The Complete Valuation Playbook for Healthcare Management Software Businesses

A data-driven guide to how healthcare management software businesses are valued abd what drives high multiples.

If you run a privately held Healthcare Management Software business and are thinking about a sale in the next 1-12 months, valuation should not be treated as a black box. In this market, the gap between an average outcome and a strong one can be very large - even for two businesses with similar revenue.

That is especially true now. Healthcare software is still a consolidation market, with repeat acquirers buying adjacent products, but buyers are also more selective than they were a few years ago. They want recurring revenue, sticky workflows, clean metrics, and a clear reason why your product matters inside a healthcare setting.

This playbook is built to help you understand what healthcare management software businesses actually sell for, what drives higher versus lower multiples, and what you can realistically do over the next 6-12 months to improve your valuation before going to market.

1. What Makes Healthcare Management Software Businesses Unique

Healthcare Management Software is not valued like generic software. Buyers are not just asking whether your product works - they are asking how deeply it sits inside care delivery, billing, scheduling, patient flow, documentation, or administrative operations, and how painful it would be for a customer to replace you.

This sector includes several distinct business types. Some businesses focus on ambulatory EMR and practice management for clinics, with scheduling, intake, patient records, payments, telehealth, and workflow tools. Others focus on hospital operations, such as referrals, care coordination, waitlists, case management, or specialist scheduling. Others sit in adjacent areas like patient engagement, clinical analytics, coding and revenue-cycle support, pharmacy workflow, or interoperability and data exchange.

That matters because not all revenue is valued the same way. A cloud-based, recurring software product that a clinic uses every day to run appointments and billing is usually more valuable than a healthcare business with heavy services, one-off implementation revenue, or lower software margin. Buyers tend to pay more for software that is embedded in daily workflow and harder to rip out.

Healthcare also has sector-specific risks that buyers always check. They will look at compliance, data security, product reliability, integration depth, clinical workflow fit, implementation burden, and whether you depend on a few key customers, payers, channels, or regulation-driven demand. In this sector, a small product issue can become a trust issue very quickly.

A final nuance: healthcare buyers care a lot about proof. Generic claims like "we integrate with everything" or "we improve outcomes" are not enough. Buyers want reference customers, retention data, real implementation history, and evidence that your software is truly embedded in the provider's workflow.

2. What Buyers Look For in a Healthcare Management Software Business

At the most basic level, buyers care about the same core things they care about in other software deals: revenue scale, growth, gross margin, EBITDA, customer retention, and how predictable future revenue looks. But in healthcare management software, they also care about where your product sits in the workflow and how hard it would be to replace.

A buyer will usually ask a few practical questions. Do customers rely on your product every day? Does it help run a mission-critical process like patient scheduling, charting, referrals, intake, coding, or care coordination? Does it connect into the rest of the healthcare stack in a way that would make switching disruptive? If the answer is yes, your valuation story gets stronger.

They also look closely at customer quality. A business with stable clinics, provider groups, hospitals, or care settings that renew consistently and expand over time will usually be valued better than a business with small, inconsistent customers, weak onboarding, and visible churn. In simple terms, buyers care about whether your customers stick around and pay more over time.

Another key lens is revenue mix. Buyers like recurring subscription revenue. They are less excited by a business where too much of the income comes from implementation projects, custom work, low-margin support, or founder-led selling that may not scale.

How private equity buyers think

Private equity buyers do not just ask, "What is this worth today?" They ask, "If we buy this now, what can it be worth in 3-7 years?" That means they think about entry multiple versus exit multiple, future growth, margin expansion, and who they can sell the business to later.

They will usually want a believable next buyer. That could be a larger strategic acquirer, a bigger private equity fund, or in rarer cases a public market path. If your business is too small, too founder-dependent, too niche, or too hard to integrate, that future buyer pool can shrink - and so does valuation.

They also think in terms of levers they can pull. Can they raise prices carefully? Cross-sell adjacent modules? Buy similar products and combine them? Improve sales discipline? Reduce duplicated costs after an acquisition? Businesses that clearly support these value-creation moves tend to attract stronger interest.

3. Deep Dive: Workflow Depth and Interoperability - Why These Matter So Much

In Healthcare Management Software, one of the biggest valuation questions is this: are you a useful tool, or are you part of the healthcare workflow that a customer cannot easily function without? That difference often has a major impact on how buyers view risk, retention, and strategic value.

