The Complete Valuation Playbook for Engineering Consulting Businesses

A data-driven guide to how engineering consulting businesses are valued and what drives high multiples.

If you run an engineering consulting business and are thinking about selling in the next 1-12 months, valuation will probably feel more confusing than it should. You may hear that infrastructure, energy transition, sustainability, digital engineering, and public-sector investment are all attractive themes. That is true. But buyers do not pay high multiples just because a company sits near attractive themes.

Engineering consulting is also a fragmented market, which means strategic buyers and private equity-backed groups are still looking for high-quality firms they can add to larger platforms. At the same time, buyers are disciplined. They are looking closely at margins, project risk, customer concentration, backlog, and whether the business can grow without the founder personally driving every major client relationship.

This playbook shows what engineering consulting businesses actually sell for, what separates higher-value firms from lower-value firms, and how you can assess where your business might sit before going to market.

1. What Makes Engineering Consulting Unique

Engineering consulting businesses are different from many other service companies because they sell expertise, trust, and technical judgment. The work often sits inside high-stakes projects: buildings, infrastructure, transport, utilities, energy assets, environmental projects, industrial facilities, data centers, and public-sector programs.

The main types of businesses in this market include:

A key valuation issue is that engineering consulting firms are usually people-heavy businesses. Buyers are not just buying revenue. They are buying the ability of your team to keep winning and delivering work after you sell.

That creates a different risk profile from software or product businesses. Revenue can be lumpy. Projects can be delayed. Margins can move quickly if a project is underpriced or badly scoped. A few senior engineers or client relationships may carry a large share of the firm's value.

Buyers will always check a few sector-specific risks: whether your backlog is real, whether your contracts protect you from scope creep, whether your professional liability exposure is under control, whether your revenue depends on one or two large projects, and whether your senior technical team is likely to stay.

2. What Buyers Look For in an Engineering Consulting Business

Buyers start with the obvious items: revenue scale, growth, profitability, cash generation, customer concentration, and the quality of the management team. But in engineering consulting, they quickly go deeper.

They want to understand where your work sits in the project lifecycle. Early-stage advisory, feasibility, design, detailed engineering, supervision, testing, and project management can all carry different margins and risk levels. A firm that gets called in early and stays involved across multiple stages of a project is usually more attractive than one that only competes for narrow, one-off assignments.

They also look at how specialized your expertise is. General engineering capability is valuable, but it is not always scarce. A firm with a recognized position in regulated, complex, or business-critical environments can attract more buyer interest because it is harder to replace.

Recurring or repeat work matters, even if you do not have "subscription revenue" in the software sense. Buyers like to see framework agreements, preferred supplier status, multi-year public-sector programs, long-standing utility relationships, repeat private developer clients, and maintenance or monitoring work that comes back each year.

How private equity buyers think

Private equity buyers usually ask a simple question: "If we buy this business today, who will want to buy it from us in 3-7 years, and why?"

That means they care about the entry multiple and the exit multiple. If they buy your firm at a certain valuation today, they need to believe they can make it bigger, less risky, more profitable, and more attractive to a future buyer.

They will look for levers such as:

- Increasing prices where your work is underpriced.

- Improving project margin tracking.

- Cross-selling into a larger customer base.

- Adding smaller specialist firms.

- Reducing founder dependence.

- Creating a stronger second layer of leadership.

- Professionalizing sales, finance, and delivery processes.

A private equity buyer does not need your business to be perfect. But they do need a believable plan for how the company becomes more valuable under their ownership.

3. Deep Dive: Why EBITDA Quality Matters More Than Revenue Alone

In engineering consulting, revenue can be misleading. Two firms can both have USD 10m of revenue, but one may be worth far more because it turns more of that revenue into dependable profit.

The source data makes this clear. Traditional consulting-led engineering firms and built environment advisory businesses often trade at modest revenue multiples. The market does not automatically award a premium just because a firm is multidisciplinary, well-established, or technically credible. Those traits help, but they are not enough on their own.

