The Complete Valuation Playbook for Architecture Businesses

A practical breakdown of how architecture businesses are valued and what drives high multiples.

Architecture businesses are being valued in a market where buyers are selective, but still active. Strategic acquirers want specialist design capability, access to resilient end markets, and teams that can help them win larger, more complex built environment projects. Private equity buyers are also interested, but they are careful about project volatility, founder dependence, and margin quality.

This guide is built for founders and CEOs of privately held architecture businesses who may sell in the next 1-12 months. It will show what architecture and related built environment businesses actually sell for, explain what drives higher or lower multiples, and give you a practical self-assessment and 6-12 month action plan.

The main point: two architecture firms with the same revenue can be worth very different amounts. The difference usually comes down to quality of revenue, margins, management depth, end-market exposure, and how risky the business feels to a buyer.

1. What Makes Architecture Unique

Architecture businesses are professional services firms, but they are not generic consultancies. Buyers value them based on a mix of creative reputation, technical delivery, client relationships, project pipeline, sector expertise, and the ability to turn skilled labor into healthy profit.

Most architecture firms fall into a few broad types:

The biggest valuation question is whether buyers see your firm as an expert advisory business or a labor-heavy project delivery business. Advisory-led firms with strong margins, recurring client relationships, and specialist expertise are usually more attractive than firms that look like small contractors with design capability attached.

Architecture also has risks that buyers will always check. These include client concentration, founder dependence, backlog quality, project delays, fee pressure, claims or professional liability exposure, and whether your profit depends on a few senior people being fully billable all year.

A strong architecture business has more than beautiful work. It has repeatable delivery, pricing discipline, good utilization, clean financials, and a leadership team that can keep clients and staff after a sale.

2. What Buyers Look For in an Architecture Business

Buyers start with the obvious: revenue scale, growth, profitability, backlog, customer base, and cash flow. But in architecture, the same numbers can mean different things depending on how they are produced.

A firm growing 20% because it won several low-margin projects may not get a premium. A firm growing 10% with repeat clients, strong fee discipline, and stable margins may be more valuable. Buyers care about whether growth is controlled and profitable, not just whether the top line is bigger.

They also look closely at the type of work. Healthcare, data centers, infrastructure, life sciences, education, public sector frameworks, logistics, and mission-critical facilities can be more attractive than purely discretionary residential or one-off private development work. Buyers often prefer markets where clients must keep spending even when the economy slows.

The main things buyers usually want to see are:

How private equity buyers think

Private equity buyers think in terms of what they can pay today and what the business could be worth in 3-7 years. They ask: "If we buy this firm now, can we grow it, improve margins, reduce risk, and sell it later to a larger buyer?"

They care about the entry multiple and the exit multiple. The entry multiple is what they pay for your business. The exit multiple is what they hope a future buyer will pay them. If your business is small, founder-led, and project-by-project, they may worry that the exit multiple will be limited.

They also think about who the next buyer could be. That could be a global engineering consultancy, a larger architecture group, a construction services platform, another private equity fund, or a strategic buyer looking for a specialist capability.

The levers they will look for include pricing improvement, better utilization, lower overhead, cross-selling into larger clients, expanding into adjacent geographies, and acquiring smaller firms. They will pay more if your business already has the systems and management team to support those moves.

3. Deep Dive: Advisory-Led Design Firm or Project Delivery Business?

One of the most important valuation questions in architecture is simple: are you mainly selling high-value expertise, or are you mainly managing labor and project execution risk?

