The Complete Valuation Playbook for Wireless Network Infrastructure Businesses

A practical, data-driven guide to how wireless network infrastructure businesses are valued and what drives higher multiples.

If you run a wireless network infrastructure business and you are considering a sale in the next 1-12 months, valuation is not just a number - it is the result of how buyers perceive your risk, your growth durability, and how “strategic” your asset is to them.

This playbook is built for founders and CEOs in wireless network infrastructure: fixed wireless OEMs, backhaul and access equipment, network engineering and integration services, RF components and antennas, private network connectivity platforms, and adjacent managed connectivity providers. It will show what similar businesses actually sell for, decode what drives higher vs lower multiples, and give you a practical self-assessment plus a 6-12 month action plan.

1. What Makes Wireless Network Infrastructure Businesses Unique

Wireless network infrastructure businesses get valued differently because buyers are underwriting two things at once:

- Technology and product risk (Does it work? Will it keep working as standards evolve?)

- Deployment and customer risk (Will carriers, utilities, or enterprises keep buying - and keep renewing?)

The main types of businesses in this sector

Most privately held wireless network infrastructure companies fall into a few recurring shapes:

- Hardware OEMs: Fixed wireless access and backhaul equipment (PTP/PTMP radios, microwave/mmWave, CPE), often with network management software attached.

- RF components and antennas: Filters, antennas, mmWave components, and adjacent RF subsystems.

- Network build, engineering, and services: Base station work, indoor DAS, maintenance, field services, integration, and turn-key deployments.

- Operators and managed connectivity: ISPs, FWA operators, wholesale connectivity, managed enterprise networks.

- Private network and IoT connectivity platforms: Private LTE/5G, programmable SIM/IoT connectivity, edge Wi-Fi/mesh - often more “software + service” than pure hardware.

Unique valuation considerations buyers will focus on

Wireless infrastructure is often “lumpy” and buyer psychology reflects that:

- Carrier and enterprise buying cycles create volatility. Even good businesses can have uneven quarters.

- Mix matters more than founders expect. A hardware-heavy revenue mix prices differently than a managed service or software-rich mix.

- Support burden and field complexity are real. Buyers discount businesses that scale revenue but require constant engineering fire drills to deliver.

- Working capital can swing enterprise value. Inventory, WIP, customer deposits, and receivables can meaningfully change the cash you take home.

Key risks buyers always check

Expect diligence to probe these areas hard:

- Customer concentration and contract durability (especially if you rely on a handful of carriers, utilities, or distributors).

- Product roadmap and standards risk (5G evolution, spectrum changes, interoperability, Open RAN dynamics).

- Security posture (especially for government, defense, utilities, and critical infrastructure deployments).

- Supply chain resilience (single-source components, long lead times, warranty exposure).

- Unit economics at scale (gross margin by product line, services margin, and whether support costs are creeping up).

2. What Buyers Look For in a Wireless Network Infrastructure Business

Buyers do not pay for what your business did - they pay for what they believe it can do predictably after they own it.

The obvious fundamentals still matter

- Revenue scale and growth: Growth matters, but in this sector buyers care about repeatability, not one-time project spikes.

- Gross margin and EBITDA margin: Profitability is a proxy for product maturity, pricing power, and operational control.

- Customer retention: In infrastructure, “retention” often looks like repeat orders, renewals for managed services, or multi-year maintenance and support.

Industry-specific “tell me what you really are” questions

Buyers typically try to classify you into one of two buckets:

- Product company (OEM or components)

- Do you have defensible IP (RF performance, firmware, interference mitigation, antenna design)?

- Are you locked into a few channel partners?

- How much of your growth is tied to a single product cycle?

- Services and deployment company (engineering and integration)

- How repeatable are your engagements?

- How much margin is tied to specific crews or key engineers?

- Do you have multi-year MSAs, or are you living project to project?

A quick guide to how private equity thinks about your business

Private equity (PE) buyers are typically underwriting:

- Entry multiple vs exit multiple: They care what they pay today and what they can plausibly sell for in 3-7 years.

- Who buys it next: A larger strategic buyer, a bigger PE fund, or (rarely) an IPO.

- Levers they expect to pull:

- Add recurring revenue (support contracts, managed services, monitoring, security).

