What Private Equity Firms Look for in Platform Acquisitions

A deep dive into the 5 interconnected criteria that PE firms look into when making platform acquisitions.

Most founders preparing for a potential PE deal focus on proving what they've built. The PE firm sitting across the table is focused on something different: what they can build on top of it.

A platform acquisition is a PE firm's foundation investment - the company they'll use to consolidate a market through follow-on acquisitions (called "add-ons" or "bolt-ons") over a 3-5 year hold period, with the goal of exiting a significantly larger, more valuable business than the one they bought. When PE evaluates a platform, they're not just buying your company. They're underwriting a multi-year thesis that starts with your business and ends with someone else buying a much bigger one. Every metric they scrutinize, every question they ask, feeds into that forward-looking model.

Understanding this logic changes how you prepare - and what you prioritize.

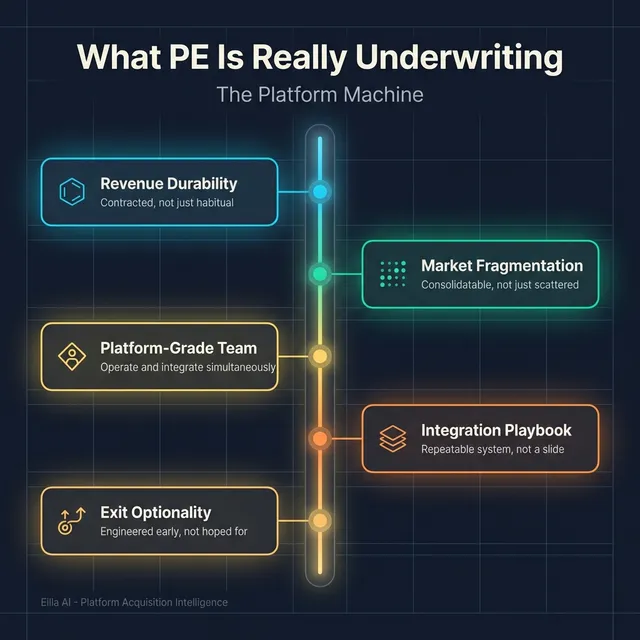

What PE firms evaluate in platform acquisitions comes down to five interconnected criteria: the quality and durability of recurring revenue, the size and structure of the market's fragmentation, the management team's ability to execute a growth-through-acquisition strategy, the credibility of a buy-and-build thesis, and whether the resulting business can attract multiple buyer types at exit in 3-5 years.

How PE Evaluates Recurring Revenue (And Why "Recurring" Alone Isn't Enough)

Recurring revenue is the foundation of many platform theses - but PE's definition of "quality" recurring revenue is far more demanding than most founders expect.

The core question a PE diligence team asks isn't "is this revenue recurring?" It's: how contractually protected, behaviorally sticky, and economically resilient will this revenue be through a downturn - and through the integration disruption that comes with bolt-on acquisitions?

This means PE teams rebuild your revenue base from the ground up during diligence. They'll create a contract-level database linking every customer to their contract terms, renewal dates, pricing clauses, and termination rights. Then they'll stress-test it.

What they actually measure:

Revenue concentration is the first filter. PE firms typically look at your top 1, 5, and 10 customers as a percentage of both revenue and gross profit. When a single customer represents more than 30% of revenue, the business becomes what some in the industry call "too easy to kill" - and that doesn't disqualify you, but it changes the price, deal structure, and diligence intensity significantly. Even at lower concentration levels (10-20%), PE will want to understand the trend: is concentration rising or falling? Did one client spike recently?

Retention metrics get dissected into layers. PE rarely accepts a single churn number. They want logo churn (how many customers leave), gross revenue retention or GRR (how much revenue you keep excluding any expansion), and net revenue retention or NRR (revenue kept including upsells and price increases). Recent industry benchmarks give useful context: for companies in the $5-20M annual recurring revenue range, median GRR sits around 88% and median NRR around 101%, according to 2025 data from firms like Jurassic Capital and Benchmarkit. PE interprets high GRR as your revenue "floor" - baseline durability - and high NRR as your "ceiling," though they'll dig into whether that NRR is driven by genuine expansion or price increases that might not be repeatable.

