The Complete Valuation Playbook for Workforce Management Businesses

A data-driven guide to what Workforce Management businesses are worth today and what drives high mutliples.

If you run a Workforce Management (WFM) software business and you are considering a sale in the next 1-12 months, you’re stepping into a market that is both crowded and consolidating at the same time. Big platforms keep buying features and customer bases, and private equity still likes predictable subscription revenue - but buyers have become more selective about what they pay up for.

This playbook is built for founders and CEOs of privately held WFM businesses. It will show you what businesses like yours actually sell for, explain what pushes multiples higher or lower, and give you a practical self-assessment plus a 6-12 month action plan to improve your valuation.

1. What Makes Workforce Management Unique

Workforce Management businesses sit in a special spot: you are often “mission-critical” (payroll, time tracking, compliance, staffing rules), but you’re also exposed to operational complexity (implementation, integrations, labor laws, union rules, shift patterns, hardware, and messy customer data).

The main types of WFM businesses

Most WFM companies fall into a few recognizable models:

- Frontline scheduling, time and attendance: shift planning, clock-in/out, overtime rules, leave, compliance.

- HCM + payroll suites: scheduling plus HR records, payroll, benefits, tax and compliance workflows.

- Workforce engagement layers: internal comms, training, pulse surveys, wellbeing, safety, performance.

- Contingent labor platforms: vendor management systems (VMS), temp labor matching, workforce marketplaces.

- Services-heavy payroll and HR outsourcing: recurring service revenue with software as an enabler, not the product.

Why valuation works differently here

WFM valuation is not only about growth. It’s also about risk and friction:

- Switching cost is high (payroll and scheduling changes are painful) - which can create sticky revenue, but only if your product is deeply embedded.

- Data and integrations matter more than founders expect. Buyers will ask: “How hard is it to integrate into our suite?”

- Implementation burden can kill SaaS economics. If every new customer needs a bespoke rollout, buyers will treat you like a services business.

- Compliance and liability are real. A payroll error is not a minor bug - it’s reputational damage and sometimes legal exposure.

Key risk factors buyers will always test

In WFM, buyers almost always dig into:

- Payroll accuracy and compliance readiness (tax rules, wage/hour, local labor laws, audit trails).

- Retention and churn by customer segment (SMB vs enterprise, frontline verticals like healthcare or retail).

- Implementation repeatability (time-to-go-live, partner ecosystem, reliance on founders).

- Security and privacy posture (employee data is sensitive; certifications and clear controls reduce buyer fear).

- Customer concentration (a few big employers can drive big ARR - and big risk).

2. What Buyers Look For in a Workforce Management Business

Most buyers - strategic acquirers and private equity - look at your business through the same simple lens:

- How predictable is revenue?

- How fast is it growing?

- How risky is it?

- How much could it be worth later?

The “obvious” fundamentals still matter

Even in WFM, the basics drive a lot of valuation:

- Recurring revenue percentage (subscription and contracted revenue beats one-off implementation fees).

- Growth rate (especially if it’s consistent quarter-to-quarter).

- Gross margin (software-like margins beat labor-heavy delivery).

- Customer retention (customers sticking around is the clearest proof you’re mission-critical).

- Clean financials (buyers pay more when they can trust the numbers).

Industry-specific things buyers care about

WFM buyers will also price your company based on sector-specific realities:

- Payroll + compliance credibility: If you touch payroll, buyers want to know you won’t create liability.

- Vertical “fit”: WFM is not one market. Healthcare scheduling looks different from retail, which looks different from logistics.

- Integration surface area: Buyers pay more for products that integrate cleanly into HRIS, ERP, accounting, identity, and time clock ecosystems.

- Product depth vs breadth: A broad suite can be valuable, but only if modules are truly adopted (not just “checkbox features”).

How private equity thinks about your WFM business

Private equity (PE) typically asks three questions:

- What multiple am I paying today, and what multiple can I sell at in 3-7 years?If your company can mature from “founder-led product” to “scaled platform,” PE can justify paying more.

