The Complete Valuation Playbook for Contract Lifecycle Management Businesses

A practical breakdown of how CLM Software businesses are valued and what drives high multiples

Contract Lifecycle Management, or CLM, has moved from “legal department software” to a broader operating system for agreements. Contracts now touch sales, procurement, finance, HR, risk, compliance, and customer success. That makes the category more strategic, but also more complex to value.

This is an important time to understand valuation because buyers are actively looking at agreement automation, AI-driven contract review, e-signature workflows, document intelligence, and regulated workflow software. At the same time, they are more careful than they were during the peak SaaS market. Growth still matters, but so do margins, retention, clean revenue quality, and a credible path to profitability.

This playbook shows what CLM and adjacent workflow software businesses actually sell for, what public markets suggest, why some companies receive premium interest, why others get discounted, and what you can do in the next 6-12 months to improve your position before a sale.

1. What Makes Contract Lifecycle Management Unique

CLM businesses are different from general SaaS companies because they sit inside legally and commercially important workflows. Your product is not just another productivity tool. It helps customers create, approve, negotiate, sign, store, search, monitor, and analyze agreements that define revenue, cost, obligations, risk, and compliance.

The sector includes several types of companies:

What makes valuation unique is that CLM can be either a narrow tool or a mission-critical system. A simple contract repository with reminders is valuable, but it may not command a high multiple. A platform that controls the full contracting workflow, integrates with Salesforce, Microsoft, procurement tools, enterprise resource planning systems, and e-signature providers, and turns contracts into usable data can be much more strategic.

Buyers will always check several risks. They will look at whether customers really use the platform across departments, whether the product is hard to replace, whether AI features are accurate enough for legal workflows, whether implementation is too services-heavy, and whether revenue is truly recurring. They will also test whether your product is a “nice-to-have” legal tool or a workflow system that customers would struggle to remove.

2. What Buyers Look For in a Contract Lifecycle Management Business

Buyers usually start with the basics: revenue size, revenue growth, gross margin, EBITDA margin, customer retention, customer concentration, and how much revenue is subscription-based. In CLM, those basics matter a lot because the category has both high-quality SaaS businesses and more implementation-heavy workflow businesses.

A strong CLM business usually has predictable annual subscriptions, high gross margins, good renewal rates, and expanding customer accounts. Expansion matters because CLM often starts in one team and spreads. A customer might begin with legal intake, then add procurement contracting, sales contracting, obligation tracking, e-signature, or contract analytics.

Buyers also care about integrations. A CLM product that connects deeply with CRM, procurement, document management, e-signature, finance, and identity systems is harder to replace. If your software becomes part of how deals get closed or how vendors get approved, it becomes more valuable.

They will also look at your customer profile. Enterprise customers can support higher contract values and better expansion, but they may require longer sales cycles and heavier implementation. Mid-market customers can be attractive if the product is easy to deploy and churn is low. Small business customers can work if the model is efficient, self-serve, and low-touch.

How private equity buyers think

Private equity buyers think in terms of entry price, improvement plan, and future exit options. They ask: “If we buy this company today, who could buy it from us in 3-7 years, and at what multiple?”

They also think about what levers they can pull. In CLM, those levers often include increasing prices, improving packaging, adding AI review modules, improving customer success, reducing churn, cross-selling into adjacent workflows, and acquiring smaller tools to build a broader platform.

A private equity buyer will usually pay more if they can clearly see a path from “good software business” to “larger, more strategic platform.” They will pay less if the company needs major product rebuilds, has weak financial records, depends too much on founder-led sales, or requires too much custom services work to win each customer.

3. Deep Dive: Why Workflow Depth and Contract Intelligence Matter So Much

The most important valuation question in CLM is not just “Do you manage contracts?” It is “How deeply do you control the agreement workflow, and how much useful data do you extract from it?”

This matters because the market is crowded. Many tools can store contracts, send renewal reminders, and support basic templates. Fewer tools become the central workflow for legal, sales, procurement, finance, and operations. Even fewer can turn contract language into structured data that helps customers reduce risk, find savings, speed up revenue, and manage obligations.

