The Complete Valuation Playbook for Precision Manufacturing Businesses

A data-driven guide to how precision manufacturing businesses are valued and what drives high multiples.

If you run a precision manufacturing business - CNC machining, sheet metal fabrication, injection molding, additive manufacturing, or integrated assembly - you’ve probably wondered what your company is actually worth.

Right now is a pivotal moment in the sector. Strategic buyers are consolidating fragmented supplier bases. Private equity firms are building platforms in aerospace, defense, medical, and specialty materials. At the same time, buyers are far more selective than they were a few years ago. Quality, positioning, and risk profile matter more than ever.

This playbook is built specifically for founders and CEOs of privately held precision manufacturing businesses considering a sale in the next 1–12 months. We will:

- Show what businesses like yours actually sell for.

- Decode what drives higher vs lower multiples.

- Walk through a real-world valuation example.

- Give you a practical self-assessment and 6–12 month action plan.

Let’s start with what makes this industry unique.

1. What Makes Precision Manufacturing Unique

Precision manufacturing is not one single business model. It spans:

- Precision CNC machining and sheet metal fabrication.

- Injection molding and precision plastics.

- Metal casting, forging, and metal injection molding.

- Additive manufacturing and rapid prototyping.

- Integrated assembly and multi-process “one-stop” shops.

- Specialized niches like aerospace components, medical device parts, micro-precision engineering, and machine vision systems.

Valuation varies significantly depending on where you sit in that spectrum.

Why this sector is different

- Asset intensityYou own expensive machines, tooling, and facilities. Buyers care about machine age, utilization, maintenance, and replacement needs.

- Customer concentration riskIt is common for 1–3 customers to represent a large percentage of revenue. That can either be seen as strength - deep, sticky relationships - or as a risk.

- Qualification-driven stickinessIn aerospace, defense, and medical, once you are qualified, it is hard to be replaced. Certifications and approval processes create switching costs. That can support higher valuations.

- Margin dispersionThis sector includes both low-margin, commoditized job shops and high-margin, specialized manufacturers with niche materials or micro-precision capabilities. The valuation gap between those two is large.

- CyclicalityExposure to automotive, industrial, or general manufacturing cycles can impact stability and valuation.

In short: two companies with the same USD 10m revenue can have very different valuations based on positioning, margins, and customer profile.

2. What Buyers Look For in a Precision Manufacturing Business

When a buyer evaluates your business, they are asking one simple question:

“Is this revenue durable, defensible, and capable of growing?”

Here’s how that breaks down.

The obvious fundamentals

- Revenue scale - Larger businesses tend to attract more buyers and better multiples.

- Revenue growth - Buyers pay more for businesses growing faster than the market.

- EBITDA margin - Higher margins usually mean better pricing power or efficiency.

- Cash flow stability - Predictable earnings reduce perceived risk.

Industry-specific nuances

- End-market exposureAerospace, defense, and regulated medical manufacturing often trade at higher multiples than general industrial job shops.

- Technical differentiationTight tolerances, exotic materials, micro-precision, or complex multi-axis machining increase defensibility.

- Breadth of capabilitiesMulti-technology platforms - CNC + molding + sheet metal + assembly - can reduce OEM vendor count and increase switching costs.

- Certifications and quality systemsAS9100, ISO 13485, FDA compliance, and cleanroom capabilities are real valuation levers.

How private equity thinks

Private equity buyers think in terms of:

- Entry multiple - What they pay today.

- Exit multiple - What they believe they can sell it for in 3–7 years.

- EBITDA growth - How much they can grow profits through:

- Price increases.

- Operational efficiency.

- Add-on acquisitions.

- Cross-selling new services.

If they believe your business could be a “platform” for consolidation, they may pay more. If they see it as a small standalone job shop, they will be more conservative.

3. Deep Dive: General Job Shop vs High-Spec Niche Specialist

One of the biggest valuation differences in precision manufacturing is this:

Are you a generalist capacity provider - or a niche, high-spec specialist?

Why this matters

The data shows that businesses serving aerospace, defense, healthcare, or micro-precision markets often trade at higher revenue multiples than general industrial suppliers.