- Who can buy this later?A bigger PE fund? A large strategic platform? A payroll giant? If the “next buyer” set is clear, valuation improves.

- What levers can I pull?In WFM, PE often expects to:

- Increase prices (especially if you are underpriced for compliance-critical value)

- Improve retention (customer success discipline)

- Reduce services intensity (standardize onboarding)

- Add bolt-ons (adjacent modules or regional expansion)

3. Deep Dive: Suite Breadth vs Implementation Burden - The Trade-Off That Moves Multiples

Here’s a WFM valuation nuance that matters more than founders expect:

Does your “suite” create real expansion value - or does it create more implementation pain?

Buyers love the idea of a suite (scheduling + HR + payroll + engagement). But they will only pay up if the suite is adopted, sticky, and scalable - not if it means every deal needs custom configuration and heavy services.

How this shows up in the data

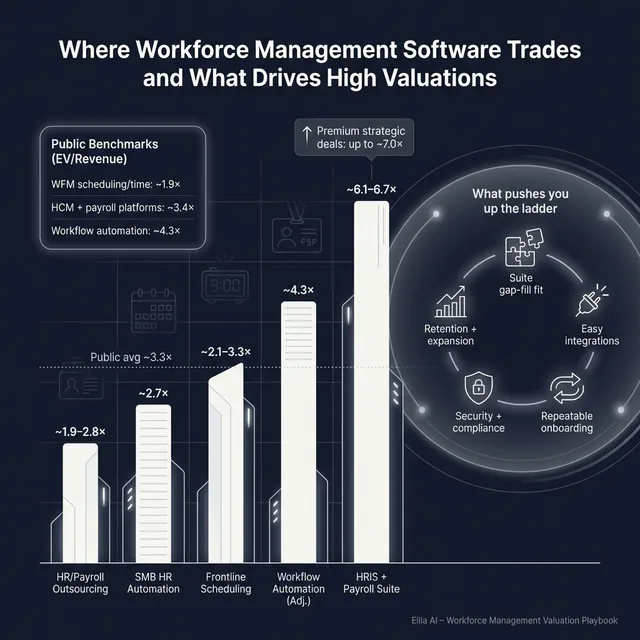

In public markets, “enterprise HCM and payroll platforms” trade at higher revenue multiples on average than pure scheduling/time tools (about 3.4x EV/Revenue vs 1.9x EV/Revenue, based on grouped public comps). Meanwhile, private deals for HRIS/payroll suite-like businesses show higher revenue multiples than scheduling-only WFM (around 6.4x vs 3.0x EV/Revenue in the grouped private comps).

That gap is the market telling you something: breadth can be valuable - but only when it behaves like software, not like a services project.

Why buyers care

A suite can justify a premium because it can create:

- Higher retention (harder to switch multiple modules at once)

- Higher revenue per customer (customers expand into more modules over time)

- More strategic relevance (the product becomes part of the core HR/payroll stack)

But the flip side is brutal:

- If your suite requires heavy implementation, buyers see delivery risk and margin pressure.

- If module adoption is shallow, buyers see “shelfware risk” (features that don’t get used).

How to move from “lower-value suite” to “higher-value suite”

If you’re more on the “painful suite” end today, you can shift in 6-12 months:

- Standardize onboarding into a repeatable playbook (fewer bespoke rollouts).

- Prove module adoption with clear usage metrics (not just “we sell it”).

- Build integration templates (common HRIS/payroll/accounting systems).

- Package and price based on outcomes (compliance, overtime savings, manager time saved).

4. What Workforce Management Businesses Sell For - and What Public Markets Show

Multiples are not “your price.” They are a language buyers use to compare deals. The smart way to use them is to understand where your business likely sits and what levers move you up or down.

The data below combines:

- Private acquisition multiples across relevant deal groups, and

- Public market trading multiples across workforce and adjacent software categories (as of mid/end 2025, per the dataset).