Contract quality matters as much as contract length. Auto-renewal clauses, termination-for-convenience rights, short notice periods, and pricing escalation mechanisms all signal how durable your revenue really is. A three-year contract with a 30-day termination-for-convenience clause is, in practice, a 30-day contract.

Pricing power is evaluated separately because it's both a value creation lever and a risk indicator. Commercial diligence providers typically examine your competitive price positioning, your history of price increases, discount dispersion across your sales team, and customer response to past pricing changes. McKinsey has argued that pricing transformations can drive roughly 3-7% margin expansion within a year - which is why PE sees pricing discipline as a direct lever on exit value, not just a revenue optimization exercise.

The bottom line: PE is underwriting whether your recurring revenue can survive a hold period that now averages over five years, absorb the disruption of multiple bolt-on integrations, and still grow. Revenue that looks "recurring" in your P&L but depends on a few relationships, short contracts, or unsustainable pricing won't survive this scrutiny.

Why Market Fragmentation Is the Growth Engine PE Needs

A fragmented market isn't interesting to PE simply because there are many small players. It's interesting when fragmentation creates a repeatable, executable path to scale that generates real economic value through consolidation, not just revenue aggregation.

PE firms are looking for markets where they can realistically execute multiple acquisitions using a consistent playbook. Bain defines a credible buy-and-build strategy as one involving at least four add-on acquisitions - meaning the target universe needs to be deep enough to sustain that pace across a full hold period.

What makes fragmentation "investable":

The valuation gap between small and scaled businesses must be real and demonstrable. PE's buy-and-build economics depend on "multiple arbitrage" - acquiring smaller companies at lower valuation multiples and selling the combined, scaled platform at a higher multiple. If a fragmented market doesn't exhibit a meaningful gap between subscale and scaled asset valuations, the math doesn't work regardless of how many targets exist.

Synergy mechanics need to be concrete and repeatable, not speculative. PE diligence teams look for clear cost or revenue synergies that activate with each add-on: centralized back-office functions, procurement leverage, standardized pricing, cross-selling across a combined customer base. Industry advisors consistently warn against assuming revenue synergies "for granted" - PE will want evidence these synergies are deliverable, not just plausible on a slide.

Integration must be feasible at the pace PE requires. A market might be fragmented with willing sellers, but if each acquisition takes 18 months to integrate and destroys customer relationships in the process, the thesis breaks down. Research from INSEAD highlights that buy-and-build success depends heavily on having a repeatable integration model - what some call an "integration SWAT team" approach - with clear accountability and execution within the first 100 days of each deal.

One dimension founders often overlook is regulatory risk. Competition authorities in the US, UK, and EU have increasingly scrutinized serial acquisitions by PE-backed platforms, even when individual deals are small. A series of seemingly minor bolt-ons can trigger antitrust review if the cumulative effect reduces local competition or increases pricing power. PE firms now factor "regulatory white space" into their fragmentation analysis from day one. Recent enforcement actions, including cases involving PE-backed healthcare roll-ups, have made this more than theoretical.

A quick self-test: If your market has dozens of potential acquisition targets in the right size range, those targets have identifiable succession or scale challenges that make them willing sellers, consolidation creates measurable synergies beyond just adding revenue, and the regulatory environment is manageable - you're sitting in the kind of market PE actively hunts for.

What PE Really Means by "Strong Management Team"

When PE says they want a "strong management team," they're not paying a compliment. They're underwriting whether your leadership can execute a compressed-timeline transformation while simultaneously running a repeatable acquisition machine.

A platform CEO, in PE's evaluation, needs to be more than a good operator. PE-backed boards are lean (typically 5-7 members), data-driven, and unusually engaged. They align around a small set of measurable objectives and probe performance variance with little tolerance for narrative explanations. The CEO must thrive in this environment - delivering execution intensity, decisiveness, and comfort with metrics-driven accountability that feels different from running a founder-led business.

