The Complete Valuation Playbook for Water Purification Businesses

A data-driven guide to how water purification businesses are valued and what drives higher multiples.

If you run a water purification business and you are considering a sale in the next 1-12 months, valuation is not just a spreadsheet exercise - it is a story about risk, repeatability, and who needs what you sell.

This playbook is built for water purification founders. It shows what similar businesses have actually sold for, explains why some outcomes land at the top of the range while others don’t, and gives you a practical framework and 6-12 month plan to improve your odds.

A big reason to think about valuation now: the sector is consolidating. Strategic buyers want capabilities in reuse, compliance, and “smart water” monitoring, while private equity is attracted to recurring aftermarket revenue and service contracts that behave like annuities. That’s good news - but only if your business is positioned the way buyers pay up for.

1. What Makes Water Purification Businesses Unique

Water purification is not one “industry” - it is a mix of product, projects, and ongoing service. That mix drives valuation more than almost anything else.

Main business types you see in this sector:

- Equipment and systems providers: filtration, membranes, RO, UV, dosing, packaged plants, mobile units, retrofit systems.

- Industrial wastewater specialists and niche tech: advanced oxidation, electrochemistry, PFAS removal, ammonia treatment, high-salinity / ZLD, mining and energy water.

- EPC and integrated water technology players: engineering, procurement, construction, plus sometimes operations.

- Services, testing, and compliance: water testing kits, lab services, legionella/hygiene compliance, field services.

- Monitoring / IoT and digital water: sensors, remote monitoring, software dashboards embedded in utility workflows.

- Water rights / resource platforms and utilities (adjacent but important): scarcity assets and regulated cash flows can command very different multiples than “normal” operating businesses.

Unique valuation considerations in water purification:

- Project revenue vs repeatable revenue: Buyers discount lumpy projects unless you can prove a reliable pipeline and a strong service tail.

- Aftermarket economics: Consumables, reagents, membranes, media replacement, rentals, monitoring subscriptions, and O&M contracts can transform the valuation profile.

- Compliance and approvals: Certifications, municipal approvals, and proven performance in regulated environments create switching costs and pricing power.

- Performance risk: Buyers will test whether your system reliably hits spec in the real world (water is messy, variable, and unforgiving).

Risk factors buyers always check:

- Customer concentration (one plant, one municipality, one EPC partner can be a big risk)

- Warranty and performance guarantees (and whether you’ve ever had to “eat” a bad installation)

- Regulatory exposure (PFAS, discharge permits, ballast water, reuse standards)

- Supply chain and install capacity (especially if your systems are custom)

- Safety, environmental liabilities, and contract terms that can create nasty surprises in diligence

2. What Buyers Look For in a Water Purification Business

Buyers value water purification businesses through three lenses: revenue quality, profitability and cash generation, and defensibility.

The obvious fundamentals still matter:

- Scale (revenue size)

- Growth (recent and believable)

- Gross margin and EBITDA margin

- Clean financials and proof the numbers match reality

But water purification has sector-specific “tells” that buyers care about even more:

Sector-specific buyer questions:

- How much of revenue is repeatable (service contracts, consumables, monitoring, rentals) vs one-time projects?

- Do you own a problem that customers must solve (compliance, uptime, permits), or are you seen as a vendor that can be swapped?

- Is your system standardized or mostly custom engineering?

- Do you have reference sites that a buyer can call and validate quickly?

- Are you embedded in customer workflows (monitoring, dosing analytics, reporting), or do you disappear after installation?

How private equity thinks about your business

Private equity (PE) is often buying with a plan to sell in 3-7 years. Their math is simple:

- They care what they pay now (entry multiple).

- They care what they can sell it for later (exit multiple).

- They want levers to improve earnings along the way.

