The Complete Valuation Playbook for Carbon Management Businesses

A practical breakdown of how carbon management businesses are valued - and what drives premium multiples.

Carbon management has moved from a “nice to have” sustainability topic into a board-level, compliance, cost, and risk issue. Buyers are paying closer attention because regulation, carbon reporting rules, energy transition pressure, and customer supply-chain demands are forcing companies to measure, reduce, report, and sometimes offset emissions with more discipline.

This guide is built for founders and CEOs of privately held carbon management businesses who may consider a sale in the next 1-12 months. It will show what businesses in and around carbon management have actually sold for, what public markets suggest, what drives higher or lower multiples, and how to assess your own company before going to market.

The valuation data and deal patterns used in this article are based on the provided company, transaction, public trading, and valuation driver data for carbon management and adjacent ESG, compliance, energy, environmental, and sustainability software businesses.

1. What Makes Carbon Management Unique

Carbon management is not one simple market. It includes software, consulting, carbon credit services, energy management, environmental infrastructure, compliance workflows, and specialized data products. That matters because buyers do not value all of these the same way.

At one end of the market are software-first businesses: carbon accounting platforms, product carbon footprint tools, ESG reporting platforms, emissions data systems, and compliance workflow software. These can attract strong revenue multiples when they have recurring revenue, high gross margins, and become embedded in the customer’s reporting process.

At the other end are consulting-led businesses: carbon audits, energy procurement advice, regulatory reporting support, sustainability strategy, and implementation services. These can be valuable companies, but buyers usually value them more like professional services businesses because growth depends more on people, billable hours, and project delivery.

There are also hybrid models. Many carbon management companies start with services because customers need help setting emissions baselines, cleaning messy data, and understanding new rules. That is not automatically bad. The question is whether services help sell and implement scalable software, or whether the business is mostly services with a software wrapper.

Buyers will always check a few sector-specific risks:

The most valuable companies in this sector usually sit at the intersection of regulation, repeatable software, hard-to-replace data workflows, and clear customer return on investment.

2. What Buyers Look For in a Carbon Management Business

Buyers start with the basics: revenue scale, revenue growth, profitability, customer concentration, margins, and cash flow. A USD 10m revenue company growing 40% with strong retention is valued very differently from a USD 10m company growing 5% with project-based revenue and weak margins.

But in carbon management, the sector lens matters just as much as the headline numbers. Buyers want to know whether customers are buying because they must comply with regulation, because they want to save energy costs, because investors are asking for disclosure, or because sustainability is part of a broader brand story. Mandatory and budgeted use cases usually attract stronger valuations than discretionary ESG projects.

They also care deeply about where you sit in the customer’s workflow. A tool used once a year to create a sustainability report is less valuable than a system that collects operational data, tracks emissions, supports audits, feeds board reporting, and connects to procurement, ERP, or compliance systems.

For strategic buyers, the key question is often: “Does this business help us sell more to our existing customers?” A compliance software group may value a carbon reporting platform because it expands its governance and reporting suite. An energy services company may value carbon management because it deepens its customer relationship. A data provider may value emissions intelligence because it strengthens its analytics offering.

How Private Equity Buyers Think

Private equity buyers think about today’s value and future resale value. They ask: “If we buy this company now, who could buy it from us in 3-7 years?”

They will consider the entry multiple, which is the valuation multiple they pay today. Then they think about the exit multiple, which is what a future buyer might pay if the company grows, becomes more profitable, and reduces risk.

They also look for practical levers. Can they raise prices? Reduce churn? Add salespeople? Cross-sell into a larger customer base? Acquire smaller competitors? Improve margins? Turn services into repeatable software implementation packages?

The cleaner and more repeatable your growth story is, the easier it is for a financial buyer to pay a strong price.

3. Deep Dive: Software-Led Compliance vs Services-Led Advisory

The biggest valuation divide in the data is not “carbon management versus non-carbon management.” It is software-led, recurring, compliance-critical revenue versus services-led advisory revenue.