Buyers care about EBITDA because it shows how much cash profit the business produces before financing and tax effects. In simple terms: if revenue is the size of the engine, EBITDA shows how much useful power the engine actually produces.

For engineering consulting firms, EBITDA quality depends on several practical things: pricing discipline, utilization of technical staff, project scoping, change-order management, subcontractor use, senior staff leverage, and how much time the founder spends on non-billable client management.

A business with 8-12 percent EBITDA margins, clean project controls, and repeat clients can feel much safer to a buyer than a business with the same revenue but volatile project profits. Buyers will often pay more for the first business because they believe the earnings will continue after closing.

If your business looks more like the left column today, you do not need to transform the whole company in 6 months. But you can start moving toward the right column by tracking project margin more clearly, documenting repeat revenue, reducing founder dependence, and proving that recent profits are sustainable.

4. What Engineering Consulting Businesses Sell For - and What Public Markets Show

The valuation data points to one clear message: engineering consulting businesses usually trade at modest revenue multiples, and buyers pay more when earnings quality, strategic fit, and scarcity are clear.

Revenue multiples are useful, but they should not be read in isolation. A low-margin firm may look expensive at 0.8x revenue, while a high-margin firm may look fair or even attractive at the same revenue multiple. EBITDA multiples often tell the better story.

4.1 Private Market Deals - Similar Acquisitions

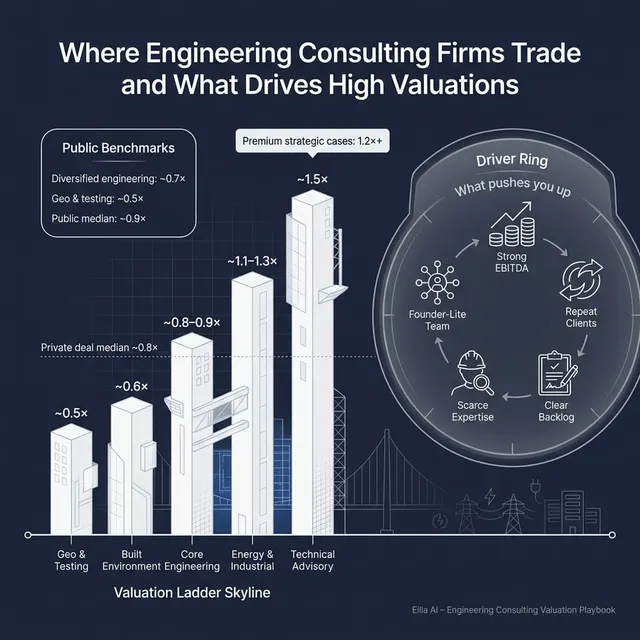

The private transaction data shows an overall average EV/Revenue multiple of around 0.9x and a median of around 0.8x. On EBITDA, the overall average was around 6.8x and the median was around 5.7x.

Built environment engineering consultancy and design services sat lower, at around 0.6x revenue and about 6.2x EBITDA. Energy, utilities, and industrial engineering services were higher on revenue, with an average around 1.3x and median around 1.1x, but still around 5.2x EBITDA. Civil construction and infrastructure contractors averaged around 0.6x revenue and about 7.9x EBITDA.

For founders, the practical takeaway is that a traditional engineering consultancy should not assume software-style revenue multiples. A credible range for many privately held engineering consulting firms may sit around 0.5x-1.0x revenue, with stronger outcomes possible when the firm has high margins, scarce expertise, repeat work, and clear strategic buyer interest.

The data also shows that headline deal value can be misleading. Some transactions include deferred payments or earn-outs, meaning part of the price is only paid if future performance targets are hit. That usually means the buyer likes the upside, but still sees risk.

4.2 Public Companies

The public market data provides a broader reference point as of the 2025 data set. These are larger, more liquid companies than most private founder-owned firms, so their multiples should not be copied directly. But they help frame how investors value different parts of the market.

The overall public company set showed average EV/Revenue of around 1.6x and median EV/Revenue of around 0.9x. Average EV/EBITDA was around 25.5x, but the median was much lower at around 9.6x. That gap tells you there are outliers in the data, so founders should pay more attention to medians and relevant segments than broad averages.