The deal data points in this direction clearly. Premium outcomes are often associated with businesses that sit inside mission-critical workflows and have credible interoperability. In the source set, buyers repeatedly paid up for software that connected into EMR environments, referrals, scheduling, imaging, analytics, or provider operations in a way that made the product more embedded and harder to displace.

Why do buyers care so much? Because workflow depth usually means higher switching costs. If your software handles appointments, intake, patient communications, billing triggers, referral routing, or clinical workflows - and connects well with the surrounding systems - customers are much less likely to rip it out. That makes revenue more durable, which is one of the main things buyers pay for.

Interoperability also expands strategic value. A buyer is not only acquiring your current revenue. They may also be acquiring a product they can plug into a wider platform, distribute across existing customers, or use to deepen their position in a healthcare setting. That is why repeat acquirers in this market often pay stronger prices for strategically adjacent assets.

If your business looks more like a stand-alone tool today, the goal is not to reinvent the company overnight. It is to make your workflow relevance more provable. That can mean stronger integrations, cleaner product positioning, better reference customers, and clearer proof that your product affects a daily operational process rather than sitting on the edge of the stack.

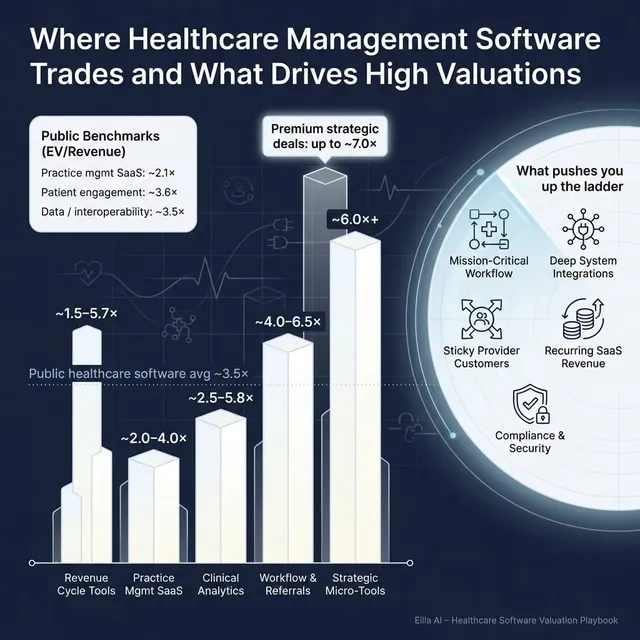

4. What Healthcare Management Software Businesses Sell For - and What Public Markets Show

Here is what the data actually shows. Private healthcare software deals can clear at much stronger multiples than many public healthcare technology names, but the spread is wide. That spread exists because buyers are paying for very different things: scale, profitability, workflow depth, strategic fit, and sometimes future upside embedded in earn-outs.

The right way to use this data is not to hunt for one magic number. It is to understand the range, then ask where your own business belongs within it.

4.1 Private Market Deals (Similar Acquisitions)

Across the precedent transactions provided, the overall average EV/Revenue multiple is 7.5x, but the median is much lower at 3.8x. That tells you immediately that the dataset includes some very high outliers and denominator effects from small-revenue deals. In practice, the middle of the private market is more useful than the average headline.

For businesses closest to ambulatory EMR, practice management, and provider workflow software, the deal data suggests that many credible software assets trade in roughly the 2.0x-6.0x revenue zone, with some higher outcomes for scarce assets, very small but strategic products, or deals where earn-outs bridge valuation expectations. EBITDA-backed businesses with solid margins can also trade on strong EBITDA multiples, often in the low-to-mid teens and sometimes above that when the asset is especially attractive.

A few patterns stand out. First, repeat consolidators show up again and again. That usually supports better prices because those buyers can underwrite synergies quickly. Second, many deals include earn-outs tied to ARR, revenue, or operating performance. That tells you buyers will stretch on valuation when upside can be shared, but some of the "premium" may be conditional rather than all cash at close. Third, very high EV/Revenue numbers on tiny revenue bases should be treated carefully - they may reflect strategic scarcity more than a broadly repeatable market multiple.

These ranges are illustrative, not a formal valuation. The same USD 10m revenue business could land in very different parts of this range depending on margin, retention, growth, interoperability, and how strategic it looks to the right buyer.

4.2 Public Companies

The public comp set is much more mixed than the private deal set. As of mid to late 2025, the overall public group in the source data trades at about 7.0x average EV/Revenue, but only 1.7x median EV/Revenue. Average EV/EBITDA is 27.4x and median EV/EBITDA is 11.9x. Again, that gap between average and median tells you outliers are pulling the averages up.

