The Complete Valuation Playbook for Renewable Energy Businesses

A practical guide to how renewable energy businesses are valued today and what drives high multiples.

If you run a privately held renewable energy business and are thinking about a sale in the next 1-12 months, valuation is not just about revenue, EBITDA, or a headline market multiple. It is about how buyers see your place in the energy transition, how much risk they think they are taking on, and whether your business feels like a scarce strategic asset or a replaceable project-and-labor business.

That matters even more now. Renewable energy is still attracting strategic buyers and private equity, but buyer appetite is more selective than it was in the easiest capital markets. Grid constraints, permitting delays, interest rates, storage economics, and pressure to prove real cash generation have made the gap wider between average assets and premium assets.

This playbook is built to help you read that market clearly. It shows what renewable energy businesses actually sell for, explains what drives higher and lower multiples, gives you a practical self-assessment, and lays out what you can realistically do in the next 6-12 months to improve your outcome.

1. What Makes Renewable Energy Unique

Renewable energy is not one business model. It includes utility-scale developers, independent power producers, asset managers, EPC firms, solar installers, battery and hydrogen technology providers, grid and electrification contractors, and specialist advisory businesses. Those models can all sit under the same broad sector label, but buyers value them very differently.

The biggest reason is that renewable energy mixes project risk, capital intensity, regulation, and long-term infrastructure logic in a way most normal businesses do not. A software company can often scale without building physical assets. A renewable energy company usually cannot. Land, grid connection, permits, offtake contracts, capex, construction execution, and operating performance all matter.

That creates very different valuation profiles. A developer with a credible pipeline, repeatable permitting engine, and strong project economics may be highly valuable, but it will still usually trade differently from a contracted owner-operator with stable cash flows. An EPC firm may grow quickly, but if buyers see it as labor-heavy and cyclical, they will usually pay a lower revenue multiple than they would for a specialist advisory or technology business with real IP.

Buyers in this sector also underwrite risk very specifically. They will always look at some version of the following:

- How real is the pipeline?

- How secure are land rights, interconnection, and permits?

- How much revenue is recurring versus one-time project work?

- How exposed are margins to equipment pricing, subcontractors, and delays?

- How concentrated is the business by customer, geography, or policy regime?

- How much of the value sits in people, and how much sits in systems, contracts, and owned assets?

In other words, renewable energy valuation is not just about growth. It is about growth quality, cash-flow visibility, and how much execution risk still sits between the buyer and the value they are paying for.

2. What Buyers Look For in a Renewable Energy Business

At a basic level, buyers still care about the usual things: scale, growth, margins, customer quality, and management. But in renewable energy, they care just as much about whether those numbers are durable.

A strategic buyer usually asks: does this give us capabilities, market access, assets, customer relationships, or pipeline we do not already have? That could mean development expertise in a hard-to-permit region, a strong C&I solar sales channel, battery integration know-how, hydrogen capability, or a meaningful fleet of operating assets. Strategic buyers often pay more when your business fills a gap that would be slower or riskier for them to build internally.

Private equity looks at the same business through a slightly different lens. They want to know what they are buying at entry, what the business could sell for in 3-7 years, and what levers they can pull in between. Those levers might include margin improvement, add-on acquisitions, better pricing discipline, building a stronger leadership team, reducing founder dependence, or shifting the revenue mix toward higher-quality recurring revenue.

How PE buyers think about your exit before they buy

A private equity firm is always asking who they can sell your business to next. In renewable energy, the likely next buyers are usually one of three groups: a larger strategic, a bigger private equity fund, or an infrastructure-style investor if the business evolves toward contracted cash flows and stronger EBITDA conversion.

That is why PE buyers are sensitive to entry multiple versus exit multiple. If they buy a labor-heavy installer at a full price and cannot improve the model, the math gets tough. If they buy a specialist technical platform, improve margins, add scale, and create more predictable cash flow, they may justify a higher entry price.

They also care about your story being transferable. If your business only works because you personally know every lender, major customer, local authority, and subcontractor, that is a problem. A buyer wants a business that can keep growing after you leave.

3. Deep Dive: Development Risk vs. Contracted Cash Flow

One of the biggest valuation questions in renewable energy is this: are buyers paying for uncertain future projects, or for visible cash flow that is already largely de-risked?