4.1 Private Market Deals (Similar Acquisitions)

Across the relevant private deal groups, WFM-related businesses tend to fall into a few bands:

- Scheduling-centric WFM SaaS tends to transact in a moderate revenue multiple range.

- Full-suite HRIS/payroll platforms tend to command meaningfully higher revenue multiples.

- Outsourcing/services-heavy models tend to price lower because a bigger share of revenue is “people-delivered.”

Here’s the simplest way to read the private market data:

These are illustrative ranges, not a promise. Your multiple depends on your growth, margin profile, risk, and deal dynamics.

4.2 Public Companies

Public markets provide a “gravity” reference point. Private deals can be above or below public comps depending on scarcity, growth, and buyer strategy - but public multiples still shape buyer expectations.

Using the grouped public comps:

- Enterprise HCM and payroll platforms trade around 3.4x EV/Revenue and 13.9x EV/EBITDA on average.

- Workforce scheduling and time/attendance trades lower on revenue multiple (about 1.9x average, 1.3x median), with EV/EBITDA stats that swing widely because some companies have unusual profit profiles.

- Enterprise workflow automation platforms (adjacent, non-HCM) trade higher (about 4.3x EV/Revenue and 30.1x EV/EBITDA), reflecting broader platform value.

- Overall across the dataset: about 3.3x EV/Revenue and 20.3x EV/EBITDA.

*The scheduling/time category shows a very wide spread between average and median EV/EBITDA in the grouped data, which usually means the “average” is skewed by outliers.

How to use public multiples correctly

Use public multiples as reference bands, not as your valuation.

- Adjust down for smaller scale, less predictable growth, customer concentration, or higher services intensity.

- Adjust up when your asset is scarce, deeply embedded, and strategically important to a buyer (especially if it fills a suite gap).

5. What Drives High Valuations (Premium Valuation Drivers)

Here’s what consistently pushes WFM businesses toward the top of the range - combining the observed deal patterns and what buyers reliably pay up for in this sector.

5.1 “Suite gap-fill” value and integration optionality

Buyers pay more when your product clearly fills a missing module in their suite and can be integrated with low friction. In the deal data, acquirers explicitly referenced plans to keep products standalone but integrate into a broader ecosystem over time, which signals they were underwriting more than current revenue.

What makes this real (not just a story):

- Proof you drive partner-sourced pipeline or attach rates

- Clean APIs and integration templates

- A product that is truly “missing” in the buyer’s lineup

5.2 Strategic tuck-ins priced on roadmap (not today’s revenue)

Some of the most extreme EV/Revenue outcomes in the dataset come from tiny revenue bases where buyers were clearly paying for product/roadmap optionality rather than current scale.

Founder takeaway: you can benefit from this dynamic if you are a clear strategic fit - but don’t assume these outlier multiples are “market pricing” for a normal standalone business. They are usually about option value.

5.3 Earn-outs that let buyers pay for upside

Multiple deals in the dataset used earn-outs tied to “stretch” performance targets. Earn-outs can support higher headline valuations because they let the buyer agree to your upside story while protecting against downside.

You get the best earn-out outcomes when:

- Targets are based on simple, auditable KPIs (ARR, revenue, EBITDA)

- Your go-to-market motion is repeatable post-close (not founder-dependent)

5.4 Security and compliance posture that reduces buyer fear

Where the product touches sensitive employee data, buyers pay more (or at least discount less) when your security and compliance posture is strong. Certifications and clear controls reduce diligence friction and widen the buyer universe, especially for enterprise adoption.

Practical examples founders recognize:

- Clear audit logs for payroll and time edits

- Strong role-based permissions

- Documented security program and third-party testing

5.5 Exceptional profitability at scale (even if revenue multiple looks “normal”)

Some deals and comps show a pattern: EV/Revenue might look modest, but EV/EBITDA can be strong when profitability is real and durable.