The data points in the source set show premium interest around AI-powered CLM, contract intelligence, agreement automation, contract collaboration, legal workflow automation, e-signatures, identity, and regulated document workflows. That does not mean “AI” alone creates value. Buyers have become more skeptical of surface-level AI features. What they value is AI that improves a real workflow: faster review, better risk scoring, cleaner clause extraction, easier search, better playbook compliance, and more reliable obligation tracking.

For founders, the practical question is whether your product is used after the contract is signed. A company that only helps create or sign agreements may still be valuable. But a company that helps customers manage renewal dates, obligations, pricing terms, compliance risk, vendor commitments, and revenue leakage can make a stronger strategic case.

If your business looks more like the left column today, the goal is not to rebuild the whole company in 6 months. The goal is to prove movement. Add better reporting, deepen one or two critical integrations, show that more departments are using the platform, and track measurable customer outcomes like faster approval times, fewer missed renewals, or higher compliance with legal playbooks.

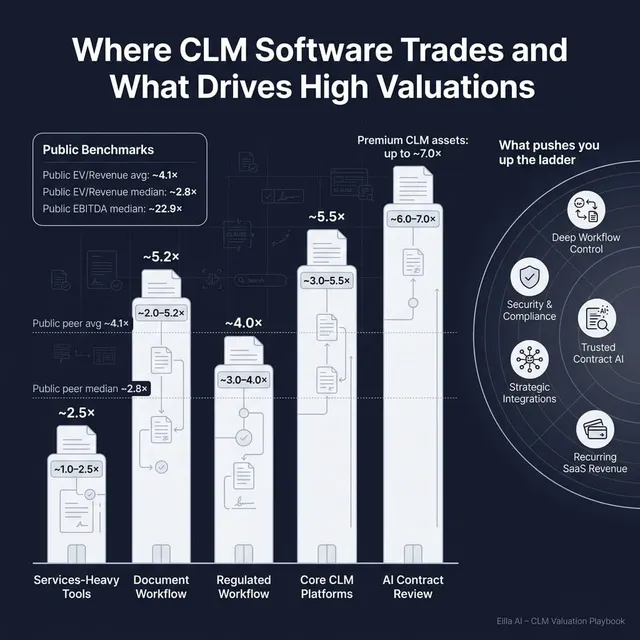

4. What Contract Lifecycle Management Businesses Sell For - and What Public Markets Show

Valuation in CLM is usually framed around revenue multiples, especially for SaaS businesses that are growing but not yet highly profitable. EBITDA multiples become more important when the business is mature, profitable, and has stable margins.

The data shows a wide range because the category includes pure SaaS, e-signature, legaltech, workflow automation, document management, RegTech, and services-heavy workflow businesses. Founders should not treat any single number as “the market.” The right multiple depends on your growth, margins, retention, product depth, customer base, and strategic relevance.

4.1 Private Market Deals - Similar Acquisitions

The private transaction set shows an overall average EV/Revenue multiple of about 3.6x and a median of about 2.9x. The overall average EV/EBITDA multiple is about 17.7x, with the median also around 17.7x. These are helpful reference points, but the spread is more important than the average.

Private deals in document workflow, collaboration, transaction management, regulated case management, HR process automation, and construction workflow software show that multiples can vary sharply. Lower-quality or less strategic workflow businesses can trade near or below 2.0x revenue. More strategic, recurring, workflow-heavy software assets can move into the 3.0x-5.0x+ range. Some assets with strong recurring revenue, high gross margins, and clear strategic buyer logic can go higher.

The practical takeaway is simple: the headline “CLM multiple” is not enough. A buyer will ask whether you are a true software platform, whether revenue is recurring, whether customers expand, and whether your workflow is important enough that a strategic buyer can justify paying above the market average.

