The Complete Valuation Playbook for Media Technology Businesses

A practical guide to how Media Technology businesses are valued and what drives high multiples.

If you are a founder or CEO of a privately held Media Technology business and you may sell in the next 1-12 months, valuation is not something to leave until the last minute. This sector is active but uneven. Buyers are still paying real money for strong assets, especially where software, workflow infrastructure, content operations, audience intelligence, and strategic communications overlap. But the spread between average and premium outcomes is wide.

This guide is built to help you understand that spread. It shows what Media Technology businesses actually sell for, what public markets say about the sector, what tends to push valuations up or down, and what you can still improve in the next 6-12 months before going to market.

The goal is not to give you a fake precise number for your company. It is to help you understand the valuation logic buyers use so you can position your business better and avoid leaving money on the table.

1. What Makes Media Technology Unique

Media Technology is not one clean category. It includes several different business types that often get grouped together in M&A, even though buyers value them differently. At one end are software-led platforms such as press release distribution tools, social media management and listening platforms, content operations systems, digital asset management tools, and customer engagement software. At the other end are services-led businesses such as influencer agencies, social campaign firms, PR advisory shops, and content execution partners.

That mix matters because valuation is heavily shaped by how much of your revenue is software, how much is repeatable, and how much still depends on people. A software-led media workflow platform with high renewal rates and strong gross margins will usually be valued very differently from a services-heavy social agency, even if both operate in the broader media and communications ecosystem.

Buyers also care about where your product sits in the workflow. In this sector, value often comes from being embedded in a daily process: managing content libraries, distributing releases, routing approvals, monitoring audiences, running campaigns, or measuring engagement. If your platform is part of an important workflow, it is harder to replace. If it is a nice-to-have add-on, valuation is usually weaker.

There are also a few risk areas that buyers always examine closely in Media Technology. They will check whether your revenue is recurring or project-based, whether your customer base is concentrated, whether your product is truly differentiated, whether margins can scale, and whether key client relationships sit with the founder or a few senior staff. In this sector, buyers are especially sensitive to businesses that look like software in the pitch but behave like agencies in the numbers.

2. What Buyers Look For in a Media Technology Business

At a basic level, buyers look for the same big things they look for in most companies: revenue scale, growth, margin quality, and predictability. But in Media Technology, they go one layer deeper. They want to know whether you have built a durable product or just assembled a useful bundle of services around a theme that happens to be hot right now.

They will usually focus on a few core questions. Are customers locked into your workflow? Do they renew? Do they expand usage over time? Is your gross margin strong enough to suggest software-like economics? Can the business keep growing without adding people at the same rate as revenue? If the answer to those questions is yes, buyers get more comfortable paying up.

Customer quality matters too. A platform serving enterprise marketing teams, publishers, broadcasters, studios, listed companies, or regulated communications functions often gets more attention than a business with many small, low-commitment customers. That is not because small customers are bad. It is because enterprise buyers tend to be stickier, contracts are often larger, and the workflow can become harder to replace.

Buyers also care about strategic fit. In this sector, many acquisitions are not just about buying revenue. They are about buying capability. A larger platform may want your audience insights module, your newsroom workflow, your media database, your creator network, your digital asset delivery infrastructure, or your enterprise relationships. The clearer that strategic fit is, the easier it is for a buyer to justify a stronger price.

How private equity thinks about it

Private equity buyers usually think in a more structured way. They ask what multiple they are paying on the way in, what the business could be sold for in 3-7 years, and what they can improve in between. They care a lot about whether your business can become more software-like over time, whether margins can expand, and whether they can add scale through add-on acquisitions.

They also think hard about the next buyer. Could they later sell the company to a larger strategic acquirer? To a bigger private equity firm? Or, less commonly in this space, to public markets? If your company sits in an attractive niche with clean recurring revenue and real workflow importance, that future buyer list is broader.

The levers they look for are practical. Can prices be increased? Can more modules be sold into the same customers? Can services be standardized or reduced? Can fragmented competitors be acquired? Can reporting, leadership, and sales execution be professionalized? The more obvious those levers are, the more confident they become.

