Why American Private Equity Is Buying Up Europe's Best Small Businesses - And What Founders Need to Know

What drives the surge of U.S. private equity buying and consolidating Europe’s SMBs.

Every week, somewhere in Europe, a founder who built a 30-person services company over 15 years gets an email from a name they don't recognize. The subject line is polite. The language is warm. And behind it sits a U.S. private equity fund with a very specific plan: buy the company, bolt on four or five similar ones across the continent, and sell the combined entity in five years for three times what they paid.

This isn't a future trend. It's the dominant pattern in European M&A right now.

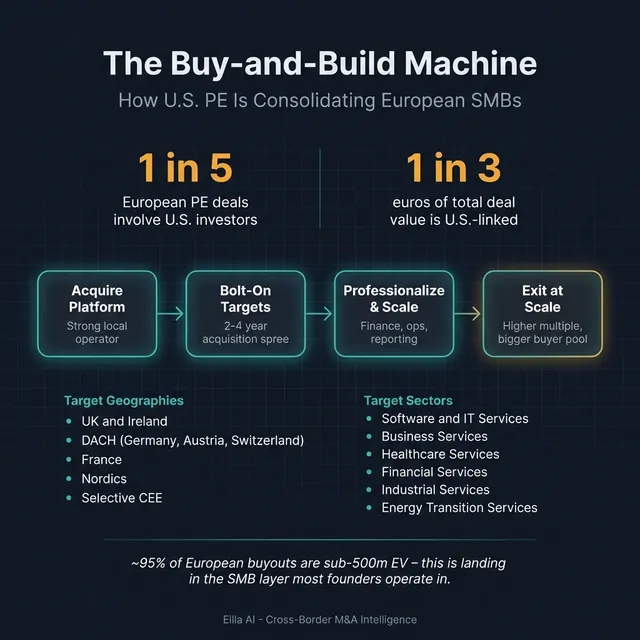

U.S. private equity firms now participate in roughly 1 in 5 European PE deals by count - and about 1 in 3 by value. In H1 2025, U.S. investors were involved in 19% of all European PE transactions, representing 34.3% of total deal value. In Q3 2025, U.S.-linked cross-border deal value in Europe surged by over 950% compared to the previous quarter. The acceleration is real, and it's disproportionately targeting small and mid-sized businesses - the companies that make up around 95% of European buyouts by deal count.

If you're a European founder running a profitable company in the 2-50 million euro revenue range, understanding this wave isn't optional anymore. It directly affects your valuation, your negotiating position, and the kind of deal you'll end up in.

What's Driving U.S. Private Equity Into European SMB Markets

The short answer is economics, structure, and timing all pointing in the same direction at once.

Start with price. European companies are cheaper than their American counterparts. The gap shows up across public and private markets - average EV/EBITDA multiples in 2024 were around 12.2x in Europe versus 12.7x in the U.S., and the gap widens significantly in public equities (STOXX 600 trading at roughly 11x EBITDA versus the S&P 500 at around 16x). For U.S. funds deploying dollars, a strong greenback makes European assets even more affordable. A business that might trade at 8-10x EBITDA in Europe could look like a bargain compared to 10-14x for a similar profile in the U.S. mid-market.

But valuation alone doesn't explain why the strategy is consolidation specifically. That comes from Europe's market structure.

The EU has over 32 million enterprises. Roughly 99% of them have fewer than 50 employees. This extreme fragmentation is the raw material for what PE calls "buy-and-build" - acquiring a platform company, then bolting on smaller competitors to create scale. In 2023 alone, sponsors executed over 750 buy-and-build acquisitions in Europe, and in the Nordics, add-on deals now represent over half of all buyout transactions. The playbook is well-established and increasingly dominant.

Then there's the seller pipeline. Within the next decade, nearly 40% of European family-owned businesses anticipate a leadership or ownership transition, yet only about 30% have formal succession plans. That gap between "I need to exit" and "I have a plan" creates a steady flow of motivated sellers - exactly the conditions that make a repeatable acquisition strategy viable.

And finally, the financing environment shifted. After a brutal 2023 - Western European buyout deal value dropped 69% that year - the combination of ECB rate cuts, expanding private credit options, and over $2 trillion in undeployed PE capital created the conditions for a sharp rebound. Average European PE deal values climbed from around 72 million euros in 2023 to 86 million euros in 2024, and 2025 has only accelerated.