For example:

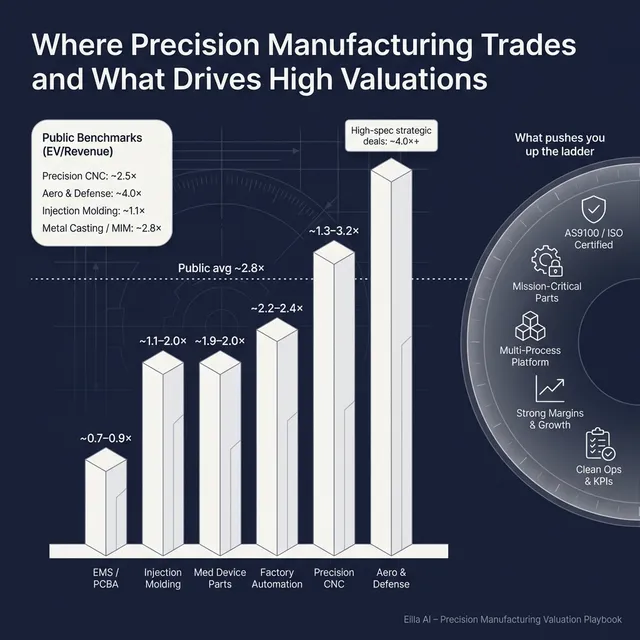

- Public precision CNC & sheet metal companies average around 2.5x EV/Revenue.

- Defense, aerospace & high-spec precision manufacturing averages around 4.0x EV/Revenue, though medians are lower and scale matters.

- Medical and life sciences component transactions average around 2.0x EV/Revenue, with some deals in the 3.8x–4.2x range for high-quality, regulated assets.

This gap is not random. It reflects switching costs and qualification barriers.

Lower-value profile vs higher-value profile

How to move from left to right

- Document quality metrics - scrap rates, on-time delivery, first article approvals.

- Deepen relationships with OEMs into lifecycle programs.

- Invest in certifications that match your target vertical.

- Build case studies around mission-critical components.

Buyers pay more for businesses that are hard to replace.

4. What Precision Manufacturing Businesses Sell For - and What Public Markets Show

Let’s look at what the data actually says.

5.1 Private Market Deals (Similar Acquisitions)

Across recent precedent transactions:

- Overall average EV/Revenue: 1.8x.

- On-demand precision manufacturing (CNC, 3D printing, sheet metal, molding):

- Average: 2.5x

- Median: 1.6x.

- Medical & life sciences component manufacturing:

- Average: 2.0x

- Median: 1.9x.

- Factory automation, machine vision, metrology:

- Average: 2.2x

- Median: 2.4x.

- Electronics manufacturing services (EMS):

- Average: 0.8x.

These are illustrative ranges. The exact multiple depends heavily on growth, margins, customer mix, and scale.

5.2 Public Companies

As of mid to late 2025, public trading multiples provide reference points.

- Overall average EV/Revenue: 2.8x.

- Precision CNC & sheet metal services:

- Average EV/Revenue: 2.5x.

- Median: 2.0x.

- Defense, aerospace & high-spec precision:

- Average EV/Revenue: 4.0x.

- Median: 2.1x.

- Integrated injection molding & plastics:

- Average EV/Revenue: 1.1x.

- Metal casting, forging & MIM:

- Average EV/Revenue: 2.8x.

Important: public companies are larger and more diversified than a typical USD 10–30m private business. Private valuations are usually at a discount to public multiples due to size, liquidity, and risk.

Think of public multiples as the upper reference band - not a guaranteed price tag.

5. What Drives High Valuations (Premium Valuation Drivers)

Across the data and sector experience, premium valuations are associated with a few consistent themes.

1. Exposure to regulated, mission-critical markets

Medical device manufacturing, aerospace, and defense with documented compliance and certifications consistently command higher revenue multiples.

Why? Switching costs are high. Qualification processes are long and expensive.

2. Multi-technology breadth that locks in OEMs

Businesses offering CNC + molding + sheet metal + assembly reduce vendor count for customers. That creates stickiness and cross-sell opportunities.

Buyers pay more when:

- A large percentage of customers use multiple services.

- Programs span prototype to production.

- You support product lifecycle, not just parts.

3. Proprietary processes or differentiated know-how

Additive manufacturing platforms with proprietary materials or technology have sometimes achieved high revenue multiples - even when EBITDA was negative - because of strategic fit.

You don’t need to be a software company. But if you have:

- Unique tooling methods.

- Proprietary material formulations.

- Specialized micro-precision capabilities.

…that can shift perception from “capacity provider” to “strategic asset.”

4. High gross margins supported by value-add

Machine vision, metrology, and IP-rich industrial technology companies with 40–55% gross margins often trade at higher multiples.

Margin is a signal of defensibility.

5. Clean operations and strong leadership

Even if not visible in headline multiples, buyers consistently reward:

- Clean financial statements.

- Low customer concentration.

- A second layer of management beyond the founder.

- Documented KPIs and production metrics.

These reduce execution risk.

6. Discount Drivers (What Lowers Multiples)

Here is what pushes businesses toward the low end of the range.

- High customer concentration with short-term contracts.

- Declining or flat revenue.

- Old equipment requiring major capex.

- Low gross margins driven by price competition.

- Exposure to highly cyclical or distressed industries.