3. Deep Dive: Workflow Criticality and Revenue Quality

One of the most important valuation questions in Media Technology is this: are you a system that sits inside the customer's operating workflow, or are you mainly an outsourced service that helps them execute around the edges?

This matters because the data shows a clear pattern. Software-led content operations, media workflow, and adjacent communication infrastructure businesses can support stronger revenue multiples than services-led businesses. In the deal data, software-oriented content operations transactions sit around the mid-single-digit revenue multiple range, while services-led campaign and agency deals often cluster much lower on revenue multiples, even when EBITDA multiples can still look healthy. Public market data shows a similar split: content and workflow infrastructure platforms, and scaled marketing software platforms, generally trade above services-heavy communications businesses.

Buyers care because workflow systems are harder to rip out. If your platform stores rich media assets, routes approvals, automates multi-channel distribution, tracks engagement, or sits between content creation and publication, you are part of the customer's operating system. Replacing you creates friction, training cost, process risk, and often compliance or brand risk. That usually supports stronger retention and better pricing power.

By contrast, if a large share of your revenue depends on project work, custom campaign execution, or founder-led relationships, buyers see more fragility. Those businesses can still sell well, especially if EBITDA is strong, but the valuation logic is different. Buyers may pay solid EBITDA multiples if they believe they can improve utilization, cut overlap, or cross-sell services. They are less likely to award software-like revenue multiples unless the business has clearly productized its offering.

A useful way to think about it is this:

If your business looks more like the left column today, the goal is not to become a completely different company overnight. The goal is to move one or two steps right. That could mean packaging services into repeatable subscriptions, increasing product usage inside the customer workflow, reducing custom work, proving renewals, or showing that margins improve as revenue grows.

4. What Media Technology Businesses Sell For - and What Public Markets Show

The data does not support one simple headline multiple for Media Technology. This is a broad category. Multiples depend heavily on whether the business is software-led or services-led, how embedded it is in customer workflows, whether growth is strong, and whether margins are scalable.

That said, the data does give founders a practical map. Private deals show what real buyers have paid for similar assets. Public companies show what larger, more liquid businesses in adjacent categories are worth in the market. Neither gives you your exact price tag, but together they create a useful range.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions provided, the overall average EV/Revenue multiple is about 3.1x and the median is about 3.0x. The average EV/EBITDA multiple is about 18.4x and the median is about 13.5x. But the spread by subsegment is important.

Software-led and workflow-oriented media technology assets generally sit above services-heavy businesses on revenue multiples. PR distribution platforms and enterprise content operations platforms show revenue multiples around the 3.5x to 5.2x range in the data. By contrast, services-led campaign, influencer, and social agencies can range from well below 1.0x revenue at the low end to roughly 2.7x-3.7x revenue for better-positioned businesses. Even in those services-heavy deals, EBITDA multiples can still be healthy when buyers believe profits are durable or can expand post-close.

A few patterns stand out. First, strategic fit matters a lot. Deals where the target clearly extends the buyer's platform often achieve stronger outcomes. Second, EBITDA matters more than many founders expect. Several deals show modest revenue multiples but still strong EBITDA multiples because buyers believed they could protect or grow profits. Third, deal structures such as earn-outs are common in this sector, especially when growth or earnings delivery still needs to be proven.

These ranges are illustrative, not promises. Your actual outcome depends on your specific revenue mix, customer quality, growth, leadership depth, and how competitive the sale process is.