The CFO role is often treated as "non-negotiable" in platform deals. PE frequently upgrades or brings in a new CFO early in the hold period because the finance function needs to do far more than produce financial statements. A platform CFO must translate the investment thesis into cash discipline, KPI instrumentation, lender reporting, and - critically - the financial architecture for serial acquisitions. PE firms explicitly match CFO profiles to their value-creation plan, and that plan is thesis-specific: a buy-and-build CFO looks very different from a turnaround CFO.

Beyond the C-suite, PE evaluates whether the broader leadership team can scale the company into a larger, more institutional business. Founder-led companies often have underbuilt capabilities in revenue operations, pricing, talent management, and systems - functions that become critical when you're integrating multiple acquisitions per year. Leadership assessments during diligence increasingly focus on complementary team strengths, agility, and change management capability, because PE has learned that too much uniformity at the top inhibits the adaptability buy-and-build demands.

The platform vs. bolt-on distinction matters here. In a platform deal, the management team is expected to build the institution. In a bolt-on acquisition, management is being absorbed into an existing institution. This difference shapes everything from governance to incentives: platform founders typically negotiate rollover equity and board participation; bolt-on founders more often face earn-outs (roughly 70% of bolt-on deals use them, according to recent practitioner data) and are less likely to receive equity in the parent company. Understanding which role PE sees you in changes how you should prepare and negotiate.

How PE Underwrites a Buy-and-Build Thesis Before Writing the Check

The buy-and-build thesis is where recurring revenue, market fragmentation, and management capability converge into a single, executable plan. PE doesn't just identify fragmented markets and hope for the best - they underwrite the entire consolidation arc before acquiring the platform.

Pipeline visibility is an important variable. PE firms increasingly treat acquisition pipeline as an operating capability, not a networking exercise. Before buying a platform, they typically require a quantified target universe - sometimes called a "Total Addressable Asset Pool" - that maps every plausible acquisition target against filters like size, geography, service mix, margins, and customer profile.

But having a list isn't enough. PE evaluates whether the platform has, or can build, a proprietary origination engine. This matters because auction-sourced bolt-ons are more expensive and harder to win. Industry data shows that PE firms historically closed 30-40% of sourced deals, but that average has recently dropped to around 25%.

PE diligence on the buy-and-build thesis also includes what you might think of as an integration stress test. They want to see evidence that acquisitions can be integrated without breaking customer experience or losing key staff. Firms that have successfully completed previous acquisitions have a significant advantage here - not because the past guarantees the future, but because it proves the team has learned how to manage the disruption.

The financing architecture is another underwriting dimension. As a platform scales through add-ons, its debt capacity typically expands - the combined entity can carry more leverage than the sum of its parts. PE models this progression carefully, including incremental bolt-on credit facilities and working capital requirements, because buy-and-build strategies consume cash. The economics need to work deal-by-deal, not just in aggregate at exit.

Why PE Models the Exit Before They Model the Entry

Perhaps the most misunderstood aspect of platform evaluation is that PE firms underwrite the exit before they close the acquisition. They're not buying your company and then figuring out who to sell it to - they're modeling the buyer universe, the required scale, and the value creation milestones needed to get there from the very first IC memo.

This "underwrite backward" approach is increasingly important because holding periods have stretched significantly. Recent data paints a consistent picture: the median PE holding period has exceeded five years, with some surveys showing 63% of funds reporting average holds above five years and 78% of firms holding assets beyond their typical horizon. This doesn't mean the 3-5 year plan is dead - it means PE wants the company to be sellable before they need to sell, creating optionality to move when market windows open.

The buyer universe PE maps at entry typically includes four routes:

A trade sale to a strategic acquirer - usually the upside case, because strategics often pay a premium for synergies (procurement scale, cross-sell opportunity, geographic expansion, or capability acquisition). PE teams name specific strategic buyers at the IC stage and map the synergy logic for each.

