The Complete Valuation Playbook for Medical Imaging Businesses

A practical guide to how medical imaging businesses are valued and what drives high multiples.

If you are considering a sale in the next 1-12 months, valuation is not just a finance exercise. In medical imaging, it is shaped by where you sit in the stack, how deeply you are embedded in clinical workflow, how much of your revenue repeats, and how much risk a buyer believes they are taking on.

That matters even more now. Radiology providers are dealing with workforce shortages and rising imaging demand, while the regulatory and commercial landscape for AI-enabled imaging products keeps evolving. At the same time, consolidation is continuing across radiology and imaging software, which means good assets can attract real buyer interest - but only if the story, numbers, and positioning are clear. (American College of Radiology)

This guide is built to do three things for founders and CEOs of privately held medical imaging businesses: show what similar companies actually sell for, explain what drives higher and lower multiples, and give you a practical way to assess where your business likely fits today - plus what you can still improve before a sale.

1. What Makes Medical Imaging Unique

Medical imaging is not one market. Buyers look very differently at four broad categories:

- imaging software and workflow infrastructure - PACS, VNA, RIS, viewers, image exchange, scheduling, requisition and referral workflows

- radiology AI and software as a medical device - decision support, triage, quantification, prioritization, reporting support

- imaging services - outpatient imaging centers, teleradiology, trial imaging services, imaging operations

- imaging hardware and components - modalities, detectors, X-ray tubes, portable scanners, other OEM-adjacent products

Those categories may all touch medical images, but they do not get valued the same way. Software that sits inside the daily clinical workflow often earns higher multiples than service-heavy businesses. Services businesses can still sell well, but buyers tend to focus more on labor dependency, site economics, reimbursement exposure, and physician coverage. Hardware businesses are usually judged through a different lens again - product margin, manufacturing risk, capital intensity, and installed base.

Medical imaging also has a level of complexity that general software buyers cannot ignore. Buyers will always look closely at regulatory status, clinical validation, workflow integration, reimbursement support, implementation burden, uptime, data security, and the practical question of whether clinicians actually use the product every day. A business can have good technology and still get marked down if it is hard to deploy, lightly used, or dependent on one champion customer.

In this sector, trust is part of valuation. If a hospital, health system, radiology group, or imaging center has relied on your platform for years, that matters. If your product is approved, validated, integrated, and hard to remove, that matters even more.

2. What Buyers Look For in a Medical Imaging Business

At the simplest level, buyers look for the same things they look for in most acquisitions: scale, growth, profit, and risk. But in medical imaging, they ask more pointed questions.

First, they want to know what you actually are. Are you mainly a recurring software company, a service operator, a hybrid, or a hardware business with software wrapped around it? That classification affects the multiple before the conversation really starts. A business with recurring software revenue, good gross margin, and low churn will usually be viewed more favorably than a business with the same revenue but more implementation work, lower margins, and heavier people dependency.

Second, buyers care about how mission-critical your product is. If your software helps interpret scans, route cases, manage referrals, orchestrate imaging workflow, or sit inside the reporting process, it becomes much harder to replace. That tends to support better retention and stronger valuation. If you are more of a nice-to-have overlay that can be turned off without much disruption, buyers will notice.

Third, they look at customer quality. A sticky customer base of hospitals, health systems, radiology groups, and imaging networks is usually worth more than a business with lots of pilots, short-term projects, or a handful of concentrated accounts. Buyers want proof that your revenue survives procurement cycles, IT scrutiny, and clinical review.

How private equity buyers think about it

Private equity buyers usually ask three practical questions.

The first is entry price versus exit price. If they buy your business today at a healthy multiple, can they grow it enough and improve the profile enough to sell it later at a similar or better multiple?

The second is who buys it after them. In medical imaging, that future buyer might be a larger imaging IT platform, a healthcare software consolidator, a strategic OEM, a radiology services platform, or a larger private equity fund.

The third is what levers they can pull in 3-7 years. Typical levers include price increases, expanding into adjacent modules, cross-selling into an installed base, international expansion, tuck-in acquisitions, better sales discipline, and margin improvement. If your business already shows a path to those value creation moves, PE interest tends to be stronger.

