The Complete Valuation Playbook for Robotic Process Automation Businesses

A practical guide to how robotic process automation businesses are valued and what drives premium multiples.

Robotic Process Automation has moved from a cost-saving tool to a broader enterprise automation layer. Buyers are no longer only asking, “Can this software automate repetitive work?” They are asking, “Is this platform embedded in mission-critical workflows, does it create measurable return on investment, and can it expand across departments?”

That matters if you are considering a sale in the next 1-12 months. RPA and workflow automation are active M&A categories, but buyers have become more selective. Strong platforms with recurring revenue, enterprise adoption, clean margins, and clear automation outcomes can attract premium interest. Services-heavy, slow-growth, or poorly documented businesses usually get discounted.

This guide shows what RPA businesses actually sell for, what public market multiples suggest, what pushes valuation up or down, and how you can assess where your own company might fit. The data and valuation logic are based on the provided market sources and transaction set.

1. What Makes Robotic Process Automation Unique

RPA businesses are not valued like ordinary software companies, and they are not valued like ordinary IT services firms either. They sit between software, workflow automation, enterprise operations, and digital transformation.

At one end of the market, you have pure software platforms: bot builders, process orchestration tools, low-code workflow platforms, monitoring dashboards, task mining, process mining, and AI-assisted automation. These businesses can look like SaaS companies if revenue is recurring, gross margins are high, and customers use the product every day.

At the other end, you have implementation-heavy automation providers. These businesses help customers design, deploy, and manage automations, often with custom work, consulting, integrations, and managed services. They may be valuable, but buyers usually apply lower multiples because revenue is more people-dependent and less scalable.

Most privately held RPA businesses sit somewhere in the middle. They have software, but also services. They may have recurring licenses, but also one-off implementation fees. They may have strong customer value, but buyers need proof that the business can scale without adding headcount at the same pace as revenue.

Key valuation considerations in RPA include:

The biggest risk buyers will check is whether your RPA business is truly a product business or mostly a services business wearing a software label. They will also examine bot reliability, customer concentration, churn, implementation complexity, AI claims, data security, and whether automations break when customer systems change.

2. What Buyers Look For in a Robotic Process Automation Business

Buyers start with the basics: revenue scale, growth, profitability, margins, customer retention, and management quality. But in RPA, they go further. They want to understand whether your platform controls important workflows or simply automates small tasks around the edges.

A buyer will usually pay more if your product is used across multiple departments. For example, automation that starts in finance but expands into operations, HR, customer support, compliance, and IT service management can support a stronger platform story. A narrow point solution can still be valuable, but it needs exceptional growth or a very clear niche.

They also care about the quality of your revenue. Recurring subscription revenue is stronger than one-time setup fees. Multi-year enterprise contracts are stronger than month-to-month small business accounts. Expansion revenue from existing customers is especially valuable because it shows that customers do not just renew - they buy more.

Buyers will also test whether your automation results are measurable. Strong RPA businesses can show metrics like hours saved, manual tasks eliminated, error rates reduced, faster processing times, or lower cost per transaction. This matters because buyers need to believe your customers have a clear reason to stay.

How private equity buyers think

Private equity buyers are financial buyers. They usually plan to own the business for 3-7 years and then sell it again. That means they care about what they can pay today, what they can improve, and who might buy the company later.

They think about valuation in two stages. First, the entry multiple: “What multiple are we paying now?” Second, the exit multiple: “What multiple might someone pay when we sell this business later?” If they believe your company can grow, improve margins, reduce churn, and become a more strategic platform, they may accept a higher entry price.

They also look for levers. In RPA, those levers may include price increases, packaging improvements, cross-selling modules, adding AI-assisted workflows, reducing custom implementation work, expanding partner channels, or acquiring smaller automation providers. If those levers are obvious and realistic, your business becomes easier to underwrite.

3. Deep Dive: Productized Platform vs Implementation-Heavy Automation

One of the biggest valuation questions in RPA is simple: are you selling repeatable software, or are you selling custom automation projects?

This distinction can have a major impact on valuation. A productized RPA platform can be sold repeatedly with limited extra cost. Once built, the same core product can serve many customers. An implementation-heavy business may still solve important problems, but each new customer may require custom workflows, manual setup, integration work, and ongoing support.