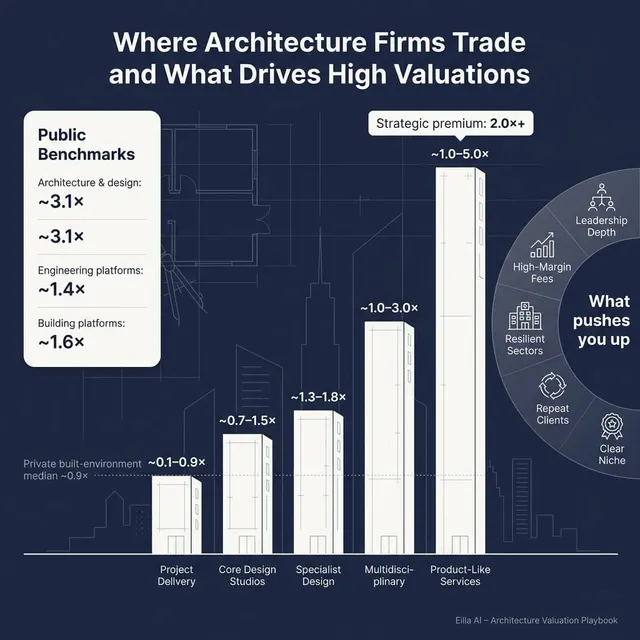

This matters because the source data shows a clear pattern. Architecture, engineering, and building design consultancies tend to trade at higher EBITDA multiples than construction and project delivery services. In the precedent transaction data, architectural, engineering, and building design consultancies showed an average EV/Revenue of about 1.3x and an average EV/EBITDA of about 10.0x. Construction and project delivery services showed a much lower average EV/Revenue of about 0.4x and average EV/EBITDA of about 5.4x.

That gap is not random. Buyers usually pay more for intellectual capital than for execution-heavy work. A firm that earns fees from specialist design, planning, advisory, and technical expertise is easier to understand as a professional services asset. A firm with large pass-through costs, subcontractor exposure, procurement risk, and on-site delivery risk starts to look more like a contractor.

Gross margin is one of the clearest signals. In the data, higher-margin consulting-style businesses showed gross margins that were often far above execution-heavy contractors. That tells buyers the revenue is driven by expertise rather than materials, subcontractors, or pass-through work.

This does not mean design-build or project delivery work is bad. It can be valuable if margins are strong, risk is controlled, and the buyer wants that capability. But if you want buyers to value you like a premium architecture consultancy, your financial reporting should clearly separate advisory fees from pass-through costs and lower-margin delivery revenue.

If your business looks more like the left column today, there are practical ways to move toward the right. Tighten project selection, price more carefully, reduce low-margin pass-through work, track project-level profit, and make your specialist expertise clearer in your pitch. Buyers need to see the economic engine, not just the portfolio.

4. What Architecture Businesses Sell For - and What Public Markets Show

Valuation data for architecture and built environment businesses is noisy. Public market multiples include very large global consultancies, micro-cap outliers, construction groups, design firms, and platform-style companies. Private deal data includes both pure consultancies and execution-heavy construction services firms.

So the right answer is not "architecture firms sell for one multiple." The better answer is: architecture firms tend to sell across a range, and where you land depends heavily on margin quality, scale, growth, specialization, leadership depth, and risk profile.

4.1 Private Market Deals - Similar Acquisitions

The private transaction data shows that built environment businesses generally sold around a median EV/Revenue of 0.9x and median EV/EBITDA of 6.6x overall. But architecture and building design consultancies performed better than construction and project delivery services.

For architectural, engineering, and building design consultancies, the private transaction average was about 1.3x revenue, with an EBITDA multiple around 10.0x. For construction and project delivery services, the average was only about 0.4x revenue, with EBITDA multiples around 5.4x. That difference is important for architecture founders: the more your business looks like a high-margin advisory and design consultancy, the stronger the valuation case.

These ranges are illustrative. A small founder-led studio with USD 5-10m of revenue should not assume it deserves the same multiple as a large, scaled, multidisciplinary consultancy. But it also should not accept a contractor-style valuation if most revenue is high-margin design and advisory work.

The private data also shows that leadership retention can matter. In several stronger deals, founders or executives stayed with the business, rolled equity, or led the combined operation after closing. For people-driven architecture firms, this reduces buyer anxiety and can support better pricing.

4.2 Public Companies

Public companies provide useful reference points, but they are not direct price tags for private architecture firms. Public businesses are often much larger, more diversified, more liquid, and easier for investors to buy and sell. Some also include unusual outliers that should not be treated as normal private company valuation benchmarks.

As of mid to late 2025, the public company data showed architecture, urban planning, and design consultancies at a median EV/Revenue of about 3.1x and median EV/EBITDA of about 16.5x. Global engineering and multidisciplinary consultancies traded lower on revenue at around 1.4x median EV/Revenue, but with more stable EBITDA multiples around 11.2x. Interior design and decoration specialists showed higher median revenue multiples, but the EBITDA data was heavily influenced by outliers and should be interpreted carefully.

The better public comps for a private architecture firm are not the highest outliers. The more grounded listed peers in the data often sit between roughly 0.4x and 2.4x revenue, especially where they are larger, diversified, and profitable. Some public companies show very high revenue multiples, but many of those are micro-cap, loss-making, platform-like, or otherwise not comparable to a normal private architecture studio.