That distinction shows up clearly in how the market values different business types. The public market data shows wide ranges, but the higher multiples often sit with businesses that either have strong owner-operator economics, scarce infrastructure characteristics, or enough scale and operating history to make future cash flows feel more predictable. The lower end is more common where revenue depends on project timing, permit outcomes, and one-off execution.

Why buyers care is simple. A megawatt in a slide deck is not the same thing as a megawatt with land secured, interconnection progressing, permits in place, financing lined up, construction managed, and a revenue path already visible. The more steps left, the more risk left. And more risk usually means a lower multiple.

This matters even if you are not a classic owner-operator. A developer, EPC, or service platform can still improve valuation by making the business feel less exposed to one-off outcomes. You do that by showing repeatability: conversion rates from pipeline to NTP, backlog visibility, standard project economics, disciplined margin tracking, and proof that project wins do not depend on heroic founder effort.

A second version of the same issue appears in service-heavy models. If buyers think your business is mostly selling people-hours, they worry about cyclicality and margin pressure. If they think your business reduces risk, compresses timelines, or solves a technically hard problem in a repeatable way, they are more likely to pay up.

Lower-value profile vs higher-value profile

If your business looks more like the left column today, the goal is not to reinvent the company overnight. It is to move one or two steps right before sale - better backlog quality, tighter reporting, cleaner margin proof, and more evidence that the business is repeatable without constant founder intervention.

4. What Renewable Energy Businesses Sell For - and What Public Markets Show

Here is what the data actually says: renewable energy is not a single multiple market. Public market valuations are much higher on average than private deal valuations, but they also cover very different business models, scales, and risk profiles. Private transactions, especially in services, EPC, and installation-heavy businesses, are often much lower.

That is why you should use market data as a range-setting tool, not as a price tag. The key question is not "what is the industry multiple?" It is "which part of the industry do I actually resemble?"

4.1 Private Market Deals (Similar Acquisitions)

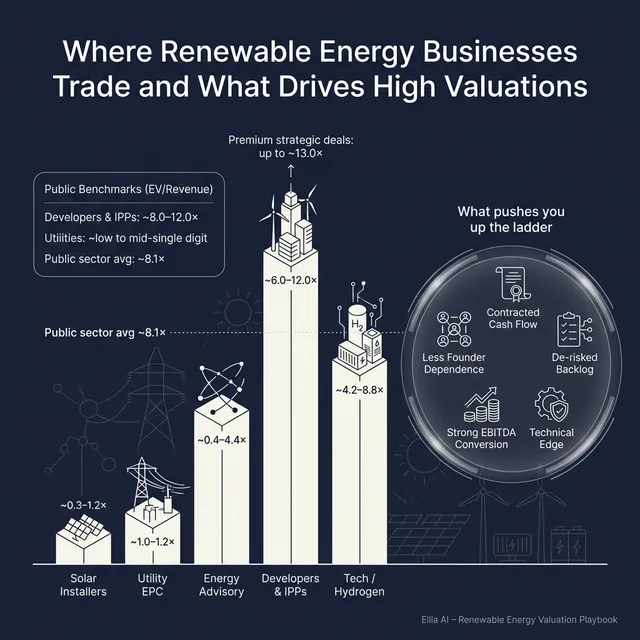

Across the precedent transactions provided, the overall average private multiple is 2.3x EV/Revenue and the median is 0.9x. On EV/EBITDA, the overall average is 12.7x and the median is 7.3x. That spread tells you something important: a few premium deals pull the average up, but many real-world transactions happen at much more modest levels.

The lowest private revenue multiples in the dataset are mostly tied to installer, EPC, and execution-led businesses. Local solar installers and integrators often sit around 0.3x to 1.2x revenue. Utility-scale EPC and grid interconnection deals are usually around 1.0x to 1.2x revenue. By contrast, specialist advisory and technology businesses can move much higher, with clean energy advisory around 4.2x revenue and hydrogen technology reaching 8.8x revenue and 29.3x EBITDA.

The practical lesson is straightforward. If your business is mostly project execution, buyers usually will not value it like a technology platform. If your business combines execution with specialist know-how, recurring service revenue, or hard-to-replace technical capability, you may pull toward the top of the range.