A sponsor-to-sponsor secondary buyout - often the base case, because it depends on standalone fundamentals rather than synergy assumptions. The key question PE asks: "What does the next sponsor's investment committee need to believe?" This means the company needs to reach a scale that fits a larger fund's check size and still have a credible next chapter of value creation.

An IPO - increasingly viable again after PE-backed IPO exit value nearly doubled to over $320 billion in 2025. But IPO optionality requires building governance structures, audit committee independence, and equity story durability well in advance. PE firms that want this option start preparing 12-24 months before a potential listing.

Continuation vehicles and GP-led secondaries - now representing a meaningful share of exits (roughly 14-20% of PE sales in 2025, depending on the source). These aren't "failure exits" - they're structured liquidity solutions that let sponsors hold performing assets longer while returning capital to limited partners.

The practical implication for founders: if you're positioning your company as a PE platform candidate, you should be thinking about who the eventual buyers of the platform are, not just who's buying you today. A PE firm that can see three or four credible exit routes - each requiring different but achievable milestones - will underwrite more aggressively than one that sees only a single path.

What value creation milestones PE typically expects across the hold period:

In the first 100 days, PE wants early wins and an established operating rhythm. McKinsey's research points to focused execution on the fastest value levers - working capital optimization, pricing and commercial excellence, and cost resets - with weekly performance reviews and a live data pipeline from day one.

By the end of year one, measurable EBITDA and cash flow improvement should be visible. Benchmarks vary by situation, but accelerated-performance transformations can target EBITDA improvement of 500+ basis points within the first year, with 70-80% of total value creation impact captured within two years.

Through years one to three, the platform should be scaling into a larger buyer universe through repeatable KPI reporting, institutional-quality finance and governance, sharpened strategic positioning, and - if the thesis includes buy-and-build - demonstrated integration capability.

By years three to five, the company should be "process-ready" for any of the mapped exit routes, with a refined equity story, clean data rooms, and governance structures that match the requirements of each potential buyer type.

Platform Acquisition Readiness: A Self-Assessment Framework

If you're a founder exploring whether your company could be a PE platform candidate, here's a framework for evaluating your own positioning across the five criteria PE weights most heavily. Each signal below reflects what diligence teams actually test.

Recurring Revenue Durability

- No single customer represents more than 15-20% of revenue, and concentration is trending down rather than up

- Gross revenue retention exceeds 85%, with clear visibility into what drives churn by customer segment

- Contracts include auto-renewal clauses and meaningful notice periods - not termination-for-convenience language that makes three-year contracts functionally month-to-month

- You've executed at least one round of price increases without triggering outsized churn, demonstrating real pricing power

Market Fragmentation and Consolidation Potential

- You can identify at least 15-20 realistic acquisition targets that fit reasonable size, geography, and service filters

- Many of those targets face succession challenges, scale limitations, or capability gaps that make them natural sellers

- Combining your business with those targets would create measurable synergies (cost savings, cross-sell revenue, procurement leverage) - not just a bigger revenue number

- The regulatory environment allows serial acquisitions without predictable antitrust friction

Management Team Readiness

- Your leadership team includes (or can quickly add) a CFO capable of institutional-quality reporting, cash management, and M&A financial architecture

- Key functions beyond the C-suite are staffed at a level that could absorb the operational complexity of integrating 2-4 acquisitions per year

- The founding team is willing to operate under a metrics-driven, PE-style board with compressed decision cycles and tight accountability

- You have a realistic view of which roles need upgrading and a willingness to make those changes in the first 100 days

Buy-and-Build Thesis Credibility

- You can articulate a specific, repeatable playbook for how each add-on creates value - not just "we'll acquire competitors"

- Your industry relationships give you proprietary access to potential targets, reducing dependence on competitive auction processes

- You have some evidence of integration capability - whether from past acquisitions, partnerships, or structured M&A preparation

- The financing math works deal-by-deal, not just in an optimistic aggregate model

Exit Optionality

- At least two exit routes are credible: you can name specific strategic buyers with clear synergy logic, and your projected scale fits the check-size range of larger PE funds

- Your business can reach institutional-quality governance and reporting within 12-18 months

- The value creation plan doesn't depend on a single lever (e.g., only revenue growth or only margin expansion) but includes multiple measurable drivers

- You're building exit readiness now, not planning to start in year four

Key Takeaways

- PE firms evaluate platform acquisitions backward from the exit - they model who buys the company from them in 3-5 years before they model the entry price.