Typical PE levers in water purification:

- Build recurring revenue: service plans, consumables programs, remote monitoring, membrane/media replacement schedules

- Pricing discipline: contract repricing, surcharge clauses, standardized scope

- Add-on acquisitions: bolt-ons that expand geography, capabilities, or service density

- Operational tightening: install efficiency, procurement, reducing warranty claims, improving project gross margins

- Cross-sell: chemicals, parts, testing, O&M into an existing installed base

PE pays more when the business already looks like a durable “platform” - not a founder-dependent project shop.

3. Deep Dive: The Biggest Valuation Nuance in Water - Recurring Aftermarket vs Project Revenue

Here’s the question that quietly decides whether you trade at a “normal equipment integrator” valuation or something materially higher:

Are you primarily paid once for a system - or paid repeatedly for outcomes over time?

The deal data and public comps consistently reward businesses that have a meaningful recurring component. In the premium drivers observed across transactions, embedded aftermarket and recurring revenue (consumables, monitoring, service) shows up as a common thread behind better outcomes, including cases where trusted testing brands and consumables pull valuations toward the 2-3x revenue territory in aftermarket-rich models. Meanwhile, project-heavy profiles often sit closer to the lower end of revenue multiples. (Premium drivers commentary; precedent transaction group ranges in sources.)

Why buyers care:

- Recurring revenue is easier to forecast.

- It reduces dependence on winning the next project.

- It typically carries better margins (especially software monitoring and consumables).

- It creates switching costs: once your parts, reagents, monitoring, and service plan are embedded, replacement is painful.

How you move from the “lower-value” version to the “higher-value” version:

- Convert installs into service contracts by default (even if small at first).

- Add remote monitoring and reporting so you stay in the customer’s workflow.

- Create a planned replacement program for membranes, media, UV lamps, filters.

- Offer performance-based tiers (“we guarantee spec, here’s the monthly plan”).

Mini-table:

4. What Water Purification Businesses Sell For - and What Public Markets Show

The most useful way to think about valuation is not “my business is worth X.” It’s: businesses like yours trade within a band, and your job is to earn your way toward the top of that band by reducing risk and improving revenue quality.

The data below separates private deals (what buyers paid) from public comps (what markets price). Use public multiples as a reference band - not a direct price tag for a private company.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions dataset, the overall average and median are around 2.9x EV/Revenue and 14.7x EV/EBITDA - but water is highly segmented. (Precedent transactions average group multiples in sources.)

At the segment level, the ranges show clear differences:

- Industrial & municipal equipment and systems tend to cluster around ~1.6x median EV/Revenue (average ~2.3x).

- Water infrastructure services / consulting / operations show higher revenue multiples in the data (median ~5.3x, average ~4.8x), reflecting stickier contracted work and operating relationships.

- Environmental testing / compliance services are lower on revenue multiples (median ~1.4x) but can show solid EBITDA multiples when margins and defensibility are clear.

- Water rights / resource intermediaries are a different animal (median ~5.6x revenue) because scarcity assets behave unlike operating companies. (All from precedent group multiples in sources.)

A simple way to interpret this: the more your model looks like repeatable contracted operations or scarce assets, the more the market pays on revenue. Pure equipment plus projects usually needs either strong profitability or a recurring tail to push valuation up.

These are not “rules.” They’re patterns from deals - your outcome depends on your mix, growth, margins, and risk.

