The Complete Valuation Playbook for AV Systems Integration Businesses

A data-driven guide to how AV systems integration businesses are valued and what drives premium multiples.

If you own an AV systems integration business and you are thinking about selling in the next 1-12 months, valuation is probably already on your mind. You may be hearing stories about strategic buyers, private equity groups, consolidation, managed services, recurring revenue, and premium multiples. Some of those stories are useful. Some are noise.

AV integration is in an interesting moment. Corporate workplaces are still being redesigned around hybrid work, schools and universities are upgrading learning environments, venues are investing in immersive experiences, and enterprises are trying to standardize meeting room technology across many locations. At the same time, buyers are becoming more selective. They are not just paying for revenue. They are paying for predictable revenue, clean margins, strong customer relationships, technical talent, and a business that can scale without the founder personally holding everything together.

This playbook shows what AV systems integration businesses can learn from private deal data, public market references, and observed premium and discount valuation drivers in adjacent systems-heavy infrastructure and equipment markets. It will help you understand what companies actually sell for, what pushes valuation up or down, and what you can do in the next 6-12 months to improve your odds of a stronger outcome.

1. What Makes AV Systems Integration Unique

AV systems integration is not a simple product resale business, even though a large part of revenue may come from equipment. It is also not a pure software business, even when the company has remote monitoring, room management, or managed service software attached. Most AV integrators sit somewhere between project-based construction services, technical consulting, hardware procurement, software configuration, field installation, and long-term support.

That mixed business model is why valuation can vary so widely. Two AV companies with the same revenue can be worth very different amounts. One may be mostly one-off project work with low visibility, tight gross margins, and founder-led sales. Another may have enterprise customers, multi-site standards programs, strong service contracts, recurring monitoring revenue, and a leadership team that can run the business without the owner. Buyers will value those two companies very differently.

The main types of AV systems integration businesses include:

The biggest valuation question is not simply “How much revenue do you have?” It is “What kind of revenue do you have?” Buyers will separate low-margin equipment pass-through from higher-value design, engineering, programming, managed services, and support. They will also check whether your customer relationships are repeatable or if every year starts from zero.

Key risks buyers will always test include backlog quality, customer concentration, project margin control, warranty exposure, manufacturer dependence, technician retention, working capital needs, and whether the founder is still the main salesperson, estimator, problem-solver, and customer relationship owner.

2. What Buyers Look For in an AV Systems Integration Business

Buyers start with the obvious items: size, growth, profitability, customer quality, and margin stability. A larger AV integrator with steady growth, clean financials, and consistent EBITDA will usually attract more interest than a smaller company with uneven results.

But the industry-specific details matter just as much. AV integration is project-heavy, so buyers want to know whether your revenue is predictable. They will look at backlog, signed contracts, recurring support agreements, renewal rates, customer repeat purchase history, and whether you have a clear pipeline for the next 6-12 months.

Buyers also care about your mix of revenue. Hardware resale is usually lower value because it can be competitive and margin-thin. Design, engineering, programming, project management, remote monitoring, maintenance, and managed services usually support a stronger valuation story because they are harder to replace and more tied to customer trust.

A strategic buyer may be looking for geographic expansion, technical talent, new verticals, manufacturer certifications, enterprise accounts, or a local service footprint. For example, a national AV platform may pay more for a regional integrator with strong enterprise relationships in healthcare, higher education, or Fortune 500 workplaces than for a similar-sized company with scattered one-off projects.

How Private Equity Thinks

Private equity buyers think about what they pay today and what they can sell the business for later. They may own the business for 3-7 years. During that time, they want to grow revenue, improve margins, reduce risk, and possibly acquire other smaller integrators.

They will ask: “Can this business become bigger, more profitable, and less risky under our ownership?” That may involve adding sales leadership, improving pricing, cross-selling managed services, centralizing procurement, buying other local integrators, or expanding into adjacent services such as IT, security, workplace technology, or digital signage.