Where This Is Happening: The Sectors and Regions U.S. Funds Are Targeting

Not all of Europe is equally attractive for consolidation, and the geographic and sector concentration tells you a lot about where the real activity sits.

Geographically, the UK remains the single largest market - U.S.-based investors were involved in over 56 billion pounds of UK PE deal value across 472 transactions in 2024, representing just over half of UK PE activity. Germany's Mittelstand - its dense ecosystem of founder-owned industrial and services businesses - has become the second most active buyout region in Europe, overtaking France for the first time in a decade. The Nordics are gaining momentum fast, with Finland, Denmark, and Norway recording the largest gains in deal count share in H1 2025. And Central & Eastern Europe is on the radar for funds willing to accept more complexity in exchange for lower entry prices.

By sector, the pattern is even clearer:

- Software and technology tops every survey and dataset. Roland Berger's 2026 outlook found 69% of respondents expect it to see the highest transaction count. The logic is straightforward: fragmented niche vendors can be centralized onto shared infrastructure, and scale increases credibility with enterprise buyers.

- Business services and logistics are close behind (68% in the same survey). These are classic roll-up arenas - fragmented provider bases, recurring contract revenue, and real procurement savings from consolidation.

- Healthcare and life sciences deal value is gaining share, particularly in healthcare IT and services around providers rather than labor-heavy clinical operations.

- Financial services - especially insurance broking, wealth management, and fund administration - grew in both deal count and value versus five-year averages in H1 2025. Regulatory and compliance costs create natural advantages for larger groups.

- Industrials and engineering services, especially testing, inspection, and certification businesses, remain attractive. Europe's commitments to defense spending and energy transition are creating new demand tailwinds.

The common thread across all of these is fragmentation plus a credible path to integration synergies. U.S. funds aren't buying random small companies - they're targeting sectors where combining five 5-million-euro businesses creates something worth materially more than the sum of the parts.

What Actually Changes When the Buyer Is American: The Deal Experience for European Founders

Here's where the conversation gets practical, because the experience of selling to a U.S. private equity buyer differs from selling to a European one in ways that many founders don't anticipate until they're deep in a process.

The purchase price mechanics feel different. In the U.S., 94% of deals use purchase price adjustment mechanisms - meaning the final price gets calculated and potentially adjusted after closing based on working capital, debt, and cash at close. In Europe, that figure is 44%. European practice has increasingly shifted toward "locked box" pricing, where the price is fixed at signing and the buyer assumes economic risk from an agreed date. Founders used to the cleaner European approach often find U.S.-style closing accounts more administratively burdensome - more negotiation on working capital targets, more post-close reconciliation, and more potential for disputes.

Earn-outs are structured differently. Earn-outs appear in roughly similar percentages of deals (around 21-23% in both markets), but U.S. deals lean heavily on revenue-based metrics (61% of earn-outs) while European deals more often use EBITDA or profit-based measures (36%). This isn't just a technical difference - it shapes what the founder optimizes for in the 1-3 years post-close and where disputes tend to arise.

FDI screening adds timeline risk. EU member states handled over 3,100 FDI screening cases in 2024, up from around 1,800 in 2023. By end of 2024, 24 EU member states had FDI screening legislation in place, and the U.S. is the top foreign investor by volume (around 30% of acquisitions flagged). Selling to a U.S. fund in a regulated sector can add weeks or months to the deal calendar, with the founder stuck operating under signing-to-closing covenants in the interim.

The post-close role often shifts toward "platform CEO." In PE deals across Europe, management continued in their roles in 71% of transactions. But when the buyer is running a buy-and-build strategy, the founder isn't just running their business anymore. They're expected to integrate acquisitions, professionalize reporting faster, and potentially delegate day-to-day operations to become more M&A-facing. U.S. sponsors tend to arrive with a more systematized consolidation playbook, which can be both an accelerant and a source of friction.

The "Second Bite" Question: Is Rolling Equity Actually Worth It?

One of the most consequential decisions a founder makes in a PE deal is how much equity to roll over. In Europe, rollover percentages of 40-50% are increasingly common, and the share of deals including rollovers has risen from 46% in 2020 to 57% in 2023 across mid-market PE transactions.

