The Complete Valuation Playbook for Technology Consulting Businesses

A practical to how technology consulting businesses are valued today and what drives high multiples.

If you run a privately held technology consulting business and are thinking about a sale in the next 1-12 months, valuation is not just a finance exercise. It is the market's judgment on your growth, your margins, your customer quality, your delivery model, and how easy it is for a buyer to believe the story.

That matters right now because technology consulting is in an active but selective market. Strategic buyers and private equity still want cloud, data, AI, cybersecurity, and platform implementation capabilities - but they are much less willing to pay for vague positioning or low-quality revenue. Buyers are rewarding proof, not promises.

This playbook is built to help you do three things: understand what technology consulting businesses actually sell for, see what drives higher versus lower multiples, and assess where your business may fit today - plus what you can realistically improve in the next 6-12 months.

1. What Makes Technology Consulting Unique

Technology consulting is a broad label, and buyers know that not all firms in the category are equal. Some businesses are mostly custom software and digital engineering shops. Some focus on cloud migration, data and AI, cybersecurity, quality assurance, or managed services. Others are vertical specialists in areas like financial services, energy, healthcare, or government.

That mix matters because buyers value technology consulting firms very differently depending on what is really being sold. A business built on time-and-materials projects with a few key client relationships will be valued differently from one with recurring managed services, deep platform credentials, or a strong foothold in a regulated vertical. On paper both may be "tech consulting," but economically they are not the same asset.

The cost structure is also different from many other industries. Your main cost is people. That means utilization, delivery discipline, bench management, staff retention, and pricing power have a direct impact on valuation. A buyer will look closely at whether profits come from a repeatable operating model or simply from founders working harder than everyone else.

The main risk factors buyers always check include customer concentration, dependence on founder-led sales, weak second-line management, revenue tied to short-term projects, margin volatility, and attrition of key technical staff. In this sector, buyers also care about whether your expertise is truly differentiated or whether it can be replaced by dozens of similar firms with cheaper delivery models.

2. What Buyers Look For in a Technology Consulting Business

At the simplest level, buyers care about four things: scale, growth, profitability, and risk. But in technology consulting, they judge each of those through a sector-specific lens.

Scale matters because larger firms usually have broader delivery capacity, more stable leadership, and less dependence on a handful of accounts. Growth matters because it signals market relevance, but buyers will test whether that growth comes from repeat customers, strong platform partnerships, and sector expertise - or from one-off project spikes.

Profitability matters a lot in this sector. The data shows that services-heavy businesses often do not command huge revenue multiples, but can still achieve strong EBITDA multiples when they prove real earnings quality. In plain English: buyers may not pay software-like prices for services revenue, but they will pay up for a business that converts revenue into dependable profit.

Risk is where many founder expectations break down. A buyer will discount your business if too much revenue sits with a few customers, too many deals rely on founder relationships, or too much delivery depends on key employees who may leave after closing. They also care about how "sticky" the work is. A recurring managed cloud or platform support contract is worth more than a project that needs to be re-sold every quarter.

How private equity thinks about your business

Private equity buyers are usually asking three practical questions. First, what price can they pay today and still generate a strong return later? Second, who could buy this business from them in 3-7 years? Third, what specific improvements can they make after acquisition?

That means they care about entry multiple versus exit multiple. If they buy your firm at a healthy price, they still need a believable path to sell it later to a larger strategic buyer, a larger private equity fund, or a bigger platform in the same space. They will think hard about whether your business can become part of a larger roll-up or consolidation story.

They also want clear levers. In this sector, those levers often include cross-selling new capabilities into existing accounts, improving utilization, professionalizing pricing, building more recurring managed services, adding tuck-in acquisitions, and reducing dependence on founders for sales and client delivery.

3. Deep Dive: Why Revenue Quality Matters More Than Headline Growth

In technology consulting, one of the biggest valuation questions is not "How fast are you growing?" but "What kind of revenue are you growing?" A business doing USD 10 million of revenue with clean recurring managed services, long customer relationships, and strong margins can be worth far more than another USD 10 million firm built on short-term custom projects.

The deal data supports this. Across the sector, many private transactions sit in fairly modest revenue multiple ranges. But some services businesses still achieve premium EBITDA outcomes when profitability is real and repeatable. That tells you buyers are not simply chasing top-line growth. They are paying for earnings durability.