For founder use, the better approach is to look at the relevant clusters. Practice management and clinic operations software names in the dataset sit roughly around 0.7x-4.0x revenue. Patient engagement names are roughly around 1.2x-2.1x revenue in the more grounded examples, though a few outliers exist. Hospital-wide enterprise HIS and EMR names are spread broadly, with some lower-growth businesses trading around 1.0x-3.3x revenue and a few much higher outliers. Data and interoperability platforms are also wide, from sub-1.0x up to stronger premium cases where margin and strategic relevance are better.

* Based on limited profitable names in the sample.** Heavily influenced by outliers, so median-style interpretation is safer than simple average.

The practical lesson is simple. Public multiples are reference points, not a price tag for your company. Private businesses are usually smaller, less liquid, and riskier than public companies, so many founders should expect a discount to the strongest public names.

But the reverse can also happen. If your business is scarce, highly strategic, tightly integrated into provider workflow, and attractive to a repeat consolidator, a private buyer may pay above what a simple public comp screen would suggest. That is why positioning and buyer targeting matter so much.

5. What Drives High Valuations (Premium Valuation Drivers)

Higher valuations in this sector usually come from a combination of strong fundamentals and strategic fit. The data does not suggest that buyers simply pay more for "healthcare software" as a category. They pay more when the asset is clearly sticky, strategically useful, and easy to underwrite.

1) Mission-critical workflow position

Buyers pay more for software that sits in a daily, essential process. That includes products tied to scheduling, intake, patient flow, EMR-connected workflow, referrals, coding, imaging, or care coordination.

Why? Because the more central you are to operations, the lower the chance a customer churns casually. A product that helps run the clinic or hospital is worth more than a product that just sits beside it.

A founder-friendly example: software that sits between appointments, patient intake, billing triggers, and provider workflow is usually more valuable than a stand-alone reporting tool with occasional usage.

2) Proven interoperability, not just integration claims

The source data shows that interoperability is associated with premium outcomes when it is real and provable. Buyers like businesses that connect well with other systems because that broadens deployment options and raises switching costs.

The key is proof. Buyers want to see live interfaces, customer references, implementation history, and evidence that integrations help win deals or keep customers. Generic "we integrate with many systems" language is rarely enough.

3) Strong recurring revenue and retention

Even when not explicitly listed in every deal summary, this is a core driver in software M&A. Buyers want recurring revenue they can trust. They pay more when customers renew, stay for years, and add products over time.

In practical terms, a business with stable annual subscriptions, low churn, and visible expansion revenue will usually attract more interest than one with recurring revenue on paper but weak customer behavior underneath.

4) High EBITDA margins or a believable path to them

This is one of the clearest premium drivers in the dataset. Several better outcomes were linked to strong EBITDA margins or to purchase structures where price upside was tied directly to EBITDA performance.

Why buyers care is straightforward: good EBITDA means the business generates real cash, not just growth stories. That expands the buyer pool, because both strategic buyers and sponsor-backed buyers can underwrite the deal more confidently.

A simple example: a healthcare software business with clean recurring revenue and solid margins is much easier to finance and therefore more likely to attract competitive bids.

5) Strategic adjacency to repeat acquirers

Some of the strongest valuation support in the source data comes from repeat buyers building platforms through acquisitions. Those buyers are not just valuing the target as a stand-alone business. They are valuing the fit.

That can include cross-sell potential, faster market entry, a missing product module, a stronger position in a care setting, or the ability to sell your product into an existing installed base. If your company fills a clear gap for known acquirers, you may be worth more to them than to the market in general.

6) Earn-out terms that are well structured and controllable

Earn-outs are not automatically good, but in this sector they often help push headline valuation higher. Buyers use them when they believe in the upside but want protection against variability in retention, growth, or integration outcomes.

If the metrics are clear, controllable, and tightly defined, an earn-out can help bridge the gap between what you think the business is worth and what the buyer is willing to pay today.

7) Clean execution basics

Founders sometimes underestimate this. Buyers pay more when your numbers are clean, your customer cohorts make sense, your gross margin is credible, your contracts are organized, and your leadership bench is not just the founder.

Premium valuation is often the result of removing doubt. Clean financials, predictable reporting, diversified customers, and a management team that can operate after closing all help move you toward the top of the range.

6. Discount Drivers (What Lowers Multiples)

Most low-end outcomes are not caused by one dramatic flaw. They usually happen because buyers see too much uncertainty and not enough proof. The more questions a buyer has to answer for themselves, the lower the multiple they are likely to offer.