3. Deep Dive: Workflow Integration and Recurring Revenue Quality

In medical imaging, one of the most important valuation questions is this: are you truly embedded in the clinical workflow, or are you still a point solution that can be swapped out?

Your source data makes this theme very clear. The stronger private deal outcomes are often tied to businesses that sit in the operational system of record, connect cleanly into existing EMR, PACS, referral, or clinical workflows, and have revenue that looks recurring rather than project-based. That combination tends to create lower churn, higher switching costs, and more obvious cross-sell value for a buyer.

Why do buyers care so much? Because embedded products are harder to rip out. If your software is connected to image management, requisition flow, reporting, scheduling, or core clinical decision support, removing it creates disruption. Buyers like disruption risk - when it hurts the customer to leave, it reduces the buyer's downside.

Recurring revenue quality matters just as much. Buyers do not only want revenue that repeats. They want revenue that repeats with evidence: renewal rates, multi-year contracts, module expansion, price realization, and low support burden. In your data, businesses with clear SaaS or ARR framing often achieved stronger revenue multiples than adjacent healthcare software businesses without the same visibility.

Founders can improve this over time. You may not be able to reinvent the whole business in 12 months, but you can move from a lower-value profile to a higher-value one.

If your business looks more like the left column today, the path forward is usually clear: deepen integrations, convert pilots to contracted deployments, track renewals and usage carefully, reduce service intensity, and prove that the product is being used in real clinical workflow rather than just tested.

4. What Medical Imaging Businesses Sell For - and What Public Markets Show

Here is what the data actually shows: medical imaging does not trade on one universal multiple. The market separates software, services, and hardware very quickly. Public markets also place a large premium on scale, recurring revenue, and category position, while private transactions usually land in a tighter and more conservative band.

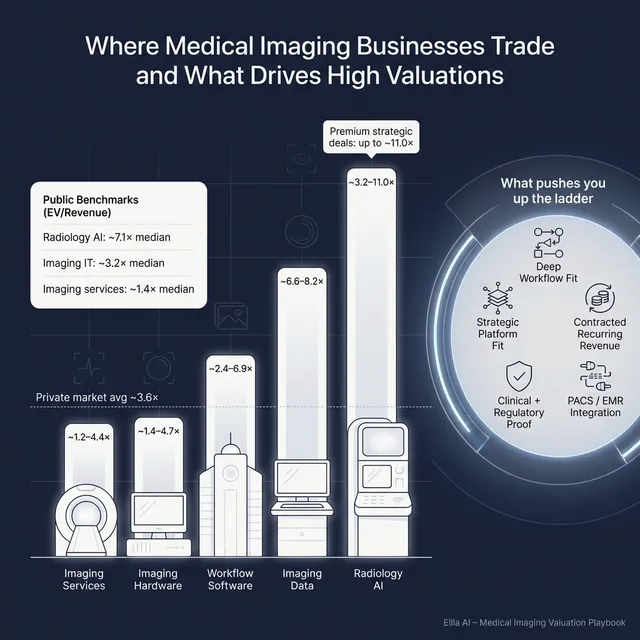

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions in your source set, the overall average private EV/Revenue multiple is 3.6x and the median is 3.2x. The overall average EV/EBITDA is 16.8x and the median is 18.0x. That is a useful baseline, but the more helpful insight is how different sub-groups behave.

Imaging workflow and healthcare software deals with recurring revenue or deep integration often sit in the higher part of the range. More service-heavy imaging businesses and equipment-related assets tend to trade lower on revenue multiples, unless they have unusual strategic value, strong profitability, or scarce technology.

A founder should not read these as fixed rules. A smaller software-led imaging business with real workflow penetration may deserve to sit well above a basic services business at the same revenue level. On the other hand, if the business is still early, customer concentration is high, and revenue quality is mixed, headline software multiples are not the right benchmark.

4.2 Public Companies

The public comp set in your source data is wider and more volatile. Overall, the average EV/Revenue is 14.8x but the median is only 3.0x. That gap tells you something important: a few high-multiple, fast-growth, loss-making companies pull the average up sharply, while the typical public company in and around this space trades much lower. Overall average EV/EBITDA is 19.6x and median EV/EBITDA is 10.8x.