Private equity also thinks about the next buyer. If they buy your business today, could they later sell it to a larger strategic acquirer, a bigger private equity fund, or another platform? Businesses with recurring revenue, strong management, clean reporting, and a clear market position are easier to resell later. That makes them more attractive today.

3. Deep Dive: Project Revenue vs Recurring Revenue

The biggest valuation nuance in AV systems integration is the difference between project revenue and recurring revenue.

Project revenue can be excellent. A large corporate headquarters buildout, university classroom upgrade, hotel renovation, or performing arts center project can produce meaningful revenue and profit. But from a buyer’s point of view, project revenue has a weakness: it must be replaced again and again. Unless you have a strong backlog and repeat customers, buyers worry that last year’s revenue may not repeat next year.

Recurring revenue changes the conversation. Service contracts, remote monitoring, help desk support, preventive maintenance, managed collaboration rooms, warranty extensions, and multi-site support agreements all make the business more predictable. Buyers usually pay more for predictability because it reduces the risk that revenue drops immediately after closing.

This is also visible in the supplied deal data from adjacent systems-heavy infrastructure markets. The highest valuation outcomes were not earned by generic exposure to a popular theme. They were earned by businesses that combined differentiated technical capability with proven monetization and real margin. In plain English: buyers did not pay a premium just because a company was in a hot sector. They paid more when the business had technology, proof, margins, and customer adoption.

For AV founders, the lesson is direct. Do not rely only on the idea that “AV is growing” or “hybrid work is here to stay.” Buyers already know that. The stronger valuation story is: “Our customers rely on us after installation. They renew support contracts. We monitor their rooms. We standardize technology across locations. We are not just project installers; we are an ongoing operating partner.”

If your business looks more like the left column today, you do not need to transform overnight. In 6-12 months, you can still improve the story. Start by attaching service agreements to every new project, converting past installations into support contracts, tracking recurring revenue separately, and proving customer retention with simple data.

4. Deep Dive: Technical Complexity Can Help Valuation - But Only If It Converts Into Profit

Many AV founders believe their business deserves a premium because the work is technically complex. Sometimes that is true. Complex environments such as enterprise campuses, universities, stadiums, broadcast facilities, command centers, healthcare systems, and mission-critical meeting spaces can be attractive to buyers.

But technical complexity by itself is not enough. Buyers will ask whether complexity creates pricing power, customer stickiness, high margins, and barriers to competition. If complex work only creates project overruns, labor shortages, and warranty issues, it can actually hurt valuation.

The supplied transaction data shows the same pattern in adjacent infrastructure and engineered systems markets. Assets serving technically demanding end markets did not automatically receive premium multiples. The premium cases were those where technical differentiation was paired with proven profitability, adoption, and management continuity. Broader industrial or infrastructure exposure alone often produced much lower revenue multiples.

For AV systems integrators, this means you should be able to show that your technical strength produces business value. For example, you might have certified engineers, strong manufacturer partnerships, low rework rates, high project gross margins, high attach rates for support contracts, and a track record of delivering multi-site rollouts on time.

The best version of the story is not “we do hard projects.” It is “we do hard projects reliably, profitably, and repeatedly for customers who keep coming back.”

5. What AV Systems Integration Businesses Sell For - and What Public Markets Show

Valuation data for privately held AV systems integration businesses is not always visible. Many deals are private, terms are undisclosed, and purchase prices may include earn-outs, seller notes, working capital adjustments, and performance-based payments.

The supplied dataset is mainly from adjacent systems-heavy infrastructure, energy equipment, hydrogen, power systems, battery, and engineered manufacturing businesses. It is not a pure AV dataset. Still, it is useful because AV integration shares some valuation issues with these markets: hardware content, installation complexity, project execution risk, technical labor, infrastructure relevance, and the difference between generic equipment revenue and differentiated systems capability.

