The Complete Valuation Playbook for Car Wash and Care Businesses

A practical breakdown of how car wash and care businesses are valued and what drives high multiples.

Car Wash and Care is no longer just a local cash-flow business. The sector now includes tunnel washes, express exterior sites, detailing studios, mobile and waterless wash operators, coatings specialists, chemicals and consumables brands, fleet service providers, and technology-enabled automotive care platforms.

That matters because buyers are not valuing every business the same way. A labor-heavy mobile wash company, a membership-driven express wash chain, and a branded coatings product business can all sit inside "Car Wash and Care", but they may attract very different multiples.

This playbook shows what businesses in and around the sector actually sell for, what public markets imply, what pushes valuation up or down, and how you can assess your own business before going to market in the next 1-12 months.

1. What Makes Car Wash and Care Unique

Car Wash and Care sits at the intersection of consumer services, automotive aftermarket, local infrastructure, and recurring maintenance. That makes valuation more nuanced than a simple "revenue times multiple" exercise.

The main business types include:

The best businesses in this sector often combine three things: repeat demand, operational discipline, and a reason customers choose them over the cheaper option. That reason can be convenience, location, speed, quality, brand, environmental positioning, fleet integration, or proprietary products.

Buyers will always check risk. In this sector, that usually means labor availability, site dependency, water and environmental rules, customer concentration, seasonality, lease terms, equipment condition, local competition, and whether reported earnings are clean.

A car wash may look simple from the outside. In a sale process, buyers will go deep on throughput, membership churn, average ticket, add-on penetration, labor scheduling, chemical cost, water cost, maintenance spend, and whether revenue is truly repeatable.

2. What Buyers Look For in a Car Wash and Care Business

Buyers start with the obvious questions: How big is the business? Is it growing? Is it profitable? Are the financial records reliable? Can the business keep growing after the founder leaves?

Then they look at the industry-specific details. For a Car Wash and Care business, buyers care about the source and quality of revenue. A business with monthly members, fleet contracts, and strong repeat customers is usually more attractive than one dependent on one-time walk-ins or discount campaigns.

They also care about how much operational effort is required to generate each dollar of revenue. Product and coatings businesses can sometimes scale more cleanly because they are less tied to daily labor scheduling. Fixed-site wash chains can be attractive when they have strong locations and high membership penetration. Mobile wash operators can be attractive when route density, fleet contracts, and app-based booking make the model predictable.

How private equity buyers think

Private equity buyers are usually asking a simple question: "If we buy this business today, can we sell it for more in 3-7 years?"

That depends on the entry multiple, the growth plan, and the likely exit buyer. They may ask:

- Could this become a larger regional or national platform?

- Could it acquire smaller local operators?

- Could pricing, memberships, add-ons, or fleet contracts improve revenue?

- Could better procurement, labor scheduling, or routing improve margins?

- Would a larger strategic buyer care about this business later?

Private equity buyers also think about the "exit multiple". If they buy your business at 6.0x EBITDA, they want to believe a future buyer might pay the same or more after the business is larger, cleaner, and less risky.

For founders, the takeaway is clear: buyers do not just pay for what you built. They pay for what they believe the next owner can build from it.

3. Deep Dive: Fixed-Site Strength vs Mobile Flexibility

One of the biggest valuation questions in Car Wash and Care is whether your model depends on fixed locations, mobile delivery, products, or some mix of the three.

Fixed-site washes can be valuable because location is hard to replicate. A high-traffic site with good access, strong signage, clean facilities, and a deep membership base can become a local infrastructure asset. Buyers like that because the business has physical scarcity.

Mobile and waterless models have a different advantage. They can meet customers where the car already sits: office parking, apartment buildings, dealerships, fleet depots, shopping centers, or airport parking. That flexibility can be powerful, especially when water use, convenience, and fleet maintenance matter.

But mobile models also face a valuation challenge. Buyers will ask whether the model has real operating leverage, or whether growth simply means hiring more people, buying more vans, and managing more daily complexity. The same revenue can be valued very differently depending on whether the mobile model has dense routes, strong utilization, recurring fleet contracts, and attractive margins.

The source data shows a clear pattern: businesses tied to enterprise automotive ecosystems, broad infrastructure, or differentiated products tend to earn stronger buyer attention. For a Car Wash and Care founder, that means the most valuable version of the business is usually not "we wash cars". It is "we own a repeatable customer relationship around vehicle care, and we can monetize that relationship in several ways."