The technical advisory category shows the highest public multiples, but founders should be careful. That segment appears to include outliers and companies with different scale, market position, and possibly different growth or margin profiles. It is not automatically comparable to a private engineering consultancy with USD 5m-30m of revenue.

The most relevant public reference points for many founder-owned engineering consulting businesses are the diversified engineering consultancy and geotechnical/testing categories. Those sit much closer to 0.5x-0.7x revenue and 4x-9x EBITDA.

Use public multiples as reference bands, not price tags. A smaller private business usually deserves a discount for scale, liquidity, customer concentration, founder dependence, and reporting quality. But a rare, highly strategic firm with strong margins, repeat work, and scarce expertise can sometimes push above the ordinary private-market range.

5. What Drives High Valuations - Premium Valuation Drivers

Higher valuations usually come from a combination of strategic fit and financial proof. Buyers may be excited by your market, but they will pay more only when that excitement is supported by numbers, contracts, and low risk.

5.1 Strong EBITDA conversion

The clearest premium driver in the data is not simply technical breadth. It is visible, reliable profit.

Buyers pay more when they can see that your revenue converts into EBITDA without constant heroics from the founder. That means project margins are stable, staff utilization is well managed, and pricing reflects the value of your expertise.

Practical examples include:

- You know which project types make money and which do not.

- You track margin by project manager, customer, and service line.

- You have reduced low-margin legacy work before going to market.

5.2 Exposure to complex or regulated end markets

Buyers like firms that serve technically demanding markets because those markets often have higher barriers to entry. Examples include energy infrastructure, power systems, utilities, data centers, transport infrastructure, regulated industrial facilities, environmental compliance, and marine or offshore assets.

This does not guarantee a high multiple. The data shows that complex end-market exposure alone is not enough. But it strengthens the buyer story if it comes with strong margins, repeat customers, and hard-to-replace technical knowledge.

5.3 Repeat client relationships and framework agreements

Engineering consulting may be project-based, but buyers still want predictability. A firm with a deep base of repeat customers is less risky than one that starts from zero every year.

Repeat work can come from public-sector frameworks, utility programs, preferred supplier arrangements, long-standing developer relationships, energy client master service agreements, or annual monitoring and inspection work.

The more you can prove that customers come back without the founder personally chasing every project, the more confident buyers become.

5.4 Strategic fit with an acquirer

A buyer may pay more if your business fills a clear gap in their platform. That could be geography, customer access, technical capability, sector exposure, or a leadership team they can build around.

Strategic fit is especially powerful when the buyer can see quick earnings impact. For example, they may believe they can cross-sell your services to their customers, use your team to win larger projects, or add your expertise to a national platform.

But strategic fit needs evidence. A buyer will not pay more just because a slide says there are synergies. They need to see real client overlap, real cross-sell opportunities, and a practical integration plan.

5.5 Clean financials and professional reporting

Clean numbers create confidence. Messy numbers create discounts.

Buyers want to understand revenue by service line, margin by project, backlog, utilization, working capital, customer concentration, subcontractor spend, and owner adjustments. If those numbers are clean, the process moves faster and buyers are less likely to reduce price during due diligence.

This is especially important in engineering consulting because project accounting can get complicated. If your financials do not clearly show which work is profitable, buyers will assume more risk.

5.6 A leadership bench beyond the founder

A founder-led business can still be highly valuable, but buyer concern rises when the founder owns the client relationships, pricing decisions, recruitment, quality control, and technical reputation.

A stronger profile has capable leaders under the founder: commercial leads, discipline heads, project directors, finance leadership, and client owners who can stay after the sale.

Buyers pay for businesses that can survive the founder's reduced role.

6. Discount Drivers - What Lowers Multiples

Discounts usually come from risk. The buyer may still like the business, but if they are unsure whether revenue and EBITDA will continue, they will lower the multiple or push more of the price into an earn-out.

The first major discount driver is weak or volatile profitability. If EBITDA moves sharply year to year, buyers will ask whether the latest profit level is sustainable. If project margin is hard to explain, they will assume some of the earnings are at risk.