As of late 2025, the public market appears to reward four things most: category leadership, strong growth, recurring or software-heavy revenue, and infrastructure-like positioning. It is much less generous to lower-growth hardware manufacturers, challenged operators, or speculative businesses with little revenue quality.

The right way to use public multiples is as a reference band, not a price tag. Public companies are larger, more liquid, and better known. That usually means a private company should be valued at a discount to public peers if it is smaller, growing more slowly, or carries more risk.

That said, there are times when a private asset can outperform a simple public-market discount. If your business is scarce, strategically important, hard to replicate, and clearly valuable to a consolidator or platform buyer, a buyer may pay above what a plain market-average approach would suggest. That is especially true when the buyer sees distribution leverage or product bundling upside.

5. What Drives High Valuations (Premium Valuation Drivers)

The data points to a handful of recurring themes. These are the things that move a medical imaging business toward the top of the range.

Embedded workflow integration

Buyers pay more for businesses that are tightly integrated into core clinical and operational workflows. In your source data, this shows up again and again in imaging IT, referral, EMR-adjacent, and connected care software deals. The reason is simple: integration creates stickiness.

In practice, that means buyers want to see live integrations with PACS, RIS, EMR, image viewers, referral systems, reporting systems, and hospital IT environments. A founder-friendly way to think about it is this: if removing your product would break daily workflow, buyers care a lot more.

Recurring revenue with proof

Recurring revenue matters, but buyers want proof, not just a label. They want signed contracts, renewal history, implementation-to-go-live conversion, upsell evidence, and low churn.

For example, instead of saying "most of our revenue is recurring," a premium story is "82% of revenue is contracted annual software revenue, gross retention is high, and customers usually add modules after year one." That kind of evidence changes how a buyer underwrites risk.

Strategic adjacency

Some assets are worth more because they fit naturally into a larger platform. Your data shows this clearly in transactions completed by repeat healthcare IT consolidators. These buyers often pay for what the target can become inside their platform, not just what it earns on its own today.

In medical imaging, this often means your product can be bundled into a larger imaging workflow suite, referral ecosystem, cloud archive, reporting platform, or diagnostics distribution channel. If the synergy story is obvious, the buyer universe usually gets bigger.

Category position and installed footprint

Buyers pay more when a business has an entrenched footprint - market leadership in a geography, strong deployment count, broad installed base, multi-country use, or a reputation that makes the business hard to displace.

This matters because it lowers buyer fear. A product that is already trusted by real hospitals and radiology groups is easier to scale than a product that still depends on early believers.

Strong profitability or a clear path to it

High EBITDA conversion at relatively modest revenue levels is a powerful signal. In your data, several of the strongest EBITDA-based outcomes came from businesses that were already profitable at small or mid-sized scale. Buyers like that because it shows the model can scale without every new dollar of revenue requiring a similar increase in cost.

For founders, this does not mean you need to maximize profit at the expense of growth. It means you should be able to explain your margin structure, show what revenue looks like once implemented, and prove that support, validation, and deployment costs are under control.

Clean operating foundations

This does not always show up directly in reported multiples, but it shows up in real processes. Buyers pay more for clean financials, low customer concentration, well-documented KPIs, clear product ownership, strong management depth, and no unpleasant surprises.

In other words, premium valuation often comes from making the buyer's decision easy. A good business with messy records can still sell, but it rarely sells as well as the same business with a clean story and clean proof.

6. Discount Drivers (What Lowers Multiples)

The low end of the range usually does not happen by accident. There are common reasons why medical imaging businesses get marked down.

The first is weak revenue quality. If too much revenue comes from one-off services, pilots, custom projects, or non-repeat work, buyers will usually pull the multiple down. They may still like the business, but they will not value it like a software company with clear recurring revenue.

The second is shallow product integration. If your product sits outside the main workflow and needs constant selling effort to stay relevant, buyers will worry about churn. In this sector, "good product" is not enough. Buyers want evidence that clinicians and administrators would feel real pain if the product disappeared.

The third is customer concentration. If one hospital group, distributor, OEM relationship, or channel partner accounts for too much of revenue, the business starts to look fragile. The same goes for key-person risk - if the founder drives sales, relationships, clinical credibility, and product direction alone, that reduces buyer confidence.