A mobile operator can move toward a higher-value profile by adding fleet packages, apartment or office partnerships, subscription plans, route density targets, technician productivity tracking, and clearer gross margin reporting. A fixed-site operator can do the same by increasing membership mix, add-on services, local brand strength, and site-level reporting.

4. What Car Wash and Care Businesses Sell For - and What Public Markets Show

Valuation data in this sector is messy because the industry includes several different models. A coatings product business, an automotive service network, a car wash operator, and a cleaning equipment company may all be relevant, but none is a perfect match for every founder.

The right way to use the data is to triangulate. Look at private transactions, look at public market trading multiples, then adjust for your size, growth, margin, risk, revenue quality, and strategic value.

4.1 Private Market Deals - Similar Acquisitions

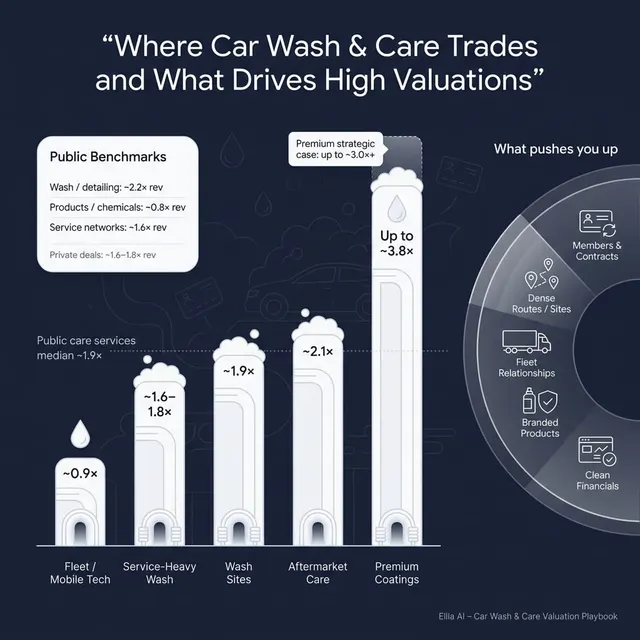

The private transaction data points to a broad range. Across the disclosed precedent transactions, the overall average EV/Revenue multiple is around 1.8x, with a median around 1.6x. The overall EV/EBITDA average and median are both around 5.2x.

The most relevant private groups suggest that automotive aftermarket products, parts, and dealership services traded around 2.1x revenue and 5.4x EBITDA on average. Vehicle infrastructure, access, parking, and logistics assets traded around 1.9x revenue and 5.0x EBITDA. Fleet, vehicle, and mobility technology assets in the data showed a lower disclosed revenue multiple around 0.9x.

For founders, the practical read is this: many service-heavy Car Wash and Care businesses may sit around the low-to-mid revenue multiple range unless they have clear recurring revenue, strong margins, or strategic scarcity. Product-led, coatings-led, infrastructure-led, or enterprise-integrated businesses can move higher if buyers believe the model scales beyond local operations.

These ranges are illustrative, not a formal valuation. A smaller founder-owned business with incomplete financials may trade below the headline range. A cleaner, faster-growing business with contracted revenue and strong margins may trade above it.

4.2 Public Companies

Public market multiples give a wider reference point, but they are not direct price tags for private companies. Public companies are usually larger, more diversified, more liquid, and more mature. Buyers often apply a discount when valuing smaller private businesses.

As of mid-to-end 2025, the public comps around Car Wash and Care show clear differences by segment. Car Wash, Detailing, and Coating Service Operators traded at an average EV/Revenue of about 2.2x and average EV/EBITDA of about 11.1x. Automotive Cleaning Products, Chemicals, and Care Equipment traded lower on revenue, around 0.8x on average, but with stronger EBITDA reference points around 8.7x on average. Automotive Service Networks showed average EV/Revenue around 1.6x, but the EV/EBITDA average was elevated by outliers, with a median around 13.5x.

The public data says two things at once. First, scaled Car Wash and Care operators can attract healthy revenue and EBITDA multiples when they have size, profitability, and repeat demand. Second, there is a big difference between the average and the median in some groups, which means outliers can distort the headline number.

Founders should use public multiples as a reference band, not a promised outcome. A smaller private company may deserve a discount for size, customer concentration, limited reporting, founder dependence, or lower liquidity. But a scarce asset with strategic value, strong growth, clean margins, and repeat revenue can sometimes command stronger interest than the basic private-company average suggests.