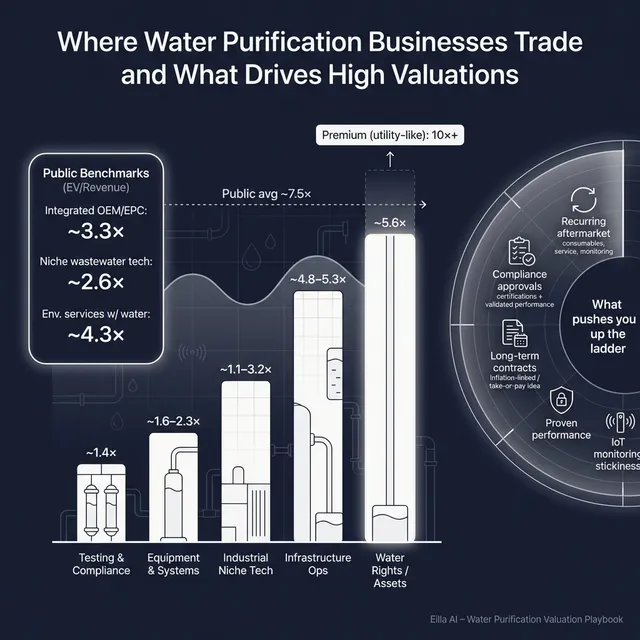

4.2 Public Companies

Public markets (as of mid-to-late 2025 per the dataset) show even wider dispersion, with an overall average and median around 7.5x EV/Revenue and 26.4x EV/EBITDA - but again, segmenting matters. (Public average group multiples in sources.)

By public group:

- Global integrated water technology OEMs & municipal EPC/operations: median ~3.3x revenue (average ~5.7x), median ~14.2x EBITDA (average ~30.0x).

- Industrial wastewater specialists & niche tech providers: median ~2.6x revenue (average ~11.6x), EBITDA multiples around ~10-11x on median/average - but revenue averages are skewed by outliers.

- Environmental services & waste management with water capabilities: median ~4.3x revenue (average ~7.8x), median ~18.9x EBITDA (average ~21.6x). (All from public average group multiples in sources.)

How to use public multiples correctly:

- Treat them as an upper and lower reference band, not your likely sale multiple.

- Private companies are usually adjusted downward for smaller scale, customer concentration, and key-person risk.

- Sometimes adjusted upward if you have scarce capabilities, strong recurring revenue, or a uniquely strategic footprint.

5. What Drives High Valuations (Premium Valuation Drivers)

The “premium outcomes” in the data aren’t magic. They come from a small set of buyer beliefs: this revenue will stick, this capability is hard to replace, and this business can compound.

Below are the premium drivers observed in the data, grouped into practical themes, plus a few fundamentals that always matter.

5.1 Compliance-driven, must-have capability

Premiums show up when your offering is non-discretionary: buyers must have it to meet standards (testing, disinfection, reuse, marine environmental rules) and you have recognized certifications or validated performance. (Premium driver: scarce compliance capability.)

What that looks like in practice:

- Third-party validations, certifications, and reference deployments that reduce buyer fear

- Documented performance across varying influent conditions

- A compliance reporting layer customers rely on

5.2 Recurring aftermarket and “installed base annuity”

Recurring mix (consumables, service, monitoring, replacement parts) smooths cyclicality and tends to lift valuation because buyers can underwrite it with more confidence. (Premium driver: embedded aftermarket and recurring revenue mix.)

Founder-friendly examples:

- Membrane/media replacement subscriptions tied to uptime guarantees

- Remote monitoring with monthly fee plus alarms and compliance reports

- Multi-year service plans bundled into every install

5.3 Utility-like visibility or scarcity dynamics

Very high premiums (in the data, >10x revenue) are linked to regulated cash flows or scarce, long-duration water assets - not typical for most operating water purification SMEs. (Premium driver: utility-like regulated cash flows; strategic control/exclusive territories.)

You can’t become a utility overnight, but you can borrow the logic:

- Long-term contracts with inflation-linked pricing

- Take-or-pay structures where customers pay for availability, not just usage

- Exclusive service concessions in defined territories (industrial parks, municipal zones)

5.4 Mission-critical monitoring and municipal switching costs

Digital/IoT monitoring embedded in municipal workflows can command higher revenue multiples because switching is painful and retention is strong. (Premium drivers: mission-critical digital/IoT; municipal approval processes.)

Practical moves:

- Add telemetry, analytics, and reporting on top of equipment installs

- Secure municipal approvals and build reference cities/utilities

- Make your platform the “system of record” for compliance reporting

5.5 Asset-light services with visible backlog

Even services businesses with modest revenue multiples can earn strong EBITDA multiples when backlog is contracted and delivery is repeatable. (Premium driver: asset-light advisory/engineering with contracted backlog.)