The second is customer or project concentration. A firm with one major client, one major framework, or one large project making up a large share of revenue will usually receive more cautious offers. Buyers worry about what happens if that work disappears after closing.

The third is founder dependence. If customers buy because of you personally, buyers may worry that value walks out the door when you step back. This can lead to lower upfront value, longer transition requirements, or performance-linked payments.

Other common discount drivers include:

A lower multiple does not always mean a bad business. Sometimes it means the business is not ready to sell yet. Many discount drivers can be reduced in 6-12 months with focused preparation.

7. Valuation Example: A Fictional Engineering Consulting Company

Let us apply the logic to a fictional company called Northbridge Engineering Partners.

Northbridge is a privately held, multidisciplinary engineering consulting firm with USD 10m of fictional revenue. It works mainly in built environment, civil infrastructure, and geotechnical advisory. It has a 40-person team, a 25-year operating history, repeat developer and public-sector clients, and modest but improving profitability.

This company is fictional. The revenue level is fictional. The valuation ranges below are illustrative only and are designed to show how the logic works. This is not investment advice, a fairness opinion, or a formal valuation.

Step 1: Select the relevant valuation reference points

For Northbridge, the most relevant private-market references are built environment engineering consulting deals and nearby geotechnical or infrastructure consulting businesses. Those references generally point to revenue multiples around 0.5x-0.9x, with built environment consulting around 0.6x in the grouped data.

The public-market references also support a cautious range. Diversified engineering consultancies trade around 0.7x revenue in the public data, while geotechnical and testing specialists sit closer to 0.5x revenue. Technical advisory companies can show higher multiples, but that group is less directly comparable unless the company has unusual scale, margins, scarcity, or strategic relevance.

So for a traditional engineering consulting firm like Northbridge, a defensible core range may be 0.6x-0.9x revenue.

Step 2: Apply the range to USD 10m of revenue

The core case assumes Northbridge is a solid, traditional engineering consulting business with credible clients, reasonable margins, and no major red flags. The range lines up with private built environment consulting evidence and public diversified engineering consulting reference points.

The strong case may apply if Northbridge has higher EBITDA margins, low customer concentration, clear backlog, repeat public-sector frameworks, and a management team that can run the business without the founder.

The premium strategic case is harder to justify, but possible if the company has scarce expertise in a highly attractive end market, such as critical infrastructure, energy transition, data centers, environmental compliance, or regulated industrial assets. Even then, the premium must be supported by earnings, not just a good story.

Step 3: What this means for founders

Two engineering consulting firms with the same USD 10m of revenue can have very different valuations.

One may be worth closer to USD 5m if margins are weak, reporting is messy, clients are concentrated, and the founder owns the relationships. Another may be worth USD 10m or more if it has strong EBITDA, repeat revenue, clean financials, a capable leadership team, and scarce technical expertise.

That is why valuation preparation matters. You may not be able to double revenue in 6-12 months, but you may be able to materially improve how buyers perceive the quality and durability of that revenue.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a practical self-check before starting a sale process. Score each factor from 0 to 2.

- 0 means weak or not proven.

- 1 means acceptable but not a strength.

- 2 means strong and well documented.

A simple interpretation:

This framework will not tell you the exact value of your business. It helps you identify where your biggest valuation gaps are.

If your score is low because of customer concentration or weak financial reporting, those issues should be addressed before a sale. If your score is already strong, your focus should be on proving the story clearly to buyers and creating a competitive process.

9. Common Mistakes That Could Reduce Valuation

The biggest mistake is rushing the sale. Many founders go to market before their numbers, story, leadership team, and buyer list are ready. That usually gives buyers more reasons to hesitate, ask for discounts, or push price into deferred consideration.

The second mistake is hiding problems. If you have a margin issue, customer loss, contract dispute, staff retention risk, or accounting weakness, it will usually surface in due diligence. Hiding it destroys trust. A better approach is to explain the issue clearly, show what caused it, and show what you have done to fix it.