5.1 Private Market Deals - Similar Acquisitions

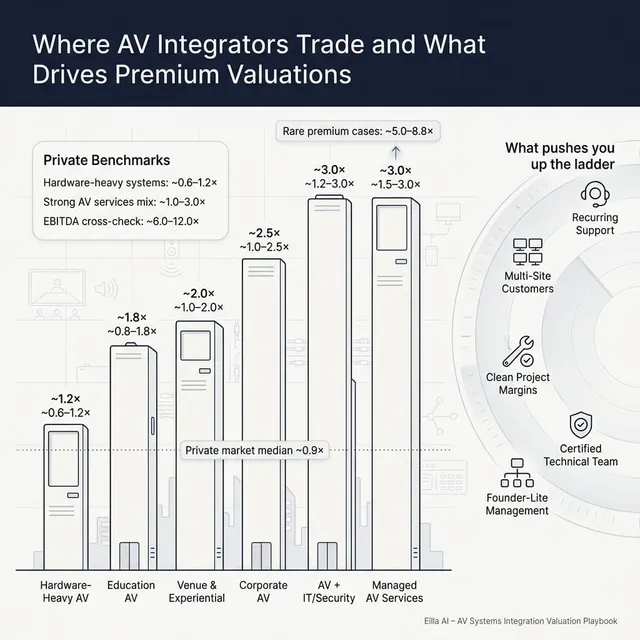

The private transaction data shows a wide spread. Across the full dataset, the average EV/revenue multiple was around 1.8x, while the median was around 0.9x. Average EV/EBITDA was around 12.2x, with a median around 8.3x.

For clean mobility fueling, gas handling, and energy infrastructure businesses, the average EV/revenue multiple was around 2.4x and the median was around 1.0x. Average EV/EBITDA was around 15.3x, with a median around 10.0x. Energy equipment, thermal systems, and battery solution businesses were lower on revenue multiples, averaging around 0.8x EV/revenue.

The most important message is the spread. Many systems-heavy, hardware-linked businesses traded around 0.6x-1.2x revenue. A small number of highly differentiated, profitable, technology-rich businesses traded far higher. For AV founders, this means buyers will not pay a premium just because the company is in an attractive technology-enabled services market. They pay more when the company has recurring revenue, technical differentiation, customer stickiness, and proof of profitable execution.

These ranges are illustrative. A founder-owned AV integrator with USD 10m of revenue, 10% EBITDA margins, limited recurring revenue, and customer concentration will not be valued the same way as a USD 30m integrator with 20% EBITDA margins, recurring managed services, enterprise accounts, and a leadership team that can scale.

5.2 Public Companies

Public markets are not a direct price tag for your company. Public companies are larger, more liquid, better known, and often have broader access to capital. Still, public multiples help frame how investors value categories around infrastructure, equipment, energy systems, and technology-enabled hardware.

The supplied public company data, as of mid to late 2025, shows a wide range. The overall average EV/revenue multiple was around 14.8x, but the median was only around 3.5x. That gap matters. It shows that a few high-growth or speculative public companies can pull the average upward, while the median gives a more grounded view of where many companies actually trade.

Founders should use public multiples as a reference band, not a direct valuation formula. Smaller private businesses usually receive a discount to public companies because they have less scale, less liquidity, less management depth, and more customer concentration risk.

But there are exceptions. A scarce private company with unusually strong strategic value can sometimes attract a premium. In AV, that could mean a company with enterprise-wide managed services contracts, national deployment capability, proprietary remote monitoring, deep workplace technology expertise, or a strong position in a high-value vertical such as healthcare, education, government, or large enterprise collaboration.

6. What Drives High Valuations - Premium Valuation Drivers

High valuations are earned, not assumed. The supplied deal data shows that buyers paid premium valuations only when several things came together: technical differentiation, proof of adoption, attractive margins, strategic relevance, and a team that could keep scaling the business.

For AV systems integration founders, the same logic applies.

6.1 Recurring Revenue and Customer Stickiness

Buyers pay more when they can see revenue that is likely to continue after closing. In AV, this includes service contracts, monitoring subscriptions, help desk support, preventive maintenance, managed meeting rooms, and long-term enterprise support agreements.