The pitch is compelling: sell a majority of your equity now, retain a meaningful stake, and participate in the upside when the combined, larger entity exits at a higher multiple. In buy-and-build scenarios, this "second bite" can sometimes exceed the proceeds from the initial sale.

But the trade-offs are real. Management incentive plans in European PE deals most often involve real equity from day one, but leaver provisions have tightened.. That means if you leave (or are pushed out) before the exit, the terms governing what happens to your equity matter enormously. Founders who negotiate the price hard but treat the shareholders' agreement as boilerplate often regret it.

The evidence on operating outcomes is cautiously positive. A rigorous UK study (The Productivity Institute, 2024) found that PE-backed companies saw statistically significant productivity improvements - over 4% for total factor productivity, up to 5% for labor productivity - along with increases in employment and capital expenditure. These effects persisted even after PE exit. But the same study flags the structural concern: buyouts use considerable debt, and financial fragility is a real risk.

For founders considering a roll, the negotiation that matters most isn't the headline valuation. It's the governance, decision rights, vesting terms, leaver definitions, and what happens when the sponsor wants to do the sixth bolt-on acquisition and you disagree.

The Counterargument: Isn't This Just Financial Engineering?

It's worth addressing the skepticism head-on, because it's partly justified.

Not every buy-and-build creates real value. Some roll-ups are primarily exercises in multiple arbitrage - buying at 5-6x and selling a combined entity at 8-10x, without materially improving the underlying businesses. When financing is cheap and exits are plentiful, this can work. When conditions tighten, under-integrated portfolios can unravel.

The difference between a value-creating consolidation and a financial engineering exercise usually comes down to integration. Are the combined businesses sharing infrastructure, cross-selling, standardizing operations? Or are they just stapled together under a single holding company? Founders who sell into a roll-up should be asking pointed questions about the integration thesis - not just the financial model.

That said, the structural case for consolidation in European SMB markets is genuinely strong. Many of these fragmented sectors have inefficiencies that scale can address: duplicated back-office costs, inability to serve enterprise clients, underinvestment in technology. A well-executed buy-and-build doesn't just inflate the exit multiple - it builds a better business. The productivity data supports this.

The question isn't whether consolidation will continue. It will. The question is whether founders selling into it are doing so with enough information to negotiate well.

How to Evaluate a U.S. PE Approach: A Founder's Framework

If a U.S. private equity fund or one of their portfolio companies contacts you, here are the questions that separate an informed response from a reactive one:

- Are you the platform or the bolt-on? Platform acquisitions typically command higher multiples (often 7-10x EBITDA) because the buyer needs your management, infrastructure, and market position as the foundation for a roll-up. Bolt-on acquisitions are priced lower (often 4-7x) because they're being plugged into an existing platform. Knowing which role you'd play fundamentally changes your leverage.

- What's the integration thesis? Ask specifically how acquired companies will be combined - shared back office, cross-sell, technology consolidation, geographic expansion. If the answer is vague or purely financial ("we'll professionalize and grow"), that's a signal to probe deeper.

- What does the post-close reporting cadence look like? U.S. PE-backed platforms typically expect monthly board packs, weekly KPI dashboards, and quarterly strategic reviews. If you're running a 20-person company with a part-time bookkeeper, the operational step-change is real.

- What are the leaver provisions? If you're rolling equity, understand exactly what happens if you leave voluntarily, are terminated without cause, or are terminated for cause. The difference can be between keeping your rolled equity at fair market value or forfeiting it entirely.

- Who are the other bolt-on targets? Understanding the fund's acquisition pipeline tells you whether they have a realistic plan or just a thesis. It also tells you how much of your time post-close will be spent on integration versus running your business.

- What's the target hold period and exit route? Most PE funds target 4-6 year holds, but median holding periods in Europe have stretched to 6.1 years (up from 5.2 in 2021). Understanding the exit plan - trade sale, larger sponsor, IPO, continuation vehicle - helps you assess whether the "second bite" opportunity is realistic.

