The Complete Valuation Playbook for Semiconductors Businesses

A practical guide to how semiconductor businesses are valued and what drives high multiples.

If you are thinking about selling your semiconductor business in the next 1-12 months, valuation is not just a finance exercise. It is a market-readiness exercise. In semiconductors, buyers are balancing technology value, customer relevance, supply chain risk, and future earnings power - often all at once.

That matters even more today because the sector is still seeing active consolidation, especially around RF, photonics, power, connectivity, and specialized component platforms. Strategic buyers are looking for capabilities they can plug into a larger product stack, while private equity is looking for businesses that can scale, clean up margins, and become attractive to a larger buyer later.

This guide is built to help you do three things: understand what semiconductor businesses actually sell for, see what drives higher and lower multiples, and assess where your company may fit today - plus what you can realistically improve in the next 6-12 months before going to market.

1. What Makes Semiconductors Unique

Semiconductor businesses are not valued like ordinary manufacturers, and they are not valued like software either. Buyers know they are often looking at a mix of intellectual property, design capability, customer relationships, product qualification history, and future socket wins - not just current revenue.

The sector itself is broad. Private semiconductor companies often fall into a few familiar categories: RF and mmWave component suppliers, analog or mixed-signal chip designers, photonics and optical component companies, compound semiconductor materials players, and specialized component or subsystem businesses that sit inside telecom, data center, aerospace, industrial, or defense applications. Those categories can all live under "semiconductors," but buyers do not price them the same way.

A core reason is business model shape. One semiconductor company may have a repeatable, qualified product sold into long-lived programs with strong gross margins. Another may depend on project-led engineering work, a handful of custom customer programs, or a single manufacturing partner. Both can be technically impressive. Only one usually gets paid like a premium asset.

Buyers also pay close attention to timing and maturity. A company with strong design wins but weak current EBITDA may still be valuable if those wins are near production and tied to credible customers. But a company with beautiful technology and no clear path to repeatable volume will often be marked down, even if management believes the future is bright.

The risks buyers always check in semiconductors are also more sector-specific than in many industries:

- Customer concentration and program concentration

- Exposure to one end market, such as telecom or consumer devices

- Dependency on one foundry, packaging partner, or key supplier

- Long qualification cycles and revenue timing risk

- Product obsolescence and pricing pressure

- Export controls, regulatory issues, and geopolitical exposure

- Whether know-how sits with a few engineers rather than the organization

In simple terms: buyers are not just asking, "What do you make?" They are asking, "How durable is demand, how hard is this to replace, and how safely can I scale it after I buy it?"

2. What Buyers Look For in a Semiconductors Business

At the highest level, buyers still care about the basics: scale, growth, gross margin, EBITDA, and cash generation. But in semiconductors, those basics are filtered through a different lens. Revenue quality matters more than headline revenue. Margin quality matters more than accounting margin alone. And technical differentiation matters only if it turns into commercial leverage.

Most buyers want to see a business that solves an important problem inside a larger system. That could mean RF front-end performance, photonics capability, power efficiency, signal integrity, thermal management, or a hard-to-replace design feature in a customer platform. If your component is mission-critical and painful to swap out, valuation usually improves.

They also want evidence that demand is durable. In this sector, that often means qualified products, sticky customer programs, long design-in cycles, multi-year supply expectations, and low practical churn once a part is embedded. Buyers know that a component qualified into a complex platform can be much more valuable than a commodity-like part sold through spot demand.

Profitability still matters, but the interpretation is nuanced. A buyer may tolerate current losses if your gross margins are attractive, your engineering spend is building future production revenue, and there is a credible line of sight to EBITDA improvement. The source data supports that point: some of the better-looking outcomes are tied less to flashy revenue multiples and more to buyers underwriting future EBITDA or cost improvement.

PE buyer thinking

Private equity buyers usually think in three layers.

First, they care about entry multiple versus exit multiple. If they buy you today, they need a believable case for selling the business in 3-7 years at a similar or better multiple to a larger strategic buyer, a larger private equity fund, or occasionally the public market. That means they are asking whether your business can become bigger, cleaner, and less risky over time.