In WFM, buyers believe profitability when:

- Implementation is standardized

- Support costs don’t explode with growth

- Renewals are strong without heavy discounting

5.6 The “boring” premium drivers that still matter

Even if they don’t sound exciting, these are consistently associated with better outcomes:

- Clean financial statements you can defend

- Predictable recurring revenue and low churn

- Customer diversification (not “one whale”)

- A leadership bench that can run without you

6. Discount Drivers (What Lowers Multiples)

Discounts happen when buyers see risk, uncertainty, or a business model that won’t scale cleanly.

The biggest WFM-specific valuation discounts

- Services-heavy delivery: If growth requires lots of people, buyers apply lower multiples because margins are harder to scale.

- Weak retention or unclear churn: If customers don’t stick, your “mission-critical” claim doesn’t hold.

- Payroll and compliance risk: Any history of payroll errors, unclear compliance controls, or messy audit trails triggers buyer caution.

- Integration fragility: One-off, brittle integrations increase cost and post-close risk.

- Customer concentration: WFM contracts can be big. Buyers will price in the risk of a single loss.

General M&A discounts that apply here too

- Messy financials or unclear revenue recognition

- Founder dependency for sales, delivery, or product decisions

- Litigation, IP issues, or security incidents

- Unclear product roadmap and weak documentation

The key point: most discounts are fixable, but they need time and evidence.

7. Valuation Example: A Workforce Management Company (Fictional)

This is a worked example to show how the logic works. The company and the numbers are fictional. The multiples and ranges are based on the dataset patterns and are illustrative - not investment advice and not a formal valuation.

Step 1: The logic

Start with public trading ranges as a sanity check: pure scheduling tools trade lower than full-suite HCM/payroll platforms.

- Use private deal ranges as the closer reference point: scheduling-centric WFM deals cluster lower, suite HRIS/payroll deals cluster higher.

- Pick a defendable base band based on what you actually are (product mix, scale, growth, margins).

- Adjust up for premium drivers you can prove, and adjust down for risks buyers will punish.

Step 2: Apply it to a fictional company

Meet ShiftBridge (fictional): a multi-module WFM SaaS for frontline businesses (retail, logistics, hospitality) with scheduling, time & attendance, basic HR records, and payroll integrations. It is mostly subscription revenue, but still has meaningful implementation work.

Assume:

- Annual revenue: USD 10.0m (fictional)

- EBITDA is not the core metric here (common for growth-stage SaaS), so we anchor on EV/Revenue.

From the dataset logic:

- Pure scheduling public comps imply a lower band (roughly 1.3-1.5x in the example logic).

- HCM/payroll SaaS public comps are higher (roughly 2.2-4.7x in the example logic).

- Private comps show ~2.1-3.3x for frontline scheduling WFM and ~6.1-6.7x for HRIS/payroll suite deals.

- Blending for a suite-leaning WFM company at smaller scale, the example logic anchored a defendable band around 3.5-6.5x.

Now apply three scenarios:

What would justify the premium-leaning case?

Not “AI in the pitch deck.” Buyers would need proof of multiple premium drivers, for example:

- Strong module adoption and expansion inside accounts

- Repeatable onboarding (less services drag)

- Security/compliance readiness that reduces diligence friction

- Clear strategic fit as a suite gap-fill for specific buyers

- Earn-out structure that lets the buyer pay for upside if needed

Step 3: What this means for you

Two WFM companies can both have USD 10m revenue and still be worth very different amounts. Multiples move when buyers believe your revenue is predictable, your product is deeply embedded, and your growth doesn’t require proportional headcount.

The founder-friendly takeaway: your valuation is not just your revenue - it’s the buyer’s confidence in what that revenue becomes over the next 3-5 years.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this as a simple way to locate yourself on the spectrum. Score each factor 0 / 1 / 2:

- 0 = weak or unclear today

- 1 = decent but inconsistent

- 2 = strong and provable

Self-assessment table

How to interpret your score

- High band (mostly 2s): you’re closer to premium outcomes because buyers see a scalable platform with lower risk.

- Middle band (mix of 1s and 2s): you can sell well, but the multiple will be sensitive to process quality and deal dynamics.

