The Complete Valuation Playbook for Telecom Software Businesses

A practical guide to how telecom software businesses are valued and what drives high multiples.

If you run a privately held telecom software business and may explore a sale in the next 1-12 months, valuation is not something to leave until the last minute. In this market, buyer appetite is still there, but it is more selective. Strategic buyers and private equity both care deeply about quality - not just growth, but how repeatable your deployments are, how much of your revenue is truly software, and how dependent the business is on founder-led execution.

This guide is built to help you understand three things clearly. First, what telecom software businesses actually sell for. Second, what pushes a business toward the top or bottom of the valuation range. Third, what you can realistically improve over the next 6-12 months before going to market.

The goal is not to pretend there is one exact answer. There is not. The goal is to help you understand how buyers think, where your business likely fits today, and what practical steps can improve your outcome.

1. What Makes Telecom Software Businesses Unique

Telecom software is not valued like generic software, and it is not valued like a telecom operator either. It sits in between. Many businesses in this sector sell software to communications service providers, mobile virtual network operators, enterprise connectivity providers, or adjacent digital service businesses. That can include BSS and OSS platforms, billing and charging systems, customer care tools, revenue assurance and fraud software, network software, provisioning tools, messaging platforms, CPaaS layers, and operator monetization tools.

What makes the sector unique is that the software often lives inside mission-critical workflows. If your platform touches billing, provisioning, rating, customer care, partner settlement, SIM management, or network operations, buyers know replacement is painful. That can be a very good thing for valuation. Sticky software in difficult-to-replace workflows tends to create durable customer relationships.

At the same time, telecom software often comes with valuation friction that pure-play SaaS does not. Many businesses in the space still have meaningful implementation work, custom integrations, managed services, or customer-specific configuration. That can lower gross margin, make growth less scalable, and make revenue feel less repeatable. In simple terms, buyers ask: is this really software, or is it software supported by a lot of people-hours?

There is also a sector credibility issue. Telecom buyers tend to be large, slow-moving, and risk-sensitive. Long sales cycles, technical procurement, integration complexity, and dependence on a small number of operators can all weigh on valuation. A business with ten telecom customers may look diversified on paper, but if two customers represent most of the revenue, buyers will still view that as concentration risk.

The key risk checks in this sector are usually the same:

- customer concentration

- implementation intensity versus true productization

- contract durability and churn risk

- gross margin quality

- speed and cost of deployment

- reliance on one founder, one lead architect, or a small delivery team

- exposure to delayed operator budgets or long procurement cycles

2. What Buyers Look For in a Telecom Software Business

At a high level, buyers still care about the obvious things: revenue scale, growth, gross margin, EBITDA, customer retention, and quality of management. But in telecom software, they usually go one layer deeper. They want to know whether your revenue is recurring, whether the product can be deployed repeatedly without heavy customization, and whether your position inside the customer matters enough to survive budget pressure.

A strategic buyer often asks a version of this question: if we buy this business, do we get a product that deepens our offering to telecom customers, improves our economics, or gives us access to customers we want? That means your valuation is not only about current numbers. It is also about how clearly your product fits inside a larger buyer’s roadmap.

For example, a buyer is more likely to pay well for a platform that helps operators launch services faster, reduce billing errors, lower support costs, improve customer self-service, or monetize new connectivity products. Those benefits are easy to explain inside an acquisition committee. A nice product with weak proof of savings or unclear customer outcomes is harder to underwrite.

Scale also matters, but in a specific way. In telecom software, buyers like evidence that new customer wins do not require reinventing the product each time. They want to see repeatable integrations, standard deployment playbooks, and a product roadmap that is not held together by custom work. If you have that, smaller companies can still get strong attention because buyers can imagine scaling the business after acquisition.

How private equity thinks about it

Private equity looks at your business through both an entry lens and an exit lens. At entry, they ask whether they can buy the company at a reasonable multiple relative to future earnings power. At exit, they ask who would want to buy it from them in three to seven years.

That second question matters a lot. A PE buyer wants to know whether your business could later be sold to a larger software group, a bigger PE fund, or in rare cases become large enough for public market relevance. If the answer is unclear, they become more conservative at entry.

They also think about specific value creation levers. In telecom software, those often include price increases, selling more modules into existing customers, reducing delivery cost, standardizing deployments, adding adjacent products, or buying smaller complementary assets. If your business already shows those levers working, PE interest usually improves.