One common discount driver is a weak recurring revenue profile. If too much of your revenue comes from services, customization, implementation, or non-repeatable projects, buyers will usually treat the business as less software-like and apply lower revenue multiples.

Another is shallow product embedding. If your software is useful but not mission-critical, or if customers can replace it without much disruption, your retention risk looks higher. In healthcare, that usually means buyers will be more cautious.

Low or inconsistent profitability also hurts. The source data shows that higher-margin businesses and businesses with EBITDA-based earn-out structures tend to be easier to support at stronger valuations. If your margins are weak and there is no believable path to improvement, buyers may question payback and lower their bid.

Customer concentration can be a serious issue. If a few clinics, provider groups, hospital systems, channels, or partners account for too much of your revenue, the business becomes riskier. The same is true if sales depend too heavily on one founder relationship or a narrow referral source.

Buyers also discount vague interoperability claims. In this sector, saying you are integrated is not the same as proving it. If interfaces are fragile, implementation takes too long, or customers do not view the integrations as valuable, the buyer may see less stickiness than your marketing suggests.

Finally, beware of optics-driven valuation arguments. Some tiny healthcare software deals show very high EV/Revenue multiples, but those can be misleading when revenue is very small. Sophisticated buyers will look past the headline number and focus on customer behavior, margins, growth quality, and strategic fit.

7. Valuation Example: A Healthcare Management Software Company

Let’s make this concrete with a fictional business. Assume a company called CareFlow Pro - a fictional Healthcare Management Software company with USD 10m of annual revenue. It sells subscription software to outpatient clinics and specialist groups, combining scheduling, intake, patient communications, provider workflow, and payments support. This example is illustrative only - it is not investment advice or a formal valuation.

Step 1: Start with the right comp set

The first step is to compare CareFlow Pro to the right businesses. It is best matched to practice management, clinic operations, ambulatory workflow, and patient-facing software - not to hospital-wide HIS platforms and not to services-heavy provider enablement businesses.

The source data suggests a sensible logic path:

- relevant public practice and engagement names often cluster around roughly 1.0x-4.0x revenue, with some stronger examples around the upper end

- relevant private ambulatory EMR and practice management deals span a much wider range, roughly around 2.2x-10.4x revenue

- because CareFlow Pro is a private company at USD 10m revenue, you would not usually jump straight to the top end of the private range unless growth, margins, retention, and strategic fit were exceptional

That is why a core range of roughly 3.0x-5.5x revenue is a defensible starting point for a credible private Healthcare Management Software business of this type.

Step 2: Apply the multiple to the fictional company

Assume CareFlow Pro has:

- USD 10m revenue

- high recurring revenue

- good gross margin

- decent but not perfect EBITDA

- strong clinic workflow relevance

- real integrations

- no extreme concentration risk

That could support a core valuation range like this:

Step 3: Understand why the range changes

A discounted case might apply if growth is slowing, services mix is high, retention is not well proven, EBITDA is weak, or integrations are more marketing story than customer reality. Two businesses with the same revenue can be valued very differently if one looks replaceable and the other looks deeply embedded.

The core range of USD 30-55m fits a solid private software business that is clearly in the healthcare management software lane, has recurring revenue, and has enough proof points to justify trading above weaker public references but below the most aggressive private outliers.

A premium case could be justified if CareFlow Pro had several strong drivers at once: excellent retention, high margins, low churn, clear interoperability proof, strong cross-sell potential, and obvious strategic value to a repeat consolidator. In that case, the buyer may pay for both the stand-alone business and the platform fit.

The founder lesson is simple: valuation is not just about revenue size. It is about what kind of revenue you have, how durable it looks, and how clearly a buyer can underwrite your future.

8. Where Your Business Might Fit (Self-Assessment Framework)

A useful way to assess your likely valuation band is to score the business honestly across a few factors. Give yourself a 0, 1, or 2 on each line. A 0 means weak, 1 means acceptable, and 2 means strong.

How to interpret your score

If you score near the top of the range, you are more likely to sit toward premium valuation territory. That does not guarantee a premium price, but it usually means buyers can tell a stronger story about durability, strategic fit, and future upside.

If you score in the middle, you are probably in fair-market territory. That is where many good businesses sit. In that case, process quality, buyer targeting, and narrative can still make a big difference.

If you score toward the low end, that does not mean your business is unsellable. It usually means the market will price in more risk. The good news is that many of these issues can be improved in the next 6-12 months if you focus on the highest-payoff fixes.