- Improve pricing discipline and discounting.

- Reduce delivery complexity and standardize implementations.

- Do add-on acquisitions (common in services and component categories).

In plain terms: PE pays more when they can see a clear path from “good business” to “great business” without betting the farm on a new technology cycle.

3. Deep Dive: Hardware-Only vs Hardware + Software/Services - The Single Biggest Multiple Divider

If you only take one idea from this playbook, take this one:

In wireless infrastructure, your multiple often depends less on “what you sell” and more on “how you get paid over time.”

Why it matters

Two companies can both sell wireless equipment into the same end markets, but one gets valued like a cyclical hardware vendor and the other gets valued like a sticky connectivity platform.

How this shows up in deal outcomes

The data shows premium outcomes when buyers believe the business has a high-margin, software- or services-rich, mission-critical layer - not just boxes shipped. For example, premium valuation commentary highlights outcomes where connectivity is bundled with monitoring, cybersecurity, managed operations, or niche mission-critical service delivery. These profiles were associated with higher EBITDA multiples in observed deals such as the maritime connectivity and cybersecurity example and services-rich connectivity providers. (See the premium driver theme: “High-Margin, Software- or Services-Rich Connectivity with Mission-Critical Use Cases.”)

Why buyers care

- Recurring revenue de-risks forecasting. Buyers can model it - and lenders are more comfortable financing it.

- Services and software create switching costs. If your monitoring, analytics, or security layer is embedded, replacement is painful.

- It changes the integration story. Strategics can cross-sell your managed layer into their installed base, supporting synergy narratives.

How to move from the lower-value profile to the higher-value profile

You do not need to “become SaaS.” You can improve your valuation profile by changing packaging and contracts:

- Turn warranty and support into tiered support plans with clear SLAs.

- Bundle “network outcomes” (uptime, latency targets, security monitoring) instead of selling only hardware.

- Productize deployment: fixed scopes, standardized BOMs, fewer custom one-offs.

A simple lens buyers use:

4. What Wireless Network Infrastructure Businesses Sell For - and What Public Markets Show

Here is the core reality: private deals cluster in “sensible” ranges, while public markets show wider dispersion because scale, liquidity, and outliers exist.

Also note: public multiples move with the market. Treat the public reference points below as representative of where this ecosystem was trading around mid-to-late 2025 based on the provided set.

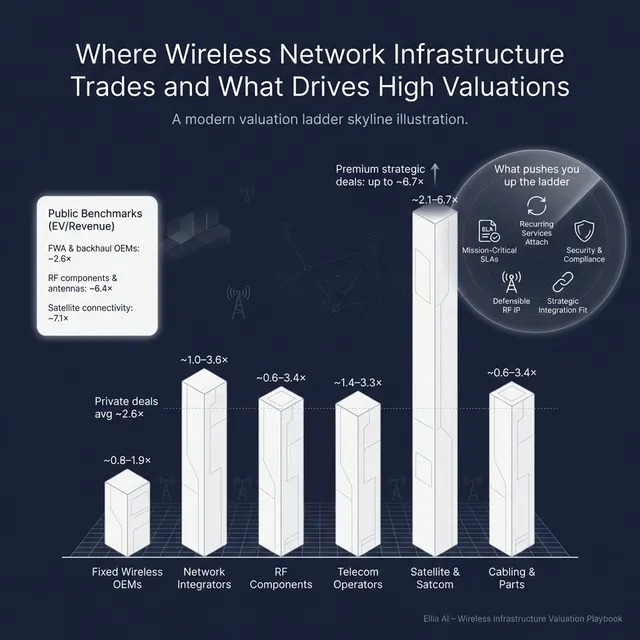

4.1 Private Market Deals (Similar Acquisitions)

Across precedent transactions in this broader wireless infrastructure universe, the overall average and median were around 2.6x EV/Revenue and 6.7x EV/EBITDA (all categories blended). But category mix drives big differences.

A helpful way to interpret private multiples:

- Equipment manufacturers tend to cluster lower on revenue multiples unless there is a strong premium narrative.

- Services and integrators can trade higher on revenue multiples when there is a durable, repeatable book of work - but EBITDA multiples often reflect execution risk and labor intensity.

- Satellite and connectivity systems show higher revenue multiples in some deals, but dispersion is wide depending on strategic context.