3. Deep Dive: Productized Telecom Software vs Software-Plus-Services

This is one of the biggest valuation questions in the sector, because it affects almost everything else: gross margin, scalability, buyer confidence, and what multiple your business can support. The core issue is simple. Are you selling a repeatable software product, or are you selling a software platform that still needs a lot of human effort to make each deployment work?

The data points in that direction clearly. Premium valuation drivers in the source material repeatedly point to software-like economics - high gross margin, meaningful EBITDA margin, and operating leverage. The logic is straightforward. Buyers pay more when growth can turn into profit without hiring a large services team to support every new customer.

The worked valuation logic in the source material makes the same point from the opposite angle. A smaller telecom BSS/OSS platform with gross margin around the low-40% range was treated more like a mixed software-plus-services business than a pure SaaS company. That kept the valuation range relatively restrained, even though the product category itself is attractive.

Why do buyers care so much? Because services-heavy businesses are harder to scale and harder to integrate. They depend more on people, tend to have more uneven margins, and can suffer if implementations slip. Pure or mostly productized software has cleaner economics and more predictable expansion. Buyers are not only buying current revenue - they are buying the shape of future revenue.

If your business looks more services-heavy today, this does not mean you are uninteresting. It means the path to a better valuation is usually about moving the model toward repeatability. That could mean standardizing integrations, reducing one-off engineering, narrowing product choices, packaging implementation into clearer tiers, or building self-service functionality for customers.

A simple way to think about it:

Founders often focus on headline growth. Buyers often focus on the quality of that growth. In telecom software, a business growing more slowly but with cleaner product economics can be more valuable than a faster-growing business that still behaves like an integration shop.

4. What Telecom Software Businesses Sell For - and What Public Markets Show

The data shows a wide spread, which is exactly what founders should expect in this sector. Telecom-related businesses are not all valued the same. Public markets reward some software categories much more than operator-like or services-heavy models, and private deal data shows the same pattern in a lower range.

The right way to use the data is not to grab the highest multiple and apply it to your revenue. The right way is to identify which business model your company most closely resembles, then adjust for growth, margin, recurring revenue quality, and risk.

4.1 Private Market Deals (Similar Acquisitions)

The precedent transaction set is broad, spanning telecom operators, telecom field services, enterprise software platforms, and communications software. Overall, the private market average in the source set is about 0.8x EV/Revenue and 8.2x EV/EBITDA, with medians of about 0.7x and 8.0x. That is a useful reminder that private deals are usually more conservative than public markets, especially for smaller businesses, mixed software-services models, or assets with limited scale.

Within that, the spread is meaningful. Enterprise software platform deals in the set sit at the low end on revenue multiples, while customer engagement and communications software and selected execution-led telecom platforms can support better outcomes when there is stronger growth, strategic fit, or better forward earnings visibility. In other words, private buyers do pay up - but usually for very specific reasons, not just because a business uses the word software.

These are illustrative reference points, not direct price tags. A small telecom software company with good product economics may deserve to sit above many of these private benchmarks. But the private market data does support one very important lesson: if your business still looks partly like services, implementation, or operator support, buyers will rarely value it like premium SaaS.

4.2 Public Companies

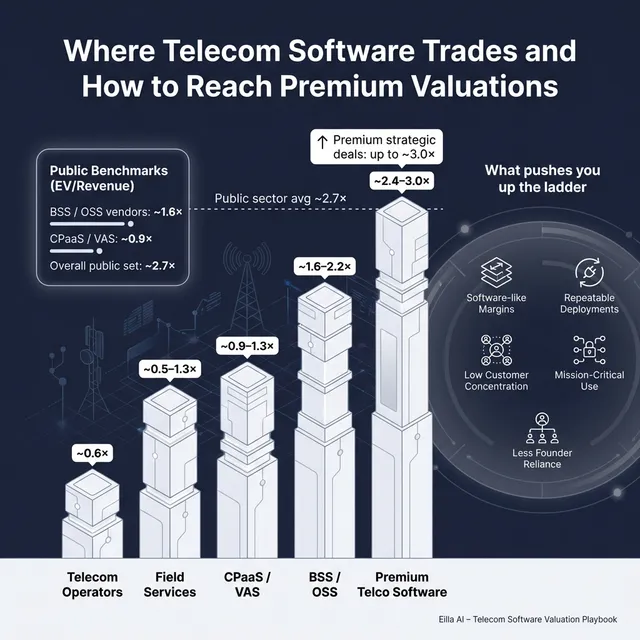

Public market trading is much richer than private deal pricing, but again the range depends heavily on what type of telecom-related company you resemble. As of mid to late 2025 in the source data, the overall public company set traded at about 2.7x average EV/Revenue and 15.3x average EV/EBITDA, with medians of about 1.8x and 6.8x. That spread exists because the sample includes software vendors, network software businesses, operators, managed service providers, and adjacent IT services groups.