- Founder-dependent sales relationships.

- Poor financial reporting or unclear margins by customer or product line.

In EMS, for example, average EV/Revenue multiples are closer to 0.7x–0.9x. That reflects lower margins and higher commoditization.

The good news: many of these are fixable within 6–12 months.

7. Valuation Example: A Precision Manufacturing Company

Let’s walk through an example.

This is a fictional company for illustration only.

Meet “NorthPoint Precision”

- Revenue: USD 10.0m.

- Services: CNC machining, sheet metal, injection molding, and light assembly.

- Employees: 35.

- Exposure: 40% aerospace and defense, 40% industrial, 20% medical.

- No proprietary IP, but strong quality systems.

We use revenue multiples because small private precision manufacturers are commonly valued that way when EBITDA is modest or volatile.

Step 1: Identify relevant comps

From the data:

- Public precision CNC & sheet metal: ~0.9x–2.9x.

- Private on-demand precision manufacturing: ~1.3x–3.2x.

- Aerospace/high-spec exposure supports upper half of ranges.

Step 2: Define realistic range

Given multi-technology breadth and some aerospace exposure - but no unique IP or deep regulated specialization - a reasonable illustrative band might be:

- 1.8x–2.8x EV/Revenue.

Step 3: Apply to USD 10.0m revenue

Midpoint around USD 23m.

If customer concentration were high or margins weak, the multiple might fall closer to 1.3x–1.6x. If strong certifications, recurring programs, and high margins were proven, it could justify the top end.

This is not a formal valuation - just a worked example to show how logic is applied.

8. Where Your Business Might Fit (Self-Assessment Framework)

Score yourself honestly.

Step 1: Score each factor 0, 1, or 2.

Step 2: Interpret

- 0–3 total - Likely lower half of range.

- 4–6 total - Solid market range.

- 7–9 total - Positioned toward premium multiples.

The goal is not ego. It is clarity on what moves valuation most.

9. Common Mistakes That Could Reduce Valuation

- Rushing the saleGoing to market without clean numbers or a clear growth story reduces buyer confidence.

- Hiding problemsQuality issues, customer disputes, or concentration risks will surface in due diligence. Surprises destroy trust and value.

- Weak financial recordsIf you cannot clearly show margins by customer or program, buyers assume risk.

- Running a non-competitive processResearch consistently shows that structured, competitive processes with advisors often lead to meaningfully higher purchase prices - sometimes around 25% higher than single-buyer negotiations.

- Naming your price too earlyIf you say, “I’m looking for USD 20m,” buyers will anchor to that. Let the market speak first.

Industry-specific mistake:Failing to document quality and certification performance. In aerospace and medical, undocumented excellence is treated as unproven.

10. What Precision Manufacturing Founders Can Do in 6–12 Months to Increase Valuation

You do not need a radical transformation. Focus on high-leverage actions.

Improve the numbers

- Increase gross margin through price adjustments or process improvements.

- Eliminate low-margin work that consumes capacity.

- Track scrap, rework, and on-time delivery and show improvement.

Reduce risk

- Diversify top 1–2 customers where possible.

- Secure longer-term purchase agreements or program visibility.

- Formalize key customer relationships beyond you personally.

Strengthen positioning

- Pursue relevant certifications if aligned with your strategy.

- Document case studies in aerospace, medical, or high-spec work.

- Show cross-sell rates across CNC, molding, and assembly.

Professionalize reporting

- Monthly management reporting.

- Clear revenue breakdown by sector.

- Clean inventory and working capital management.

If you move from “good operator” to “institutional-quality business,” your multiple can move meaningfully.

11. How an AI-Native M&A Advisor Helps

Selling a precision manufacturing business is not just about valuation theory. It is about execution.

An AI-native M&A advisor changes the game in three ways.

1. Higher valuations through broader buyer reach

AI expands the buyer universe to hundreds of qualified acquirers based on deal history, sector focus, synergies, and financial capacity.

More relevant buyers means:

- More competition.

- Stronger offers.

- A higher chance your deal closes, even if one buyer drops out.

2. Initial offers in under 6 weeks

AI-driven buyer matching, faster preparation of marketing materials, and streamlined due diligence support mean conversations and initial offers can happen much faster than traditional manual processes.

Speed reduces deal fatigue and uncertainty.

3. Expert advisory, enhanced by AI

You still get experienced human M&A advisors driving your process - negotiating, framing the story, managing buyers.

The difference is:

- Data-backed positioning.

- Wall Street-grade materials.

- Credibility with acquirers.

- Institutional-quality process - without traditional bulge-bracket costs.

If you would like to understand how an AI-native M&A process can support your exit, book a demo with one of our expert M&A advisors. It could be the most important preparation step you take before going to market.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.