Why do buyers care so much about revenue quality? Because in consulting, revenue can disappear fast if it is tied to a single project, a single budget cycle, or a single decision-maker. Buyers want to know whether your clients come back, whether they expand spend over time, and whether your work sits in an important part of the customer's technology stack.

This is also why ecosystem positioning alone is not enough. The data shows that being a cloud, AI, or ServiceNow specialist can help your story, but it does not guarantee a premium. Buyers still want proof that the positioning turns into repeatable delivery, good margins, and strong client retention.

A useful way to think about it is this:

If your business looks more like the left side today, the goal is not to change everything overnight. The practical move is to shift more of your revenue toward repeat customers, attach managed services where possible, document account expansion rates, and make sure at least part of your commercial engine works without you in the room.

4. What Technology Consulting Businesses Sell For - and What Public Markets Show

Here is what the data actually shows. Technology consulting businesses do not trade like software companies. Public market reference points are generally moderate, and private market outcomes vary widely depending on specialization, margins, and how recurring the revenue base feels.

For most founder-owned firms, the key takeaway is simple: your likely valuation sits inside a services range, not a software range. That range can still be attractive, but the difference between the low end and high end is driven by quality of earnings, customer stickiness, and strategic relevance.

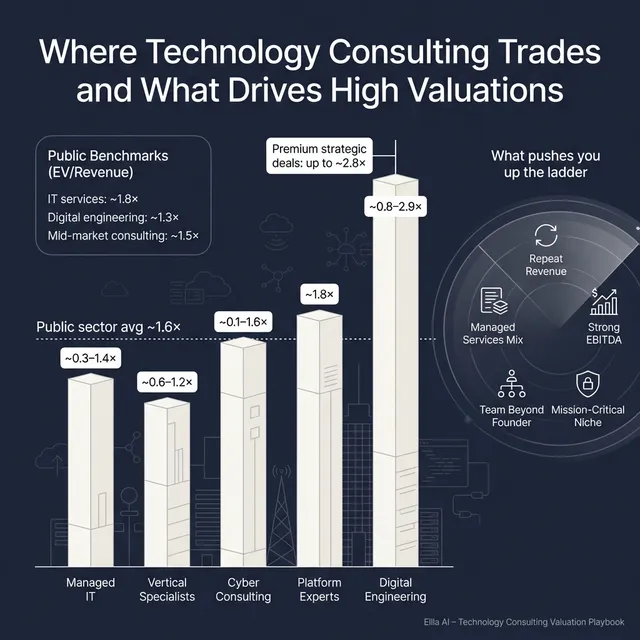

4.1 Private Market Deals (Similar Acquisitions)

The private deal data shows a broad overall average and median of about 1.6x and 1.2x EV/revenue, respectively, across precedent transactions. But that overall number hides very different outcomes across subsegments. Full-scope digital engineering and IT services deals in the data range from roughly 0.5x to 2.9x revenue, with a few outliers and data-quality issues that should be treated carefully. Managed IT and infrastructure-heavy deals are generally lower, while stronger digital engineering and niche specialist firms can push higher.

The pattern is also clear that strong EBITDA can matter as much as headline revenue. Several services businesses with only moderate revenue multiples still achieved EV/EBITDA in the mid-to-high teens when margins were credible and the acquirer could underwrite near-term earnings. That is a classic consulting-sector pattern.

These ranges are illustrative, not a guaranteed price list. A smaller founder-led firm with weak margins may land below the headline averages, while a scarce, high-retention, high-margin specialist can push toward the top end or beyond it.

4.2 Public Companies

As of mid-to-late 2025, the public market reference set for technology consulting and adjacent IT services traded at about 1.6x average EV/revenue and 17.8x average EV/EBITDA overall, with median figures closer to 1.2x EV/revenue and 9.3x EV/EBITDA. That tells you public markets are not generally putting software-style revenue multiples on this category.

Within the public data, global diversified IT services firms tend to trade around roughly 1.5x - 2.0x revenue on average, with stronger large-scale names pushing above that. Digital engineering and product development specialists show a wider spread, with weaker subscale names trading below 1.0x and better growth names trading above 2.0x. SMB and mid-market consulting firms are also mixed, ranging from weak sub-1.0x profiles to better-positioned firms above 2.0x revenue.

*That EV/EBITDA figure is distorted by outliers and should be used cautiously.

Founders should use public multiples as reference bands, not as a direct price tag for a private company. Public firms are usually larger, more diversified, more liquid, and easier to diligence. A private business is often adjusted downward for smaller scale, founder dependence, lower growth, or customer concentration.