That distinction shows up clearly in the precedent deal set. Software-led compliance and regulatory platforms reached materially stronger revenue and EBITDA multiples than consulting-heavy or equipment/service-heavy businesses. Consultancy-style environmental and energy businesses in the data traded around or below 1.0x revenue in some cases, while software-led compliance and asset management platforms reached roughly 4.4x-6.4x revenue.

Buyers pay more for software-led models because each additional customer can often be served without adding the same amount of headcount. If the product is well built, one more customer does not require one more consultant. That is what buyers mean when they talk about scalability.

In carbon management, this is especially important because customer problems can be messy. Emissions data may live across spreadsheets, suppliers, meters, ERP systems, bills, factories, and procurement records. If your company solves that complexity with repeatable software and clear workflows, you look much more valuable. If every customer requires a custom consulting project, buyers will discount the multiple.

If your business looks more like the left column today, that does not mean it is unsellable. But in the 6-12 months before a process, you should work to prove that services are enabling software adoption, not replacing the software product.

A practical move is to separate revenue clearly. Show buyers what is recurring subscription revenue, what is implementation, what is advisory, and what is pass-through or low-margin work. Then show how the software portion is growing faster and becoming a larger share of the business.

4. What Carbon Management Businesses Sell For - and What Public Markets Show

Valuation multiples in carbon management are wide because the market includes very different business models. A carbon credit project developer, an energy consultancy, an ESG data platform, and a compliance software company may all be “carbon management” businesses, but buyers value their revenue differently.

The right way to use multiples is not to pick the highest number and apply it to your revenue. The right way is to identify which group your business most closely resembles, then adjust up or down based on growth, margins, revenue quality, customer stickiness, and strategic scarcity.

4.1 Private Market Deals Similar Acquisitions

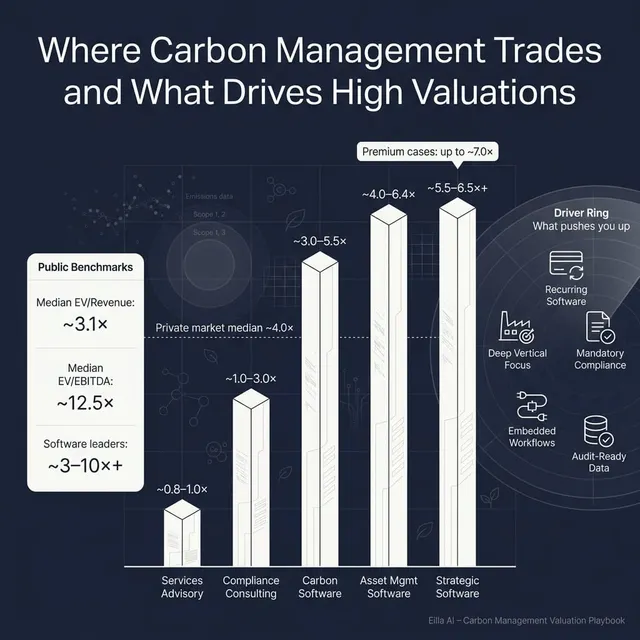

The precedent transaction set shows a broad private market range. Overall, the average EV/Revenue multiple was about 3.5x and the median was about 4.0x. On EBITDA, the average was about 11.0x and the median was about 9.1x.

The real insight is the spread by business model. Consulting-heavy environmental, energy, and sustainability services businesses generally sat much lower, often around 0.9x revenue. Software-led compliance, regulatory, and asset management platforms achieved materially stronger outcomes, often in the 4.0x-6.4x revenue range. EBITDA multiples for profitable software-led compliance businesses also reached the low double digits and higher in stronger cases.

These ranges are illustrative. A smaller company with strong growth, high retention, and clear software revenue can beat a larger but slower services-led business. Equally, a company with “AI” or “carbon” in the story but weak retention and messy delivery may not receive a premium.

4.2 Public Companies

Public market multiples give founders a reference point, not a direct sale price. Public companies are usually larger, more liquid, more diversified, and more mature than private founder-led businesses. That means private companies often trade at a discount unless they are growing very fast or are strategically scarce.