The third mistake is weak financial records. Engineering consulting firms need clean reporting around revenue, gross margin, EBITDA, backlog, utilization, customer concentration, and project profitability. If buyers cannot understand the economics, they will not give you full credit for them.

Another major mistake is not running a structured, competitive sale process with an advisor. M&A research and deal experience show that a well-run competitive process with an advisor can lead to meaningfully higher purchase prices, often referenced around 25 percent higher than less structured approaches. The logic is simple: when multiple serious buyers are competing, each buyer has to show its best hand.

Founders also reduce valuation by revealing the price they want too early. If you tell buyers you are looking for USD 10m of enterprise value, many buyers will anchor near that number. You may get USD 10.1m or USD 10.2m offers instead of discovering what the market might really pay. Let the market come back with offers first.

Industry-specific mistakes include underestimating project liability risk and failing to explain backlog quality. A buyer will want to know not only how much backlog you have, but how profitable and deliverable it is. A large backlog of low-margin or risky work may be less valuable than a smaller backlog of well-priced repeat client work.

10. What Engineering Consulting Founders Can Do in 6-12 Months to Increase Valuation

You do not need to reinvent the business before a sale. The goal is to remove buyer doubts and highlight the value that already exists.

Improve the numbers

Start with project profitability. Identify which service lines, clients, project managers, and contract types produce the best margins. Stop chasing work that creates revenue but little profit.

Clean up monthly reporting. Buyers should be able to see revenue, gross margin, EBITDA, backlog, utilization, customer concentration, and working capital without confusion. If your numbers require long explanations, fix them before buyers see them.

Review pricing. Many engineering consulting firms are underpriced because they have historically won work through relationships, not pricing discipline. Even modest fee increases on new work can improve EBITDA and buyer confidence.

Reduce risk

Document backlog clearly. Separate signed work from verbal expectations. Show timing, margin expectations, customer names, and delivery risk.

Reduce customer concentration where possible. You may not be able to replace a major customer in 6 months, but you can build a clearer plan for expanding other accounts and winning new repeat clients.

Strengthen the leadership bench. Buyers want to see that discipline leads, project directors, and commercial leaders can run the company after closing. If the founder is still the only true decision-maker, that will hurt valuation.

Improve the buyer story

Create a clear sector narrative. Do not just say you are a multidisciplinary engineering firm. Explain where you are strongest: infrastructure, geotechnical, energy, public-sector frameworks, regulated sites, sustainability, data centers, or complex built environment work.

Prove repeatability. Show repeat clients, multi-year relationships, framework agreements, renewal history, and examples where one project led to more work.

Prepare evidence for premium drivers. If you claim technical scarcity, show certifications, case studies, hard-to-win projects, expert staff, and customer references. If you claim strong margins, show project-level proof.

Prepare for due diligence early

Organize contracts, insurance policies, claims history, employee records, customer agreements, lease obligations, and project documentation. A clean data room creates confidence and keeps the process moving.

Review professional liability exposure. Buyers in this sector will care deeply about claims, warranties, indemnities, insurance limits, and project risk.

Prepare management for buyer meetings. The best meetings are not founder monologues. They show that the wider team understands customers, projects, margins, hiring, and growth.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can help you reach a broader and more relevant buyer universe. Instead of relying only on the obvious local buyers, AI can identify hundreds of qualified acquirers based on deal history, sector fit, financial capacity, geography, strategic gaps, and likely synergies. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal closes even if one buyer drops out.

AI can also speed up the early stages of the process. Buyer matching, outreach preparation, marketing materials, financial analysis, and due diligence support can all move faster when technology is built into the workflow. That can help founders reach initial conversations and offers in under 6 weeks, depending on readiness and buyer response.

The best process still needs expert human judgment. Experienced M&A advisors know how to frame the story, challenge buyer assumptions, protect price discovery, and manage tension in negotiations. AI enhances that work by making the process broader, faster, and more data-driven.

For engineering consulting founders, the right outcome is not just finding a buyer. It is finding the right buyer, creating competition, presenting the business professionally, and protecting value through diligence and negotiation. If you would like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.