Second, they care about what levers they can pull after closing. In semiconductors, that may include pricing discipline, gross margin improvement, lower overhead, better sourcing, broader channel access, add-on acquisitions, or tighter focus on the most profitable product lines and end markets.

Third, they care about management depth. If too much of the company depends on the founder, one CTO, or a handful of customer-specific relationships, PE will worry that the asset is hard to institutionalize. That does not kill a deal, but it often changes the structure - more earn-out, more rollover equity, more holdbacks, and sometimes a lower upfront valuation.

Strategic buyers think somewhat differently. They may pay more when your product fills a real gap in their portfolio, gives them a new customer set, strengthens an existing product bundle, or helps them sell a bigger solution. The precedent deals in the source set show this clearly: some of the strongest revenue multiples came when the buyer could justify integration value and near-term accretion, not just standalone cash flow.

3. Deep Dive: Design Wins, Productization, and the Path to EBITDA

One of the biggest valuation questions in semiconductors is this: are you mainly selling engineering effort, or are you building a repeatable product business with operating leverage? That distinction matters because buyers pay very differently for technical capability that scales versus technical capability that needs to be resold every quarter.

The source data points in that direction. Premium outcomes in private deals were often tied either to strategic adjacency - where a buyer could plug the asset into a larger platform - or to a believable earnings story, where buyers could justify strong EV/EBITDA even if EV/Revenue did not look extreme. In other words, the market often pays up when it can see how the business becomes more profitable after acquisition.

Why buyers care is simple. In semiconductors, revenue can look promising for years before it becomes efficient revenue. Buyers want to know whether current R&D and customer development work is turning into qualified, repeatable, margin-rich product sales. If the answer is yes, they can underwrite future EBITDA. If the answer is no, they start to worry the company is really an engineering services business wearing a semiconductor label.

A useful way to think about it is this:

Founders can move from the left side to the right side over time. Usually that means narrowing product focus, proving customer conversion from development to volume, reporting margin by product line, and showing which engineering spend supports future production revenue rather than open-ended experimentation. Buyers do not need perfection. They need a story they can believe and diligence can confirm.

A second nuance is customer concentration versus design-win quality. In many industries, concentration is automatically bad. In semiconductors, that is not always true. If a large share of revenue comes from a deeply embedded, sticky, long-life program with a credible customer and strong margin, buyers may tolerate more concentration than they would in a simple distribution business. But if the revenue depends on one unproven program, one unstable customer, or one delayed qualification cycle, the same concentration becomes a serious discount.

4. What Semiconductors Businesses Sell For - and What Public Markets Show

The headline lesson from the data is that semiconductor and adjacent component businesses do not trade on one clean multiple. Public market valuations are wide, and private transaction multiples are generally lower and more grounded. The right valuation band depends heavily on product type, scale, profitability, end-market exposure, and whether a buyer sees strategic fit.

The public data set is broad and includes some clear outliers, especially in photonics and niche optics. The private deal set is more conservative and, for most founder-owned businesses, is often the better starting point. Public multiples are still useful - but more as boundary markers than as direct price tags.

4.1 Private Market Deals (Similar Acquisitions)

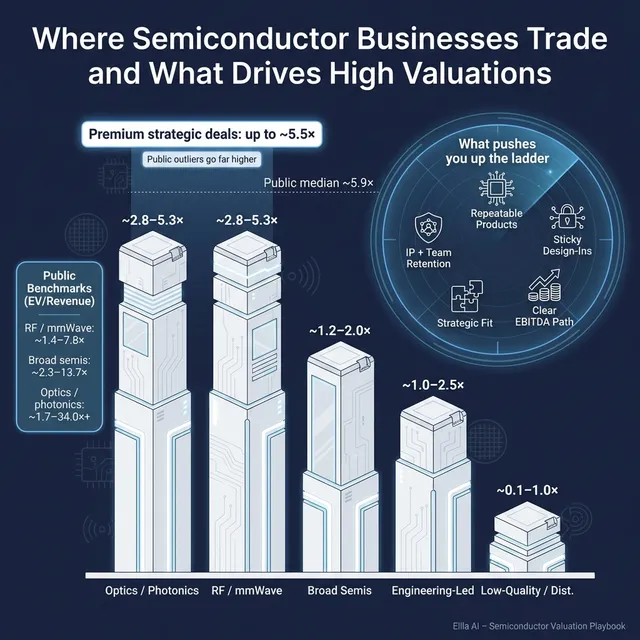

The precedent transactions point to an overall private market average of about 2.0x EV/Revenue and a median of about 1.2x EV/Revenue, with average EV/EBITDA of 11.1x and median 10.6x.