Buyers care because scalable software usually deserves a higher multiple than services revenue. Software can grow faster and produce higher margins. Services revenue is often more dependent on people, utilization, delivery quality, and project pipeline.

The transaction data supports this split. Software-oriented workflow and process automation businesses show materially higher revenue multiple potential than lower-margin business process automation services and outsourced operations. At the same time, the data also shows that software positioning alone is not enough. Some broad workflow software businesses still traded at modest multiples when revenue declined, margins were weak, or the strategic story was not supported by clean financial momentum.

If your business looks more like the left column today, the goal is not to pretend otherwise. Buyers will find out. The better move is to spend 6-12 months shifting the mix: standardize deployments, package common use cases, reduce custom work, track recurring revenue separately, and show that gross margin improves as the company scales.

4. What Robotic Process Automation Businesses Sell For - and What Public Markets Show

Valuation ranges in RPA are wide because the category includes several different business models. A pure enterprise workflow automation platform is not the same as an automation consulting firm. A finance automation SaaS company is not the same as a document workflow provider. A low-growth services-heavy company is not the same as a fast-growing platform embedded in enterprise operations.

The right way to use the data is to look for the most relevant peer group, then adjust for your company’s size, growth, margins, retention, and risk.

4.1 Private Market Deals - Similar Acquisitions

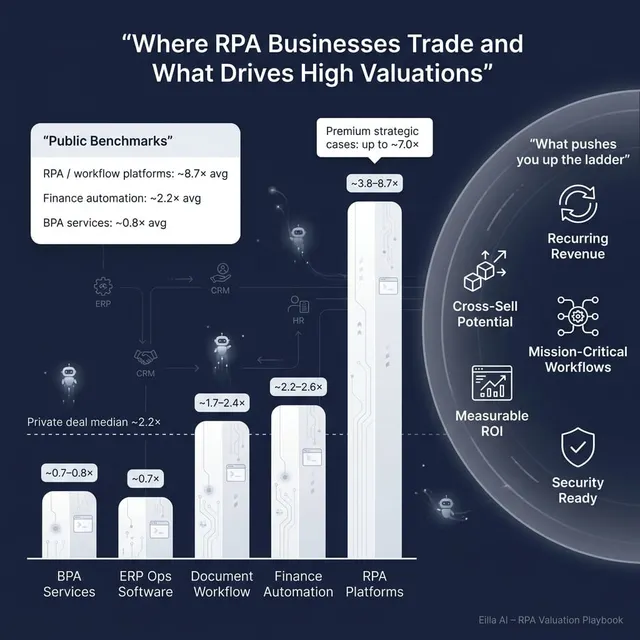

The private transaction data shows an overall average EV/Revenue multiple of around 3.5x and a median of around 2.2x. But the category mix matters a lot.

Enterprise workflow, process automation, and service management software showed an average EV/Revenue of around 5.5x, but a median of only around 1.3x. That tells you there were some high-multiple outliers, but many deals happened at much more modest levels. HR process automation and performance management software averaged around 3.2x revenue with a median of around 2.7x. IT services, consulting, and custom automation solutions averaged around 2.8x revenue. ERP, financial, and manufacturing operations software came in much lower, around 0.7x revenue.

The key message: headline RPA multiples can be misleading. A founder may hear about a high-multiple automation deal and assume it applies to their business. But buyers will separate software revenue from services revenue, recurring revenue from project revenue, and growing customers from shrinking customers.

4.2 Public Companies

Public market data gives a useful reference point, but it is not a direct price tag for your private company. Public companies are usually larger, more liquid, better known, and more diversified. They often deserve higher multiples than smaller private businesses with more concentration risk.

As of the provided 2025 market data, enterprise RPA, low-code, and workflow automation platforms showed the highest average EV/Revenue multiple at around 8.7x, though the median was much lower at around 3.8x. That gap matters. It means a few very highly valued public companies pull the average upward.

Business process automation services and outsourced operations traded much lower, around 0.8x average EV/Revenue and 0.7x median EV/Revenue. Finance, accounting, compliance, and reporting automation software averaged around 2.2x EV/Revenue, with a median of around 2.6x. Document, content, and information workflow management software averaged around 2.4x EV/Revenue, with a median of around 1.7x. Horizontal enterprise application and work management platforms averaged around 3.1x EV/Revenue, with a median of around 3.4x.