The public company set shows an overall average EV/Revenue of about 18.7x, but that average is distorted by outliers. The median EV/Revenue is much more useful at about 3.1x. For EV/EBITDA, the average was about 24.3x and the median was about 12.5x. These public market figures are from the 2025 dataset provided.

The public data reinforces a simple point: buyers pay more for scalable software, strong gross margins, regulatory relevance, and strategic data assets. They pay less for low-margin services, volatile credit exposure, weak profitability, or models that require heavy capital spending.

As a founder, use public multiples as upper and lower reference bands. Then adjust downward for smaller scale, customer concentration, slower growth, or heavier services mix. In rare cases, adjust upward if your business is a scarce strategic asset that a buyer cannot easily build.

5. What Drives High Valuations Premium Valuation Drivers

Premium valuations usually come from a combination of financial quality and strategic relevance. One driver alone rarely does all the work. The strongest businesses show several of these traits at the same time.

5.1 Software-First Revenue

Buyers pay more when revenue is recurring, product-led, and scalable. In carbon management, this means customers pay for a platform they use repeatedly, not just a one-time carbon audit.

Examples include carbon accounting software, supplier emissions data workflows, product carbon footprint tools, and compliance reporting platforms. The more your product becomes the customer’s system of record for emissions data, the stronger the valuation story.

5.2 Mission-Critical Regulation

Regulation is a powerful driver when it creates non-discretionary demand. Buyers like revenue that is tied to rules customers must follow, not budget items they can cut when times get hard.

For carbon management, strong examples include CSRD, ESRS, CBAM, EU Taxonomy, Scope 1, Scope 2, Scope 3 reporting, product carbon footprint requirements, and supplier-level emissions disclosure. Regulation alone is not enough. The premium comes when your product helps customers comply in a recurring, auditable, hard-to-replace way.

5.3 Deep Vertical Specialization

A horizontal carbon tool can be useful, but a deeply specialized platform can be more defensible. Buyers value companies that understand the data, workflows, language, and compliance pain of a specific customer group.

For example, a platform built for mid-sized manufacturers may handle supplier data, product-level footprints, factory emissions, energy usage, and customer reporting requests better than a generic ESG reporting tool. That specialization can reduce churn and increase strategic value.

5.4 Strong Gross Margins and Delivery Discipline

High gross margin means that after direct costs, a large share of revenue is left to pay for sales, product, management, and profit. Software businesses often have higher gross margins than consulting businesses because they are less dependent on billable labor.

In carbon management, buyers will look closely at implementation costs. If onboarding each customer takes months of custom work, the model may be less scalable than it first appears. If onboarding is repeatable and supported by templates, integrations, and automated data collection, the business looks stronger.

5.5 Embedded Workflows and Integrations

A product that sits inside a customer’s workflow is harder to remove. Buyers value integrations with ERP systems, procurement tools, utility data, supplier portals, reporting systems, and audit workflows.

The more your platform becomes part of how the customer runs compliance, procurement, operations, or board reporting, the more strategic it becomes. A simple dashboard is easier to replace than a platform tied into real business processes.

5.6 Strategic Fit for Acquirers

Some buyers pay more because your product fills a gap in their platform. A governance software company may want carbon compliance. An energy services group may want emissions data. A data provider may want carbon intelligence. An industrial software buyer may want decarbonization workflows.

This is where competitive tension matters. If several buyer groups can each tell a different strategic story for why they need your business, your process can create stronger price discovery.

5.7 Clean Financials and a Credible Team

Even the best market story can be damaged by poor numbers. Buyers pay more when financials are clean, revenue is well categorized, churn is tracked, margins are clear, and forecasts are believable.

They also want to know the business can run after a sale. A strong leadership bench, documented processes, and limited founder dependency can all improve buyer confidence.

6. Discount Drivers What Lowers Multiples

The most common discount driver is a services-heavy model. If buyers conclude that most revenue comes from people doing projects, not software being used repeatedly, the valuation usually moves closer to consulting multiples.