The fourth is unclear regulatory and clinical positioning. In medical imaging, ambiguity around approvals, intended use, validation evidence, post-market obligations, or reimbursement support creates real discount pressure. Buyers do not like unresolved regulatory questions.

The fifth is poor margin visibility. Hybrid imaging businesses often struggle here. If you cannot clearly separate software revenue, services revenue, implementation cost, support burden, and gross margin by product line, buyers assume the worst.

The sixth is hard-to-scale delivery. This is especially relevant in imaging services, trial imaging, and AI deployments that need heavy customization, manual review, or specialist input every time a new customer goes live. If scaling revenue means scaling headcount almost one-for-one, buyers will notice.

None of these issues automatically kill a deal. But they usually push a business toward the lower end of the valuation range unless you address them before going to market.

7. Valuation Example: A Medical Imaging Company

Let’s make this practical with a fictional company.

Assume a business called NorthBridge Imaging AI. It sells radiology AI decision-support software to hospitals and imaging groups. The company has deep integrations into PACS and reporting workflow, generates mostly recurring software revenue, and has USD 10.0m in annual revenue. This company is fictional, and the revenue level is fictional too. The valuation logic below is illustrative only - it is not investment advice or a formal valuation.

Step 1: Start with the right comp set

The most important choice is the comp set. For a business like NorthBridge, the right starting point is not imaging centers, hardware OEMs, or trial imaging services. It is radiology AI decision-support software and nearby imaging workflow software.

Your source logic for a similar radiology AI software business points to a public-market revenue multiple range of about 3.2x to 13.5x, before tightening the high end for execution risk and limited proof. That is directionally useful, but public markets can be noisy, especially in AI-heavy categories. So the right move is to use that public range as an outer reference, then cross-check it against more grounded private transaction bands.

The private deal data suggests that most practical healthcare software transactions, even good ones, clear at materially lower levels than the most optimistic public AI names. That is why a sensible process usually narrows the range into a core band that reflects both upside and realism.

Step 2: Apply the logic to the fictional company

For NorthBridge, I would frame valuation like this:

- Discount case - the company has good technology, but customer concentration is high, renewal history is short, and deployments still require meaningful services work

- Base case - recurring revenue is real, integrations are solid, retention looks healthy, and the company is clearly software-led

- Premium case - the company is deeply embedded in workflow, has multi-year contracts, low churn, broad referenceability, strong net revenue retention, and clear strategic relevance to larger imaging platforms

This range fits the source logic well. The low end is supported by the lower part of the radiology AI public range and by more conservative private software outcomes. The high end reflects what can happen when a radiology AI business combines strategic relevance with strong workflow integration and recurring revenue quality - but still applies discipline versus the most aggressive public market outliers.

Step 3: What this means for founders

Two medical imaging businesses with the same USD 10m of revenue can be worth very different amounts. One may be worth around USD 35m because the revenue is mixed, the customer base is concentrated, and the product is not deeply embedded. Another may be worth USD 80m+ because buyers view it as sticky infrastructure with real expansion value.

That is the core lesson of valuation in this sector. Revenue matters, but profile matters almost as much. The better your revenue quality, workflow depth, customer proof, and strategic fit, the more likely you are to move from a fair price to a premium one.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple way to use this playbook is to score your business honestly. The goal is not perfect precision. The goal is to identify what most affects valuation and where improvement will pay off fastest.

Score each factor 0, 1, or 2.

- 0 = weak today

- 1 = decent but not standout

- 2 = strong and well evidenced

How to interpret your score

- 14-20 points - you are closer to the premium end of the range

- 8-13 points - you likely fit within fair-market valuations, with a few areas that could still move the outcome

- 0-7 points - you may still sell, but there is probably meaningful value left on the table if you rush the process now

Be honest when scoring. Founders often overestimate product strength and underestimate buyer concern about concentration, renewals, and implementation burden. The point of the exercise is not to flatter the business. It is to focus improvement where it matters most.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders sometimes decide to test the market before the numbers, narrative, and process are ready. That usually leads to weaker first impressions, lower bids, and more buyer leverage later.