Within that, the better outcomes came from businesses that looked strategically important or had a clear earnings case. In the source deals, capability-driven optics and semiconductor-adjacent transactions reached roughly 2.8x to 5.3x revenue, while more distribution-led, services-heavy, or lower-quality assets sat much lower, sometimes around 1.0x revenue or below. The pattern is straightforward: buyers pay more when the asset strengthens a portfolio, improves product breadth, or carries credible margin potential.

A founder should read those numbers carefully. They are not saying "all semiconductor companies sell at 1-2x revenue." They are saying that private deal reality is usually more conservative than public market chatter, and that premium outcomes need a reason. In this data set, that reason is usually strategic importance, scale, cleaner earnings potential, or both.

4.2 Public Companies

The public group data is much broader and more volatile. Across the full set, average public EV/Revenue is 14.0x and median is 5.9x, while average EV/EBITDA is 54.1x and median is 31.0x. Those averages are lifted by very high-multiple outliers, especially in certain optical and photonics names. For most private founders, the median is the more useful reference point.

At the segment level, the clearest pattern is this: broad, scaled semiconductor platforms and strong specialty component businesses generally trade above the weakest RF or hardware peers, but not every "semiconductor" label earns a premium. Growth, gross margin, product defensibility, and the market's confidence in future earnings all influence the result.

These public multiples are best thought of as a reference band for mid to late 2025, not a direct answer for your company. Public businesses are usually larger, more liquid, and followed by investors every quarter. A private company is typically adjusted downward for smaller scale, less liquidity, thinner management, higher customer concentration, and more diligence risk.

That said, there are situations where a private company can push toward the upper end of a sensible range. If you own a scarce capability, fit neatly into a strategic acquirer's roadmap, and can show a believable path to margin improvement, buyers may stretch beyond what a plain vanilla comp screen would suggest.

5. What Drives High Valuations (Premium Valuation Drivers)

The source data gives a useful message: premium outcomes in this sector are rarely about "good story" alone. They usually happen when a buyer can justify more value than the seller's standalone financials suggest.

Strategic fit that is obvious, not vague

This is the strongest premium driver in the source deals. Buyers paid more when the asset strengthened an existing platform - for example by filling a product gap, deepening a photonics stack, expanding into a useful RF adjacency, or adding technology that could be bundled into a larger solution.

Why it matters: a strategic buyer is not only valuing your current revenue. They are valuing cross-sell potential, installed base leverage, faster product roadmap execution, and the chance to win more business because your capability is now part of a broader offering.

A founder-friendly way to frame this is: are you a nice technology, or are you a missing puzzle piece for a larger player?

A credible path to EBITDA improvement

The data also shows that some better outcomes were driven more by earnings logic than by revenue hype. Buyers were willing to support strong EV/EBITDA outcomes when they believed margins could improve through scale, cost takeout, product mix, or integration.

Why buyers pay more for this: semiconductor buyers know near-term reported EBITDA can be misleading if the business is still investing in R&D, scaling manufacturing, or carrying duplicated overhead. If they can see how your current profile becomes more efficient after closing, valuation can improve.

Practical examples:

- Product lines with high gross margin but under-absorbed overhead

- Revenue growth that is about to drop through to EBITDA

- Clear segment reporting showing which products are already economically attractive

Enough scale to matter

Scale showed up clearly in the source set. Higher revenue multiples tended to be easier to justify when the business was big enough for an acquirer to absorb meaningfully and when the buyer could state that the deal would be accretive in a reasonable timeframe.