Founders can apply this even if you sell equipment:

- Productize O&M, optimization, and compliance services

- Standardize scopes and pricing

- Track backlog like a disciplined services firm

5.6 The fundamentals buyers always pay for

Even when your tech is great, buyers still reward:

- Clean financials that reconcile

- Diversified customers and industries

- A leadership bench beyond the founder

- Clear unit economics on installs (project margin by job, warranty history)

6. Discount Drivers (What Lowers Multiples)

Discounts happen when buyers see uncertainty, volatility, or “surprises waiting in diligence.” In water purification, the biggest value killers are usually predictable - and fixable.

Common discount drivers:

- Project-heavy revenue with weak backlog (buyers fear the cliff)

- Customer concentration (one refinery, one municipality, one EPC partner)

- Low or inconsistent gross margins (custom engineering, change orders, warranty pain)

- Unproven performance claims (no third-party validation, few reference sites)

- High warranty exposure or aggressive guarantees

- Founder dependency (sales, engineering, and key relationships sit in one person)

- Messy financials (mixing personal expenses, unclear job costing, poor revenue recognition)

Sector-specific red flags:

- Regulatory or permitting fragility: if your solution depends on approvals you don’t control, buyers price in delay risk.

- “Science project” tech positioning: patented does not automatically mean valuable - buyers pay for validated adoption, not patents alone.

7. Valuation Example: A Water Purification Company

This example is fictional. The company and the USD 10m revenue level are made up to show the logic. The valuation ranges are illustrative - not investment advice and not a formal valuation.

Step 1: The plain-English logic

If you sell hardware/equipment plus services (not pure software), a defensible starting point is usually EV/Revenue, especially when EBITDA is not clean or not yet stable.

From the provided data:

- Private equipment/system deals cluster around roughly ~1.1-3.2x revenue in the “equipment and systems” band. (Private football field 25th-75th in sources.)

- Public OEM/EPC comps show a corridor where the more defensible middle often sits around ~1.0-3.5x revenue, with upper quartiles into the ~4-5x range for stronger profiles. (Public comp corridor and quartiles in sources.)

- Higher 7-9x+ bands exist in the dataset, but they are typically tied to very different models (utilities, water rights, extreme micro-cap outliers, or special situations) and are not good anchors for a typical private equipment-plus-services SME. (Outlier discussion and premium drivers in sources.)

So you typically:

- Pick the closest segment band (equipment + services).

- Start with a core multiple corridor.

- Adjust up for recurring revenue, compliance moat, and switching costs.

- Adjust down for concentration, lumpiness, and performance risk.

Step 2: Apply it to a fictional company

Fictional company: ClearRiver Systems

- USD 10m revenue

- Sells packaged industrial reuse systems (membrane + polishing) and installs them

- 30% of revenue is recurring (service plans, monitoring, consumables)

- Gross margin is improving due to more standardized designs

- Customer base: industrial plants + a few municipal/utility-adjacent deployments

A practical set of scenarios:

How this maps to the dataset logic:

- The discounted multiple reflects SME risk, project exposure, and limited proof of repeatability - but stays above the lowest outliers because the business has real installs and a service component.

- The core range aligns with the equipment/system private band and the more defensible public OEM corridor.

- The premium scenario assumes ClearRiver has real evidence of premium drivers: meaningful recurring revenue, compliance validations, and early switching-cost dynamics - enough to justify the upper end of the corridor used in the worked example logic. (Base corridor selection and rationale in sources.)

Step 3: What this means for you

Two water purification businesses can both have USD 10m revenue and be worth radically different amounts - because buyers are paying for confidence and repeatability, not just sales.

Your job in the next 6-12 months is to turn “we think this will keep happening” into “here is the proof it will.”

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this like a mirror, not a grade. Score each factor 0-2:

- 0 = weak / not present

- 1 = partly true / improving

- 2 = strong / buyer-ready

How to interpret your total:

- High band: You likely resemble the profiles that can justify upper-range multiples in the sector corridors.