For a private RPA founder, public comps should be used as reference bands. If your business is smaller, slower growing, less profitable, or more customer-concentrated than the public peers, expect a discount. If your company is scarce, growing quickly, highly profitable, and strategically important to a buyer, you may be able to push above the normal private range.

The most practical takeaway is that many good RPA software businesses may fall somewhere around the 2.5-4.5x revenue area, with higher outcomes possible when the company has clear premium drivers. Services-heavy or low-growth automation businesses may fall meaningfully below that.

5. What Drives High Valuations - Premium Valuation Drivers

Premium valuations are not created by calling yourself an RPA platform. They are created by proof. Buyers pay more when they can see that the product is important, sticky, scalable, and hard to replace.

Mission-critical workflow position

RPA platforms are more valuable when they sit inside daily enterprise workflows. If your software helps run customer support, finance operations, HR onboarding, IT service management, compliance, or security incident processes, buyers see more strategic value.

The reason is simple: tools embedded in daily workflows are harder to remove. If employees, managers, and systems rely on your platform every day, switching becomes painful. That lowers perceived risk for the buyer.

Practical examples include automations that approve invoices, route customer requests, manage employee onboarding, reconcile records, monitor exceptions, or trigger compliance workflows.

Security and compliance readiness

Enterprise automation often touches sensitive systems and data. Bots may access customer records, employee files, financial systems, internal approvals, or regulated workflows. That makes security and compliance a real valuation driver.

Buyers will value clean permission controls, audit trails, role-based access, certifications, secure deployment options, and strong governance. These features reduce procurement friction and make it easier for large customers to approve your platform.

But compliance alone does not create a premium. It supports the valuation story when combined with growth, retention, and strong economics.

Platform breadth and cross-sell potential

A narrow tool can be valuable, but a platform with multiple modules can give buyers a bigger growth story. In RPA, that may mean bot design, workflow orchestration, monitoring, analytics, document automation, approval routing, exception handling, and AI-assisted recommendations.

Breadth matters because buyers can imagine selling more to the same customers. If a customer starts with finance automation, the buyer may see opportunities in HR, operations, customer service, or IT.

The important point is that breadth must be real. A long feature list is not enough. Buyers want evidence that customers actually buy multiple modules and expand usage over time.

Strong installed base and usage metrics

A large active user base can support a premium valuation even when current profits are limited. In RPA, buyers care about deployed bots, automated processes, active users, usage frequency, transactions processed, and departments covered.

These metrics show that the platform is not just purchased - it is used. Usage is powerful because it signals product-market fit and future monetization potential.

If you can show that customers start small and then automate more processes over time, your valuation story becomes much stronger.

High gross margins and efficient delivery

Premium software multiples require software-like margins. Buyers want to see that each additional customer does not require a large amount of custom work.

High gross margin tells buyers that the product can scale. Strong EBITDA, or a clear path to EBITDA, tells them the business can produce cash. Even if you are investing for growth, you should be able to explain how margins improve as the company matures.

For an RPA business, this often means reducing custom implementation, creating reusable templates, building partner delivery capacity, and improving customer onboarding.

Clean financials and predictable revenue

Buyers pay more when the numbers are easy to trust. That means clean revenue recognition, clear separation of software and services revenue, accurate gross margin reporting, consistent customer metrics, and well-documented contracts.

Predictable revenue is especially important. Recurring subscriptions, multi-year agreements, low churn, and expansion revenue make a buyer more comfortable paying a stronger multiple.

If your financials are messy, buyers may not walk away, but they will usually lower the price or add protection into the deal structure.

6. Discount Drivers - What Lowers Multiples

The biggest valuation discount in RPA comes from weak proof. If the company has an attractive product story but cannot prove growth, retention, margins, or customer value, buyers will not pay for the story alone.

Revenue decline or flat growth is a major issue. The provided transaction data shows that even workflow software companies can trade at modest multiples when revenue deteriorates or EBITDA is negative. Buyers may still be interested, but they will treat the business as a turnaround or tuck-in acquisition rather than a premium platform.

Services-heavy revenue also lowers multiples. If most revenue comes from custom projects, implementation, or consulting, buyers will value the company more like a professional services business. That does not mean the business has no value. It means the multiple will likely be lower than for a scalable software platform.