Use public multiples as a reference band, not a direct valuation. If you are smaller, more founder-dependent, slower growing, or lower margin, buyers will usually apply a discount to public multiples. If you are scarce, highly specialized, growing well, and strategically important to a buyer, you may push closer to the high end of the private range or beyond it.

5. What Drives High Valuations - Premium Valuation Drivers

Premium valuations are not usually caused by one magical factor. They come from a cluster of signals that make buyers believe your business is durable, differentiated, and easier to scale after acquisition.

Strong management retention and leadership depth

Architecture is a people business. Buyers worry that if the founder leaves, clients and senior designers may leave too. That risk directly affects valuation.

You can reduce this risk by showing that client relationships are spread across multiple senior leaders, not just you. A buyer will feel more comfortable if studio heads, sector leads, and project directors are visible, credible, and likely to stay.

Practical examples include a clear second-line leadership team, signed employment or retention plans, documented account ownership, and willingness from key leaders to roll some equity or participate in an earnout where appropriate.

Large-scale, complex, multidisciplinary capability

Buyers pay more for capabilities that would take years to build. A firm that can handle complex planning, architecture, engineering coordination, project management, and specialist technical work is more valuable than a narrow studio that only does one part of the project.

This is especially true when the firm gives the buyer access to larger projects or new client budgets. If a buyer can acquire you and immediately bid for work it could not previously win, your strategic value increases.

For founders, this does not mean you need to become a global consultancy in 12 months. But you should clearly show where your capability is difficult to replicate: specialist sectors, proprietary design process, technical certifications, public sector frameworks, sustainability credentials, or long-standing client access.

High-margin advisory revenue

High gross margin is one of the clearest signs that buyers are acquiring expertise, not pass-through revenue. In architecture, fee-based design, planning, and advisory revenue is generally more attractive than revenue that includes heavy subcontractor, materials, or delivery costs.

Buyers will look for clean reporting. They want to understand how much revenue is pure design or advisory work, how much is project management, and how much is lower-margin delivery or pass-through cost.

If your financials mix everything together, you may be undervalued. Separating revenue streams can help buyers see the quality of your core business.

Strong EBITDA conversion

EBITDA is a simple measure of operating profit before certain accounting and financing costs. Buyers use it as a rough way to understand how much cash profit your business can produce.

Architecture firms with strong EBITDA margins tend to command better attention because they show pricing power and operational discipline. Good margins suggest that you are not just keeping designers busy, but managing scope, pricing, utilization, and overhead well.

Examples include clear fee proposals, strong change-order discipline, low rework, high staff utilization, and senior people spending time on high-value work rather than constantly rescuing weak projects.

Exposure to resilient and mission-critical end markets

Not all project sectors are valued equally. Buyers often prefer end markets where clients need to keep investing, even during slower economic periods.

Examples include healthcare, infrastructure, education, data centers, logistics, life sciences, public sector work, energy transition, and regulated technical facilities. These areas can make revenue feel more durable than luxury residential, speculative commercial development, or discretionary interiors.

If you serve more resilient end markets, make that clear. Show the percentage of revenue by sector, client type, and project stage. Buyers want evidence, not just a broad statement that your work is "diversified."

Growth with margin resilience

Growth is valuable only if it does not damage profit. Buyers are cautious when a firm grows quickly but margins fall, staff burnout rises, or project quality weakens.

The strongest story is growth with stable or improving margins. That tells buyers your business can scale without breaking. It also supports the idea that future revenue is worth paying for.

Good evidence includes multi-year revenue growth, stable EBITDA margins, rising average project size, repeat client work, and a backlog that converts into profit.

Clean financials and predictable pipeline

Even great firms lose value if the numbers are hard to trust. Buyers need clean monthly management accounts, clear revenue recognition, project-level profitability, and a realistic pipeline.

A strong pipeline is not just a list of hopeful opportunities. Buyers will want to know what is contracted, what is highly likely, what is speculative, and when revenue should be recognized.

The clearer your numbers, the less risk the buyer has to price in.

6. Discount Drivers - What Lowers Multiples

The lower end of the valuation range usually reflects risk. Buyers do not simply pay less because they are difficult. They pay less because they see issues that could reduce future profit or make integration harder.

The most common discount driver in architecture is founder dependence. If you personally own the biggest client relationships, approve every design decision, and close most new work, the buyer may worry that they are buying you rather than the business.

Another major discount is weak margin quality. If revenue is growing but profit is thin, buyers will ask whether the firm has pricing power. Low margins can also suggest poor scope control, too much unpaid design work, weak utilization, or too many low-value projects.