A customer who buys one installation and disappears is useful. A customer who standardizes on you across 50 locations and signs a multi-year support agreement is much more valuable.

Practical examples include:

- Service contracts attached to most new installations

- Remote monitoring revenue tracked separately

- Multi-site enterprise customers with repeat work

- High renewal rates on support agreements

6.2 Technical Differentiation That Creates Margin

Technical skill matters when it gives you pricing power or protects you from lower-cost competitors. Buyers like companies that can solve difficult problems, but only if those problems are profitable.

In AV, this may include complex control systems, broadcast-grade environments, command centers, secure government installations, healthcare simulation rooms, immersive venues, or enterprise collaboration standards across multiple geographies.

The key is proof. Buyers will want to see gross margin by project type, rework rates, change orders, utilization, and whether technical complexity leads to better economics.

6.3 Strong Position in Demanding End Markets

The supplied data suggests that technically demanding end markets can support stronger strategic interest, especially when customers face high operational or regulatory requirements. For AV businesses, similar end markets include healthcare, higher education, government, defense, enterprise workplaces, transportation hubs, entertainment venues, and mission-critical facilities.

These customers often have higher switching costs. They care about uptime, security, reliability, support, and standardization. If you are embedded in those environments and have a strong track record, buyers may view your revenue as higher quality.

6.4 Platform Potential

A buyer may pay more if your business can become a platform for growth. That means the company is not just a collection of projects. It has systems, people, processes, and a market position that can support expansion.

In AV, platform potential might include:

- A strong second layer of management

- Repeatable sales process

- Standard project management systems

- Scalable service operations

- Ability to acquire smaller local integrators

- Clear geographic or vertical expansion path

The supplied data also highlights the value of management continuity. When a target’s leadership can help the buyer expand into a region or sector, the business becomes more than an asset purchase. It becomes a growth engine.

6.5 Clean Financials and Clear Reporting

Clean financials are not exciting, but they are one of the biggest valuation protectors. Buyers need to understand revenue, gross margin, EBITDA, backlog, working capital, project profitability, and recurring revenue.

In AV, messy reporting can create real problems. If hardware, labor, subcontractors, service, and warranty costs are not tracked clearly, buyers may assume margins are worse than you say. That can lead to lower offers, more aggressive diligence, or larger holdbacks.

6.6 Diversified Customers and Manufacturer Relationships

Customer concentration can lower valuation. If one customer represents 30%-40% of revenue, a buyer will worry about what happens if that customer leaves. The same applies to manufacturer concentration if your business depends too heavily on one vendor relationship or product line.

Premium outcomes are more likely when revenue is spread across high-quality customers, contracts are documented, and manufacturer partnerships are strong but not overly dependent.

7. Discount Drivers - What Lowers Multiples

Some AV businesses sell at the low end of the range because buyers see risk. The risk may be fixable, but if it is still present during a sale process, it usually affects valuation.

The most common discount driver is low revenue quality. If most revenue is one-off project work, backlog is thin, service contracts are limited, and customer repeat rates are not tracked, buyers will assume the business has to rebuild itself every year.

Another discount driver is margin uncertainty. AV projects can look profitable at the proposal stage but become less attractive after labor overruns, change orders, warranty work, subcontractor issues, or equipment delays. If you cannot show project-level margin data, buyers may price in a risk discount.

Founder dependence is also a major issue. If you personally control key customer relationships, sales, estimates, vendor negotiations, hiring, and escalations, buyers may worry that the business weakens after you leave. Even if you plan to stay for a transition period, buyers prefer companies where the leadership team already operates independently.

Other common discount drivers include:

The supplied transaction data also shows a broader lesson: markets do not automatically reward a popular theme. Many adjacent infrastructure and equipment businesses traded at modest revenue multiples despite being exposed to large decarbonization trends. For AV, the parallel is clear. Hybrid work, smart buildings, and collaboration technology are attractive themes, but buyers still need proof that your company has durable revenue, margin, and execution quality.