Illustrative private deal ranges by segment (from the provided transaction set):

These are illustrative ranges, not “price tags.” Your exact outcome depends on growth, margins, customer mix, and the buyer universe.

4.2 Public Companies

Public markets provide a “reference band,” but you must adjust for:

- Smaller scale and lower liquidity (private discount is common).

- Higher customer concentration.

- Less diversified product lines.

- Sometimes, scarcity can create a premium (a buyer needs your asset to accelerate a roadmap).

From the provided public segment averages:

How to use this as a founder:

- Use public multiples as outer guardrails, not a direct valuation.

- Expect adjustments downward for private scale and risk.

- Expect adjustments upward only when you have clear premium drivers (below) and a competitive process that creates real buyer tension.

5. What Drives High Valuations (Premium Valuation Drivers)

Premium outcomes in this sector are not magic. They usually come from a small set of repeatable narratives buyers will pay up for.

Below are the most common premium themes, anchored in the observed premium driver set, plus standard M&A “must-haves.”

5.1 Strategic integration synergies for large buyers

Strategic acquirers pay more when they can clearly explain:

- Why your product plugs into their portfolio

- How they can cross-sell it quickly

- Where they can reduce duplicated costs

This showed up in transactions where the buyer could fold antennas, test solutions, or network equipment into a larger platform and capture synergy value beyond standalone metrics. The buyer is effectively paying for “faster time-to-strategy.” (Premium driver: Integration Synergies for Large Strategic Buyers.)

Practical examples:

- You have named accounts the buyer already sells into.

- Your radios or edge gear attach naturally to their fiber, core, or managed services.

- You have an integration toolkit (APIs, provisioning, OSS/BSS hooks) that reduces rollout risk.

5.2 High-margin, mission-critical software and services layers

Buyers pay more when your margin profile suggests you are not just shipping hardware - you are delivering an outcome.

The data highlights premium outcomes in services-rich, mission-critical connectivity contexts (managed operations, cybersecurity, niche vertical connectivity). (Premium driver: High-Margin, Software- or Services-Rich Connectivity with Mission-Critical Use Cases.)

Practical examples:

- Managed private network SLAs for utilities, ports, logistics, mining.

- Monitoring and RF analytics that customers rely on daily.

- Security features that are “required,” not optional.

5.3 Vertical IP moats in RF, firmware, or silicon

Premium narratives emerge when your differentiation is hard to copy:

- Proprietary PHY/MAC algorithms

- Interference mitigation and spectrum efficiency advantages

- Antenna or beamforming IP

- In rare cases, ownership of key chipset layers

This theme appears in deals where vertical integration of chipsets or deep hardware IP created strategic value beyond near-term profitability. (Premium driver: Vertically Integrated Chipset/Hardware IP.)

Practical examples:

- Measurable performance advantage vs competitors in real deployments.

- Certifications, patents, or defensible engineering lead time.

- A roadmap that buyers can leverage across multiple product lines.

5.4 Regulated or defensible niches with durable recurring demand

Some wireless infrastructure businesses live in environments where:

- Regulatory approvals are hard

- The geography is hard to serve

- The customer base is mission-critical

That defensibility can support premium outcomes even if growth is not “venture-like.” (Premium driver: Geographic or Sector Niche with Defensible Recurring Demand and Regulatory Barriers.)

Practical examples:

- Government or utility contracts with multi-year terms.

- Maritime, disaster response, public safety, critical infrastructure connectivity.

- A region with limited competition due to approvals, terrain, or logistics.

5.5 Strategic adjacency to space, satellite, or defense - when real

This is not for everyone, but it can be a genuine premium band when credible:

- Space and satellite adjacency (direct-to-device, phased arrays, payload integration) has driven outlier outcomes in the provided set.

- Defense and security signal intelligence or EW optionality can broaden buyer pools.

The key word is credible. Buyers will not pay for “optionality” unless you can prove real product fit, programs, or IP relevance. (Premium drivers: Strategic Technology Adjacency to Space and Satellite; Defense and Security Signal Intelligence / EW Capability Optionality.)