Why buyers care: tiny assets create friction. Integration effort, diligence cost, management time, and customer transition risk can be almost as high for a small deal as for a mid-sized one. A buyer will pay more when your revenue base is large enough to matter and stable enough to model.

This does not mean small companies cannot sell well. It means smaller companies usually need sharper differentiation to offset their size.

Management continuity and technical retention

Several source deals included founder retention, rollover equity, lock-ups, or earn-outs. That is common in semiconductors because so much value can sit inside specialized engineering knowledge, customer relationships, or product roadmaps.

Why buyers pay more for this: if your value is concentrated in people and technical know-how, continuity reduces risk. A buyer may be willing to stretch on headline value if the key team is staying and incentives are aligned.

For founders, this often means valuation is not just about price. Structure matters. Earn-outs, equity rollover, and retention packages can be tools that increase effective value, especially when the buyer wants your team as much as your revenue.

Clean deal perimeter and diligence readiness

The source data highlights clean debt-free and cash-free structures with normal working capital assumptions. That may sound technical, but the principle is simple: buyers pay more when they trust what they are buying.

Why this moves value: a messy balance sheet, unclear inventory treatment, fuzzy transfer pricing, or confusing carve-out financials forces a buyer to price in risk. A cleaner company gets tighter bids and fewer surprises late in the process.

Practical examples:

- Clear working capital targets

- Product-level margin visibility

- Clean inventory reserves and warranty treatment

- Clear separation of one-time engineering revenue versus repeat production revenue

High-quality revenue in mission-critical applications

Even where the source set does not spell this out numerically, it is a classic semiconductor premium driver. Buyers pay more for revenue tied to difficult qualifications, long product lives, regulated or high-reliability applications, and performance that is hard to replace.

Examples include:

- Aerospace and defense programs

- Industrial platforms with long design cycles

- Data center and optical infrastructure applications where qualification matters

- RF or power components where redesign is painful and risky

Basic but powerful value drivers still matter

Some premium drivers are not glamorous, but they work:

- Clean monthly financials

- Diversified customers

- Strong gross margins

- Predictable bookings and backlog

- Low churn once designed in

- A real leadership bench beyond the founder

These do not create a premium story on their own. But they make every other premium story easier to believe.

6. Discount Drivers (What Lowers Multiples)

Most discounted outcomes are not caused by one fatal flaw. They come from a pile of risks that make a buyer less certain. In semiconductors, uncertainty gets priced fast.

A common discount driver is weak revenue quality. That can mean too much project work, customer-funded development with no repeat production, one-time inventory pulls, distributor-driven volatility, or programs that are always "about to ramp" but never do. Buyers will not pay premium multiples for revenue they cannot trust.

Another major issue is loss-making performance without a believable bridge to profitability. Losses alone do not kill value. But losses with unclear product economics, heavy fixed cost, and no visible EBITDA inflection usually drag multiples down. The worked company logic in the source material makes this point directly: a small, loss-making hardware semiconductor business should usually sit below premium software-like valuations and below the most optimistic public photonics comps.

Customer and program concentration are also frequent discounts. If one customer, one OEM, or one design win drives too much of the story, buyers will worry about negotiation power and fragility. This is especially true when the customer relationship sits heavily with the founder or one salesperson.

Supply chain exposure can also lower value. If your business depends on one foundry, one packaging route, one critical material, or a fragile overseas supply chain, buyers will test that hard in diligence. The same goes for export control risk, sanctions exposure, or heavy dependence on geopolitically sensitive end markets.

Other common discount factors include:

- Unclear intellectual property ownership

- Weak quality systems or inconsistent yields

- Inventory issues and obsolete stock

- No clear margin reporting by product line

- Founder-centric management

- Aggressive forecasting unsupported by orders or design-win evidence

- Poor financial controls and long closes

The good news is that many discounts are fixable. Buyers do not require perfection. They require transparency, evidence, and fewer avoidable surprises.

7. Valuation Example: A Semiconductors Company

Let’s turn the logic into a practical example.