4.2 Public Companies

The public company set is much richer and much noisier. As of mid to late 2025, the overall public group in your data traded at an average of 8.1x EV/Revenue and 23.8x EV/EBITDA, with medians of 5.5x and 14.1x respectively. That is far above the private market averages, but it includes large owner-operators, diversified utilities, and high-growth renewable platforms with more scale, financing access, and liquidity.

The most relevant public reference groups for many privately held renewable businesses are the renewable project developers and IPPs, plus the European and Nordic developers and asset managers. Those groups broadly support mid-single-digit to low-teens revenue multiples, but there is huge dispersion depending on growth, profitability, scale, and how much of the story is contracted operating cash flow versus earlier-stage development.

Founders should use these public multiples carefully. They are useful as an upper and lower reference band, especially when they are broken into the right subgroups. But they are not direct private market price tags. A smaller private business should usually be adjusted downward for lack of scale, lower liquidity, more customer or project concentration, and greater execution risk.

That said, there are exceptions. If your company is scarce, strategically important, technically differentiated, or has unusually visible future cash flow, a buyer may stretch beyond where a simple "small private company discount" would suggest.

5. What Drives High Valuations (Premium Valuation Drivers)

The premium outcomes in your data are not random. They tend to cluster around a few themes.

Differentiated know-how, not just project capacity

The strongest premium pattern in the private deals is specialist knowledge or IP. In your dataset, the deals that really break away from ordinary installer and EPC multiples are the ones tied to technical advisory depth, hydrogen technology, or a more defensible engineering and risk-reduction proposition.

Buyers pay more for this because scarce expertise is harder to replace than project labor. A founder can relate to this easily: if customers hire you because you solve a complex interconnection problem, de-risk battery integration, shorten development timelines, or give lenders comfort around technical performance, that is worth more than simply showing up with crews.

Examples:

- A technical advisory layer that customers reuse across projects

- A repeatable toolchain for development, siting, or performance optimization

- Proprietary hydrogen, storage, or system integration know-how

More visible, higher-quality revenue

Renewable businesses with clearer future revenue streams usually get more buyer confidence. That can mean contracted operating revenue, strong backlog, asset management contracts, long-term O&M agreements, or a development machine with credible conversion history.

Buyers pay more because they are underwriting less uncertainty. A business with repeat revenue from managing or operating assets is easier to value than one that depends on each next project win.

Examples:

- Multi-year asset management or O&M contracts

- A development pipeline with clear stage gates and real conversion data

- Recurring service revenue attached to installed assets

Strong EBITDA conversion and cash generation

Some premium outcomes come from businesses that turn revenue into EBITDA efficiently. That does not mean every high-multiple renewable business must already be highly profitable, but it does mean buyers want proof that the model can convert scale into cash.

This is especially true for larger strategic and infrastructure-minded buyers. If they can see immediate earnings contribution, the asset becomes easier to justify internally.

Examples:

- Strong gross margins plus disciplined overhead

- Projects or services that produce repeatable contribution margin

- Clear evidence that growth is not destroying cash

Risk reduction buyers can explain to their investment committee

A premium business helps the buyer feel safer, faster, or smarter. The data supports this in specialist advisory and engineering-led businesses where deep technical teams reduce execution, supply chain, quality, and ESG risk.

That is valuable because buyers are not only buying revenue - they are buying fewer surprises.

Examples:

- In-house engineering depth with sector reputation

- Strong quality assurance and supplier management

- A track record of navigating permitting, grid, and compliance complexity

Scarcity and strategic fit

Some businesses are worth more because the buyer cannot easily find another one like them. That might be a unique regional footprint, a rare capability in storage or hydrogen, a strong community solar channel, or a hard-won customer base with utilities, corporates, or public sector buyers.

Scarcity matters because competitive tension matters. If more than one buyer sees you as strategically important, valuation usually improves.

Clean financials and management credibility

This is not glamorous, but it matters in every deal. Buyers pay more when they trust the numbers, understand the margins by business line, and believe the leadership team can operate after closing.

A premium company usually has:

- Clean monthly reporting

- Clear backlog and pipeline definitions

- Margin visibility by project type or service line

- A team that is deeper than the founder alone

6. Discount Drivers (What Lowers Multiples)

The most common reason renewable businesses miss the top of the range is simple: buyers see too much uncertainty relative to the quality of the earnings.

A business tends to trade lower when revenue is one-time, margins swing sharply from project to project, and too much depends on timing, policy, or a small number of people. That does not make the business bad. It just makes it harder to underwrite.