5. What Drives High Valuations - Premium Valuation Drivers

High valuations are not random. The source data shows several clear premium patterns, and they line up with what buyers typically reward in Car Wash and Care.

5.1 Real geographic coverage

Buyers pay more when geographic reach means real operating infrastructure, not just a map on a website. A business with dense local sites, strong fleet coverage, or controlled regional operations is more valuable than one with scattered, lightly used service areas.

For a car wash operator, this could mean multiple high-quality locations in a metro area. For a mobile operator, it could mean dense routes and dependable technician coverage. For a coatings or chemicals business, it could mean strong distributor relationships and repeat customers across regions.

The key is proof. Buyers want to see that geographic coverage creates revenue, efficiency, and defensibility.

5.2 Recurring revenue and customer stickiness

Memberships, fleet contracts, dealership programs, corporate accounts, and subscription-like care packages all make revenue more predictable. Predictable revenue reduces buyer fear.

In this sector, recurring revenue may come from unlimited wash plans, ceramic coating maintenance packages, fleet wash contracts, parking-location partnerships, or regular dealership reconditioning work.

Buyers care because sticky customers make the next year easier to forecast. A business with the same revenue but weaker repeat behavior will usually feel riskier.

5.3 Enterprise and institutional relationships

The source data highlights stronger strategic value when businesses are integrated into enterprise automotive ecosystems: original equipment manufacturers, dealerships, fleets, insurers, financing platforms, parking operators, or mobility infrastructure.

For founders, this matters because institutional customers can create volume, predictability, and credibility. A mobile wash company with repeat fleet contracts may be easier to underwrite than one relying only on consumer app bookings.

But buyers will check the depth of those relationships. A signed multi-year contract is stronger than an informal referral arrangement. High retention is stronger than one-time project work.

5.4 Multiple revenue streams per customer or location

Buyers like businesses that can earn more from the same customer relationship. In Car Wash and Care, that might mean wash memberships plus detailing, coatings, windshield treatment, odor removal, interior protection, fleet inspections, tire shine, retail products, or digital scheduling.

This matters because it can increase average revenue without needing to win a new customer every time. It also makes the business more strategic to buyers who want a platform for broader automotive care.

A single-purpose wash can still be attractive. But a business that owns the customer relationship and can add profitable services often earns a stronger narrative.

5.5 Scalable product or coatings economics

The source data shows a premium pattern around asset-light consumables, coatings, paints, primers, protective products, and detailing solutions. These models can scale differently from labor-heavy services.

A product or coatings business may have better gross margins, repeat purchasing, brand value, and distribution leverage. It is less exposed to daily technician scheduling, route planning, weather disruptions, and local labor issues.

For service businesses, this does not mean you need to become a manufacturer. But adding proprietary or branded care packages can strengthen your story if the margins and repeat usage are real.

5.6 Clean financials and strong operating discipline

Even if your business has great growth, messy numbers can lower buyer confidence. Clean monthly financials, clear site-level or route-level margins, reliable revenue recognition, and well-tracked key metrics all help buyers trust the story.

Important metrics include membership count, churn, average ticket, gross margin, labor cost as a percentage of revenue, chemical cost, water cost, utilization, fleet retention, and maintenance spend.

A buyer will pay more when they do not have to guess.

5.7 Leadership depth beyond the founder

Many private Car Wash and Care companies are founder-led. That is not a problem by itself. It becomes a valuation issue when the founder is the sales engine, operations manager, customer relationship owner, pricing authority, and finance lead all at once.

A stronger management bench reduces transition risk. Buyers want to know the business can perform after closing.

That can include a general manager, site managers, fleet account lead, operations lead, finance controller, or documented processes that reduce founder dependence.

6. Discount Drivers - What Lowers Multiples

Discount drivers are not moral judgments. They are buyer risk signals. The more risk buyers see, the more they lower the price, demand seller financing, add earnouts, or walk away.

The first major discount is service intensity without strong margins. A mobile wash business that grows only by adding more technicians, vans, and scheduling complexity may be viewed as a local service company rather than a scalable platform. Buyers will ask whether growth actually improves profit.

The second discount is weak repeat revenue. If most revenue comes from one-time customers, discounting, weather-driven demand, or seasonal spikes, buyers have less confidence in next year’s performance. That usually lowers the multiple.