Common discount drivers include:

Another discount driver is unclear differentiation. RPA is a crowded market. If buyers cannot quickly understand why your platform wins, where it is strongest, and why customers choose you instead of larger vendors or internal automation teams, they will be cautious.

The good news is that many discount drivers are fixable. You may not double revenue in six months, but you can clean up reporting, reduce customer concentration, document ROI, package your product better, and build a more credible buyer narrative.

7. Valuation Example: A Robotic Process Automation Company

This example is fictional. The company, revenue level, and valuation scenarios are illustrative only. They are not investment advice, not a formal valuation, and not a fairness opinion.

Let’s call the fictional company FlowForge Automation.

FlowForge has USD 10m of annual revenue. It sells an enterprise RPA platform with drag-and-drop bot design, workflow orchestration, monitoring dashboards, KPI tracking, and security controls. Around 75% of revenue is recurring software subscription revenue, and 25% comes from implementation and support services. Customers are mostly mid-market and enterprise clients in finance, logistics, healthcare administration, and business services.

Step 1: Select the right valuation lens

For FlowForge, the most relevant reference points are enterprise RPA, workflow automation, low-code platforms, finance automation, and horizontal work management platforms. The lower services-style public ranges are less relevant because FlowForge is primarily a software platform, not an outsourced operations provider.

The public software comps in the data cluster broadly around the low-to-mid single digit revenue multiple range for many mature automation and workflow software companies, with some large strategic platforms trading higher. Private software-oriented automation deals also show a wide range, but more grounded private ranges support a core range around 2.8-4.2x revenue for a smaller private RPA platform with credible software characteristics.

Step 2: Apply the logic to USD 10m revenue

A reasonable base case for FlowForge might be around 2.8-4.2x revenue, implying USD 28-42m of enterprise value on USD 10m revenue.

If FlowForge has stronger premium drivers - for example, fast growth, high retention, strong gross margins, enterprise contracts, measurable ROI, low churn, and broad platform usage - the multiple could move higher.

If FlowForge has weaknesses - for example, high services mix, customer concentration, weak growth, poor margins, limited usage data, or messy financials - the multiple could move lower.

The premium strategic case should not be treated as the default. It requires evidence. A buyer would need to believe FlowForge is scarce, growing, sticky, secure, scalable, and strategically important.

Step 3: What this means for founders

Two RPA companies with the same USD 10m of revenue can be worth very different amounts.

One company may be worth closer to USD 20m because revenue is flat, services-heavy, concentrated in a few customers, and dependent on founder-led delivery. Another may be worth USD 50m or more because revenue is recurring, growing quickly, highly profitable, diversified, and embedded in core enterprise workflows.

That is why valuation preparation matters. You are not just selling last year’s revenue. You are selling the buyer’s confidence in the next five years.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a simple internal scoring tool. Score each factor from 0 to 2.

0 means weak or unproven.1 means acceptable but not a clear strength.2 means strong and well supported by data.

Interpret the total honestly:

The goal is not to flatter yourself. The goal is to identify which improvements would most increase buyer confidence.

For example, moving from 60% recurring revenue to 80% recurring revenue may matter more than launching a new feature. Reducing customer concentration may matter more than adding another dashboard. Cleaning up financial reporting may matter more than rewriting your website.

9. Common Mistakes That Could Reduce Valuation

Rushing the sale

A rushed sale usually leaves money on the table. If you go to market before your numbers, customer story, product narrative, and data room are ready, buyers will see risk. Risk lowers price.

A strong process starts before the first buyer call. You should know your revenue mix, gross margins, churn, retention, customer concentration, pipeline, product roadmap, and key growth drivers.

Hiding problems

Problems discovered late in due diligence are much more damaging than problems explained early. Buyers do not expect perfection. They do expect honesty.

If churn increased, a major customer left, margins dipped, or an implementation went badly, explain what happened and what changed. Hiding issues destroys trust and often leads to price cuts, tougher terms, or a failed deal.

Weak financial records

Weak financial records are one of the most avoidable valuation problems. In RPA, buyers will want to separate software subscription revenue, services revenue, support revenue, implementation fees, and any usage-based revenue.

They will also want clear gross margin by revenue type. If software gross margin is strong but blended margin looks weak because services are mixed in, poor reporting can hide the quality of your business.