That said, public multiples are still helpful. They show what the market broadly thinks of different technology consulting models. If your business has scarce capabilities, strong margins, and strategic fit for a buyer, you may outperform the broad averages. If it is project-heavy, thin-margin, or generic, public references will not save the valuation.

5. What Drives High Valuations (Premium Valuation Drivers)

The best valuations in technology consulting usually come from a mix of strategic relevance and earnings quality. Buyers pay more when they can clearly see why your business matters and why the economics are durable.

5.1 Strong profitability that is clearly documented

The deal data shows one of the most important patterns in this sector: premium outcomes often show up more in EBITDA multiples than in revenue multiples. That means buyers reward firms that prove they can turn revenue into dependable profit.

In practice, that looks like strong utilization, disciplined pricing, sensible delivery management, and margins that are not artificially boosted by underpaying founders or skipping key costs. Buyers especially like businesses where profitability is clearly documented and the deal is accretive - meaning it adds to the acquirer's earnings quickly after closing.

5.2 Repeatable revenue, not just busy revenue

A buyer will pay more for revenue that feels likely to stay. In this sector, that often means recurring managed services, support retainers, platform optimization work, long-standing accounts, or customer relationships that expand over time.

For example, a cloud consultancy that lands a migration project and then keeps the client for optimization, cost governance, security, and managed support is usually more valuable than a firm that just completes the initial project and moves on.

5.3 Specialization in mission-critical work

The data suggests that specialization in regulated or mission-critical environments can support better outcomes - but only when backed by real economics. Buyers like firms that sit close to core workflows in areas such as financial services, energy trading, government, healthcare, cybersecurity, or major enterprise platforms.

Why? Because customers are slower to switch, the work is harder to commoditize, and the buyer can often build a bigger platform around that expertise. But specialization by itself is not enough. It has to translate into retention, margins, and a believable growth story.

5.4 Ecosystem credibility with proof behind it

Being known for ServiceNow, AWS, Azure, Salesforce, Google Cloud, cybersecurity tooling, or AI implementation can help. It gives buyers a quick way to understand your market position and where future pipeline may come from.

But the data also shows that ecosystem adjacency is a supporting factor, not a guaranteed premium. Buyers still want hard proof: repeatable implementation playbooks, referenceable customers, strong certifications, healthy gross margins, and a track record of turning partnerships into revenue.

5.5 A business that works beyond the founder

This is one of the biggest practical premium drivers in founder-owned consulting firms. Buyers pay more when your business does not depend on you for every sale, major client relationship, key hire, and delivery escalation.

A firm with a real leadership bench, documented delivery processes, and salespeople or practice leaders who can win and retain clients without founder rescue will almost always be valued more favorably than one where the founder is the operating system.

5.6 Clean financials and a credible growth story

Even great businesses lose value if buyers cannot understand them. Premium outcomes are much easier when your financial reporting separates revenue by service line, customer, geography, and margin profile, and when your story matches the numbers.

If you say you are an AI consultancy but 80% of your revenue comes from undifferentiated QA staffing, buyers will figure that out fast. The premium comes when positioning and economics line up.

5.7 Earnout structures can support higher headline valuations

The private deal data shows repeated use of earnouts in technology consulting acquisitions. That matters because it tells you buyers are often willing to pay more when part of the price is tied to post-close revenue or EBITDA performance.

For founders, the lesson is not "accept any earnout." The lesson is that a premium valuation in this sector is often conditional. If your growth story is strong but not fully proven, an earnout may be the bridge between your expectations and the buyer's risk concerns.

6. Discount Drivers (What Lowers Multiples)

Low valuations in technology consulting usually happen when buyers see fragile revenue, unclear profits, or too much concentration risk. The headline service offering may sound attractive, but the economics underneath it do not feel safe.

A common discount driver is project-heavy revenue with weak visibility. If a large part of your revenue resets every few months and there is no recurring support layer underneath, buyers will worry about post-close revenue slippage. The same goes for weak gross margin discipline, underutilized teams, and inconsistent pricing.

Customer concentration is another major issue. If one or two accounts drive a large share of revenue, the buyer will discount the business because one relationship problem can damage the whole investment case. Founder concentration creates the same problem. If the top accounts stay because of you personally, that is not fully transferable value.

The data also suggests that specialization without profits is not enough. A firm may have a good niche in capital markets, energy, cyber, or cloud, but if EBITDA is weak or negative, buyers are unlikely to award a premium just because the sector sounds attractive.

