible operating leverage, and real strategic scarcity, a premium case becomes easier to defend.

What would push ForgePath down or up?

A discounted case could apply if too much revenue is tied to projects, deployments are slow, customer concentration is high, or the buyer sees the product as a feature rather than a platform. In that case, the business may still be attractive, but the multiple gets pulled closer to services-led outcomes.

A core case makes sense if the company is clearly software-led, has recurring revenue, can show measurable customer ROI, and has reasonable evidence that it can scale without linearly adding services cost.

A strong case becomes more credible if the company looks like scarce industrial software - high customer stickiness, strong gross margin, low churn, fast time-to-value, good cross-sell potential, and clear platform fit for a strategic buyer.

The point is not that USD 70m is "the answer." The point is that two manufacturing technology businesses with the same USD 10m of revenue can be worth very different amounts depending on business model quality, strategic fit, and execution risk.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple self-assessment can help you see whether you are closer to the bottom, middle, or top of the valuation range. Score each factor from 0 to 2.

- 0 = weak

- 1 = acceptable

- 2 = strong

Be honest. This is not a pitch deck exercise. It is a way to identify where improvement will matter most.

How to interpret your total score

10-12 pointsYou are likely closer to premium territory. That does not guarantee a premium multiple, but it means the business has many of the features buyers usually pay up for.

6-9 pointsYou are likely in fair-market territory. A good process can still produce a strong result, but the business probably has a few issues that cap the top end today.

0-5 pointsYou may still be sellable, but there is probably meaningful value left on the table. In many cases, 6-12 months of focused work can improve the outcome materially.

The real benefit of this exercise is not the score itself. It is the gap analysis. If your business is weak on recurring mix, retention proof, and deployment repeatability, those are the areas most likely to change the valuation conversation.

9. Common Mistakes That Could Reduce Valuation

One of the most expensive mistakes is rushing the sale. Founders sometimes decide to sell, send a few materials to the market, and hope buyers will "see the value." In practice, if the numbers, narrative, and process are not ready, buyers sense it immediately and use that uncertainty against you.

Another major mistake is hiding problems. If customer churn is rising, a deployment went badly, margins are weaker than they look, or a big account is at risk, it will usually surface in diligence. When buyers discover issues late, they do not just reduce price. They lose trust. That can hurt terms, structure, and certainty of closing.

Weak financial records also reduce value. In this sector, buyers want to see revenue by product, services versus software mix, gross margin by segment, customer concentration, retention, implementation economics, and a clean picture of recurring revenue. If you can improve reporting over the next 6-12 months, that work often pays back many times over.

A lack of a structured, competitive sale process is another costly error. When only a small handful of buyers are contacted, you lose leverage. Research commonly shows that a well-run, competitive process with an advisor can produce meaningfully higher purchase prices - often around 25% higher - because buyers know they are competing, not negotiating in a vacuum.

Many founders also hurt themselves by revealing what price they want too early. If you tell buyers you are hoping for, say, USD 10m of enterprise value, do not be surprised when offers cluster around USD 10.1m or USD 10.2m. You have killed price discovery. Let the market tell you what the business is worth before you anchor the number.

A few industry-specific mistakes matter a lot in manufacturing technology:

- Overstating how "productized" the business is when delivery is still highly customized. Buyers will test this very quickly.

- Failing to prove customer ROI in factory terms. If you cannot connect your product to throughput, downtime, scrap, quality, labor, or schedule performance, your value story will feel weaker than it should.

10. What Manufacturing Technology Founders Can Do in 6-12 Months to Increase Valuation

The good news is that valuation is not only about what your business is today. It is also about what you can prove before you go to market. A focused 6-12 month plan can materially improve both price and deal certainty.

10.1 Improve the quality of revenue

Try to shift more revenue toward recurring software, support, and subscription-like contracts. Reduce one-off custom work where possible, or at least separate it clearly in your reporting so buyers can see the core software engine.

If you can standardize packaging, pricing, and contract structure, do it. Buyers like businesses they can understand quickly and scale cleanly.

10.2 Prove ROI more clearly

Build a sharper case-study library. Show before-and-after metrics in factory language: scrap reduction, better OEE, faster changeovers, better schedule adherence, fewer quality escapes, improved labor efficiency, lower downtime.

This is one of the highest-return areas in the sector because buyers need to believe customers will keep buying, renewing, and expanding.

10.3 Reduce implementation drag

Look closely at deployment time, implementation margin, and how much custom work each customer needs. Standard connectors, templates, playbooks, and clearer onboarding can all help.

Even if you cannot fully transform the model in a year, showing that deployments are getting faster and more repeatable can improve how buyers think about scale.

10.4 Clean up concentration and customer risk

If one or two customers dominate revenue, try to broaden the base before a sale. If contracts are short or renewals are informal, tighten them up. If expansion within existing accounts is strong but undocumented, start measuring it properly.

A buyer will pay more when revenue feels diversified and durable.

10.5 Make your numbers easier to trust

Prepare clean monthly reporting on revenue mix, margins, retention, backlog, pipeline, and customer concentration. Separate product, services, and any hardware revenue clearly. Make sure your forecasts are realistic and tied to evidence.

Trust matters in M&A. Better reporting does not only improve diligence. It can improve valuation because buyers gain confidence faster.

10.6 Strengthen the strategic narrative

Do not just describe features. Explain where your business sits in the manufacturing stack and why that position matters. Are you a plant performance layer? A planning optimization engine? A quality intelligence platform? A visibility and control bridge between systems?

The clearer your role, the easier it is for a buyer to imagine how you fit into a larger platform and why they should pay more.

10.7 Reduce founder dependence

If you are still the main closer, main product translator, and main delivery problem-solver, start reducing that dependence now. Push customer relationships deeper into the team. Build a second layer in sales, delivery, and customer success.

Buyers do not want to feel that the asset walks out the door if the founder steps back.

11. How an AI-Native M&A Advisor Helps

A modern manufacturing technology sale is no longer just about who you already know. The biggest valuation gains often come from reaching the right buyers - not only the obvious ones. An AI-native advisor can expand the buyer universe to hundreds of relevant acquirers based on real signals like deal history, strategic fit, financial capacity, installed base overlap, and likely synergies. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal still closes even if one bidder drops out.

Speed also matters. With AI-driven buyer matching, faster outreach, better preparation of marketing materials, and support through diligence, the process can move much faster than a manual-only approach. That can help founders reach initial conversations and offers in under 6 weeks, which matters when momentum and confidentiality both count.

The strongest version of this model combines AI with experienced human advisors. You still want seasoned M&A professionals running the process, shaping the story, handling negotiations, and giving buyers confidence. The AI advantage is that it makes the process broader, faster, and more informed - while the human advisory layer keeps the framing, positioning, and execution at a Wall Street-grade level without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.