5.6 The unsexy premium drivers buyers still demand

Even if your tech is great, buyers pay more when basics are clean:

- Clean financials and clear revenue recognition

- Strong leadership bench beyond the founder

- Diversified customer base and a clear pipeline

- Documented KPIs (bookings, backlog, churn/renewals, gross margin by line)

6. Discount Drivers (What Lowers Multiples)

Low-end outcomes usually come from one of two things: risk or uncertainty. Buyers discount what they cannot underwrite.

Common discount drivers in wireless infrastructure:

6.1 Revenue that is “lumpy” without a clear engine

- One-off deals that cannot be repeated

- Dependence on a single spectrum event, grant program, or product cycle

- Weak backlog visibility

What helps: show multi-year repeatability (renewals, support contracts, repeat orders, MSAs).

6.2 Too much customer concentration

If one customer can pause capex and cut your year in half, buyers price that risk.

What helps: demonstrate expansion across accounts, geographies, or verticals - and show how fast you can replace lost revenue.

6.3 Hardware economics without a moat

If your differentiation is “we are cheaper,” buyers worry about margin compression and competitive churn.

What helps: prove performance differentiation, certifications, switching costs, and installed-base stickiness.

6.4 Services businesses that are founder-dependent

For integrators and engineering-heavy businesses, buyers discount:

- Projects that rely on a few key people

- Inconsistent gross margins

- Poor documentation and inconsistent delivery

What helps: standardized delivery playbooks, training systems, and a second layer of leaders.

6.5 Weak visibility into true profitability

If your financials blur product margin, services margin, warranty costs, and support burden, buyers assume the worst.

What helps: segment reporting, clean KPIs, and credible explanations of margin drivers.

7. Valuation Example: A Wireless Network Infrastructure Company

This is a worked example to show how the logic works, not a prediction. The company and revenue are fictional, and the valuation ranges are illustrative - not investment advice or a formal valuation.

Step 1: The valuation logic

For a small-to-mid-sized wireless infrastructure business, buyers typically triangulate:

- Closest public comps (as reference bands)

- Closest private precedent deals (what buyers actually paid)

- Your business profile (hardware vs services mix, margins, growth, customer risk, IP)

For a hardware-centric fixed wireless OEM at around USD 10m revenue, the provided logic suggests a defensible baseline of roughly ~1.2-2.2x EV/Revenue, anchored on the closest public hardware categories (fixed wireless OEM/backhaul, RAN OEM, broadband access hardware) and private equipment deal bands. The private equipment precedent set also supports a roughly ~0.8-1.9x EV/Revenue band for comparable equipment manufacturers.

Premium drivers can push you above that if you credibly shift toward:

- Higher-margin recurring services/software

- Strong growth with improving margins

- Clear strategic synergy or defensible IP

Discount drivers can pull you down if you have:

- Concentration, lumpy revenue, weak margins

- Commodity positioning

- Poor financial clarity

Step 2: Apply it to a fictional company

Fictional company: “SkyBridge Wireless”

- Revenue: USD 10.0m (fictional)

- Mix: 70% fixed wireless backhaul equipment, 30% support + network monitoring subscriptions

- Gross margin: improving due to better software attach and standardized deployments

- Customers: mix of regional ISPs and a few enterprise private network wins

Illustrative valuation scenarios (EV based on revenue multiple):

Step 3: What this means for you

Two businesses can both be “USD 10m revenue” and still land in very different valuation outcomes because buyers pay for:

- durability of revenue,

- predictability of margins,

- and strategic value to the buyer universe.

If your goal is to maximize price, the play is not “argue for a higher multiple.” The play is to earn it by reducing perceived risk and making your premium narrative undeniable.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as a fast, honest diagnostic. Score each factor 0-2:

- 0 = weak / unclear

- 1 = okay

- 2 = strong / buyer-ready

Scoring table

How to interpret your total

- High band: You look like a premium asset - you are likely to attract more buyer types and better terms.

- Middle band: You are “fair market” - price will be sensitive to process quality and buyer fit.

- Low band: You will get offers, but you are likely to be valued like a riskier, more cyclical asset unless you fix the biggest red flags.

The goal is not a perfect score. The goal is to identify the 2-3 changes that most move buyer perception.

9. Common Mistakes That Could Reduce Valuation

9.1 Rushing the sale

If you start a process without clean numbers, a tight narrative, and a buyer-ready data room, you force buyers to assume risk. Risk shows up as lower price, tougher terms, or both.