4.2 Public Companies

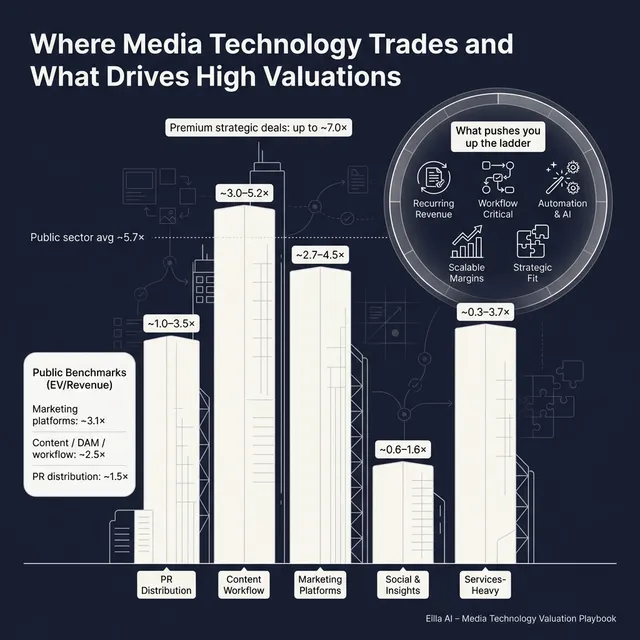

The public market data covers a broad set of adjacent categories as of mid to late 2025. Overall, the average EV/Revenue multiple in the set is 5.7x, but the median is only 1.4x. The average EV/EBITDA is 31.2x, while the median is 13.1x. That big gap between average and median tells you something important: a few scaled, high-quality software names pull the average up, while many smaller or slower-growing companies trade much lower.

The cleanest takeaway is that larger, scaled software platforms with stronger growth and better margins trade at the highest levels. Marketing automation and customer engagement platforms are the strongest group in the data, with EV/Revenue often around 2.7x to 4.5x and, for profitable names, high EBITDA multiples. Content and digital asset management businesses also trade relatively well, roughly around 2.1x to 4.2x revenue in the sample. Social media management and audience insights platforms are lower on average, roughly around 0.6x to 1.6x revenue in the sample, reflecting more mixed growth and margin profiles. PR distribution platforms mostly sit around 1.0x to 2.3x revenue. Services-led PR and communications businesses are generally lower.

Public multiples should be used as reference bands, not direct pricing tools. Public companies are usually much larger, more diversified, more liquid, and better known than privately held businesses. That usually means private company multiples should be adjusted downward for smaller scale, customer concentration, weaker reporting, or less predictable growth.

At the same time, there are cases where a private business can argue for a stronger outcome than a simple downward adjustment would suggest. That happens when the asset is scarce, strategically valuable, deeply embedded in a workflow, or clearly attachable to a larger buyer's platform. In other words, public comps help frame the conversation, but strategic value still shapes the final answer.

5. What Drives High Valuations (Premium Valuation Drivers)

The premium outcomes in this sector usually come from a mix of strategic fit, software-like economics, and lower perceived risk. Buyers do not just pay for what your business is today. They pay for what they believe it becomes in their hands, and how safely they can get there.

5.1 Clear platform adjacency

One of the strongest premium drivers in the source data is strategic adjacency. Buyers pay more when your business clearly extends their existing platform, customer offer, or workflow coverage. That could mean a PR distribution tool adding reach to a communications platform, a social media capability deepening a digital services stack, or a content workflow product strengthening a media operations suite.

Why this matters is simple: the buyer can see immediate cross-sell and integration value. They are not buying a random asset. They are buying something attachable.

For founders, that means you should be able to explain where you fit in the buyer's world. For example:

- Your platform helps a larger communications suite move from planning into distribution.

- Your content workflow tool helps a DAM or publishing platform become more operationally central.

- Your audience insights layer helps a customer engagement platform become more valuable to marketers.

5.2 Technology that actually improves delivery and margins

The data also supports a premium for technology-enabled workflow businesses, especially where AI, cloud delivery, automation, and orchestration reduce labor intensity and improve scalability. But buyers are practical here. They do not pay more just because you say "AI" or "automation."

They pay more when the technology shows up in the numbers and the customer behavior. Does it lower delivery cost? Does it improve gross margin at scale? Does it make the workflow stickier? Does it reduce churn? Does it increase module adoption?

In plain terms, "tech-enabled" becomes valuable when it changes the business model, not just the product demo.

