The Complete Valuation Playbook for Travel Software Businesses

A practical, data-backed guide to how travel software businesses are valued and what drives high multiples.

If you run a travel software business and you may sell in the next 1-12 months, valuation is no longer something to think about only at the end. Travel software is in a period where consolidation matters, strategic buyers want assets that help them win distribution or own hotel workflows, and buyers are becoming much more selective about what counts as real software value versus revenue that is simply exposed to travel volumes.

This guide is built to help you understand three things in plain English: what travel software businesses actually sell for, what pushes valuations up or down, and what you can do in the next 6-12 months to improve your outcome. It is based on the deal and public market data in your sources, but it also explains the buyer psychology behind those numbers.

The goal is not to pretend there is one exact price for your company. There is not. The goal is to help you see where your business likely sits on the valuation spectrum, and what would move it higher.

1. What Makes Travel Software Unique

Travel software is not one single market. Buyers look very differently at a hotel channel manager, a property management platform, a B2B travel distribution network, a corporate travel software business, a loyalty platform, and a tourism analytics company.

That matters because the same headline revenue can mean very different things. One business may have sticky subscription revenue from hotel operations software. Another may have transaction-driven revenue tied to booking volumes. A third may look like software on the surface but still depends heavily on people, supplier relationships, or manual support behind the scenes.

In this sector, the main business models usually fall into a few buckets:

- Hotel distribution and connectivity software - such as channel management, booking engines, and pricing or revenue tools

- Hospitality operations platforms - such as PMS, POS, guest operations, and other property systems

- B2B travel marketplaces and supply aggregation - where value comes from inventory access, distribution reach, and network position

- Travel enablement and adjacent software - such as loyalty, enterprise integration, data intelligence, and corporate travel tools

- Consumer booking platforms - which can set public market reference points, but are usually not the best direct comp for a private B2B software company

The unique valuation question in travel software is this: are you really selling software value, or are you selling access to travel flows? Buyers pay much more for businesses that are deeply embedded in customer workflows, hard to replace, and able to keep margins strong as they scale.

The risks buyers always examine are also sector-specific. They will check supplier concentration, reliance on a few large hotel groups or channels, the depth of your integrations, exposure to booking volume swings, contract structure, implementation complexity, uptime and data accuracy, and whether your customers would face real pain if they switched away from you.

2. What Buyers Look For in a Travel Software Business

At a basic level, buyers still care about the usual things: revenue scale, growth, gross margin, EBITDA, customer retention, and whether your numbers are clean. But in travel software, they also care deeply about where you sit in the travel stack and how defensible that position is.

A strategic buyer usually asks questions like these:

- Does this asset help us control more of the booking, pricing, guest, or operations workflow?

- Does it strengthen our connectivity to hotels, agencies, airlines, or enterprise customers?

- Does it bring a network position, supplier leverage, or cross-sell opportunity we do not already have?

- Is this revenue durable enough that we can safely pay up for it?

That means a founder-friendly way to think about valuation is not just "how fast are we growing?" but "how essential are we to the customer and how hard are we to replace?" A business with moderate growth but deep workflow integration can be worth more than a faster-growing but shallow tool.

Buyers also look hard at revenue quality. They want to know how much revenue is recurring, how much is usage-based, how much is project work, and how sensitive the model is to travel demand swings. In this industry, two companies with the same top line can have very different value depending on whether their revenue is contracted software revenue or transaction-linked revenue with weaker protection.

Private equity buyer thinking

Private equity firms think in a slightly different way from strategics. They still want quality, but they are always asking what they can sell the business for in 3-7 years.

So they think about:

- Entry multiple versus exit multiple - if they buy at a strong price today, can they still sell later at an equal or higher price?

- Future buyer universe - would this business appeal later to larger strategic buyers, bigger PE funds, or public market investors?

- Value creation levers - can they raise prices, improve margins, add adjacent products, acquire smaller competitors, or professionalize the sales engine?

For PE, travel software is most attractive when the business already looks institutional: repeatable sales, strong retention, visible profitability, and a product that sits in a mission-critical part of the travel workflow. They are less excited by businesses that depend too heavily on founder relationships, custom work, or one-off supplier deals.

3. Deep Dive: Connectivity Depth, Switching Costs, and Revenue Quality

One of the biggest valuation differences in travel software comes down to a simple question: are you a true piece of infrastructure, or are you just another layer that could be swapped out?