For telecom software founders, the most relevant public reference point is the telco BSS/OSS and digital care and billing software group. That group trades around roughly 0.6x to 2.1x EV/Revenue in the company-level data, with many of the more credible names clustering in the high-1x to low-2x area. Network software and selected programmable SIM or private network platforms can also trade around the mid-1x range, while operator monetization layers and value-added services often sit lower. Large IT services groups tend to trade around roughly 1.8x to 3.2x revenue, but that is not a clean comp for smaller telecom software companies because the scale, diversification, and profitability are very different.

* This category is skewed by a very large outlier in the source set.** Based on profitable names only where EBITDA multiple is available.

The practical takeaway is simple. Public multiples are a reference band, not a direct answer. Founders should usually treat them as an upper guide, then adjust downward for smaller scale, lower growth, lower margins, customer concentration, and execution risk. In rare cases, a scarce and highly strategic telecom software asset can narrow that discount or even push above the obvious range if buyers see unusual strategic value.

5. What Drives High Valuations (Premium Valuation Drivers)

The source data shows that premium outcomes are rarely random. Buyers consistently pay more when they can underwrite a business as scalable, repeatable, and easy to fit into a larger platform. In telecom software, that tends to show up in a few clear themes.

Software-like economics

The clearest premium driver is evidence that your business behaves like software, not like outsourced delivery. High gross margin, good EBITDA margins, and visible operating leverage all matter. Buyers are more confident paying up when they believe each new dollar of revenue can turn into profit at a healthy rate.

A founder-friendly way to think about this: if you win three more customers next year, do you need to add a lot of service staff to support them, or does the product do most of the work? Businesses that can answer that question well usually get better attention.

Repeatable deployments and standardized integrations

Telecom software buyers care a lot about whether the product can be rolled out again and again without major reinvention. This showed up in the source commentary as the software equivalent of scalable execution capacity. In a field services business, scale comes from having a big delivery organization. In telecom software, scale comes from having productized deployment.

Examples of what this looks like:

- pre-built integrations into common operator systems

- standard onboarding playbooks

- predictable implementation timelines

- low engineering involvement after contract signature

Clear near-term growth story

Premium valuations often need more than historical results. Buyers want a believable story for what happens next. The source data points to deals where buyers could underwrite visible forward growth and earnings expansion, rather than just trailing performance.

In practice, that means you are stronger if you can point to real near-term catalysts such as:

- signed but not yet launched operator customers

- clear expansion modules for existing customers

- entry into adjacent geographies with the same product

- upsell from core billing or care into self-service, analytics, IoT, or adjacent modules

Diversified customer base and broad distribution footprint

Buyers pay more for businesses that do not live or die by one or two telecom customers. In the source material, companies with broader customer bases and more diversified demand looked more resilient and easier to scale. That matters in telecom because one delayed procurement cycle can badly hurt a small vendor.

The ideal buyer story is not just "we serve major operators." It is "we serve multiple customers with repeatable use cases, and no single account can break the business."

Strategic fit with a larger buyer

Some of the best outcomes happen when a buyer can immediately see how your business makes their own platform stronger. That could be because your product fills a gap, improves retention, deepens a customer relationship, or opens access to new budgets inside telecom accounts.

For example, a business that sits between customer activation, billing, and support can have more strategic value than a narrower reporting tool, because it becomes harder to displace and easier to cross-sell around.

Low integration risk and team continuity

Buyers pay more when they believe the business will keep working after the deal closes. The source data highlights continuity as a positive theme in several transactions. In telecom software, this is less about protecting field execution and more about protecting product roadmap, customer success, and integrations.

That means buyers like to see:

- a management team beyond the founder

- documented implementation processes

- stable technical leadership

- customer relationships that are company-owned, not founder-owned

Clean basics still matter

Even when the product is strong, premium valuations are hard to achieve without clean fundamentals. Buyers consistently reward businesses with predictable recurring revenue, good financial records, clear KPI tracking, diversified customers, and a leadership team that can operate without daily founder firefighting.

6. Discount Drivers (What Lowers Multiples)

Headline multiples can be misleading because many businesses in this sector trade at the low end for very understandable reasons. A lower multiple does not always mean a bad company. It often means buyers see more work, more risk, or less certainty.

One of the biggest discount drivers is mixed economics. If your gross margin is modest, services revenue is high, and deployments are highly customized, buyers tend to view the business as only partly software. That usually leads to a lower valuation than a cleaner SaaS profile, even if customers like the product.