Another major discount is weak revenue quality. One-off projects, short contracts, unclear renewal patterns, high churn, or customers that only buy once every few years all make buyers cautious. Carbon management companies sometimes struggle here when revenue comes from initial baselining work but does not convert into ongoing monitoring and compliance workflows.

Low or unclear margins also reduce value. If the company is growing but every new customer requires expensive manual work, buyers will question whether the business can scale profitably.

Carbon credit exposure can also create discounts. Buyers will check credit quality, verification, permanence, additionality, reputational risk, and regulatory treatment. If credits are low quality or revenue depends heavily on volatile credit pricing, the multiple can compress.

Customer concentration is another issue. If a few large customers represent a major share of revenue, buyers will worry about what happens if one leaves. This is especially important if those customers are also tied to custom implementations.

Other common discount drivers include messy financial records, unclear revenue recognition, founder dependency, weak sales process, limited product differentiation, poor data security, and overreliance on a regulation that may change.

The good news is that many discount drivers can be improved before a sale. You may not change your whole business model in 6-12 months, but you can clean up reporting, separate revenue lines, reduce churn, document repeatable processes, and make the business easier for a buyer to trust.

7. Valuation Example: A Carbon Management Company

This example is fictional. The company, revenue level, and valuation ranges are illustrative and are designed to show how valuation logic works. This is not investment advice, a fairness opinion, or a formal valuation.

Imagine a fictional business called CarbonForge, a carbon management software company serving mid-sized manufacturers. It helps customers calculate product carbon footprints, manage Scope 1, Scope 2, and Scope 3 emissions data, prepare CSRD and CBAM-related reporting, and support customer sustainability requests from large enterprise buyers.

Assume CarbonForge has USD 10m of revenue. Most revenue is recurring software subscription revenue, with some implementation and data-cleaning services. The company is growing well, has strong gross margins, and is becoming embedded in manufacturing compliance workflows.

Step 1: Select the Relevant Multiples

The most relevant private market references are software-led compliance, regulatory, ESG, and environmental asset management companies. Those generally support a core revenue multiple range around 4.0x-5.5x for a strong but not extreme private company.

Services-led consulting references are less relevant if CarbonForge is truly software-first. Very high public market outliers are also less relevant because those often reflect much larger, broader, or unusual data franchises.

Step 2: Apply the Range

The discounted case could apply if CarbonForge has heavy services revenue, weak retention, unclear margins, limited product differentiation, or a lot of founder-led delivery.

The core case could apply if it has clear recurring software revenue, good growth, credible margins, and strong exposure to regulation-driven manufacturing use cases.

The premium case could apply if the company has very strong retention, high growth, high gross margins, deep manufacturing specialization, strong integrations, a clean management team, and several strategic buyers that see it as a missing product in their platform.

Step 3: What This Means for Founders

Two carbon management businesses with the same USD 10m revenue can be worth very different amounts. One may be worth USD 25m because it is mostly project-based advisory. Another may be worth USD 65m because it is recurring, embedded, compliance-critical software.

That is why valuation preparation matters. You are not just selling revenue. You are selling revenue quality, growth durability, buyer confidence, and strategic relevance.

8. Where Your Business Might Fit Self-Assessment Framework

Use this framework as a rough self-assessment. Score each factor from 0 to 2:

- 0 = weak or unclear

- 1 = decent but not proven

- 2 = strong and well evidenced

How to Interpret Your Score

Be honest. The goal is not to give yourself a flattering score. The goal is to identify which improvements could have the biggest valuation impact before you enter a sale process.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. A buyer process is not just a set of calls. You need clean numbers, a clear story, prepared materials, a buyer list, and answers to the questions buyers will ask. If you start before you are ready, you can lose leverage quickly.

The second mistake is hiding problems. Issues will surface in due diligence. If churn, margin pressure, customer concentration, data quality issues, or product limitations appear late in the process, buyers lose trust. Lost trust usually means a lower price, tougher terms, or no deal.

The third mistake is weak financial records. In carbon management, you should be able to separate recurring software revenue, implementation revenue, advisory revenue, pass-through revenue, and any carbon credit-related revenue. Buyers need to understand what they are valuing.