9. Common Mistakes That Could Reduce Valuation

One of the biggest mistakes is rushing the sale. Founders often decide to sell, send out a few materials, and hope the market rewards them. But if your numbers are not ready, your story is fuzzy, and your buyer list is too narrow, you are giving away leverage before the process even starts.

Another major mistake is hiding problems. In healthcare software deals, issues always come out in diligence - churn, implementation failures, weak integrations, concentration, compliance gaps, messy reporting. If buyers discover problems late that should have been disclosed earlier, trust falls and value usually falls with it.

Weak financial records are another avoidable discount. If you cannot clearly show recurring versus non-recurring revenue, software versus services gross margin, cohort behavior, or true EBITDA normalization, buyers will fill in the gaps conservatively. In many cases, 6-12 months is enough time to improve revenue recognition, reporting clarity, KPI tracking, and margin visibility.

A very costly mistake is running an unstructured sale process. A competitive process with an experienced advisor typically creates more tension between buyers, improves positioning, and often leads to meaningfully higher purchase prices. In M&A, the best price usually comes from competition and preparation, not from taking the first decent inbound call.

Another common error is telling buyers the price you want too early. That kills price discovery. If you say you want USD 10m of value, many buyers will simply come back at USD 10.1m or USD 10.2m instead of telling you what they may really have paid in a competitive process.

There are also healthcare-specific mistakes. One is overstating interoperability when the integrations are shallow or hard to maintain. Buyers in this sector know how to test that claim. Another is failing to separate software from services economics. If implementation and support are dragging margins down, you need to show buyers the real software engine underneath.

10. What Healthcare Management Software Founders Can Do in 6-12 Months to Increase Valuation

The best pre-sale work is usually not a dramatic pivot. It is a focused effort to make the business more understandable, more durable, and easier for buyers to underwrite.

Improve the numbers

Start by cleaning up your revenue and margin reporting. Separate recurring software revenue from implementation, training, and services. Track gross margin by revenue type. Show renewal behavior clearly. If possible, improve EBITDA by removing avoidable inefficiencies and low-value custom work.

If churn is a problem, attack it directly. Review onboarding, customer support, pricing, contract structure, and product friction. In this sector, even a modest improvement in retention can materially improve how buyers see durability.

Strengthen product stickiness

Deepen your role in the workflow. That does not mean building ten new modules. It means making your current product more essential. Focus on the features, integrations, and usage patterns that customers rely on daily.

Document your interoperability properly. List live integrations, implementation timelines, customer references, and real workflow outcomes. Buyers reward proof, not broad claims.

Reduce obvious risk

Diversify concentration where possible. If too much revenue sits with a few customers, one channel partner, or one founder-led sales relationship, start reducing that dependence now. A broader customer base usually leads to a better valuation story.

Also tighten the basics: contracts, security processes, compliance documentation, customer success reporting, and leadership ownership beyond the founder. Buyers pay more when they feel the business can perform after closing without heroic founder involvement.

Build a sharper market narrative

Founders often describe their business too broadly. Before a sale, sharpen the positioning. Are you really a practice management platform? A provider workflow software company? A care coordination tool? A patient access platform? Clear positioning helps the right buyers understand why they should care.

Map the likely acquirer universe. Which strategic buyers are already buying nearby assets? Which sponsor-backed platforms are building in adjacent areas? If you can show a clear fit with known acquirer strategies, you improve your odds of a premium outcome.

Prepare for a competitive process

Get your materials ready before you launch. That includes clean historical numbers, a strong growth story, customer metrics, product proof points, and a clear explanation of why the business matters in healthcare workflow.

A well-run process does not just create more buyer conversations. It creates better buyer behavior. That is often where the real valuation lift comes from.

11. How an AI-Native M&A Advisor Helps

Selling a Healthcare Management Software business is partly about valuation, but it is also about process design. The broader and more relevant your buyer universe is, the better your odds of creating competition, improving terms, and keeping optionality if one buyer drops out. An AI-native advisor can expand that buyer universe to hundreds of qualified acquirers based on deal history, synergies, financial capacity, and other signals - which means more relevant outreach, stronger competitive tension, and a higher chance the deal actually closes.

Speed matters too. With AI-driven buyer matching, faster creation of process materials, and more efficient support during diligence, initial conversations and offers can often be reached much faster than in a manual-only process. In many cases, that means getting to first offers in under 6 weeks rather than letting momentum fade.

The point is not replacing human advice. The point is combining expert human M&A advisors with AI that makes the process broader, faster, and more precise. That gives you Wall Street-grade advisory quality - strong materials, stronger buyer positioning, and sharper deal framing - without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.