The private deal data shows this clearly in installer and EPC-style businesses. Those companies can still be attractive acquisitions, but buyers usually value them more conservatively because revenue can be labor-led, local, competitive, and exposed to project timing.

Common discount drivers include:

- Too much one-off project revenue and not enough recurring service or operating income

- Weak gross margin discipline or inability to show profitability by segment

- Heavy customer concentration, especially one utility, one EPC partner, or one key developer

- Founder dependence in relationships, origination, pricing, or execution

- Pipeline that looks large but is poorly evidenced

- Permitting, interconnection, or land issues that are not fully surfaced

- Aggressive forecasts with little historic proof

- Working capital pressure, especially where project timing creates cash swings

- Exposure to subsidy, tariff, or policy changes without diversification

- Equipment or subcontractor risk concentrated in a few vendors

There are also sector-specific discount issues buyers often spot fast. One is backlog quality. A large stated backlog does not help much if buyers think it is full of soft opportunities or underpriced work. Another is mix confusion. If you present as a platform business but the economics look like a contractor, buyers will usually default to the lower category.

The good news is that many of these discounts are fixable, or at least explainable, before a sale. Buyers do not need perfection. They need clarity.

7. Valuation Example: A Renewable Energy Company

To show how valuation logic works in practice, let us use a fictional company called NorthGrid Renewables. This is not a real company, and the revenue number is fictional. Assume NorthGrid has USD 10m of annual revenue and operates as a mid-sized renewable energy platform combining development, EPC oversight, and long-term asset management for solar and storage projects.

This example is illustrative only. It is not investment advice, not a fairness opinion, and not a formal valuation.

Step 1: Start with the closest market reference points

The most relevant public comp logic in your source set points to two close public groups:

- Renewable project developers and IPPs

- European/Nordic renewable developers and asset managers

The worked logic provided for a real business at fictional USD 10m revenue supports a broad revenue-based range of about 6x to 12x, with the upper end extending to roughly 13x in a stronger case. The reason for narrowing the range is sensible: this kind of business is still an execution and project-risk business, not a software company, so it should not automatically get the highest market multiples. But if it has operating history, real assets under management, and a credible de-risked platform, it can still sit in the upper half of the relevant comp band.

Step 2: Apply that logic to the fictional company

Assume NorthGrid has these characteristics:

- USD 10m revenue

- Good regional track record in solar plus storage

- Some recurring asset management and O&M revenue

- Decent but not spectacular margins

- Clear project pipeline, but not all of it fully de-risked

- Moderate founder dependence

- No obvious proprietary technology

That profile probably supports a solid core case, but not the absolute top end.

What would push NorthGrid down?

A lower-end case would be more likely if recurring revenue is limited, the pipeline is early-stage, margins are thin, or too much of the business still looks like project execution. In that case, buyers might lean toward 4x-6x revenue, or USD 40-60m.

What would push NorthGrid up?

A premium case becomes more plausible if NorthGrid can prove more visible cash flow, stronger EBITDA conversion, deeper management, and a more differentiated technical position. If buyers see it less like a contractor and more like a regional platform with repeatable development and operating economics, a 9x-12x or even 13x revenue outcome becomes easier to defend.

What founders should take from this

Two renewable businesses with the same USD 10m revenue can have very different values. One might be worth USD 45m. Another might be worth USD 110m or more. The gap is usually not caused by accounting tricks. It is caused by buyer confidence in future cash flow, scarcity, and risk.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple way to use this playbook is to score your business honestly. Give yourself 0, 1, or 2 points on each factor.

- 0 = weak / unclear

- 1 = decent / mixed

- 2 = strong / clearly evidenced

How to interpret the score

- 18-24 points: You are moving toward the premium end. Buyers can likely tell a clear quality story.

- 10-17 points: You are in fair-market territory. A good process matters a lot because the story can go either way.

- 0-9 points: You probably have more work to do before sale, or you should expect buyers to price in meaningful discounts.

The point of this exercise is not to flatter yourself. It is to spot where one or two improvements could make the biggest difference.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Founders often assume the market will "see the value" if they just start conversations. Usually it does not work that way. If your numbers are messy, your pipeline is hard to verify, and your story is not well framed, buyers will fill in the blanks with caution.