What This Means If You're Considering an Exit

If you're running a European SMB in a fragmented sector - services, tech, healthcare, financial services, industrials - the probability that a U.S. PE fund (or one of their European platform companies) will approach you is higher than it's ever been. That approach might come directly from a fund, through a local intermediary, or as a bolt-on inquiry from a portfolio company you've never heard of.

The founders who navigate this well tend to share a few characteristics: they understand the buy-and-build model before they're in a process, they know what their business looks like as a platform versus a bolt-on (the difference in valuation can be 2-3x), and they negotiate the post-close terms with the same rigor as the price.

The founders who don't navigate it well tend to get surprised - by the disclosure burden, the timeline, the earn-out structure, or the reality of what "partnering with PE" actually means in practice.

We work with founders preparing for exactly these kinds of conversations. If you're thinking about your options and want to understand how your business fits into the current landscape - whether as a platform, an acquisition target, or something you want to keep building independently - it's worth having that conversation early. Book a confidential discussion with one of our M&A advisors.

Key Takeaways

- U.S. private equity now participates in roughly 1 in 5 European PE deals and about 1 in 3 by value, with H1 2025 showing 19% deal count participation and 34.3% of deal value.

- Around 95% of European buyouts by count are small-cap or mid-market (under 500 million euros enterprise value), making SMBs the primary target for consolidation strategies.

- The core drivers are a persistent valuation gap (European assets trade cheaper than U.S. equivalents), extreme market fragmentation (99% of EU enterprises have fewer than 50 employees), and a succession wave (40% of family businesses facing transition within a decade).

- The most targeted sectors are software/technology, business services, healthcare services, financial services, and industrials - all characterized by fragmentation and credible integration synergies.

- The UK, Germany (DACH), France, and the Nordics are the primary geographic targets.

- Deal structures differ materially between U.S. and European buyers: purchase price adjustments (94% in U.S. vs 44% in Europe), heavier disclosure expectations, and revenue-based earn-outs are all more common with U.S. acquirers.

- Founders selling into buy-and-build strategies should negotiate post-close governance, leaver terms, and decision rights as carefully as the headline price - especially given tightening leaver provisions.

- The productivity evidence is cautiously positive (4-5% gains in UK studies), but leverage risk is real, and not all roll-ups create genuine operational value.

Frequently Asked Questions

Why are U.S. private equity firms buying European small businesses? European SMBs trade at lower valuation multiples than comparable U.S. companies, the market is extremely fragmented (over 32 million enterprises, 99% with fewer than 50 employees), and a generational succession wave is creating motivated sellers. These conditions make buy-and-build consolidation strategies particularly attractive for U.S. funds with deployable capital.

What sectors are most targeted by U.S. PE in Europe? Software and technology, business services and logistics, healthcare IT and services, financial services (especially insurance broking and wealth management), and industrials including testing and inspection. All share high fragmentation and realistic paths to integration synergies that justify the consolidation model.

How does selling to a U.S. PE buyer differ from selling to a European buyer? The biggest practical differences are in purchase price mechanics (U.S. buyers use post-close adjustments in 94% of deals versus 44% in Europe), disclosure expectations (heavier documentation burden), earn-out structures (U.S. favors revenue-based metrics), and potential FDI screening delays that can add weeks or months to the timeline.

What is a buy-and-build strategy in private equity? A buy-and-build (or roll-up) strategy involves acquiring a "platform" company and then making multiple smaller bolt-on acquisitions to consolidate a fragmented market. The goal is to create scale, improve operations, and exit the combined entity at a higher valuation multiple than the individual acquisitions cost. In Europe, add-on acquisitions represent over half of all buyout transactions in some regions.

Should founders roll equity when selling to private equity? Rollover equity (retaining a stake in the combined entity) offers potential upside if the business grows and exits at a higher multiple. But founders should negotiate leaver provisions, governance rights, and vesting terms carefully - in 2024, 78% of PE incentive schemes applied leaver provisions to both strip and sweet equity, meaning the terms of departure matter enormously.

How long does a U.S. PE acquisition of a European business typically take? Timelines vary, but expect 4-9 months from initial discussions to closing. FDI screening requirements (active in 24 EU member states as of 2024, with over 3,100 cases processed) can add additional time when the buyer is a non-EU entity. Cross-border regulatory complexity is one of the most underestimated timeline risks for founders in these transactions.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.