5.3 Strong EBITDA conversion or a believable path to it

Several deals in the source data show an important pattern: buyers sometimes pay strong EBITDA multiples even when revenue multiples are not extraordinary. That is common in Media Technology, especially where part of the business is still services-heavy but profitability is real and durable.

Buyers like businesses where profits can scale faster than revenue because of better utilization, shared overhead, improved pricing, or productization. This matters for founders because a business does not need to look like a pure SaaS company to command a good valuation. But it does need to show that earnings are not fragile.

Practical examples:

- A campaign execution business that has standardized delivery and improved team utilization.

- A workflow platform that can add customers without adding support headcount at the same pace.

- A hybrid software-services company where services help land the account, but software drives retention and margin over time.

5.4 Revenue that is measurable, repeatable, and contractable

In this sector, premium outcomes often go to companies that can turn a story into measurable future delivery. That is why earn-outs are common. Buyers are willing to support stronger headline valuations when renewals, contracts, retention, expansion, and EBITDA targets are visible enough to underwrite.

This is especially important if your business is still moving from service-heavy to platform-heavy. Buyers may not fully pay for the future on day one, but they may pay for it if you can structure and prove it.

That means founders should focus on a few basics:

- Multi-year or recurring contracts where possible.

- Clear renewal and retention reporting.

- Module usage data.

- Revenue by product, not just by customer.

- A believable bridge from today's margin to tomorrow's margin.

5.5 Reduced key-person risk

A surprising number of media and marketing-related acquisitions depend on management staying after the deal. The source data makes that clear. Buyers often require founder or executive retention where client relationships, delivery quality, and growth depend heavily on a few people.

This cuts both ways. If the business depends too much on you, buyers may worry. But if you have a strong leadership bench and are willing to support a transition, that can protect valuation.

The premium version is a business where:

- Customer relationships are spread across a team.

- Product ownership is not stuck in one head.

- Sales and delivery are documented and repeatable.

- The next layer of leadership is visible and credible.

5.6 Clean company fundamentals

Some premium drivers are not glamorous, but they matter in every serious process. Buyers pay more when the numbers are clean, revenue is easy to understand, KPIs are consistent, churn is measured, margins are segmented properly, and the leadership team is prepared.

In practice, this means predictable monthly reporting, clean customer cohorts, clear gross margin by line of business, low customer concentration, and credible forecasts. Founders often underestimate how much valuation is won or lost simply because a buyer trusts - or does not trust - the information they are seeing.

6. Discount Drivers (What Lowers Multiples)

Low-end outcomes usually do not happen because of one dramatic flaw. More often, they happen because a buyer sees too many reasons to be cautious at the same time.

The most common discount driver in Media Technology is revenue quality that looks weaker than the story. If a company presents itself as a platform business but a large share of revenue comes from custom service work, one-off projects, or founder-led relationships, buyers usually pull the multiple down. They may still like the asset, but they will value it more conservatively.

Another discount driver is limited proof that the product is truly embedded. If customers can replace your tool without much pain, or if product usage is shallow, retention risk rises. Buyers discount businesses that sit at the edge of the workflow rather than in the middle of it.

Small scale is also a real discount. The source material specifically highlights that very small companies often suffer a size haircut because of customer concentration, illiquidity, and limited operating history at scale. Even when the product is real, buyers know smaller businesses can be more fragile.

Other common discount factors include:

- High customer concentration.

- Low visibility on renewals or pipeline.

- Weak gross margins for a business presented as software.

- Churn that is not measured clearly.

- Heavy dependence on paid acquisition or unstable channels.

- Product claims around AI, blockchain, or automation without commercial proof.

- Founders who hold too much of the customer, product, or team knowledge themselves.

The good news is that many of these issues are fixable or at least manageable. Buyers do not expect perfection. They do expect honesty, preparation, and evidence.

7. Valuation Example: A Media Technology Company

To make the logic concrete, here is a fictional example. The company and revenue figure below are made up for illustration. This is not investment advice and not a formal valuation. It is simply a way to show how buyers might think.