This shows up clearly in the deal data. One observed premium driver is enterprise-grade embeddedness in core hotel operations and connectivity. The source commentary highlights that buyers care not just about having integrations, but about the depth of those integrations - authentication, mapping, reconciliation, error handling, service levels, and the time and cost saved for the customer. In other words, "connected" is not enough. Buyers want to see that ripping you out would be painful.

This also explains why some apparently strategic assets still sold at modest revenue multiples in the private market. Small hotel connectivity and channel-management deals in the data cleared around 0.8x to 2.6x revenue, even though the products sounded useful. That tells you something important: workflow relevance helps, but it does not automatically create a premium if the company is still subscale, lightly profitable, or strategically narrow.

The second part of this issue is revenue quality. Many travel software businesses mix subscription revenue with transaction-linked revenue. Buyers do not reject transaction exposure. In fact, they may like it if it scales well. But they will ask whether the revenue is durable and whether margins remain strong as volume grows. A business that claims software-like economics but in practice has hidden servicing costs, supplier dependency, or fragile take rates will be marked down.

A useful way to think about it is this:

If your business looks more like the left column today, the path upward is usually clear. Deepen integrations. Measure implementation time saved. Track uptime and error rates. Show retention by cohort. Reduce manual work. Prove that you are not just connected to the travel ecosystem - you are embedded in it.

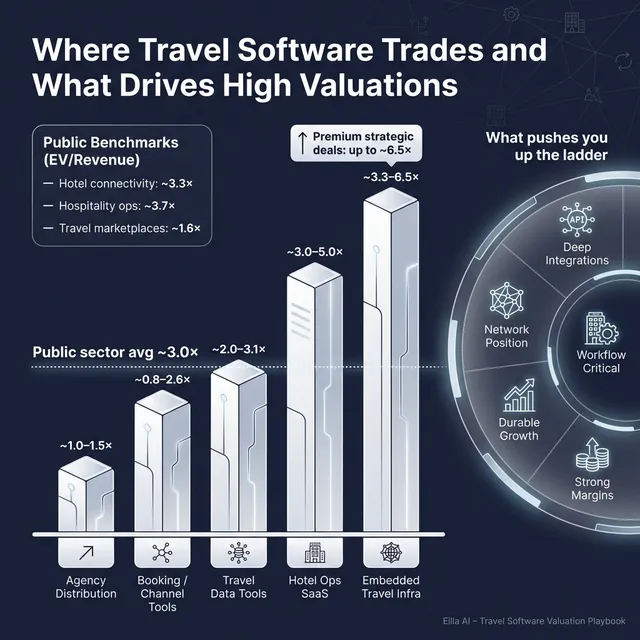

4. What Travel Software Businesses Sell For - and What Public Markets Show

Here is what the data actually shows: private travel software deals are generally lower than public market trading multiples, but there is a wide spread based on margin profile, growth, and strategic importance. Small feature-level tools often sell at modest revenue multiples. More scaled, profitable, and strategically embedded businesses can command much stronger outcomes.

The right way to use this data is not to grab one headline number. It is to understand the band, then decide where your business sits inside it.

4.1 Private Market Deals (Similar Acquisitions)

The precedent transaction data points to a private market that is fairly disciplined overall. Across the private deals provided, the average EV/revenue multiple is 1.7x and the median is 1.3x. The average and median EV/EBITDA are both 11.6x. That is a useful baseline because it reminds founders that private buyers usually pay less than public markets, especially for smaller businesses.

But the spread matters. In the data, small hotel distribution and booking engine assets tend to clear around 0.8x to 2.6x revenue. A travel agency distribution platform sold at around 1.5x revenue and 11.6x EBITDA. A tourism data intelligence platform achieved around 3.1x revenue. The pattern is clear: buyers pay more when they can see scale, credible profitability, and durable strategic position - not just product features.

These ranges are illustrative, not fixed. A larger, cleaner, faster-growing travel software asset with stronger margins can sit above them. A services-heavy or customer-concentrated business can sit below them.

4.2 Public Companies

Public market comps give a higher reference band, but they should be used carefully. As of late 2025, the overall public comp set in your sources trades at about 3.0x average EV/revenue and 24.5x average EV/EBITDA, with median figures of 2.9x and 13.8x respectively. That is materially above the private market averages.