4.2 Public Companies

Public companies provide a useful reference band, but they are not a direct price tag for private companies. Public companies are often larger, more liquid, more diversified, and better known. Smaller private companies are usually adjusted down for scale, customer concentration, management depth, and execution risk.

As of the mid to end of 2025 data in the sources, the broader public peer set shows an average EV/Revenue multiple of about 4.1x and a median of about 2.8x. The average EV/EBITDA multiple is about 26.9x, with a median of about 22.9x.

Public markets show that scale, mission-critical workflows, growth, gross margin, and profitability all matter. Larger enterprise workflow companies can trade at higher revenue multiples because they are deeply embedded in customer operations. Document and content workflow companies can still be valuable, but often trade more moderately unless they have strong growth or a special strategic angle.

Founders should use public multiples as an upper and lower reference band, not as a direct sale price. If your company is smaller, growing more slowly, or less profitable than public peers, buyers will normally discount the multiple. If your company owns a scarce workflow, has high retention, strong AI-enabled contract intelligence, and is strategically important to a buyer, you may be able to argue for a premium.

5. What Drives High Valuations - Premium Valuation Drivers

High valuations happen when buyers believe your business is not only healthy today, but also strategically valuable tomorrow. In CLM, that usually means your platform is hard to replace, has room to grow, and solves a problem that buyers care about deeply.

Deep workflow ownership

Buyers pay more when your product controls the contracting process from intake to execution to post-signature management. This means customers are not just storing documents. They are creating, approving, negotiating, signing, tracking, and analyzing agreements inside your system.

A buyer will see more value if your platform is used by legal, sales, procurement, finance, and operations rather than just one small legal team. Broader usage means higher switching costs and more expansion potential.

AI that improves real contract work

The source data shows strong investor and buyer interest around AI-powered contract review, contract intelligence, contract analysis, clause extraction, and automated workflows. But the premium comes from practical AI, not AI branding.

Examples include AI that helps users compare contract language against playbooks, spot risky clauses, extract renewal dates, identify pricing terms, flag non-standard liability language, or summarize obligations for business users. Buyers want evidence that the AI is accurate, trusted, and used inside real customer workflows.

High recurring revenue and strong retention

CLM buyers prefer subscription revenue because it is more predictable. They also care about whether customers renew, expand, and add modules over time.

Strong retention tells buyers that the product is important. Expansion tells buyers that the product has more room to grow inside existing accounts. In CLM, expansion might come from adding business units, countries, contract types, AI modules, e-signature volume, vendor management, or analytics.

Enterprise-grade security and compliance

Contracts contain sensitive commercial, legal, personal, and financial information. Buyers will place more value on platforms with strong security, permissioning, audit trails, data controls, and compliance features.

This is especially important if your customers are in financial services, healthcare, public sector, legal services, or large enterprises. Security and compliance do not always create a flashy sales story, but they reduce buyer fear and support a stronger valuation case.

Strategic integrations

A CLM platform becomes more valuable when it fits into the systems customers already use. Important integrations include CRM, e-signature, procurement, finance, document storage, identity, Microsoft Office, and collaboration tools.

For example, a platform that helps sales teams generate contracts from CRM data, route approvals to legal, send for signature, store the final agreement, and push renewal obligations back into customer systems has a much stronger story than a standalone repository.

Clean financials and clear metrics

Even an excellent product can lose value if the financial story is messy. Buyers want to see clean revenue recognition, clear recurring revenue, gross margin by product line, implementation revenue separated from subscription revenue, customer retention data, and a simple bridge from bookings to revenue.

This matters because buyers are not only buying your past performance. They are underwriting the future. Clean numbers help them trust the future.

Strong leadership beyond the founder

Many CLM businesses are founder-led, especially in sales, product vision, and customer relationships. That is normal. But buyers pay more when the company can run without the founder being involved in every major deal or product decision.

A strong second layer of leadership in sales, product, engineering, customer success, and finance reduces transition risk and makes the company easier to buy.

6. Discount Drivers - What Lowers Multiples

Discounts usually come from uncertainty. If buyers cannot understand your revenue quality, customer stickiness, margins, product differentiation, or future growth, they lower the price to protect themselves.

