The Complete Valuation Playbook for Utilities Businesses

How utilities businesses are valued today and what drives high multiples.

If you own a privately held utilities business and are thinking about a sale in the next 1-12 months, valuation is not just a finance exercise. It is really a question of how buyers see the quality, durability, and strategic importance of your cash flows.

That matters even more now. Utilities and utility-adjacent infrastructure are sitting in the middle of several strong forces at once - grid investment, water infrastructure renewal, energy transition spending, tighter regulation, and ongoing consolidation. Buyers are still interested, but they are more selective about what deserves an infrastructure-like multiple and what deserves a contractor-like one.

This playbook is built to help you understand what utilities businesses actually sell for, what pushes valuation up or down, and what you can do in the next 6-12 months to improve your position before going to market.

1. What Makes Utilities Unique

Utilities are not valued like a normal services company, and they are not valued like software either. In this sector, buyers care most about the durability of cash flow, the essential nature of the service, the quality of the asset or network position, and the amount of revenue that is protected by regulation, long-term contracts, or hard-to-replace infrastructure.

The sector itself includes several different business models. Some companies are regulated network owners and operators in electricity, gas, water, or wastewater. Others are integrated utilities with a mix of regulated operations and broader energy or environmental services. Then there are utility-adjacent businesses - such as high-voltage engineering, grid maintenance, water engineering, utility EPC, and energy transition infrastructure providers - that serve the sector but do not own the network economics themselves.

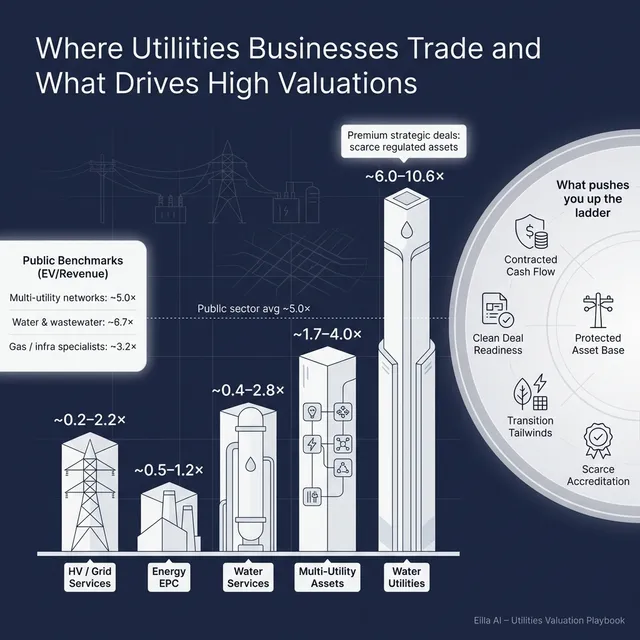

That distinction matters a lot. A business with recurring, regulated, infrastructure-like cash flow can trade very differently from a business with similar revenue but more project risk, more working capital swings, and less visibility. The data in your sector shows exactly that pattern: public utility operators tend to trade at materially higher revenue multiples than private contractor-like businesses, while private transactions cluster lower unless the target has something scarce, strategic, or strongly protected.

Buyers will also look hard at risks that are very specific to utilities. These include regulatory exposure, permitted returns, asset condition, capex needs, customer concentration, leakage or service-quality performance in water, grid reliability in power, safety record, labor availability, and exposure to political decisions around rates and infrastructure spending. In utilities, a business can look stable from the outside but still carry real value leakage if those risks are not well managed.

2. What Buyers Look For in a Utilities Business

At the most basic level, buyers still look for the usual things: scale, stable revenue, healthy margins, reliable growth, and credible management. But in utilities, those basics get filtered through one key question: how dependable is this business over a long period of time?

Strategic buyers often pay up when your business strengthens their geographic footprint, adds regulated or quasi-regulated cash flow, fills a capability gap, or gives them access to a scarce part of the network value chain. For example, a small regulated territory, a valuable water license footprint, or accredited high-voltage capabilities can matter more than a flashy growth story.