Another common issue is weak growth visibility. Buyers get nervous when revenue is flat or declining and management cannot point to a credible path back to growth. The source commentary makes this especially clear: modern product language by itself is not enough. Without evidence of re-acceleration, buyers stay cautious.

Customer concentration is another major discount factor. In telecom software, even a good product can be marked down if too much revenue comes from a handful of operator accounts, reseller channels, or geographies. Buyers know one lost contract or procurement freeze can materially hurt the business.

Founder dependence also lowers value. If the founder is the main salesperson, key product architect, senior delivery manager, and top customer relationship owner, a buyer sees transition risk. That does not kill a deal, but it often lowers the price or increases earnout pressure.

Other common discount drivers include:

- poor revenue quality or unclear recurring revenue split

- weak KPI reporting on churn, expansion, and implementation costs

- low EBITDA or no path to profitability

- product roadmap risk

- customer contracts that are easy to exit

- long unpaid pilots that do not convert

- messy financials that make diligence harder

The good news is that many of these issues are fixable. Buyers will live with imperfections. What they dislike is uncertainty they cannot measure.

7. Valuation Example: A Telecom Software Company

To show how the logic works, here is a fictional example. The company is fictional. The USD 10m revenue figure is fictional. The valuation ranges below are illustrative only - not investment advice, not a fairness opinion, and not a formal valuation.

Let’s imagine a company called SignalForge. It sells a telecom BSS/OSS platform to mobile virtual network operators and smaller communications service providers. The product includes billing, provisioning, customer care, and partner management. Revenue is USD 10m. Gross margin is 48%. EBITDA margin is 8%. Growth is healthy but not hyper-growth. Implementations are getting more standardized, but there is still some services content in the model.

Step 1: Start with the most relevant comp set

The source material suggests the most relevant public anchor for this kind of business is the telco BSS/OSS and digital care and billing platform group. In the worked example provided, the core public reference band for that category supported roughly a mid-1x to low-2x revenue range. The source logic then widened that band modestly to allow for small-cap dispersion, but stayed cautious because the business profile was still mixed rather than pure SaaS.

That logic is sound. For a USD 10m revenue business like SignalForge, a sensible starting point is not the highest software multiple in the market. It is a practical core band based on relevant telco software comps, then adjusted for quality.

Step 2: Build a base case

SignalForge is not a pure-play SaaS business. Gross margin is better than the low-40% example in the source material, but still below what most buyers would call premium software economics. That means the base case should stay disciplined.

A reasonable base range would be around 1.6x to 2.2x revenue, implying an enterprise value of USD 16-22m. That keeps the company within the logic of the BSS/OSS public comp band while recognizing that it still carries some software-plus-services characteristics.

Step 3: Consider the premium case

Now assume SignalForge improves several important things before sale:

- gross margin rises above 55%

- deployments become much more standardized

- no customer is more than 15% of revenue

- churn is low and expansion within customers is visible

- the management team can run delivery without founder bottlenecks

- there are signed near-term launches that support a credible growth step-up

In that case, buyers may stretch higher because the business starts to look more like a scalable telecom software platform and less like a custom implementation business. A premium case could be around 2.4x to 3.0x revenue, implying USD 24-30m.

Step 4: Consider the discounted case

Now flip the profile:

- two customers make up half the revenue

- growth has slowed sharply

- deployments are still bespoke

- gross margin is stuck in the low-40% range

- EBITDA is thin or inconsistent

- the founder is central to product and delivery

That business is still sellable, but buyers will protect themselves. A discounted case might fall to around 1.0x to 1.5x revenue, implying USD 10-15m.

What should founders take from this? Two telecom software businesses with the same USD 10m revenue can reasonably be worth very different amounts. The difference usually comes down to how software-like the model is, how repeatable the product is, and how much risk a buyer sees in growth, concentration, and execution.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple self-assessment can help you estimate whether your business is closer to the discounted end, the fair-market middle, or the premium end. Score each factor from 0 to 2.

- 0 = weak today

- 1 = acceptable but not standout

- 2 = strong and buyer-friendly

Scoring framework

How to use it

Give yourself a score for each factor, then total it honestly.

A practical interpretation:

- 0-8: likely closer to the lower end of the valuation range

- 9-15: likely in the fair-market middle

- 16-20+: closer to premium territory if the story is credible and well presented

This is not a pricing formula. It is a way to see where the biggest value gaps are. Most founders do not need to improve everything. Usually, fixing two or three high-impact weaknesses does more for valuation than polishing ten minor ones.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders sometimes decide to test the market before the numbers are ready, the growth story is clear, or the buyer materials are strong. That usually leads to weak first impressions and lower offers. Buyers are not just judging the business - they are judging how well prepared you are.