- Low band (many 0s): buyers will still engage, but you’re more likely to see discounted offers unless you fix the biggest risks first.

The point is not to “grade yourself.” It’s to identify which 2-3 changes could move your multiple the most in 6-12 months.

9. Common Mistakes That Could Reduce Valuation

These are avoidable, and they show up constantly in founder-led sale processes.

Rushing the sale

If you go to market before your numbers and story are ready, buyers anchor on uncertainty. In WFM, uncertainty becomes “risk,” and risk becomes a lower multiple.

Hiding problems

Buyers will find issues in due diligence: churn, payroll errors, security gaps, customer disputes, margin leakage. When you hide problems, you don’t just lose value - you lose trust, and trust is often the difference between a premium offer and a retrade.

Weak financial records

This is one of the most fixable valuation killers in 6-12 months:

- Separate subscription vs services revenue clearly

- Track gross margin by revenue type

- Make retention and churn metrics consistent and defensible

No structured, competitive sale process with an advisor

Running a structured process matters because competition drives price. Research often cited in M&A advisory circles suggests structured, advisor-led competitive processes can increase purchase prices meaningfully (commonly referenced around ~25% uplift) - not because advisors “talk buyers up,” but because process design improves leverage and price discovery.

Revealing what price you’re after too early

If you say “we want USD 50m,” you often cap your upside. Buyers may simply come back with USD 50.1m, USD 50.2m - instead of showing what they would actually pay in a competitive process.

Two WFM-specific mistakes that hurt valuation

- Treating implementation as “just delivery”: buyers want proof it is repeatable and scalable.

- Underinvesting in compliance and auditability: if your product touches time/payroll, weak controls are a direct valuation discount.

10. What Workforce Management Founders Can Do in 6-12 Months to Increase Valuation

You don’t need a massive pivot. You need targeted improvements that reduce buyer risk and strengthen the “why this is valuable” story.

Improve the numbers buyers pay for

- Increase subscription mix (even modestly) by packaging services into implementation fees and pushing ongoing value into subscriptions.

- Reduce churn with a focused retention plan: onboarding milestones, usage triggers, renewal playbooks.

- Raise prices where value is clear (compliance, payroll accuracy, overtime reduction), and prove it with case studies.

Make your suite feel real (not theoretical)

- Measure module adoption and expansion. Show how many customers actively use each module.

- Create 2-3 “standard packages” for your core verticals (retail, healthcare, logistics) to reduce bespoke work.

- Build or harden the integrations buyers expect (HRIS, payroll rails, ERP/accounting, identity).

Reduce diligence friction (this can directly protect your multiple)

- Formalize security and privacy posture (policies, testing, incident response plan).

- Improve compliance audit trails (who changed time entries, approvals, payroll adjustments).

- Document implementation processes and reduce founder dependency.

Strengthen your deal narrative with proof

- Build a simple “buyer deck story” around: mission-critical workflow, stickiness, scalability, and why you are a suite gap-fill.

- Gather proof points: retention cohorts, deployment times, expansion rates, case studies.

- If appropriate, be open to an earn-out structure to bridge expectations - but only if KPIs are simple and auditable.

11. How an AI-Native M&A Advisor Helps

Selling a WFM business is not only about finding “a buyer.” It’s about finding the right set of buyers - the ones who will value your product’s role in their suite, trust your numbers, and compete for the deal.

An AI-native M&A advisor helps you get higher valuations through broader buyer reach. AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, synergy fit, and financial capacity. More relevant buyers creates more competition, stronger offers, and more options if one buyer drops out.

It also compresses timelines. With AI-driven buyer matching and outreach, plus faster creation of marketing materials and diligence support, you can often reach initial conversations and offers much faster than in a manual-only process - frequently within weeks rather than quarters.

Finally, you still want expert humans driving the process. The best outcomes come from experienced advisors who know how buyers think, how to position your business, and how to run a competitive process - with AI enhancing speed, coverage, and execution quality. The goal is Wall Street-grade advisory quality without traditional “bulge bracket” costs.

If you’d like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.