No structured competitive process

A one-buyer conversation rarely produces the best price. Buyers have more leverage when they believe they are the only serious option. A structured competitive process changes that dynamic.

Research commonly cited in M&A shows that running a competitive sale process with an advisor can lead to meaningfully higher purchase prices, often around 25% higher than less structured approaches. The exact uplift varies by deal, but the principle is clear: competition improves price discovery.

Revealing your target price too early

Do not tell buyers what price you want before the market has spoken. If you say you are looking for USD 10m, many buyers will anchor around USD 10.1m or USD 10.2m, even if they might have paid much more.

Your job is to create a process where buyers reveal what the business is worth to them. Price discovery works best when qualified buyers compete.

Overclaiming AI capability

Many RPA companies are adding AI features, but buyers are skeptical of vague claims. “AI-powered” is not enough.

If AI is part of your story, show exactly what it does: document extraction, exception handling, process recommendations, natural language workflow creation, predictive monitoring, or automated testing. Then show adoption and customer value.

Ignoring bot maintenance risk

RPA buyers will ask what happens when customer systems change. Do bots break? Who fixes them? How often? How much support is required?

If your platform has strong monitoring, alerting, version control, testing, and maintenance workflows, make that clear. If not, buyers may discount the business because they see hidden support costs.

10. What Robotic Process Automation Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers care about

Start by separating revenue clearly. Break out recurring software, implementation, support, managed services, and one-time work. Then calculate gross margin for each category.

Next, focus on retention. Show logo retention, revenue retention, expansion revenue, churn, and customer cohort behavior. Buyers love seeing customers expand over time because it proves the platform becomes more valuable after deployment.

You should also reduce services dependency where possible. Productize common implementation steps. Create templates for common workflows. Train partners or customer success teams to handle repeatable deployments.

Prove customer value

Create simple case studies with numbers. For example: “Customer reduced invoice processing time by 60%,” “Customer automated 40,000 monthly tasks,” or “Customer saved 2,500 employee hours per quarter.”

Do not rely only on testimonials. Buyers want evidence. Build a repeatable return-on-investment story around time saved, cost removed, errors reduced, faster processing, or better compliance.

Track usage metrics. Deployed bots, active workflows, transactions processed, departments using the platform, and monthly active users can all strengthen the story.

Reduce buyer risk

Clean up contracts. Make sure customer agreements are signed, transferable where possible, and easy to review. Multi-year contracts and renewal history can support stronger valuation.

Address security gaps. Prepare documentation around access controls, certifications, audit logs, data handling, permissioning, and incident history. Enterprise buyers will care.

Build a management bench. If every major sale, deployment, and customer relationship depends on you, buyers will discount for founder risk. Even a small but capable leadership layer can improve confidence.

Strengthen the strategic story

Position the company around the buyer’s logic, not just your product features. A buyer wants to know why your platform matters, why customers stay, where expansion comes from, and how the business can grow after acquisition.

Map likely acquirer groups. These may include larger RPA platforms, workflow automation vendors, low-code platforms, ERP and CRM ecosystems, IT services companies, business process outsourcing firms, finance automation vendors, and private equity-backed software platforms.

Finally, prepare before you launch a process. A clean data room, clear financial model, strong customer metrics, and credible management presentation can materially improve buyer confidence.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can improve an exit process by expanding the buyer universe far beyond the obvious names. In RPA, the best buyer may not be the largest automation vendor. It could be a workflow software company, an IT services group, a finance automation platform, a private equity-backed software buyer, or a strategic acquirer looking for AI-enabled automation capability.

AI can help identify hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, product overlap, customer synergies, and acquisition behavior. More relevant buyers usually means more competition, better price discovery, and a higher chance the deal closes because there are more options if one buyer drops.

AI-driven buyer matching, outreach support, marketing material creation, and due diligence preparation can also accelerate the process. In many cases, initial conversations and offers can be reached in under six weeks when the business is prepared and the buyer universe is well targeted.

The best outcomes still require expert human judgment. Experienced M&A advisors help frame the story, prepare the numbers, manage buyer tension, negotiate terms, and protect you from avoidable mistakes. AI makes the process broader and faster; expert advisors make it credible and controlled.

If you would like to understand how an AI-native process can support your exit, book a demo with one of Eilla AI’s expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.