Within the public set, different travel software categories trade very differently. Hospitality operations platforms screen highest on revenue multiples in this dataset, helped by stronger growth, deeper workflow ownership, and more software-like economics. Hotel distribution and connectivity software trades in the low-3x revenue area. B2B distribution marketplaces are lower on revenue multiples but can still look attractive when margins are strong. Consumer OTAs can trade well too, but they are usually not the best direct comp for a private B2B travel software business because scale, liquidity, and business model are very different.

Founders should use public multiples as a reference band, not a price tag. Public companies are larger, more liquid, better covered by investors, and usually have more diversified revenue. That means a smaller private company often deserves a discount versus public trading multiples.

That said, there are cases where a private asset can justify a premium to public reference points. This usually happens when the asset is scarce, strategically important, profitable, and offers a buyer something hard to build quickly - such as deeply embedded connectivity, an unusually strong supplier network, or a very attractive margin profile.

5. What Drives High Valuations (Premium Valuation Drivers)

The source data points to a simple truth: buyers do not pay premium multiples for travel software just because it sounds digital. They pay more when the business combines software-like economics with strategic importance and credible future growth.

5.1 Scalable software economics

High gross margin and solid EBITDA matter a lot in this sector. The premium driver commentary in the source data explicitly links stronger outcomes to businesses with margin profiles buyers can trust as they scale.

Why do buyers pay more for this? Because it reduces risk. If your margins hold as volume grows, a buyer can more confidently underwrite future cash flow.

What this looks like in practice:

- Revenue grows faster than support headcount

- New customers do not require huge custom work

- Transaction growth does not create hidden servicing cost

- You can clearly explain revenue recognition and cost of delivery

5.2 Deep workflow embeddedness

Being embedded in core hotel or travel operations is one of the strongest strategic valuation drivers in this market. Buyers pay more when your software is not just helpful, but operationally essential.

Why? Because it creates switching costs. If replacing you would disrupt reservations, pricing, inventory sync, guest workflows, or distribution accuracy, buyers see lower churn risk and better cross-sell potential.

Examples:

- Your integration sits between the hotel and many external channels

- You handle complex mapping, reconciliation, and uptime-sensitive workflows

- Your product is part of daily operational activity, not a side tool used once a month

5.3 Demonstrated growth at meaningful scale

Growth on its own is not enough. Buyers want to see growth that is real, durable, and happening at enough scale to matter.

The source commentary highlights that revenue acceleration becomes more valuable when paired with improving margins and credible forward earnings power. A small feature tool growing off a tiny base is less exciting than a business that has already crossed into institutional territory.

Examples:

- Consistent year-on-year growth rather than one lucky spike

- Strong expansion inside existing accounts

- A sales engine that can be repeated, not just founder-led wins

5.4 Network position and supplier leverage

Travel is a networked industry. If your platform has real reach with suppliers, distributors, or customers, that can be highly valuable - but only if that reach improves economics.

Buyers pay more when network position turns into pricing power, better conversion, stronger retention, or supplier access that others cannot easily copy.

Examples:

- You aggregate inventory in a way that improves conversion or take rate

- Your installed base helps you win better terms with partners

- Your scale lets you launch adjacent products more easily than smaller rivals

5.5 Forward visibility supported by earnout-friendly KPIs

The source data shows several deals using earnouts or contingent consideration. That usually happens when buyers like the upside, but want protection around performance.

This can actually support stronger headline valuations if your KPIs are measurable and trustworthy. A buyer is more willing to stretch when they can tie part of the price to future revenue, EBITDA, booking volume, active integrations, room nights, or similar operating indicators.

5.6 Clean, low-friction business quality

Not every premium driver is industry-specific, but they still matter. Buyers pay more for businesses that are easy to understand and easy to diligence.

That includes:

- Clean financial statements

- Predictable recurring revenue

- Low customer concentration

- Clear reporting by product and customer segment

- Strong leadership below the founder

- A believable growth story supported by actual data

6. Discount Drivers (What Lowers Multiples)

The other side of the market is just as important. Many travel software businesses do not sell at the top of the range because buyers see too many reasons to discount the story.

The first discount driver is subscale, narrow product scope. The lower private-market revenue multiples in the source data are a reminder that small tools do not get premium treatment just because they serve hotels or travel agencies. If the product is narrow, customer count is limited, and expansion potential is unclear, buyers usually stay disciplined.