8. Valuation Example: An AV Systems Integration Company

This example is fictional. The company, revenue level, valuation range, and multiples are illustrative only. This is not investment advice, not a formal valuation, and not a fairness opinion.

Assume a fictional company called NorthStar AV Integration has USD 10m of revenue. It designs, installs, and supports corporate AV systems for mid-market and enterprise customers. It has a mix of conference rooms, training rooms, digital signage, and unified communications projects. About 18% of revenue comes from recurring support and monitoring contracts.

Step 1: Select the Relevant Reference Points

We would not value NorthStar using only public company multiples. Public companies in the supplied dataset trade at median EV/revenue levels around 3.5x overall, with some segments much higher. But those public companies are larger, more liquid, and often technology or manufacturing businesses with different risk profiles.

We would also not use the lowest private transaction multiples blindly. Some systems-heavy private deals in the dataset traded around 0.6x-1.2x revenue, especially where businesses were more industrial, hardware-heavy, or lower growth. But a strong AV integrator with recurring services, enterprise customers, and high technical capability may deserve better than a generic hardware-heavy reference.

The practical approach is to triangulate. For a private, subscale, systems-heavy AV business with some recurring revenue, a defensible base case might sit around 1.0x-2.0x revenue, depending heavily on EBITDA. A stronger company with meaningful recurring revenue, high margins, low customer concentration, and a strong management team could push higher. A weaker company with thin margins and limited visibility could fall below that range.

Step 2: Apply the Logic to NorthStar AV Integration

Assume NorthStar has:

- USD 10m revenue

- 14% EBITDA margin

- 32% gross margin

- 18% recurring support revenue

- No customer above 14% of revenue

- Strong enterprise repeat business

- Clean project-level reporting

- A capable operations leader under the founder

A buyer may look at both revenue and EBITDA. At USD 10m revenue and 14% EBITDA margin, NorthStar has USD 1.4m of EBITDA.

This table shows why EBITDA matters so much in AV integration. A USD 10m business with only 5% EBITDA margin has USD 500k of EBITDA. A USD 10m business with 18% EBITDA margin has USD 1.8m of EBITDA. Same revenue. Very different valuation conversation.

Step 3: What Could Push NorthStar Higher?

NorthStar could move toward a stronger valuation case if it had 30%-40% recurring revenue, multi-year enterprise contracts, low churn, a national accounts program, strong gross margins, and a management team that could run without the founder.

It could move lower if it had customer concentration, weak backlog, low recurring revenue, poor project tracking, heavy warranty issues, or if the founder was still the only person who could sell and manage key accounts.

The lesson is simple: revenue starts the valuation conversation, but revenue quality determines where the conversation goes.

9. Where Your Business Might Fit - Self-Assessment Framework

Use this as a simple self-assessment. Score each group from 0 to 2.

0 means weak or not yet proven. 1 means acceptable but not best-in-class. 2 means strong and well documented.

Total score: 18 points.

Be honest with yourself. The goal is not to get a perfect score. The goal is to identify which improvements can move valuation the most before you go to market.

For most AV founders, the biggest payoff areas are recurring revenue, margin reporting, customer diversification, backlog visibility, and reducing founder dependence.

10. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Many founders start talking to buyers before their numbers, story, and process are ready. That often leads to lower offers because buyers see uncertainty and price in risk.

The second mistake is hiding problems. If there are margin issues, customer concentration, a weak pipeline, warranty exposure, or messy project accounting, buyers will usually find it in due diligence. Hiding issues damages trust. Once trust is damaged, buyers either reduce price, ask for more protection, or walk away.

Weak financial records are another common value killer. In AV integration, this is especially important because buyers need to understand project margins, labor costs, equipment margins, subcontractor costs, warranty costs, and service profitability. If your accounting does not separate those clearly, buyers may assume the worst.