They also care about the quality of your revenue. Revenue backed by rate cases, regulated returns, framework contracts, long-term operations and maintenance agreements, or essential customer demand will usually be valued more highly than revenue that must be re-won every year. In this sector, buyers want to know not just how much revenue you have, but how much of it they can reasonably trust three years from now.

Margin quality matters too. High EBITDA margins in utilities often signal something important: durable infrastructure economics, not just good cost control. The source data shows that the highest EV/EBITDA outcomes tend to cluster around businesses with strong margins and long-duration, protected cash flows. That is very different from a labor-heavy contractor with variable margins and a stop-start project pipeline.

How private equity thinks about it

Private equity buyers usually start with a simple question: if they buy your business today, who can they sell it to in 3-7 years, and at what kind of multiple? If the likely future buyer is a larger strategic acquirer or infrastructure investor, that supports a stronger entry case. If the business is harder to exit because it is too small, too mixed, or too dependent on one founder, that can limit what PE will pay.

They also think carefully about entry multiple versus exit multiple. If they pay a high price today, they need confidence that the business will become more valuable over time through growth, better margins, add-on acquisitions, stronger systems, or movement toward a more infrastructure-like profile.

In utilities, PE buyers often look for a few clear levers: rate-base or contract-backed growth, bolt-on acquisitions, operational efficiency, geographic density, cross-sell into existing utility customers, and professionalization of reporting and governance. If they can see those levers clearly, they are more likely to stretch.

3. Deep Dive: Infrastructure-Like Cash Flows vs Contractor-Like Revenue

This is one of the most important valuation questions in utilities: does your business look like an owner/operator of durable utility economics, or does it look more like a contractor serving the sector? That single distinction can move valuation a lot.

The source data makes this very clear. Public regulated multi-utility network owners and operators sit around the mid-single-digit EV/Revenue range on average, while private transactions across broader utility services and contracting often cluster much lower. The overall public group averages about 5.0x EV/Revenue and 13.8x EV/EBITDA, while the overall precedent transaction set averages about 2.1x EV/Revenue and 10.3x EV/EBITDA. That gap is the market telling you something important: durable, protected cash flows are worth more than exposed, project-driven revenue.

Why do buyers care so much? Because infrastructure-like cash flow usually means longer visibility, lower customer churn, more predictable margins, and less dependence on constant new sales. A buyer can borrow against that cash flow more confidently, plan capex more clearly, and underwrite a safer exit. Contractor-like revenue, by contrast, often comes with bid risk, margin pressure, labor variability, and lumpier working capital.

This does not mean service or EPC businesses cannot sell well. They can - especially if they own scarce technical capability. The data shows that high-voltage specialists and other critical-path utility contractors can attract strong interest, sometimes with earn-outs tied to future performance. That tells you buyers do value scarce capability, but they often structure deals to protect themselves from execution risk.

If your business looks more contractor-like today, the goal is not to pretend otherwise. The goal is to move toward the higher-value profile wherever realistically possible: lock in more recurring operations and maintenance revenue, build framework agreements, increase visibility on future work, deepen accreditations, improve safety performance, and show that margins are not just cyclical good luck.

4. What Utilities Businesses Sell For - and What Public Markets Show

The useful way to read valuation data in utilities is not to hunt for one magic number. It is to understand the range and then ask why some businesses sit at the top of that range and others do not.

Broadly, the data shows two things. First, public markets give the highest reference points to businesses with long-duration, infrastructure-like economics. Second, private deals usually clear at lower levels unless the target has unusually strong strategic value, scarcity, or highly protected cash flows.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions provided, the overall average is about 2.1x EV/Revenue and 10.3x EV/EBITDA, with median EV/Revenue of about 1.0x and median EV/EBITDA of about 9.7x. That is a wide spread, which reflects how varied the sector is. Small water utilities with scarce regulated territories can trade at very high revenue multiples, while contractor-like or services-heavy businesses can sell below 1.0x revenue.

For founder-owned private businesses, the practical read-through is this: most deals are not priced off headline public utility multiples. They are priced off what your specific revenue actually looks like in terms of durability, margins, risk, and strategic value to the buyer. If your business is more owner/operator-like, you can justify a better range. If it is more project-based, buyers will usually pull you back toward lower private-market levels unless there is a clear scarcity story.