The second is weak revenue quality. If too much revenue depends on travel volumes without enough contractual protection, or if the business relies heavily on services and manual account work, buyers will view that as lower-quality revenue. The same goes for unclear take rates, messy revenue recognition, or margin claims that do not hold up under diligence.

The third is shallow integration depth. Saying "we integrate with lots of systems" is not enough. Buyers will test whether those integrations are truly deep, whether customers depend on them daily, and whether churn would really be painful. If your connectivity is easy to copy, the valuation usually falls back toward lower-end software or even services multiples.

The fourth is concentration. That could mean customer concentration, supplier concentration, or channel concentration. If one hotel chain, one distribution partner, one OTA relationship, or one founding salesperson explains too much of the business, buyers get nervous.

The fifth is operational fragility. Founder-led sales, weak KPI reporting, poor cohort visibility, inconsistent margins, and technical debt all create discounts. Buyers are not only buying your current revenue - they are buying confidence in what happens after closing.

None of these issues is fatal on its own. But the more of them you have, the more likely your deal lands at the lower end of the range, or requires an earnout to bridge the gap.

7. Valuation Example: A Travel Software Company

Let us turn the logic into a worked example.

Assume a fictional company called AtlasStay Connect. This is not a real business. Assume it has USD 10m of annual revenue, and the valuation ranges below are purely illustrative - not investment advice, not a fairness opinion, and not a formal valuation.

AtlasStay Connect is a B2B hotel connectivity platform. It sells API-based distribution and booking infrastructure to hotels and travel partners. It has a healthy gross margin, positive EBITDA, recurring software revenue plus transaction-linked revenue, and solid retention. The reason this is a useful example is that it sits in one of the most interesting valuation pockets in travel software: software-like, but still exposed to travel transaction volumes.

Step 1: How the valuation logic works

The cleanest starting point is to look at the most relevant public comp band for hotel distribution, connectivity, and revenue SaaS. In your source data, that group trades at about 3.3x EV/revenue. That gives us a useful anchor, but probably a conservative one for a smaller, high-growth private asset with strong margins.

Then we cross-check against broader travel-tech public ranges. The source valuation logic notes a wider public reference range of roughly 2.2x to 4.8x revenue across relevant adjacent travel-tech buckets. That helps reflect the fact that some travel software businesses behave more like pure SaaS, while others look more like distribution platforms or mixed software-marketplace models.

Finally, we sanity-check against private market data. Private transactions overall are much lower on average, but profitable, scaled, strategically useful businesses can outperform the average. The source example also uses an EBITDA cross-check based on an observed 11.6x EV/EBITDA private deal multiple. That is useful because it reminds us that profitability can support value even when revenue multiples look conservative.

Step 2: Apply the logic to AtlasStay Connect

For a fictional USD 10m revenue business, a sensible framework might look like this:

- Discounted case: use a lower-end revenue multiple if the company has weaker retention, concentration, or shallower integrations

- Core case: use a mid-range multiple if the company is profitable, growing well, and clearly embedded in customer workflows

- Premium case: use a higher multiple if the company is scarce, strategically important, has strong margins, and offers real infrastructure value

Why not use the private-market average of around 1.3x-1.7x revenue as the main answer? Because that would likely understate a genuinely software-like, profitable, strategically embedded travel infrastructure asset. Why not automatically jump to the highest public comps? Because smaller private companies still deserve discounts for size, liquidity, and risk.

If AtlasStay Connect also had strong EBITDA margins, the EBITDA cross-check could support the case. For example, if it generated USD 2.0m EBITDA, an 11.6x EBITDA cross-check would imply about USD 23m EV. That is a useful floor-style reference, but it may still understate a high-quality travel software asset if growth, retention, and strategic value are unusually strong.

Step 3: What founders should take from this

Two travel software businesses with the same USD 10m revenue can easily be worth very different amounts. One may be worth around USD 25m because it is subscale, concentrated, and lightly embedded. Another may be worth USD 50m+ because it is profitable, sticky, and strategically hard to replace.

That is the real point of valuation work. Revenue matters. But in this sector, the quality of that revenue and the depth of your position in the travel workflow often matter just as much.

8. Where Your Business Might Fit (Self-Assessment Framework)

A simple self-assessment can help you estimate where you likely sit in the range. Score each item 0, 1, or 2:

- 0 = weak

- 1 = acceptable

- 2 = strong

Be honest. This is most useful when you use it to spot the biggest improvements you can still make before going to market.