Assume a fictional company called VectorBeam Technologies. It designs RF and photonic semiconductor components for telecom infrastructure and industrial connectivity applications. It has USD 10m of revenue, strong gross margin, growing customer interest, but is still around break-even to modestly loss-making at EBITDA because it continues to invest in engineering and commercialization.

This company is fictional. The revenue level is fictional. The valuation ranges below are illustrative only - not investment advice and not a formal valuation.

Step 1: How the logic works

The right starting point is not the highest public multiple you can find. It is the closest set of comparable businesses by product type, scale, and maturity.

For a business like VectorBeam, the best anchors are usually:

- Private semiconductor, optics, and component acquisitions

- Public RF, specialty component, and selected photonics names

- A discount to the most stretched public comps if the company is smaller and not yet solidly profitable

The source logic for a real semiconductor case points to a sensible rule: a sub-scale, loss-making hardware component business should usually sit in a more grounded revenue multiple band than larger, profitable, or strategically exceptional public names. Applied to a fictional USD 10m revenue company, a practical core range might be around 2.5x to 4.2x revenue, with upside only if premium drivers are strong and downside if risks are high.

Step 2: Apply it to the fictional company

Assume VectorBeam has these characteristics:

- USD 10m revenue

- Gross margin around 65%-70%

- Several meaningful design wins

- Revenue still somewhat concentrated

- EBITDA slightly negative because of ongoing R&D

- Strong technology, but not yet broad market scale

That leads to the following illustrative valuation view:

Why each case could happen

Discounted case - 2.0x to 2.5xThis is where the business may land if revenue is too concentrated, EBITDA losses are widening, production ramp timing is uncertain, or too much of the story depends on future wins that are not yet well evidenced.

Core range - 2.5x to 4.2xThis is the most defensible band for many sub-scale private semiconductor businesses with strong technology but incomplete maturity. It reflects good product value, decent margins, and some strategic relevance - but also acknowledges private-market discounts for size, liquidity, and risk.

Premium case - 4.5x to 5.5xThis usually requires more than good technology. You would want clear strategic fit for a larger buyer, visible production ramps, customer validation, cleaner EBITDA trajectory, and ideally a profile where the acquirer can explain synergies or accretion quickly.

Step 3: What this means for founders

Two semiconductor businesses with the same USD 10m of revenue can be worth very different amounts. One may be seen as an interesting engineering shop with uncertain scaling. Another may be seen as a strategic capability bolt-on with durable product revenue and margin upside.

That is why valuation work matters before the sale process starts. The goal is not to "spin" the company. The goal is to make the real quality of the business easier for buyers to see - and easier for them to underwrite.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple self-assessment can help you estimate whether your business is closer to the low end, middle, or premium end of the market. Score each line 0, 1, or 2. Be honest. This is most useful when it is uncomfortable.

How to interpret your score

10-12 pointsYou are closer to premium territory. That does not guarantee a premium multiple, but it means your story is more likely to support strong buyer interest and tighter valuation ranges.

6-9 pointsYou are in fair-market territory. This is where many good private semiconductor businesses sit. A strong process and a few targeted fixes can make a meaningful difference.

0-5 pointsYou may still be sellable, but buyers are likely to focus on risk. In that case, a 6-12 month preparation period can have a real payoff.

The point of this exercise is not self-judgment. It is to identify where improvements can move value most.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often start talking to buyers before the numbers, story, and process are ready. In semiconductors, that is especially dangerous because buyers will ask hard questions about margins, design wins, supply chain, and program timing. If your answers are not organized, they assume the risk is higher than it may really be.

Another major mistake is hiding problems. Maybe a program slipped. Maybe a customer is at risk. Maybe there is inventory that should have been reserved more aggressively. These issues almost always surface in diligence. When they do, trust drops, leverage disappears, and value often falls faster than the original problem justified.

Weak financial records are also costly. Many private semiconductor companies have decent accounting, but not decision-grade reporting. Buyers want to understand revenue by product line, gross margin by customer or family, R&D intensity, backlog quality, and where EBITDA can improve. If those basics are unclear, buyers either lower price or use structure to protect themselves.