9.2 Hiding problems

Issues will surface in diligence. When buyers find them late, they do not just re-price the deal - they lose trust and start protecting themselves with holdbacks, earn-outs, or walk-away rights.

9.3 Weak financial records

Wireless infrastructure buyers want to understand:

- gross margin by product line,

- services margin vs hardware margin,

- warranty reserves and support burden,

- true EBITDA after normalizing one-time items.

If your reporting cannot answer those questions quickly, you will pay for it in valuation.

9.4 Not running a structured, competitive process with an advisor

You do not get the best price by “finding one buyer.” You get it by creating competition and controlling information flow.

Some sell-side market guidance cites that advisors can increase final sale price by 6%-25% by expanding buyer coverage and running a tighter process. (Axial) Even if your result is not exactly that number, the underlying mechanism is real: more qualified bidders typically means stronger price and terms.

9.5 Revealing what price you are after instead of letting the market bid

If you say you want “USD 10m,” many buyers will anchor close to it (USD 10.1m, USD 10.2m) rather than showing you what they might have paid in a competitive situation.

Price discovery works when buyers tell you their number first - and you make them compete.

9.6 Two wireless-specific mistakes that show up often

- Over-customization: bespoke deployments can win deals but destroy scalability and margin clarity.

- Under-investing in security and compliance: in critical infrastructure and enterprise private networks, weak security posture can eliminate whole buyer categories.

10. What Wireless Network Infrastructure Founders Can Do in 6-12 Months to Increase Valuation

You rarely need a massive pivot. You need focused, buyer-aligned upgrades.

10.1 Improve the numbers buyers trust

- Build segment margin reporting: hardware gross margin, services gross margin, warranty/support costs.

- Reduce “surprise” costs: tighten warranty reserves, standardize installs, document support burden.

- Clean up working capital: reduce aged receivables, rationalize inventory, document backlog and shipment cadence.

10.2 Increase recurring and reduce lumpiness (without becoming SaaS)

- Launch tiered support and SLA packages (good, better, best).

- Bundle monitoring, RF analytics, and security as paid add-ons.

- Convert repeatable customers into multi-year frameworks or MSAs where possible.

This directly maps to premium outcomes associated with services-rich, mission-critical connectivity layers. (Premium driver: High-Margin, Software- or Services-Rich Connectivity with Mission-Critical Use Cases.)

10.3 De-risk the customer story

- Create a plan to reduce top-customer dependence (even modest progress helps).

- Document pipeline quality: named opportunities, stages, and close rates.

- Build vertical case studies (utilities, ports, mining, public safety) that demonstrate repeatability.

10.4 Make your differentiation provable

- Publish performance benchmarks that matter (throughput, reliability, interference resilience).

- Package your IP story: what is actually proprietary (firmware, RF design, provisioning, security).

- If you have credible adjacency to defense or satellite ecosystems, document it with proof (programs, certifications, deployments) - optionality only matters when it is real. (Premium drivers: Defense/EW optionality; Space/satellite adjacency.)

10.5 Build the “buyer-ready” machine

- Create a clean data room with contracts, customer list, KPIs, product roadmap, and financial segmentation.

- Reduce founder dependence by elevating a commercial and operational second-in-command.

- Build an “equity story” that explains why your business wins and why it keeps winning.

11. How an AI-Native M&A Advisor Helps

Selling a wireless infrastructure business is hard because the buyer universe is fragmented: strategics, components consolidators, managed connectivity platforms, regional operators, defense-adjacent groups, and PE funds all look at your business differently.

An AI-native M&A advisor helps in three practical ways:

Higher valuations through broader buyer reach. AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, synergy fit, and financial capacity. More relevant buyers creates more competition, stronger offers, and more fallback options if one buyer drops.

Initial offers in under 6 weeks. AI-driven buyer matching, faster outreach, and accelerated creation of marketing materials can compress timelines so you reach serious conversations and initial offers much faster than a manual-only process.

Expert advisory, enhanced by AI. The best outcomes still require experienced human bankers: positioning, negotiation, and process control. AI helps them move faster, cover more ground, and present your business with “public-company-grade” clarity - without traditional bulge-bracket cost structures.

If you’d like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.