These ranges are illustrative, not automatic. A small private utility platform with real recurring economics may deserve more than a generic services comp. A business that looks like a contractor, even if it serves utilities, may deserve less than regulated operator comps.

4.2 Public Companies

As of mid to end-2025, the public sector reference set averages about 5.0x EV/Revenue and 13.8x EV/EBITDA, with medians of about 4.8x and 12.8x respectively. But again, the average hides meaningful segment differences.

Regulated water and wastewater utilities generally trade at the upper end of the range, helped by essential service characteristics, visible cash flows, and strong margins. Regulated multi-utility network owners also trade well, typically in the mid-single-digit revenue range and low-to-mid teens on EBITDA. By contrast, more diversified or commodity-exposed utility groups, and businesses with broader non-utility exposure, often trade at lower revenue multiples because the cash flow is less clean or less protected.

*This average is skewed by a high-multiple outlier in the provided data, so median-style interpretation is more sensible than taking the raw mean at face value.

The right way to use public multiples is as a reference band, not as your price tag. Public companies are larger, more liquid, better diversified, and usually have lower key-person risk. So private businesses usually get adjusted downward from public levels for size, concentration, and liquidity.

That said, there are cases where a private business can punch above its size. If your asset is scarce, strategically important, hard to replicate, or gives a buyer a valuable foothold in a regulated or essential service niche, the market may reward that. But you need a credible reason - not just a hope - for why your business should be treated more like infrastructure and less like a generic private company.

5. What Drives High Valuations (Premium Valuation Drivers)

The clearest premium driver in utilities is durable cash flow. Buyers pay more when they believe your revenue is hard to dislodge, visible over time, and backed by regulation, long-term contracts, or essential infrastructure.

A second major driver is infrastructure-like margin quality. In the source data, many of the stronger EV/EBITDA outcomes are tied to businesses with high and stable operating margins. Buyers are not just rewarding profitability in general. They are rewarding the kind of profitability that suggests defensible economics and low downside risk.

A third driver is strategic scarcity. Sometimes the asset is small, but strategically important. A regulated local water footprint, a scarce service territory, or critical-path network capability can create buyer urgency. When a buyer sees a chance to add a hard-to-buy asset into a larger platform, valuation can move up.

A fourth driver is technically scarce capability. In utility contracting and engineering, buyers pay more for businesses that are hard to replace - accredited high-voltage work, safety-critical delivery, trained labor pools, and proven delivery on complex infrastructure. Even when the buyer uses an earn-out, that is often a sign they see value in the capability but want protection against delivery risk.

A fifth driver is exposure to long-duration energy transition spending - but only when it is credible. EV charging, grid upgrades, distributed energy infrastructure, and related build-out can support valuation when attached to durable rollouts, protected customer relationships, or long-term frameworks. Buyers do not usually pay a premium for just having the right buzzwords. They pay when the growth is real and underwritten.

A sixth driver is clean execution readiness. This sounds less glamorous, but it matters a lot. Clean financials, clear segment reporting, stable leadership below the founder, diversified customers, and a simple, believable equity story all help buyers get comfortable. Comfort increases competition, and competition increases value.

Here is how those premium themes tend to show up in real buyer behavior:

6. Discount Drivers (What Lowers Multiples)

The biggest discount driver is uncertainty. Buyers lower multiples when they feel they are stepping into something they cannot reliably underwrite - messy revenue mix, poor visibility, volatile margins, capex surprises, regulatory exposure, or weak reporting.

A common problem in utilities is being too mixed. If your business combines a good recurring core with lower-quality project work, but you cannot clearly separate the two in your numbers, buyers may value the whole company off the lower-quality component. This happens all the time. The story may be better than the data presentation.

Customer and contract concentration also pulls value down. If too much of your revenue depends on one utility, one municipality, one framework, or one rate decision, the buyer sees fragility. The same goes for businesses where the founder personally owns the key relationships or technical know-how.