A very common error is running an unstructured sale process. Good businesses can get sold badly. Research across M&A markets consistently shows that a structured, competitive process with an advisor tends to produce meaningfully higher prices - often around 25% higher - because more buyers see the opportunity, competitive pressure improves offers, and the story is framed professionally. In a sector as technical as semiconductors, that process advantage can be even more important.

Another avoidable mistake is revealing what price you want too early. If you tell buyers you are hoping for, say, USD 40m of enterprise value, many of them will anchor around that number instead of telling you what they would pay in a competitive setting. You kill price discovery. Instead of learning that one buyer may value your business at USD 48m or USD 55m because of strategic fit, you may get a cluster of offers just above the number you volunteered.

Two industry-specific mistakes also show up often:

First, overselling pipeline as if it were production revenue. Buyers know the difference between evaluation, design win, qualification, and real volume. Blurring those stages hurts credibility.

Second, failing to explain the supply chain and manufacturing model clearly. If a buyer cannot quickly understand your foundry strategy, packaging path, yields, inventory discipline, and second-source risk, they start pricing in worst-case assumptions.

10. What Semiconductors Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers care about most

Start by improving reporting, not just performance. Break revenue into clear buckets: production revenue, NRE or development revenue, repeat versus one-time sales, and major product families. Show gross margin and contribution logic cleanly. If buyers can see where the real economics are, valuation discussions become easier and more credible.

Also work on the clearest bridge to EBITDA. You do not need to become highly profitable overnight. But you should be able to show how revenue growth, product mix, pricing, or operating discipline can improve earnings over the next 12-24 months.

Improve revenue quality and reduce buyer fear

Focus on converting technical traction into commercial proof. Tighten the evidence around design wins, qualifications, backlog, and production ramps. Buyers respond better to a smaller set of well-documented opportunities than to a giant pipeline slide with no proof.

If customer concentration is high, try to broaden it where realistic. If that is not possible in the timeframe, at least document why the concentrated revenue is sticky, how long the program life is, and what switching costs protect it.

Make the business easier to buy

Clean up working capital, inventory reporting, and contract visibility. If there are carve-out issues, related-party items, or messy balance sheet questions, address them before launching a process. The source data suggests clean deal perimeter matters more than many founders realize.

You should also strengthen management continuity. Identify who owns product, operations, finance, quality, and customer relationships. If the entire company still routes through you, buyers will discount that risk.

Build a sharper strategic narrative

Do not just describe your technology. Describe why a specific type of acquirer would care. Which portfolio gap do you fill? Which customer access do you unlock? Which product bundle becomes stronger with your capability inside it?

This is where many founders leave money on the table. Technology alone is rarely enough. Strategic relevance is what gets buyers to stretch.

Fix avoidable diligence issues

In the next 6-12 months, practical wins can matter a lot:

- Shorten month-end close time

- Tighten forecasts to actuals

- Document IP ownership clearly

- Improve supply chain mapping

- Separate one-time engineering work from recurring product revenue

- Prepare a clean story for yields, quality, and warranty exposure

These are not glamorous projects. They are valuation projects.

11. How an AI-Native M&A Advisor Helps

Selling a semiconductor business is partly about finding the right buyer, and partly about running the right process. An AI-native M&A advisor helps on both fronts. Instead of reaching a limited buyer list, AI can expand the universe to hundreds of qualified acquirers based on deal history, product adjacency, synergies, buyer capacity, and strategic fit. More relevant buyers mean more competition, stronger offers, and a better chance the deal closes even if one buyer drops out.

It also speeds up the early stages of the process. With AI-assisted buyer matching, faster preparation of marketing materials, and more efficient support during diligence, initial conversations and first offers can often be reached in under 6 weeks. That matters because momentum is a real asset in M&A.

The best version of this is not AI instead of advisors. It is expert human advisors enhanced by AI. You still want experienced M&A professionals who know how to position the company, manage buyer psychology, structure the process, and negotiate the hard moments. AI simply helps them do that with broader reach, better data, and far more speed.

The result is advisory quality that feels institutional without the traditional bulge-bracket cost base. If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.