Let us imagine a fictional company called SignalFlow. SignalFlow sells a software-led content operations and distribution platform for corporate communications teams, PR functions, and media-rich brand teams. Its products include newsroom workflow, media contact management, content approvals, analytics, and asset distribution. It has USD 10m of annual revenue, solid gross margins, and a mix of mid-market and enterprise customers.

Step 1: Start with the comp logic

The source data suggests a practical valuation framework for this part of the sector:

- Public PR distribution and social/listening businesses often sit in roughly the low-1x to low-2x revenue range.

- Content workflow and DAM-type software can sit higher, around roughly 2.0x to 4.0x-plus in public markets.

- Private transactions for PR distribution and content operations software show roughly 3.0x to 5.2x revenue in the more relevant software-led deal set.

- Services-heavy businesses often trade lower on revenue multiples, even if EBITDA multiples can still be attractive.

For a USD 10m revenue private company like SignalFlow, the right starting point is not the overall public average. It is the private software-led range, adjusted for growth, margins, workflow stickiness, and size.

A sensible core revenue multiple range for a good Media Technology platform at this scale is therefore around 3.5x to 5.5x revenue. That is broadly consistent with the private market logic in the source set and the public reference points, while allowing for a private-company discount versus larger public names.

Step 2: Apply it to the fictional company

Assume SignalFlow has the following profile:

- USD 10m revenue

- High gross margins

- Mostly subscription revenue

- Good retention

- Moderate but not exceptional growth

- Useful integrations into adjacent platforms

- Some services revenue for onboarding, but not too much

That would support a core valuation range around USD 35m to USD 55m EV.

Now assume an upside case where SignalFlow also has:

- Clear enterprise adoption

- Strong net revenue retention, meaning customers spend more over time

- Deep workflow embedment

- Measurable automation benefits

- A broader buyer universe because it fits strategic platform roadmaps

In that case, a premium range of up to around 6.5x-7.0x revenue is not impossible, implying up to around USD 65m-70m EV.

Now assume a weaker version of the same company:

- Revenue still USD 10m

- Higher services mix

- Less clear product differentiation

- Shallow integrations

- Customer concentration

- More founder dependence

- Slower growth or weaker retention

That profile could easily fall toward 2.5x-3.5x revenue, implying roughly USD 25m-35m EV.

Step 3: What this means for founders

Two Media Technology businesses with the same revenue can be worth very different amounts. That is one of the biggest lessons in this sector. Revenue alone does not determine value. Buyers care about the type of revenue, the quality of the workflow position, the margin profile, and how much strategic value they can unlock.

That is why positioning matters so much. If you can show that your revenue is recurring, your product is embedded, your economics improve with scale, and your business fits naturally into a larger platform, you move toward the top of the range. If you cannot, buyers tend to fall back to more conservative logic.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple way to use this playbook is to score your business honestly across three groups: high-impact factors, medium-impact factors, and bonus factors. Give yourself 0, 1, or 2 points on each line.

- 0 = weak today

- 1 = acceptable but not standout

- 2 = strong and buyer-friendly

How to interpret the score

- 20-26 points: You are closer to premium territory. That does not guarantee a premium multiple, but your profile is lining up with what buyers usually pay more for.

- 12-19 points: You are in fair-market territory. A good process can still produce a strong outcome, but there are likely one or two areas that limit valuation.

- 0-11 points: You are likely closer to the low end today. That does not mean you should not sell. It means the biggest gains may come from improving a few key factors before launching a process.

The point of this exercise is not to flatter yourself. It is to identify where one or two changes could have the biggest impact on value.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes founders make is rushing the sale. If your numbers are not clean, your story is not sharp, and your data room is incomplete, buyers will sense it quickly. That usually leads to lower first offers, slower processes, and painful renegotiations later.

Another mistake is hiding problems. In almost every deal, issues come out during diligence anyway. Maybe churn is higher than reported. Maybe a large customer is at risk. Maybe the product roadmap is behind. If you hide that, the problem becomes bigger because trust is damaged. Buyers can handle known issues much better than surprise issues.