The fourth mistake is failing to show clear KPIs. You should track revenue growth, gross margin, retention, churn, recurring revenue, customer concentration, average contract value, implementation costs, and sales pipeline quality. If you do not track the business clearly, buyers will assume more risk.

The fifth mistake is not running a structured, competitive sale process. Research and market experience show that a structured process with an advisor can lead to meaningfully higher purchase prices, often cited around 25%, because more qualified buyers create better price discovery and stronger leverage.

The sixth mistake is revealing your target price too early. If you tell buyers you want USD 10m of enterprise value, many will anchor around that number and offer USD 10.1m or USD 10.2m. You may never learn what they would have paid in a competitive process.

Two sector-specific mistakes are also common. One is overstating the quality of carbon credit revenue without proving verification, permanence, additionality, and reputational safety. The other is presenting a services-heavy business as pure software when the numbers do not support it. Buyers will find the truth, so it is better to frame the business accurately and show the path toward more scalable revenue.

10. What Carbon Management Founders Can Do in 6-12 Months to Increase Valuation

Improve the Numbers

Start by cleaning up revenue categories. Separate software subscription, implementation, advisory, usage-based fees, and credit-related revenue. This helps buyers apply the right multiple to the right revenue.

Improve gross margin visibility. Show what it costs to serve customers, onboard them, support them, and renew them. If you can reduce manual delivery or standardize implementation, do it before going to market.

Focus on retention. Buyers care about whether customers stay, renew, and expand. Even modest improvements in churn, renewal rates, and expansion revenue can materially improve the valuation story.

Strengthen the Software Story

Document how your product is used every month, not just once a year. Show login activity, recurring workflows, reporting cycles, integrations, automated data collection, and audit trails.

Build proof that services support the software, rather than replacing it. For example, create standard onboarding packages, customer templates, data connectors, training modules, and implementation playbooks.

If you serve a specific vertical, make that obvious. For manufacturers, show product carbon footprint workflows, supplier data collection, factory-level emissions tracking, CBAM readiness, and customer reporting use cases.

Reduce Buyer Risk

Fix messy contracts where possible. Renew key customers, extend contract terms, reduce unusual terms, and document pricing clearly.

Reduce founder dependency. Buyers should see a team that can sell, deliver, support, and manage the business without every important decision going through you.

Prepare for diligence early. Gather financial statements, customer contracts, pipeline data, product metrics, security policies, employee information, and legal documents before buyers ask.

Build a Better Buyer Narrative

Map your buyer universe. Good buyers may include ESG software platforms, compliance software companies, energy management groups, industrial software companies, data providers, consulting firms, and private equity-backed platforms.

Create a clear strategic story for each buyer group. Do not just say, “We are a carbon management platform.” Explain how you help each buyer expand product coverage, cross-sell, enter a regulated workflow, or strengthen customer retention.

The strongest 6-12 month plan is not a total reinvention. It is a focused cleanup of the exact areas buyers use to justify higher or lower multiples.

11. How an AI-Native M&A Advisor Helps Soft CTA

A strong exit process depends on reaching the right buyers, creating competition, and telling the story in a way buyers understand. An AI-native M&A advisor like Eilla AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, sector focus, and likely synergies.

More relevant buyers usually means more competition, stronger offers, and a higher chance the deal actually closes. If one buyer slows down or drops out, a broad and well-qualified process gives you more options instead of forcing you to accept weaker terms.

AI can also speed up the early stages of the process. Buyer matching, outreach support, marketing material creation, and diligence preparation can help founders reach initial conversations and offers in under 6 weeks, instead of relying only on manual research and slow document preparation.

The best outcomes still require expert human judgment. Experienced M&A advisors bring credibility with acquirers, shape the deal narrative, prepare the numbers, manage negotiation tension, and help position your business in the most attractive but defensible way. The AI-native model is about combining expert advisory with better speed, reach, and process quality.

If you would like to understand how an AI-native process can support your exit, book a demo with one of Eilla AI’s expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.