- Recurring revenue quality is assessed through concentration risk, contract durability, cohort-based retention (GRR and NRR), and demonstrated pricing power - not just whether revenue repeats.

- Market fragmentation is attractive when it supports multiple add-on acquisitions with repeatable synergies, real valuation arbitrage between subscale and scaled assets, and manageable regulatory risk.

- Management teams in platform deals are expected to operate under PE-style governance from day one - including metrics-driven boards, institutional-quality finance functions, and the capability to integrate acquisitions repeatedly.

- Buy-and-build credibility depends on pipeline visibility, proprietary deal sourcing, proven integration playbooks, and deal-by-deal financing economics.

- Exit optionality requires at least two feasible routes (strategic sale, sponsor-to-sponsor, IPO, or continuation vehicle) and governance structures that preserve flexibility across all of them.

- Holding periods now routinely exceed five years, making early exit readiness a strategic advantage rather than premature planning.

- Founders who understand PE's evaluation framework can start positioning their company 12-24 months before a process begins - which is exactly the kind of preparation that changes outcomes.

FAQ

What is a platform acquisition in private equity? A platform acquisition is a PE firm's initial investment in a company that will serve as the foundation for a buy-and-build strategy. The PE firm uses the platform to acquire smaller companies (add-ons or bolt-ons) in the same or adjacent markets, consolidating them into a larger, more valuable business over a 3-5 year hold period before exiting.

How much recurring revenue do PE firms expect from a platform company? There's no universal threshold, but PE firms strongly prefer businesses where the majority of revenue is contractually recurring rather than merely "repeat." More important than the percentage is the quality: gross revenue retention above 85%, low customer concentration (ideally no single customer exceeding 15-20% of revenue), and contract structures with auto-renewal clauses and meaningful termination protections.

Why do private equity firms prefer fragmented markets for platform strategies? Fragmented markets create the conditions for multiple arbitrage - acquiring smaller companies at lower valuation multiples and exiting a larger, combined business at a higher multiple. They also offer enough acquisition targets to sustain a multi-deal strategy. Add-on acquisitions now represent over 76% of PE-backed buyouts, making fragmentation a structural requirement for the dominant PE value creation model.

How do PE firms evaluate management teams differently for platform vs. bolt-on acquisitions? Platform management is expected to build and run an institutional-grade business capable of serial acquisitions. This means PE-ready governance, a thesis-matched CFO, and integration capability. Bolt-on management is typically being absorbed into the platform's existing structure - with earn-outs rather than equity participation, less governance involvement, and a primary focus on retention of key people and customer relationships during integration.

When should founders start preparing for a PE platform acquisition? Ideally 12-24 months before entering a formal process. PE diligence is extensive, and the companies that perform best are those that have already addressed revenue concentration, strengthened contract structures, built institutional-quality financial reporting, and developed a clear view of their market's consolidation potential before a PE firm ever opens a data room.

What exit routes do PE firms plan for at the time of platform acquisition? PE firms typically map four potential exit routes at entry: a strategic trade sale (often the upside case due to synergy premiums), a sponsor-to-sponsor secondary buyout (often the base case), an IPO (which requires early governance preparation), and continuation vehicles or GP-led secondaries (increasingly common, representing 14-20% of PE exits in 2025). Strong exit optionality means at least two of these routes are genuinely feasible.

If you're a founder considering an exit and want to understand how PE firms would evaluate your business as a platform candidate, it's worth having that conversation early. Our M&A advisors work with European founders across the range where these dynamics matter most - and a 30-minute call can clarify where you stand and what's worth focusing on before a process begins. [Book a conversation with our team.]

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.