The first discount driver is weak recurring revenue. If a meaningful share of revenue comes from one-time implementation, custom projects, professional services, or non-repeatable work, buyers will usually apply a lower multiple. Services can be useful, but they should support the software rather than define the business.

The second is poor or unclear retention. CLM products should become more valuable over time as customers add contracts, data, users, departments, and workflows. If customers churn after initial deployment, or if usage falls after signing, buyers will question whether the product is mission-critical.

The third is heavy customization. Some enterprise buyers require configuration, but if every deployment feels like a custom project, buyers will worry about scalability. A software business that needs too many people to implement and support each customer can start to look more like a services business.

The fourth is weak gross margin. The public peer set shows that many strong software businesses in and around this market have gross margins in the 70% to 80%+ range. If your gross margin is much lower, buyers will ask whether hosting costs, support load, services delivery, or product architecture are limiting scalability.

The fifth is AI risk. If your AI features are not reliable, not explainable, or not trusted by legal users, buyers may discount the story. In CLM, bad AI can create legal and commercial risk. Buyers want evidence of accuracy, controls, auditability, and real adoption.

Other common discount drivers include customer concentration, slow growth, founder dependency, weak financial records, no clear sales process, unclear product roadmap, security gaps, and an unclear competitive position.

7. Valuation Example: A Contract Lifecycle Management Company

This example is fictional. The company, revenue level, valuation range, and multiples are illustrative only. This is not investment advice, not a formal valuation, and not a fairness opinion.

Assume a fictional CLM company called Northstar Contracts. It has USD 10m of annual revenue. It sells subscription software to mid-market and enterprise customers, with modules for contract intake, workflow approvals, AI-assisted review, e-signature routing, repository management, renewal tracking, and contract analytics.

The valuation logic starts with the market data. Private workflow and document software deals in the source set cluster around an overall average of about 3.6x revenue and median of about 2.9x revenue, with better workflow software assets reaching into the 3.0x-5.5x area. Public software peers in related categories show an overall average of about 4.1x revenue and median of about 2.8x revenue, with higher values for scaled, strategic workflow platforms.

For Northstar Contracts, a reasonable core range might be around 3.5x-5.5x revenue. That range is supported if the company is a true SaaS workflow platform, growing well, and has decent retention. A premium case could move higher if it has strong AI adoption, enterprise customers, high recurring revenue, clean metrics, strong gross margin, and broad integrations. A discounted case could move lower if the company has heavy services revenue, high churn, weak margins, or unclear financial records.

The key lesson is that two CLM businesses with the same USD 10m of revenue can be worth very different amounts. One might be worth closer to USD 25m-30m if revenue is lumpy, churn is high, and implementation work dominates. Another might be worth USD 60m-70m if it has strong recurring revenue, high retention, deep workflow ownership, trusted AI, and a clear strategic fit for buyers.

This is why valuation preparation matters. You cannot control the market, but you can control how clearly buyers understand your revenue quality, customer value, growth story, and risk profile.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a practical scoring tool. Score each factor from 0 to 2. A score of 0 means weak or unclear. A score of 1 means acceptable but not exceptional. A score of 2 means strong and well-supported by data.

A total score of 10-12 suggests you may be closer to premium multiple territory, assuming market conditions are supportive. A score of 6-9 suggests a fair-market outcome where process quality and buyer fit will matter a lot. A score below 6 suggests you may have meaningful work to do before selling, unless there is a special strategic reason a buyer wants your company now.

Be honest with yourself. The goal is not to “win” the scorecard. The goal is to identify which 2-3 improvements could have the biggest valuation impact before you go to market.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Founders often start conversations with buyers before the numbers, story, and process are ready. That can lead to weak first impressions, low initial offers, and avoidable issues during diligence.

The second mistake is hiding problems. Buyers will find the issues later. If churn is rising, a large customer is at risk, gross margin is under pressure, or AI accuracy is inconsistent, hiding it usually destroys trust and reduces value. It is better to explain the issue, show the plan, and show early evidence of improvement.