Weak financial records are another common value leak. If revenue is not segmented clearly, margins are hard to follow, customer cohorts are messy, or KPI reporting is inconsistent, buyers discount the business because uncertainty rises. In many cases, 6-12 months is enough time to improve reporting materially.

A lack of a structured, competitive sale process also reduces valuation. Founders who negotiate with one buyer in a loose process often leave money on the table. Research and market practice consistently support the idea that a structured competitive process with an advisor can lead to meaningfully higher prices - often around 25% higher - because multiple buyers create tension, improve price discovery, and strengthen negotiating leverage.

Another major mistake is revealing the price you are hoping for too early. If you tell buyers you are looking for, say, USD 10m of value, many will anchor right above that - maybe USD 10.1m or USD 10.2m - instead of telling you what they might actually pay in a true market process. Let the market speak first.

Two sector-specific mistakes matter especially in Media Technology. The first is overclaiming that a services-heavy business is really a software company. Buyers will test that quickly. The second is talking about AI, automation, or proprietary workflow without showing adoption, usage, or financial impact. In this sector, unsupported product claims do not create premium value. They often create skepticism.

10. What Media Technology Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work is usually not a dramatic pivot. It is targeted improvement in the handful of areas buyers care about most.

Improve the numbers

Start by tightening financial reporting. Separate subscription revenue from services. Show gross margin by business line. Track retention, churn, customer expansion, and sales efficiency in a clean monthly format. If you have low-hanging fruit on pricing, packaging, or cost structure, act on it now rather than hoping a buyer will pay you for potential alone.

If your EBITDA story is weak today, build a credible path. Buyers do not need perfection, but they do need to see that profits can improve in a durable way.

Improve revenue quality

Try to shift as much revenue as possible toward repeatable contracts, subscriptions, retainers, or recurring platform fees. If onboarding or campaign work is still important, package it clearly so buyers can see it as enabling product revenue rather than replacing it.

Reduce concentration where possible. Even one or two new meaningful customers can help if the current book is too dependent on a small handful of accounts.

Improve workflow stickiness

Show that your product is embedded. Increase integrations. Track product usage. Highlight where customers rely on you inside daily operations. If customers only use one feature today, expand module adoption before going to market.

In Media Technology, a product that touches more steps in the workflow is usually worth more than a narrow point tool.

Improve the buyer story

Map the likely buyer universe and understand why each category would care. Strategic buyers may care about adjacency, workflow coverage, customer access, or cross-sell. Private equity may care about margin expansion, productization, and buy-and-build opportunities. Your positioning should reflect that.

This is also the right time to sharpen the narrative around what kind of business you really are. Buyers reward clarity. They discount confusion.

Reduce key-person risk

If too much runs through you, start fixing that now. Push more customer ownership into the team. Document sales and delivery processes. Make sure the next layer of leadership is visible. If buyers believe the value walks out the door with the founder, valuation suffers.

Prepare for diligence before the process starts

The easiest value to preserve is the value you do not lose in diligence. Clean up contracts, intellectual property files, product documentation, employment matters, board records, and KPI definitions. Build a data room early. You want diligence to confirm your story, not weaken it.

11. How an AI-Native M&A Advisor Helps

Selling a Media Technology business is partly about valuation analysis, but it is also about running the process well. An AI-native M&A advisor improves outcomes first by broadening the buyer universe. Instead of speaking to a narrow list, AI can help identify hundreds of qualified acquirers based on deal history, strategic fit, synergies, and financial capacity. More relevant buyers means more competition, stronger offers, and a better chance the deal still closes even if one buyer drops out.

It also speeds up the process. With AI helping on buyer matching, outreach, preparation of marketing materials, and diligence support, it is possible to move from planning to initial conversations and offers much faster than in a manual-only process. In many cases, that means getting to initial offers in under 6 weeks.

Just as importantly, AI should enhance expert advice, not replace it. The best outcome comes from experienced human M&A advisors using AI to work faster, cover more ground, and position the business more effectively. That means stronger materials, better buyer targeting, tighter numbers, and a story told in the language acquirers actually use - without the cost structure of a traditional bulge bracket bank.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.