A rough way to interpret the total:

- 10-12 points: you are closer to premium territory

- 6-9 points: you likely sit in the fair market middle

- 0-5 points: your business may still sell, but more preparation could materially improve value

The point is not to label your business as good or bad. The point is to identify where a small number of focused improvements could move the multiple in a meaningful way.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often decide to sell, tell a few contacts, and hope a buyer will "see the potential." That usually leads to weak offers because the numbers, narrative, and process are not ready.

Another mistake is hiding problems. In travel software, issues around customer concentration, churn, supplier dependency, margin quality, uptime, or technical debt will come out in diligence. When buyers discover a problem late, they do not just discount the issue itself - they also discount trust.

Weak financial records are another common value leak. If you cannot clearly separate recurring software revenue from services, or show margins by product line, or explain how revenue is recognized, buyers become cautious. In many cases, 6-12 months of cleanup can make a meaningful difference.

A major mistake is running an unstructured process without an advisor. Research often shows that a competitive, well-run sale process with an experienced advisor can increase purchase prices by around 25%, largely because it improves positioning, buyer competition, and negotiation leverage.

Another avoidable error is telling buyers what price you want too early. If you say you are looking for a USD 10m valuation, do not be surprised if buyers come back at USD 10.1m or USD 10.2m rather than showing you the real maximum they may have paid. You kill price discovery when you anchor too low.

Two travel-software-specific mistakes are especially costly. First, overclaiming that the business is "pure software" when margins or delivery costs do not support that story. Second, failing to document the depth and reliability of your integrations. In this sector, both claims will be tested hard.

10. What Travel Software Founders Can Do in 6-12 Months to Increase Valuation

The good news is that you usually do not need a massive strategic pivot to improve valuation. Most of the time, a focused 6-12 month plan can make the business easier to buy and easier to pay up for.

10.1 Improve the numbers buyers care about

Start by tightening the financial story. Separate recurring software revenue, transaction-linked revenue, and services revenue. Show gross margin clearly. Show EBITDA clearly. Build monthly reporting that lets a buyer see trend lines without guessing.

Then work on obvious margin improvements. Reduce low-value custom work, standardize onboarding, price support more intelligently, and remove revenue streams that look large but contribute little profit. Buyers pay more for clean economics.

10.2 Strengthen revenue quality

Work on retention and expansion. If customers stick around and buy more over time, that is one of the strongest valuation signals you can send.

Also reduce concentration where possible. Add mid-sized customers. Deepen partner breadth. Make sure no single supplier or channel explains too much of the growth story.

10.3 Increase your embeddedness

Deepen integrations that make you harder to replace. Measure the value clearly: uptime, error reduction, faster onboarding, fewer failed bookings, better mapping accuracy, smoother reconciliation.

If you can show that customers save time, avoid revenue leakage, or reduce operational risk because of your platform, you move closer to the higher-value end of the market.

10.4 Make growth look durable, not accidental

Buyers do not want one-off spikes. They want repeatability.

That means building a clear go-to-market story:

- Which customer segments convert best

- Which channels bring the best customers

- Which products expand best after the first sale

- Which KPIs predict long-term account value

10.5 Prepare the deal before the deal

Build a proper buyer-ready package. That includes a clean financial model, key KPI dashboard, customer concentration analysis, contract summary, tech overview, and a simple story about why your business matters strategically.

Also prepare for diligence early. Fix messy contracts. Clarify IP ownership. Organize data security materials. The easier you are to diligence, the easier you are to buy.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can improve outcomes first by expanding the buyer universe far beyond the usual shortlist. Instead of relying on a narrow manual list, AI can help identify hundreds of qualified buyers based on deal history, strategic fit, synergies, and financial capacity. More relevant buyers usually means more competition, stronger offers, and a better chance the deal closes even if one buyer drops out.

It also speeds up the process. With AI helping match buyers, prepare marketing materials, and support diligence, initial conversations and first offers can often be reached in under 6 weeks. That matters because momentum is a major advantage in any sale process.

Just as important, AI does not replace experienced advisors - it makes them stronger. The best outcome still comes from expert human M&A advisors who know how to frame your story, manage negotiations, and speak the buyer's language. AI helps them work faster, go broader, and support a more rigorous process.

The result is often Wall Street-grade preparation and process quality without traditional bulge-bracket costs. If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.