Other common discount factors include:

- Weak second-line leadership

- High employee churn in delivery teams

- Unclear revenue recognition or poor monthly reporting

- Too much reliance on subcontractors without margin control

- Generic "we do everything" positioning

- No proof of customer retention or account expansion

- Data-quality issues in the financials that make buyers distrust the story

The good news is that many of these are fixable. A discount is often not a verdict on the market - it is a sign that the buyer sees too much uncertainty.

7. Valuation Example: A Technology Consulting Company

To show how valuation logic works in practice, here is a fictional example. The company, its characteristics, and its USD 10 million revenue level are illustrative only. This is not investment advice or a formal valuation.

Let us call the business NorthPeak Digital. It is a fictional technology consulting firm focused on cloud modernization, data engineering, and application development for mid-market customers. It has around 100 employees, a strong engineering team, and some recurring support work - but it is still mainly a services-led company rather than a software business.

7.1 How the valuation logic works

Step one is choosing the right comparison set. For a business like NorthPeak Digital, the most relevant benchmarks are private full-scope digital engineering and IT services deals, plus public digital engineering and mid-market IT consulting peers. The source data suggests that for firms of this type, a reasonable EV/revenue range for a smaller, services-led consulting business is around 1.0x to 2.6x revenue.

That range makes sense because it sits within the public-market interquartile ranges for relevant services peers and below the stronger private outliers. It also reflects the reality that a smaller private consultancy usually carries more execution risk and less diversification than larger public firms.

Step two is adjusting for company-specific strengths and weaknesses. If the business has strong margins, repeat customers, low customer concentration, and leadership depth, it can move toward the top of the range or above it. If it has weak profitability, short project cycles, or heavy founder dependence, it moves toward the low end.

Step three is considering deal structure. In this sector, a buyer may be willing to agree to a higher headline number if part of the consideration is contingent on future performance. So the "best" valuation may not all be guaranteed cash at closing.

7.2 Applying the logic to NorthPeak Digital

Assume NorthPeak Digital has USD 10.0 million in annual revenue.

Base case:

- Relevant multiple range: 1.4x to 2.2x revenue

- Implied enterprise value: USD 14m - USD 22m

Why this is the base case: NorthPeak has a good technical niche and decent customer retention, but it is still mostly services-led and not large enough to command top-tier scarcity pricing by default.

Premium case:

- Relevant multiple range: 2.3x to 2.8x revenue

- Implied enterprise value: USD 23m - USD 28m

This could apply if the company has strong EBITDA margins, low concentration, repeat managed services revenue, a deep leadership team, and clear strategic value to a larger buyer that wants its platform capabilities or customer relationships.

Discounted case:

- Relevant multiple range: 0.9x to 1.3x revenue

- Implied enterprise value: USD 9m - USD 13m

This could apply if the business depends heavily on the founder, has lumpy project revenue, weak margins, poor reporting, or a few customers that account for too much of total sales.

The key founder lesson is simple: two firms with the same revenue can be worth very different amounts. In this sector, valuation is not just about size. It is about how safe, profitable, and transferable the revenue looks to a buyer.

8. Where Your Business Might Fit (Self-Assessment Framework)

A useful way to think about valuation is to score your business honestly across the factors buyers care about most. Do not use this as a precise pricing model. Use it to see whether you are closer to the discount end, the middle of the market, or the premium end.

Score each factor from 0 to 2:

- 0 = weak

- 1 = acceptable

- 2 = strong

A rough interpretation:

- 0-8 points: likely lower-end valuation zone unless the business has a very special strategic angle

- 9-16 points: fair market range for a solid business

- 17-24 points: closer to premium territory, especially if buyers see strategic fit

The point of this exercise is not to flatter yourself. It is to identify where a small number of improvements could move the number meaningfully. In technology consulting, reducing customer concentration or proving EBITDA quality often matters more than polishing the pitch deck.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often start the process before the numbers are ready, before the story is clear, and before the management team is prepared for diligence. That usually leads to lower bids, more retrading later, or both.

Another mistake is hiding problems. If customer concentration is high, margins are weaker than they look, or a key employee is planning to leave, it will usually surface in diligence. When buyers discover issues late, they do not just lower price - they lose trust.

Weak financial records are a major value killer in this sector. Many consulting firms could materially improve valuation in 6-12 months just by tightening monthly reporting, cleaning up revenue recognition, separating recurring from project revenue, and showing margin by customer or service line. Buyers do not like ambiguity, especially when paying for a people-heavy business.