The second mistake is hiding problems. In renewable energy, issues around permits, interconnection, contract quality, margin leakage, or customer concentration almost always come out in diligence. When they surface late, the damage is worse than if you had addressed them early. Buyers can live with problems. They hate surprises.

The third is weak financial records. Many renewable businesses do not clearly separate development revenue, EPC revenue, recurring service revenue, project margins, and overhead. That makes it harder for buyers to understand the real earnings power of the company. Often there is low-hanging fruit here in the 6-12 months before a sale.

The fourth mistake is running a weak, unstructured sale process. Research finds seller advisers can improve private-seller deal valuations, and strong market canvassing and real price discovery matter to establishing fair value. (SSRN) In practice, founders often treat an advisor-led competitive process as capable of lifting price meaningfully - often around 25% versus a poorly run process - because more qualified buyers see the deal, more tension is created, and weaker bids are exposed faster. The exact uplift is never guaranteed, but the logic is real. (SSRN)

The fifth mistake is revealing the price you want too early. If you tell buyers you want a USD 10m enterprise value, many of them will stop doing their own best work and simply cluster around that anchor. You kill price discovery. In M&A research, anchoring effects clearly matter in negotiated outcomes. (Harvard Business School)

There are also two renewable-specific mistakes worth calling out. One is overselling pipeline quality. Buyers know that a 500 MW pipeline can be worth very different things depending on stage, grid, land, and permit reality. The other is failing to explain storage, hybrid, or hydrogen exposure in a disciplined way. If it sounds like optional upside with no proof, buyers usually give it little value.

10. What Renewable Energy Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers actually underwrite

Start by cleaning up your reporting. Separate revenue by business line. Show gross margin by project type or service type. Track backlog, pipeline stage, conversion, and working capital clearly.

If you can improve even one thing here - margin visibility, recurring revenue reporting, backlog quality, or cash conversion - you make the business easier to price.

Improve revenue quality, not just revenue volume

Do not chase growth at any cost before a sale. In this sector, USD 1 of recurring asset management, O&M, or clearly contracted revenue is usually worth more than USD 1 of low-margin, one-off execution work.

Practical moves:

- Lock in multi-year service contracts where possible

- Tighten pricing discipline on project work

- Exit or reduce low-quality revenue that creates noise but not value

De-risk the development story

If you are a developer or hybrid platform, turn soft pipeline into hard evidence. Buyers want to know what stage each project is at, what has been secured, and what still stands in the way.

Practical moves:

- Standardize pipeline stage definitions

- Document permit, land, and interconnection status clearly

- Show historic conversion rates by stage, not just total headline MW

Show that the business works without you

A founder-dependent business can still sell, but it rarely sells as well as a business with visible management depth.

Practical moves:

- Push key customer ownership into the team

- Build a second layer under you

- Document commercial, project, and financial processes

- Make sure at least a few leaders are strong enough to stay and grow the business post-close

Strengthen the premium story

Think hard about what makes your business genuinely scarce. Is it technical depth, regional permitting success, battery integration capability, utility relationships, commercial channel access, or a strong owner-operator model?

Then make that advantage visible. Buyers do not pay premium prices for vague strengths. They pay for strengths they can underwrite.

Prepare for diligence before going to market

Good exits are often won before the first buyer call. Create a clean data room. Reconcile the financials. Surface the weak points yourself. Fix what is fixable and frame what is not.

That alone can protect value because it reduces late-stage renegotiation.

11. How an AI-Native M&A Advisor Helps

The biggest advantage of an AI-native M&A advisor is buyer reach. Instead of limiting your process to a small list of obvious names, AI can help map hundreds of relevant buyers using deal history, synergies, financial capacity, sector focus, and other signals. That broader buyer universe usually means more competition, better offers, and a better chance the deal still closes even if one bidder drops out.

It also speeds up the process. With AI helping on buyer matching, outreach preparation, marketing materials, and diligence support, you can often reach initial conversations and offers much faster than in a manual-only process - in many cases in under 6 weeks from launch, assuming the company is prepared.

That does not replace human advice. It improves it. The best outcome still comes from experienced M&A advisors who know how to frame your business, pressure-test your numbers, handle buyer psychology, and negotiate hard points in the deal. AI simply makes that advisory work faster, broader, and more data-driven.

The result is Wall Street-grade process quality without traditional bulge-bracket cost structures. If you'd like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.