Another is hiding problems. In medical imaging, buyers will eventually find the issues - contract gaps, churn risk, regulatory uncertainty, customer concentration, data security concerns, unresolved reimbursement questions, or product limitations. If they discover those issues late, the damage is worse than the issue itself because trust drops.

A third is weak financial records. This is common in founder-led businesses, especially where software, services, and implementation revenue are mixed together. If you can improve margin reporting, revenue visibility, cohort tracking, renewal reporting, and product-level economics in the next 6-12 months, that work often pays back many times over in valuation.

A fourth is not running a structured, competitive process with an advisor. A good process creates buyer tension, protects confidentiality, and improves leverage. Research frequently points to meaningfully higher pricing from structured competitive sale processes, often around 25% better than single-buyer or poorly run situations. That is not a guarantee, but it is directionally important.

A fifth is telling buyers what price you want too early. This kills price discovery. If you say you want USD 10m of enterprise value, many buyers will simply come back at USD 10.1m or USD 10.2m instead of telling you what they might actually have been willing to pay. Let the market show its hand first.

Two industry-specific mistakes show up often in medical imaging:

First, founders sometimes oversell the AI and undersell the workflow reality. Buyers care less about flashy model claims and more about where the product sits in the radiologist's day, how often it is used, and whether hospitals renew.

Second, founders often fail to separate software economics from clinical or implementation support costs. In this sector, that separation matters. If buyers cannot see the real margin profile of the software business, they will usually mark the whole company down.

10. What Medical Imaging Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work is usually not a massive pivot. It is a set of focused improvements that make the business look safer, stickier, and easier to underwrite.

Improve revenue quality

Convert pilots into multi-year contracts where possible. Tighten renewal processes. Reduce one-off service revenue as a percentage of total revenue. Track gross retention, net retention, and implementation-to-go-live conversion. If your business is truly recurring, make that visible.

Deepen workflow integration

Prioritize integrations that make the product harder to replace - PACS, RIS, EMR, reporting, referral, cloud archive, or image exchange depending on your model. Document usage inside workflow, not just deployment counts. Buyers want evidence of embeddedness.

Strengthen proof points

Line up reference customers. Package clinical validation, outcomes data, uptime records, case studies, and deployment metrics cleanly. If you sell into providers, show why customers keep using the product after the first contract term. If you sell into life sciences or OEM channels, show renewal and expansion logic there too.

Clean up the financial story

Separate software, services, implementation, and support revenue. Show gross margin by line if possible. Build a clear monthly KPI dashboard covering bookings, ARR, retention, churn, pipeline, contract duration, and customer concentration. This work is not glamorous, but it directly affects valuation.

Reduce avoidable risk

Diversify away from oversized accounts where you can. Put stronger contracts in place. Resolve known regulatory or compliance loose ends. Build a management bench so the business does not look founder-dependent. Buyers pay more when the business looks transferable.

Sharpen the buyer narrative

Do not describe the company as "an AI business" and stop there. Position it correctly. Are you workflow infrastructure, decision support, triage, quantification, imaging operations software, or an imaging data platform? The clearer the category and strategic fit, the easier it is for the right buyers to see value.

11. How an AI-Native M&A Advisor Helps

A strong sale outcome usually comes from buyer competition, good positioning, and process discipline. That is where an AI-native M&A advisor can materially improve results.

First, AI expands the buyer universe. Instead of talking to a narrow list of obvious names, an AI-native process can identify hundreds of qualified buyers based on deal history, likely synergies, financial capacity, sector behavior, and fit. More relevant buyers usually means more competition, stronger offers, and a better chance the deal actually closes if one bidder drops out.

Second, AI can speed up the process. Better buyer matching, faster outreach, faster preparation of marketing materials, and tighter support during due diligence can help founders reach initial conversations and offers in under 6 weeks in many situations. Speed matters because momentum matters.

Third, the best AI-native advisors combine technology with experienced human judgment. You still want expert M&A advisors running the process, shaping the story, preparing the numbers, and speaking the buyer's language. The advantage is that AI helps them do that with more market coverage, better intelligence, and more efficiency - delivering Wall Street-grade advisory quality without traditional bulge-bracket cost structures.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.