The third discount is customer or location concentration. If one fleet account, dealership group, office park, or site contributes too much revenue, buyers will worry about what happens if that relationship ends.

Other common discount drivers include:

Some discount drivers are fixable in 6-12 months. Others take longer. The key is to identify them before buyers do, then either improve them or explain them clearly.

7. Valuation Example: A Car Wash and Care Company

Let’s apply the logic to a fictional company. This example is not investment advice, not a formal valuation, and not a fairness opinion. It is only designed to show how buyers may think.

Assume a fictional company called ClearBay Auto Care. ClearBay generates USD 10m of annual revenue. It provides mobile waterless washing, detailing, and light protective care services to consumers, apartment buildings, office parks, and local fleets.

ClearBay has an app-based booking system, a small set of fleet accounts, some recurring care packages, and a growing brand in two metro areas. It is still service-heavy, but it has better route density than a pure on-demand operator.

Step 1: Select the right valuation anchors

The right starting point is not software companies. ClearBay uses technology, but it is still mostly an operating service business. That means buyers would likely anchor to car wash, automotive services, mobile care, fleet service, coatings, and adjacent automotive aftermarket transactions.

The source data suggests several guideposts:

- Public car wash / detailing / coating service operators trade around 1.9x median revenue and 9.2x median EBITDA.

- Private precedent transactions in adjacent automotive and mobility services average around 1.6-1.8x revenue overall.

- Automotive aftermarket product and care deals average around 2.1x revenue.

- Premium product-led or coatings-led assets can reach higher revenue multiples.

- Smaller, early-stage, service-heavy companies usually deserve a discount to large public operators.

Step 2: Narrow the range

For ClearBay, a reasonable core revenue multiple range might be around 1.3x-1.8x revenue. That reflects a service-heavy operating model, some recurring revenue, some technology enablement, and a need to prove scale, margins, and defensibility.

A stronger case could reach around 2.0x-2.4x revenue if ClearBay has high fleet retention, strong gross margins, dense routes, documented churn, a real management team, and evidence that each new market improves profitability.

A weaker case could fall closer to 0.8x-1.2x revenue if revenue is mostly one-time consumer demand, margins are thin, financials are messy, or the founder is central to daily operations.

A true premium case would need more than a good story. Buyers would want proof: strong recurring revenue, superior margins, enterprise accounts, proprietary products or coatings, exceptional retention, defensible geographic density, and a clear path to scale.

Step 3: What this means for founders

Two Car Wash and Care companies with USD 10m of revenue can be worth very different amounts.

One may be worth closer to USD 10m because it is labor-heavy, local, seasonal, and hard to transfer. Another may be worth USD 20m or more because it has recurring fleet contracts, dense routes, strong margins, clean reporting, and a management team that can run without the founder.

This is why valuation work before a sale matters. You are not just selling revenue. You are selling the quality, predictability, and future usefulness of that revenue.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a practical self-check. Score each factor from 0 to 2:

- 0 = weak or not proven

- 1 = average or partially proven

- 2 = strong and clearly documented

Be honest. The purpose is not to flatter the business. It is to identify the areas that will have the biggest impact before a sale.

How to interpret your score

If you score 10-12, you likely have several features buyers associate with premium outcomes. That does not guarantee a premium valuation, but it gives you a better story and more leverage.

If you score 6-9, you may sit in the fair market range. You probably have a sellable business, but there may be clear improvements that could increase buyer confidence.

If you score 0-5, a sale may still be possible, but the business likely needs preparation. Buyers may see too much risk, ask for a lower price, or structure more of the consideration as an earnout.

The goal is not perfection. The goal is to move the highest-impact items before launching a sale process.

9. Common Mistakes That Could Reduce Valuation

Rushing the sale

Many founders go to market before the numbers, story, and process are ready. That can cost real money.

In Car Wash and Care, preparation means more than having tax returns. Buyers will want to understand recurring revenue, customer retention, site or route economics, labor costs, add-on revenue, equipment condition, and how the business performs by month.

A rushed process gives buyers more reasons to discount.

Hiding problems

Do not hide issues. They usually surface in due diligence.

If you have customer concentration, weak margins, lease risk, environmental issues, employee misclassification risk, or messy revenue recognition, address it directly. Buyers can accept known problems more easily than surprises.

A surprise late in the process destroys trust. Once trust is damaged, price usually follows.