Client concentration also hurts valuation. A firm with one or two major clients may look strong today, but fragile tomorrow. Even if those clients are excellent, buyers will usually discount the multiple if losing one relationship would materially damage the business.

Other common discount drivers include:

Most of these issues can be improved. You do not need a perfect business to sell. But you do need to know which risks buyers will see and prepare a credible explanation or improvement plan before going to market.

7. Valuation Example: An Architecture Company

Let’s apply the logic to a fictional architecture company. The company and revenue level below are made up. The valuation ranges are illustrative only and are not investment advice or a formal valuation.

Assume Northstar Studio is a privately held architecture and design consultancy with USD 10m of annual revenue. It has 35 employees, a mix of commercial, cultural, education, and residential work, and a strong design reputation. Most revenue is fee-based design and advisory work, not construction delivery.

Step 1: Selecting the right valuation logic

For Northstar Studio, we would not use software-style multiples. It is a professional services firm. It sells expertise, creativity, client relationships, and project delivery, not recurring software subscriptions or product intellectual property.

The most relevant private market reference is architecture, engineering, and building design consultancies. The source data shows average EV/Revenue around 1.3x and average EV/EBITDA around 10.0x for that group, with a practical private-company revenue range often around 0.7x-1.5x for smaller and mid-sized consultancies.

We would also look at public architecture and built environment companies, but with caution. Public architecture and design consultancies showed a median EV/Revenue around 3.1x, but many public companies are much larger, more diversified, or distorted by outliers. For a small private firm, it is usually more realistic to start with private transaction data and then adjust based on quality.

Step 2: Applying the range to USD 10m revenue

For a boutique architecture business with USD 10m revenue, a defensible base-case range might be around 0.7x-1.2x revenue, or USD 7m-12m enterprise value.

If Northstar has stronger premium drivers - high margins, repeat clients, resilient sectors, second-line leadership, strong backlog, and clear specialist positioning - the range could move higher, perhaps toward 1.3x-1.8x revenue.

If Northstar has weaknesses - founder dependence, thin margins, inconsistent backlog, unclear financials, or high exposure to volatile development work - the range could fall toward 0.4x-0.7x revenue.

A strategic premium case would require more than good design. It would usually require something scarce: a highly attractive niche, unusually strong margins, deep leadership bench, mission-critical sectors, a strong pipeline, or a buyer that sees immediate strategic value.

Step 3: What this means for founders

The lesson is that revenue alone does not determine value. Two USD 10m architecture firms can have very different outcomes.

One may be worth USD 6m because it is founder-dependent, low-margin, and project-by-project. Another may be worth USD 15m or more because it has strong margins, repeat clients, a clear niche, and a leadership team that can run the business without the founder.

That is why the 6-12 months before a sale matter. You may not be able to double revenue in that time, but you can often improve how buyers perceive risk, quality, and future growth.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a simple scoring tool. It will not give you a formal valuation, but it can help you understand whether your business is more likely to sit near the lower, middle, or higher end of the valuation range.

Score each factor from 0 to 2:

- 0 = weak or not proven

- 1 = acceptable but not clearly strong

- 2 = strong and well evidenced

Interpreting your score

Be honest with yourself. The purpose is not to "win" the scorecard. The purpose is to find the few areas where improvement could have the biggest valuation impact.

If you score low because of weak financial reporting, that may be fixable in months. If you score low because of founder dependence, you can start moving client ownership to senior leaders now. If you score low because of low margins, you can review pricing, scope control, and project selection before launching a sale process.

9. Common Mistakes That Could Reduce Valuation

Rushing the sale

Many founders start a sale process before the business is ready. They have unclear financials, no prepared buyer story, weak pipeline detail, and no evidence for the valuation they want.

That usually leads to weaker offers. Buyers see uncertainty, and uncertainty becomes a discount.

Hiding problems

Problems will come out in due diligence. If you hide client churn, margin issues, disputes, staff problems, or pipeline weakness, buyers will lose trust.

Once trust is damaged, the buyer may lower the price, demand tougher deal terms, or walk away entirely. It is usually better to disclose issues clearly and explain what you are doing about them.

Weak financial records

Architecture firms often underinvest in financial reporting. That can be costly in a sale.

Buyers want to see revenue by client, sector, service line, project type, and geography. They also want project-level profitability, backlog detail, utilization, and a clear bridge from accounting profit to EBITDA.