- Middle band: You can sell, but expect buyers to negotiate hard on risk - your upside comes from tightening proof points.

- Low band: You may still sell, but the best ROI is often doing 6-12 months of “de-risking work” first.

9. Common Mistakes That Could Reduce Valuation

9.1 Rushing the sale

If you go to market before your numbers and story are ready, buyers will smell urgency - and urgency is discounted. Prepare the narrative, the data room, and the buyer list before you start outreach.

9.2 Hiding problems

In diligence, issues surface. If you hide them, the problem becomes “risk plus trust collapse,” which is worse. You’re better off framing the issue and showing a plan and proof of progress.

9.3 Weak financial records

Water purification businesses often suffer from unclear job costing and mixed project vs service margin reporting. Clean this up:

- Project margin by job (planned vs actual)

- Service gross margin separately tracked

- Warranty and rework costs clearly identifiedThis is one of the fastest ways to increase buyer confidence.

9.4 Not running a structured, competitive process with an advisor

A competitive process creates leverage. Research is commonly cited in the industry that running a structured process with an advisor can lead to meaningfully higher outcomes (often referenced around ~25% higher purchase prices) because it improves positioning, buyer competition, and negotiation dynamics.

9.5 Revealing what price you want instead of letting the market bid

If you tell buyers you want “USD 10m,” you often cap your own upside. Many buyers will come back at USD 10.1m or USD 10.2m instead of showing you what they would truly pay in a competitive process. Price discovery works when you create demand first.

9.6 Water-specific mistake: treating performance proof as optional

In this sector, buyers do not buy claims - they buy validated outcomes. If you can’t quickly provide reference sites, performance data, and third-party validations, buyers either discount heavily or walk.

10. What Water Purification Founders Can Do in 6-12 Months to Increase Valuation

Think in three tracks: improve the business, improve proof, improve the process.

10.1 Improve revenue quality (biggest payoff)

- Turn every install into a default service contract option (good/better/best tiers)

- Launch an installed base program: consumables, replacement schedules, preventative maintenance

- Add remote monitoring and compliance reporting where feasible

- Reduce concentration: land 2-3 new anchor customers in different plants/industries

This directly aligns with premium outcomes tied to recurring revenue mix and switching costs. (Premium drivers in sources.)

10.2 Reduce operational risk buyers fear

- Standardize designs: fewer custom one-offs, more repeatable SKUs/configurations

- Tighten project execution: improve install margin consistency and reduce rework

- Track warranty costs and implement root-cause fixes

- Ensure contracts don’t include open-ended performance liabilities

10.3 Build defensibility and trust

- Secure key certifications and third-party validations

- Create a “reference pack”: case studies, performance curves, customer contacts, before/after data

- If you sell into municipalities, invest in approvals and a small set of flagship deployments (switching costs matter here). (Premium drivers: municipal approvals; IoT stickiness in sources.)

10.4 Make the company easier to buy

- Clean financials with clear segmentation (projects vs service vs consumables)

- Build a leadership bench: a buyer wants to know the business runs without you

- Prepare diligence materials early: customer contracts, backlog, gross margin bridge, product documentation

11. How an AI-Native M&A Advisor Helps

A strong exit is often less about one buyer “loving” you and more about creating the conditions where multiple buyers compete. An AI-native advisor helps by expanding reach and accelerating the process without sacrificing quality.

Higher valuations through broader buyer reach: AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, and synergy signals. More relevant buyers means more competition, stronger offers, and more backup options if a buyer drops late in the process.

Initial offers in under 6 weeks: AI-driven buyer matching and connecting, faster creation of marketing materials, and structured support through diligence can compress timelines. The result is earlier serious conversations and faster initial indications of interest than a purely manual process.

Expert advisory, enhanced by AI: You still need experienced humans running the deal - framing the story, defending the valuation, and negotiating terms. AI strengthens that work by improving targeting, tightening materials, and keeping the process disciplined, delivering Wall Street-grade advisory quality without traditional “bulge bracket” costs.

If you’d like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.