The third mistake is weak financial records. In CLM, buyers will want to separate subscription revenue, implementation revenue, support revenue, and any custom services revenue. They will also want retention, gross margin, customer concentration, bookings, renewals, and revenue recognition to be clean. If your numbers are messy, buyers assume more risk.

The fourth mistake is not running a structured, competitive sale process with an advisor. Research and market experience show that a structured competitive process with an advisor can lead to meaningfully higher purchase prices, often cited at around 25%. The reason is simple: more qualified buyers, better positioning, and real competition usually create better outcomes.

The fifth mistake is revealing the price you want too early. If you tell buyers you want USD 10m of enterprise value, many will anchor around that number and offer USD 10.1m or USD 10.2m. That kills price discovery. A good process lets the market tell you what the business is worth.

Two CLM-specific mistakes are also common. One is overstating AI differentiation without proof of customer usage. Buyers will test whether the AI is real, accurate, and valuable. The other is failing to show post-signature value. If your story ends at “we help contracts get signed,” you may miss the bigger valuation narrative around obligations, renewals, risk, revenue leakage, and contract intelligence.

10. What Contract Lifecycle Management Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers

Start by cleaning up revenue reporting. Separate subscription revenue from services, implementation, support, usage-based fees, and one-time work. Show recurring revenue clearly.

Track gross margin by revenue type. If services are dragging down blended margin, show buyers what the software margin looks like separately. Then reduce unnecessary custom work where possible.

Improve renewal visibility. Build a simple dashboard showing customer renewal dates, renewal outcomes, churn reasons, expansion revenue, and at-risk accounts. Buyers will pay more attention to retention if it is clearly tracked.

Strengthen the product story

Pick the workflows where you are strongest and prove them with data. For example, show that customers reduce contract approval time, improve compliance with playbooks, reduce missed renewals, or speed up sales contracting.

Deepen the integrations that matter most. You do not need to integrate with everything. But if most of your customers use Salesforce, Microsoft, a procurement platform, or a major e-signature tool, make those integrations easy to explain and easy to demo.

Show real AI usage. Track how often AI review, clause extraction, risk scoring, summarization, or obligation tracking is used. Buyers will care more about adoption and accuracy than feature lists.

Reduce buyer risk

Fix financial hygiene before diligence starts. Clean management accounts, consistent revenue recognition, clear customer-level data, and a reliable forecast can make a major difference.

Reduce founder dependency. Start moving key sales, customer success, and product relationships to your leadership team. Buyers want to know the company can perform after a transaction.

Prepare customer proof. Collect case studies, usage data, renewal stories, and references. In CLM, proof matters because buyers want to know the software is embedded in real workflows, not just purchased and underused.

Prepare the sale narrative

Do not position your business as “just contract management.” Position it around the business problem you solve: faster revenue contracting, safer procurement, better compliance, lower legal workload, fewer missed obligations, or better visibility into commercial risk.

Build a buyer-specific story. A legaltech buyer may care about legal workflow depth. A workflow automation buyer may care about enterprise process automation. An e-signature or document platform may care about agreement data and cross-sell. A private equity buyer may care about retention, pricing, and consolidation potential.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can help you reach a broader and more relevant buyer universe. Instead of relying only on obvious buyers, AI can identify hundreds of qualified acquirers based on deal history, product fit, customer overlap, financial capacity, and strategic logic. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal closes if one buyer drops out.

AI can also help move faster. Buyer matching, outreach preparation, marketing materials, diligence support, and process management can be accelerated. For founders considering a sale in the next 1-12 months, speed matters because buyer appetite and market windows can change quickly.

The human advisor still matters. Expert M&A advisors bring judgment, negotiation experience, credibility with buyers, and the ability to frame your company in the language buyers understand. AI enhances that work by making the process broader, faster, and more data-driven.

The result is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how an AI-native process can support your exit, book a demo with one of Eilla AI’s expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.