Another discount factor is contractor-like earnings without contractor-like discipline. If backlog is weak, claims management is messy, margins swing sharply, and working capital consumes cash, buyers will assume the risk is higher than management says. In utilities, stable optics matter. Unpredictability gets punished.

Weak compliance, safety, or regulatory history is another major red flag. In many sectors, buyers can live with some operational mess. In utilities, safety incidents, permit issues, environmental non-compliance, leakage performance problems, or poor service-quality metrics can materially reduce confidence and price.

Finally, buyers discount companies that require too much explanation. If your revenue recognition is unclear, segment reporting is inconsistent, or the real margin of each business line is hidden, buyers protect themselves by lowering valuation.

7. Valuation Example: A Utilities Company

Let’s make this practical with a fictional example.

Assume HarborGrid Utilities, a fictional privately held UK utilities business with USD 10.0m of annual revenue. It operates a mix of local electricity, gas, and water-related network assets plus a small EV charging infrastructure footprint. It has been around for over 20 years, has 80 employees, and looks more like an owner/operator with infrastructure-style characteristics than a pure EPC contractor.

This company is fictional, and the revenue figure is fictional. The valuation range below is illustrative only - not investment advice and not a formal valuation.

Step 1: How the logic works

The cleanest starting point is to anchor HarborGrid against the most relevant public comp group: regulated multi-utility network owners and operators. In the source data, that public band supports roughly 3.85x to 6.10x EV/Revenue for businesses with that kind of profile.

Then you cross-check. If HarborGrid looked more contractor-like - more like utility infrastructure EPC or specialist delivery rather than a true owner/operator - a lower band closer to utility services or gas-distribution specialist public comps might make more sense. If it were more clearly weighted to protected, water-regulated cash flow, a higher band closer to water utility comps could be justified.

You also use private deals as a reality check. The private regulated multi-utility and energy distribution transaction band in the source set is lower, roughly 1.7x to 4.0x revenue, which reflects the normal private company discounts for size, liquidity, and risk. That does not mean HarborGrid must price there, but it reminds you not to apply public comps blindly.

Step 2: Apply it to the fictional company

On USD 10.0m revenue, the core public-anchor range implies:

- Low end: 3.85x = about USD 39m

- High end: 6.10x = about USD 61m

That gives a sensible core range for a mature, network-style utilities business with no obvious start-up premium and no extraordinary moat.

You can then frame three practical scenarios:

Step 3: What would move HarborGrid up or down?

A discounted case would apply if the business turns out to be more contractor-like than it first appears, has customer concentration, weak recurring revenue, margin volatility, or unclear asset economics.

A core case fits if the company genuinely has infrastructure-like characteristics, decent revenue visibility, and operating stability, but nothing unusually scarce or strategic.

A premium case could be defensible if HarborGrid has a scarce regional footprint, a strong share of regulated or very long-term contracted revenue, excellent margins, strong compliance history, and a buyer that sees meaningful strategic value in the asset.

The point is simple: two utilities businesses with the same USD 10m revenue can be worth very different amounts. Buyers are not just buying revenue. They are buying the quality, durability, and strategic usefulness of that revenue.

8. Where Your Business Might Fit (Self-Assessment Framework)

A useful way to assess your likely position is to score yourself honestly across the factors that most affect valuation. Use 0 for weak, 1 for acceptable, and 2 for strong.

How to use the score

If you score in the top band, you are closer to premium territory. That does not guarantee a premium outcome, but it means your business is more likely to attract broad interest and stronger competition.

If you score in the middle band, you are probably in fair-market territory. That is still very saleable, but your outcome will depend heavily on process quality, storytelling, and how well your numbers support the narrative.

If you score in the lower band, that does not mean you should never sell. It means there may be clear value creation work you can do first. The goal of this exercise is not self-criticism. It is to identify which improvements will move the needle most.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often decide to sell only after burnout, a growth slowdown, or an unsolicited offer. That usually means the numbers, the story, and the process are not fully prepared. Buyers sense that quickly, and rushed sellers rarely get the best outcome.