A lack of a structured, competitive sale process also hurts valuation. Research has repeatedly shown that running a disciplined process with an advisor often leads to meaningfully better outcomes, sometimes around 25% higher purchase prices, because it creates competition, improves positioning, and reduces the risk of a single buyer controlling the narrative.

Another avoidable mistake is telling buyers the price you want too early. Once you say you want, say, USD 10 million of enterprise value, many buyers will simply work backward from that anchor and offer USD 10.1 million or USD 10.2 million instead of showing you what they might really pay in a competitive process. That kills price discovery.

There are also industry-specific mistakes. One is overclaiming AI or platform expertise without proof in the numbers. Buyers hear these claims all day. If the revenue mix, certifications, margins, and customer references do not back it up, it weakens credibility. Another is failing to lock in key delivery leaders before a sale. In consulting, people are the product, and buyers discount businesses where the core team may not stay.

10. What Technology Consulting Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work is usually not a massive strategic pivot. It is a focused effort to improve quality, reduce risk, and make the business easier for a buyer to underwrite.

10.1 Improve the numbers

Start by tightening financial reporting. Make sure you can clearly show revenue by customer, service line, project versus recurring mix, gross margin, and EBITDA trend. Build a simple KPI pack that shows bookings, backlog, utilization, customer retention, and account expansion.

If margins are soft, look for practical fixes. That may mean pricing discipline, less discounting, better staffing mix, tighter subcontractor control, or exiting lower-quality work. In this sector, even modest margin improvement can move valuation more than a similar increase in revenue.

10.2 Improve revenue quality

Look for ways to convert project work into ongoing relationships. That could mean support retainers, cloud optimization services, managed security, data operations, platform administration, or application maintenance.

Also document what is already sticky. Many founders underestimate how valuable repeat customers are because they think of the work as "project-based." A buyer may see it differently if you can show three-year account histories and expansion patterns.

10.3 Reduce concentration and founder dependence

If one client is too large, start broadening the base now. If too much selling flows through you, shift more commercial responsibility to practice leaders or account managers. If major client relationships are personal to you, bring other team members into those accounts before going to market.

This is one of the highest-payoff areas because it directly reduces perceived risk. A buyer pays more for transferability.

10.4 Sharpen your niche story

Do not try to be everything to everyone during a sale process. Buyers respond better to a clear story: for example, "We are the go-to partner for cloud modernization and data engineering in regulated mid-market financial services," or "We are a strong ServiceNow implementation and managed services partner for enterprise customers."

The market data suggests that specialization helps most when it is paired with real margins and retention. So the goal is not just better messaging. It is aligning messaging with the strongest economics in the business.

10.5 Lock down key people and delivery capability

Identify the people a buyer will worry about losing and take action early. That may include retention bonuses, clearer career paths, new employment agreements, or broader management visibility in client relationships.

A consulting firm with strong people but weak retention planning often gets discounted. Buyers know the revenue can walk out the door if the team feels uncertain.

10.6 Prepare for diligence before the process starts

Build your management presentation, financial pack, customer list, employee summary, and contract database before launching a sale. Make sure your data room tells a clean story.

The smoother the process, the easier it is for buyers to move quickly and bid with confidence. In technology consulting, uncertainty usually gets priced as risk.

11. How an AI-Native M&A Advisor Helps

Selling a technology consulting firm is not just about finding one buyer. It is about finding the right set of buyers, creating real competition, and presenting the business in a way that makes the value obvious. That is where an AI-native M&A process can materially improve outcomes.

First, AI can expand the buyer universe far beyond the usual shortlist. Instead of a narrow set of obvious acquirers, an AI-native process can identify hundreds of qualified buyers based on deal history, capability gaps, synergies, financial capacity, and other signals. More relevant buyers means more competition, stronger offers, and a better chance the deal closes even if one buyer drops out.

Second, AI can compress the early stages of the process. Faster buyer matching, faster creation of marketing materials, and better support during diligence can help founders reach initial conversations and offers in under 6 weeks. Speed matters because momentum often drives better outcomes.

Third, AI works best when combined with experienced human advisors. You still need seasoned M&A professionals to frame the story, defend the numbers, manage negotiations, and speak the buyer's language. The result is advisory quality that feels closer to Wall Street-grade execution, but without the cost structure of a traditional bulge-bracket process.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.