Not running a structured competitive process can also reduce valuation. Research often cited in M&A markets shows that working with an advisor and running a competitive process can lead to meaningfully higher purchase prices, often around 25%. The logic is simple: when multiple serious buyers compete, you get better price discovery and better leverage on deal terms.

Another mistake is telling buyers what price you want too early. If you say, “I’m looking for USD 10m,” many buyers will anchor around that number. You may get offers at USD 10.1m or USD 10.2m, even if a competitive process could have shown that the right buyer was willing to pay more. Let the market come back with offers before you reveal your expectations.

Two AV-specific mistakes are especially common.

First, founders often fail to separate hardware resale from higher-value services. If your financials make the business look like a low-margin equipment reseller, buyers may value it that way.

Second, some founders underinvest in service contract conversion. They finish strong installations but do not turn those installed systems into long-term support relationships. That leaves money and valuation on the table.

11. What AV Systems Integration Founders Can Do in 6-12 Months to Increase Valuation

You do not need to reinvent the business before selling. But you do need to make the business easier to understand, easier to trust, and easier to underwrite.

Improve the Numbers

Start by cleaning up margin reporting. Separate hardware, labor, subcontractors, programming, project management, service, and warranty costs. Buyers should be able to see which revenue is attractive and which revenue is lower margin.

Improve pricing discipline. Review underpriced service work, weak change order practices, and projects where labor overruns are common. Even small margin improvements can matter because buyers often apply a multiple to EBITDA.

Track recurring revenue separately. Show monthly recurring revenue, annual recurring revenue, service contract renewal rates, attach rates, and churn. If you do not measure it, buyers will not give you full credit for it.

Improve the Revenue Story

Convert past installations into service contracts. Your installed base is one of your best assets. If you completed projects over the last 3-5 years, those customers may need support, upgrades, monitoring, or standardization.

Build a clean backlog and pipeline report. Buyers want to know what revenue is already contracted, what is highly likely, and what is speculative. Do not mix all pipeline together.

Reduce customer concentration where possible. If one customer is too large, focus sales activity on adding new accounts or expanding smaller ones before going to market.

Reduce Risk

Move key customer relationships away from the founder. Introduce account managers, service leaders, and project executives before a sale process starts. Buyers should see that customers trust the company, not just you.

Document your operating processes. Estimating, procurement, project management, installation, programming, service handoff, and warranty response should not live only in people’s heads.

Retain technical talent. AV businesses are people-heavy. If buyers see high technician turnover or no plan for retaining key engineers and project managers, they will worry about delivery risk.

Improve the Buyer Story

Clarify your niche. “We do AV” is less compelling than “we are the leading enterprise workplace AV and managed collaboration provider in our region” or “we specialize in higher education classroom technology and campus-wide AV support.”

Show why you are hard to replace. That might be customer trust, certifications, response times, technical skill, enterprise standards, vertical expertise, or a strong service model.

Prepare the deal materials before outreach. Buyers should receive a clear, professional story with clean numbers, credible growth opportunities, and no obvious gaps.

12. How an AI-Native M&A Advisor Helps

Selling an AV systems integration business is not just about finding one buyer. It is about finding the right buyer universe, creating competition, preparing the story, and managing the process so buyers understand the value of your company.

An AI-native M&A advisor can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, geography, service overlap, vertical focus, and likely synergies. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal closes because you have options if one buyer drops out.

AI can also speed up the early process. Buyer matching, outreach preparation, process materials, diligence support, and market mapping can move faster than a manual-only process. That can help founders reach initial buyer conversations and offers in under 6 weeks, while still keeping the process structured.

The best model is not AI replacing expert advisors. It is expert human M&A advisors using AI to work faster, search broader, and position the business more effectively. You still need experienced deal judgment, buyer credibility, negotiation skill, and clean deal framing. AI helps the advisor bring Wall Street-grade preparation and buyer coverage without traditional bulge bracket costs.

If you would like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.