Another major mistake is hiding problems. In utilities, issues always surface - customer concentration, compliance gaps, deferred maintenance, margin weakness, or working capital pressure. If you disclose them early and show a plan, buyers usually stay engaged. If they discover them late, trust drops and value often falls with it.

Weak financial records are also costly. If you cannot clearly show recurring versus project revenue, real segment margins, normalized EBITDA, capex needs, and cash conversion, buyers will either slow down or reduce price. In many businesses, six to twelve months is enough time to materially improve this.

A lack of a structured, competitive process is another avoidable valuation leak. Research and market experience consistently show that running a structured sale with competitive tension and the right advisor typically leads to meaningfully higher outcomes - often around 25% better purchase prices than a one-buyer conversation. In utilities, where buyer universes can be broader than founders expect, this matters a lot.

Another common mistake is telling buyers the price you want too early. That kills price discovery. If you tell the market you want USD 10m of enterprise value, many buyers will anchor right above that - maybe USD 10.1m or USD 10.2m - instead of showing you the real value they might have paid in a competitive process.

Two sector-specific mistakes are especially important in utilities. The first is failing to separate regulated or recurring revenue from project revenue in your materials. If those are blended together, the better revenue often gets dragged down. The second is under-documenting safety, compliance, and asset-condition performance. In this sector, those are not side issues. They are part of the valuation case.

10. What Utilities Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers care about

Start by making your reporting sharper. Split revenue by business line, customer type, and revenue quality. Show what is recurring, what is regulated, what is framework-based, and what is purely project-driven. That alone can change how buyers see the business.

Also improve margin transparency. If your better business lines are hidden inside blended reporting, bring them out clearly. Clean up working capital discipline and reduce one-off costs where possible. Buyers do not mind normal business imperfections, but they want to see what the business really earns.

Improve the quality and visibility of revenue

Where realistic, move revenue toward the more durable end of the spectrum. Renew contracts early. Extend framework agreements. Add maintenance and operations work to project relationships. Reduce overreliance on one customer or one contract cycle.

If you serve energy transition markets, make the exposure concrete. Buyers will care more about signed pipeline, recurring service work, and contracted rollout programs than broad claims about being well-positioned for the transition.

Reduce risk before buyers find it

Review safety records, compliance procedures, environmental matters, permit status, insurance, and any regulatory issues now - not during diligence. Fixing a weakness before going to market is much cheaper than negotiating around it later.

If your business depends heavily on you, start transferring relationships and responsibilities. Bring forward a second layer of management. Buyers pay more when they believe the company can perform well after the founder exits.

Sharpen the strategic story

Do not just describe what your business does. Explain why it matters. Are you a scarce regional utility platform? A specialist owner/operator with protected economics? A critical high-voltage capability provider? A water-focused business with unusual contract durability? The sharper the story, the easier it is for buyers to place you in the right valuation bucket.

This is also the time to prepare buyer-ready materials. Good materials do not just look polished. They frame the business in the language buyers use to justify paying more.

Run a real process, not a casual conversation

Even a great business can get an average price if the process is weak. Build a buyer list that goes wider than the obvious names. That often means strategics, infrastructure investors, private equity, and cross-border buyers who already know the sector.

A real process creates comparison, pressure, and optionality. In practical terms, that often matters just as much as improving EBITDA.

11. How an AI-Native M&A Advisor Helps

Selling a utilities business is partly about valuation, but it is also about reach and process. An AI-native M&A advisor can expand the buyer universe far beyond the handful of names most founders already know. By identifying hundreds of relevant acquirers based on deal history, strategic fit, synergies, and financial capacity, AI helps create more competition, better offers, and more fallback options if one buyer drops out.

It also speeds up the path to market. With AI helping match buyers, support outreach, prepare materials, and organize diligence, initial conversations and offers can often be reached in under 6 weeks. That speed matters because momentum is one of the biggest advantages in a sale process.

Just as importantly, AI does not replace expert advice - it strengthens it. The best outcome still comes from experienced M&A advisors who know how to frame the story, manage buyers, and negotiate the deal. The difference is that AI helps those advisors work faster, cover more ground, and support you with Wall Street-grade quality without the traditional bulge bracket cost base.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.