If you have 6-12 months, improve this now. Better reporting can directly reduce buyer uncertainty.

No structured competitive process

Selling to one buyer who approached you can feel easy, but it often leaves money on the table. A structured process creates competition, and competition improves price discovery.

Research commonly cited in M&A shows that running a structured competitive process with an advisor can lead to meaningfully higher purchase prices, often around 25% higher than less competitive approaches. The exact uplift varies, but the principle is clear: more qualified buyers usually means stronger negotiating leverage.

Revealing your target price too early

If you tell buyers you want USD 10m, many will anchor around that number. You may receive offers of USD 10.1m or USD 10.2m, even if a buyer might have paid more.

Let the market come back with offers. Price discovery works best when qualified buyers compete based on their own view of value.

Mixing high-quality design fees with low-quality pass-through revenue

This is a specific issue in architecture and built environment firms. If your financials combine advisory fees, procurement, subcontracted work, and pass-through costs into one revenue line, buyers may assume the whole business has lower-quality economics.

Separate the revenue streams. Show what is high-margin design and advisory work versus lower-margin delivery or pass-through activity.

Overstating the value of the portfolio

A beautiful portfolio helps, but buyers do not pay only for past work. They pay for future cash flow.

Awards, design reputation, and iconic projects matter most when they translate into repeat clients, pricing power, recruiting strength, and future pipeline.

10. What Architecture Founders Can Do in 6-12 Months to Increase Valuation

You do not need to reinvent the business before a sale. The highest-return work is usually about reducing buyer risk and making the value drivers easier to prove.

Improve the numbers

Start with project profitability. Review which projects, sectors, clients, and service lines produce the best margins. Then shift business development toward work that looks more like your best-performing projects.

Tighten pricing and scope control. Architecture firms often give away unpaid work through unclear scope, weak change-order discipline, or excessive senior involvement. Small improvements here can lift EBITDA meaningfully.

Build clean monthly reporting. At minimum, you should be able to show revenue, gross margin, EBITDA, backlog, pipeline, utilization, and project profitability by category.

Strengthen the revenue story

Break down revenue by client, sector, geography, and service line. Buyers want to know what kind of revenue they are buying.

Highlight repeat clients and framework agreements. Even if architecture is not a subscription business, repeat work can act like recurring revenue in the eyes of buyers.

Clarify backlog quality. Separate signed work, verbally awarded work, high-probability pipeline, and speculative opportunities. Do not make buyers guess.

Reduce key-person risk

Move client relationships from the founder to a wider leadership team. Have senior people lead client meetings, proposals, and project reviews before the sale process begins.

Document the operating rhythm of the business. Buyers feel better when they see systems for project staffing, quality control, client communication, billing, hiring, and project reviews.

Consider retention plans for key employees. You do not need to promise anything unrealistic, but you should know who is critical to the buyer’s confidence.

Sharpen the strategic story

Pick your clearest niche. Are you strongest in healthcare, education, workplace, cultural projects, public realm, hospitality, residential, sustainability, or technical facilities? A focused story is usually more valuable than "we do everything."

Show why a buyer should care. That might be access to a geography, a client base, a specialist capability, a design reputation, or a team that can help them win larger projects.

Prepare proof. Buyers need evidence: case studies, client retention, win rates, margins by sector, backlog, awards, certifications, and leadership bios.

Clean up avoidable risks

Resolve disputes where possible. Review professional liability history. Make sure contracts, employee agreements, leases, insurance, and intellectual property ownership are organized.

Clean up working capital. Late billing, slow collections, and unclear work-in-progress accounting can create price adjustments late in the process.

Fix the basics before buyers arrive. The fewer surprises they find, the stronger your negotiating position.

11. How an AI-Native M&A Advisor Helps

Selling an architecture business is not just about finding a buyer. It is about finding the right buyers, creating competition, preparing the numbers, and framing the story in a way that buyers understand.

An AI-native M&A advisor like Eilla AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, geography, sector focus, and likely synergies. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes because you have options if one buyer drops out.

AI can also speed up the early stages of the process. Buyer matching, outreach preparation, marketing materials, data organization, and due diligence support can move faster than manual-only processes. That can help founders reach initial conversations and offers in under 6 weeks when the business is prepared.

The human advisor still matters. Expert M&A advisors bring judgment, buyer credibility, negotiation experience, and the ability to frame your business in the language acquirers understand. The AI enhances that work by making the process broader, faster, and more data-driven.

The result is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.