Another major mistake is hiding problems. If churn is rising, margins are weaker than expected, a customer may leave, or product delays have hurt growth, that will usually come out in diligence. When buyers discover issues late, they do not just discount the business. They lose trust, which can hurt price, terms, and closing certainty.

Weak financial records are also costly. In this sector, many businesses can improve valuation meaningfully in 6-12 months just by making the financials easier to understand. Buyers want clear separation between recurring software revenue and services revenue, clean gross margin reporting, better revenue recognition, and KPI tracking that actually matches how the business is sold.

A lack of competitive process is another avoidable error. Research and market experience consistently support the idea that running a structured, competitive sale process with an advisor often leads to meaningfully higher outcomes - commonly around 25% better purchase price than a single-buyer conversation. Competition improves both price and deal certainty.

Another common mistake is telling buyers your target price too early. If you say you want USD 10m of enterprise value, many buyers will anchor around that number and come back with USD 10.1m or USD 10.2m instead of revealing what they might really pay. You kill price discovery when you do the buyer’s job for them.

There are also two telecom software-specific mistakes worth flagging. First, failing to clearly separate product revenue from implementation and managed services revenue. If buyers cannot tell what part of the business is true software, they default to caution. Second, failing to document integrations and deployment processes. In this sector, undocumented complexity often scares buyers more than the complexity itself.

10. What Telecom Software Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work is usually not a dramatic pivot. It is targeted improvement around the few things buyers care about most.

Improve the economics

Start by making the business look more software-like if that is directionally true. Reduce low-value custom work where possible. Package implementation more clearly. Push standard integrations and templates. Measure gross margin by revenue type so you can prove that software margins are stronger than blended company margins suggest.

Also look for quick EBITDA improvement without hurting the product. Buyers respect founders who can show better discipline on delivery cost, pricing, and project scoping.

Improve the quality of revenue

Buyers will pay more when they can trust the revenue base. That means tightening contracts, reducing churn, improving renewals, and pushing module expansion into existing customers. If possible, reduce reliance on one or two major customers before launch.

If your pipeline has near-term launches or expansions, work to convert those into signed, dated proof points. Buyers place much more value on visible near-term revenue than on ambition.

Improve repeatability

Document the product. Document the deployment model. Document the integrations. One of the strongest moves a telecom software founder can make before sale is to show that implementation is becoming standardized and does not rely on a few heroes inside the business.

This also helps reduce founder dependence. If customer success, onboarding, and delivery are clearly institutionalized, buyer confidence rises.

Improve the story

You need more than numbers. You need a buyer-friendly explanation of why your business matters. That story should answer simple questions:

- what problem do we solve for telecom customers?

- why is the product hard to remove?

- why are customers likely to stay and expand?

- what makes deployments more repeatable today than two years ago?

- why can a buyer grow this business faster than we could alone?

The strongest sale stories are specific, not polished. Buyers trust proof more than adjectives.

Get sale-ready

Over the next 6-12 months, prepare as if diligence starts tomorrow. Clean up monthly reporting. Build a simple KPI dashboard. Separate software and services clearly. Prepare customer cohort analysis, concentration summaries, churn data, pipeline conversion data, and implementation economics.

This work does not just help diligence. It often changes how buyers value the business because it reduces uncertainty.

11. How an AI-Native M&A Advisor Helps

For founders, one of the hardest parts of a sale is not just valuation. It is running a process that reaches the right buyers, creates real competition, and keeps moving fast enough that momentum is not lost. That is where an AI-native M&A advisor can change the outcome.

First, AI expands buyer reach. Instead of relying on a short list of obvious names, it can help identify hundreds of qualified buyers based on deal history, strategic fit, likely synergies, financial capacity, and similar signals. More relevant buyers means more competition, stronger offers, and a better chance the deal still closes even if one buyer drops out.

Second, AI can materially speed up the process. With AI-driven buyer matching, outreach support, process materials, and diligence preparation, founders can often get to initial buyer conversations and early offers much faster - often in under six weeks. Speed matters because deals lose value when processes drag.

Third, the best outcome still comes from human expertise, but AI makes that expertise more powerful. Expert M&A advisors with decades of experience can use AI to prepare sharper materials, position the business more strategically, and speak the language buyers expect. The result is advisory quality that feels far closer to Wall Street-grade execution, without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.