Weak financial records

Poor records make buyers nervous because they cannot tell what they are really buying.

For this sector, founders should be able to show clean revenue by service type, gross margin by location or route, labor cost, chemical cost, water cost, maintenance spend, membership revenue, fleet revenue, and customer retention.

The good news is that financial reporting can often be improved within 6-12 months.

No structured competitive process

A structured sale process with an advisor typically leads to meaningfully stronger outcomes because it creates competition. Research often cited in M&A suggests advised, competitive processes can produce purchase prices around 25% higher than less structured approaches.

The reason is simple. If only one buyer is involved, that buyer controls the tempo. If several qualified buyers are involved, the market helps reveal the real value.

Revealing your target price too early

Do not tell buyers the price you want at the start.

If you say you want USD 10m, many buyers will anchor around that number. You may get offers at USD 10.1m or USD 10.2m even if the market might have supported more.

A good process lets buyers show you what they are willing to pay before you narrow the conversation.

Ignoring site, route, or fleet-level data

Car Wash and Care buyers do not just buy headline revenue. They buy operating performance.

If you cannot show which locations, routes, fleets, or service lines are profitable, buyers may assume the worst. That can reduce valuation even if the business is actually strong.

Overstating the "tech" angle

Many Car Wash and Care businesses use apps, booking tools, customer databases, or route planning software. That helps, but it does not automatically make the business a technology company.

Buyers will ask whether the technology improves margins, retention, utilization, customer acquisition, or scalability. If not, they will still value the business as a service operator.

10. What Car Wash and Care Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers care about

Start with gross margin and EBITDA margin. Review labor scheduling, technician productivity, chemical usage, water cost, procurement, overtime, discounting, and underpriced services.

For mobile operators, improve route density and utilization. For fixed-site operators, increase throughput, membership conversion, add-on penetration, and off-peak demand. For coatings and detailing businesses, track margin by package and upsell path.

Small improvements in margin can have a large effect on valuation because many buyers value the business based on EBITDA.

Make revenue more predictable

Push more customers into memberships, maintenance plans, fleet contracts, or recurring care packages. Buyers will reward revenue they can see coming.

If you serve fleets, get contracts in writing. If you serve apartment buildings, office parks, or dealerships, formalize the relationship. If you have memberships, track churn and payment failure.

A buyer should be able to see not just what you sold last month, but why customers will still be there next month.

Clean up reporting

Prepare monthly financials, not just annual tax accounts. Separate revenue by service line. Track gross margin by location, route, fleet, or package.

Build a simple dashboard with:

- Revenue

- Gross margin

- EBITDA

- Membership count

- Churn

- Average ticket

- Fleet revenue

- Labor cost

- Chemical and water cost

- Customer reviews

- Utilization or throughput

You do not need an overly complex finance system. You need numbers that are consistent, understandable, and trusted.

Reduce founder dependence

Document your operating playbook. Train managers. Move customer relationships into the company, not just the founder’s phone.

Create clear responsibilities for sales, operations, finance, fleet relationships, technician training, and customer service. Buyers pay more when the company can run without constant founder intervention.

Strengthen the buyer story

Before going to market, decide what you are really selling.

Are you the best express wash chain in a growing metro? A mobile fleet care provider with dense routes? A premium detailing and coatings brand? A sustainable waterless wash platform? A high-margin consumables company?

The sharper the story, the easier it is for buyers to understand why your business matters.

Fix avoidable diligence issues

Review leases, permits, environmental practices, equipment maintenance logs, employee classifications, insurance, customer contracts, and supplier agreements.

Do not wait for buyers to find problems. Identify them early, fix what you can, and prepare clear explanations for what remains.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can help founders run a broader, faster, and more competitive process without losing the judgment of experienced human advisors.

The first advantage is buyer reach. AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, synergies, financial capacity, geography, and other signals. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal closes because there are more options if one buyer drops.

The second advantage is speed. AI-driven buyer matching, buyer outreach, marketing material preparation, and due diligence support can help generate initial conversations and offers in under 6 weeks. That does not mean cutting corners. It means removing manual bottlenecks from the process.

The third advantage is expert advisory enhanced by AI. You still need experienced M&A advisors who know how to frame the business, manage buyers, protect leverage, and negotiate. AI helps those advisors prepare better materials, analyze buyers faster, and position the company in the most attractive way.

For Car Wash and Care founders, the outcome is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.