The Complete Valuation Playbook for Mortgage Services Businesses

A practical to how mortgage services businesses are valued and what drives higher multiples.

If you run a privately held Mortgage Services business and are thinking about selling in the next 1-12 months, valuation is probably one of the biggest questions on your mind. You may have heard that fintech platforms trade at high revenue multiples, that financial software is attractive to buyers, or that private equity is actively consolidating parts of the lending ecosystem. Some of that is true. Some of it is incomplete.

Mortgage Services sits in a complicated part of the market. It touches regulated lending, bank and non-bank lender workflows, credit decisioning, borrower experience, loan servicing, compliance, data, integrations, and often a meaningful amount of implementation or managed service work. That makes valuation more nuanced than simply saying, "we are fintech, so we deserve a fintech multiple."

This playbook shows what similar businesses have sold for, what public markets suggest, what pushes valuation up or down, and how to think about your own business using a practical self-assessment and 6-12 month action plan.

1. What Makes Mortgage Services Unique

Mortgage Services businesses are not all the same. Some are software platforms that help lenders originate, underwrite, process, or service loans. Some provide loan management systems, document workflows, compliance tools, borrower portals, payment support, quality control, or credit decisioning. Others are more services-heavy, supporting lenders with implementation, custom development, managed operations, data processing, or consulting.

That mix matters because buyers do not value all revenue equally. A recurring software subscription that is deeply embedded in a lender's workflow is usually worth more than one-off project revenue. A compliance-critical platform used every day by operations teams is usually worth more than a nice-to-have reporting tool. A business with proprietary data or decisioning assets can be worth more than a business that mainly resells labor or builds custom features.

Mortgage Services also sits inside a regulated and high-consequence workflow. Mistakes can create compliance issues, borrower complaints, loan defects, delays in closing, repurchase risk, or servicing problems. Buyers will always ask whether your system or service improves speed, accuracy, compliance, customer experience, or lender profitability.

The main types of companies in this market include:

The unique valuation question is not just "how much revenue do you have?" It is "what kind of revenue is it, how hard is it to replace, how profitable is it, and how deeply does it sit inside the mortgage workflow?"

Buyers will also focus on risk. In this sector, the major risk factors include customer concentration, exposure to mortgage cycle volatility, weak lender retention, unclear revenue recognition, regulatory issues, dependence on a few senior experts, heavy custom development, poor integration documentation, cybersecurity gaps, and thin financial reporting.

2. What Buyers Look For in a Mortgage Services Business

Buyers start with the obvious: revenue scale, growth, profitability, margins, customer retention, management quality, and whether the business can keep growing after the founder steps back. These are the basics in almost every M&A process.

But in Mortgage Services, the buyer lens goes deeper. Buyers want to know whether your business is tied to a durable workflow. Do lenders rely on you every day? Are you part of origination, underwriting, document collection, servicing, compliance, or credit decisioning? Would replacing you be painful, risky, and time-consuming?

They also want to know whether your revenue is tied only to mortgage volume. A business that makes money only when origination volume is high can be more cyclical. A business that also serves servicing, compliance, loss mitigation, portfolio monitoring, payments, or ongoing loan management may be viewed as more resilient.

Strategic buyers, such as larger financial software companies, banking technology vendors, data providers, consulting firms, and outsourcing platforms, usually look for product fit. They ask: can we sell this into our existing customers? Does it fill a gap in our platform? Does it give us domain talent, regulatory credibility, integrations, or customer access?

Private equity buyers look at the business slightly differently.

How Private Equity Buyers Think

Private equity buyers usually buy with a 3-7 year plan. They ask what multiple they are paying today, what the business could look like in several years, and who might buy it from them later. That future buyer could be a strategic acquirer, a larger private equity fund, or, in rare cases, the public markets.

They also look for practical levers. Can pricing be improved? Can more customers be added through a stronger sales engine? Can churn be reduced? Can services be packaged into recurring revenue? Can one product be cross-sold into another lender segment? Can smaller competitors be acquired and integrated?

For Mortgage Services, private equity will usually be most attracted to businesses that combine three things: predictable revenue, mortgage-specific workflow depth, and clear room to grow without needing constant founder involvement.

3. Deep Dive: Software-Like Revenue vs Services-Heavy Revenue

One of the most important valuation questions in Mortgage Services is whether your business looks more like a software platform or a services business.

This does not mean services are bad. In mortgage technology, implementation, configuration, workflow design, compliance support, and managed services can be extremely valuable. The issue is whether services make the business stickier and more profitable, or whether they make it look like a labor-intensive consulting shop.

The transaction data supports this distinction. Private financial software and fintech platform transactions in the dataset generally cluster around lower revenue multiples than many public software peers, with private deal medians closer to around 1.0x revenue and average financial software/fintech platform deals around 1.5x revenue. However, where businesses have stronger earnings, embedded regulatory workflows, or bank-specific transformation capability, the EV/EBITDA multiples can be more compelling.

That tells founders something important: in this data set, premium valuation is not mainly about claiming to be "fintech." It is about proving that your revenue converts into durable profit and that your product or service is hard to replace.

A Mortgage Services company with a heavy project mix can still be attractive if projects lead to long-term customer relationships, repeat maintenance, recurring platform fees, or expansion into additional departments. But if every dollar of revenue requires custom work, senior founder involvement, and new delivery effort, buyers will usually apply a lower multiple.

If your business looks more like the left column today, you do not need to reinvent it in 6 months. But you can start moving it toward the right. Separate product revenue from services revenue. Document implementation steps. Turn recurring support into named subscription packages. Track retention by customer cohort. Show buyers that services are not just labor - they are a path to product adoption, retention, and expansion.

4. Deep Dive: Embedded Compliance and Credit Workflows

Another major valuation nuance is whether your business sits inside a high-consequence mortgage workflow.

Buyers pay more attention when a company supports decisions or processes that lenders cannot afford to get wrong. Examples include loan origination workflows, underwriting support, credit decisioning, compliance checks, regulatory reporting, servicing operations, payment workflows, document management, audit trails, and exception handling.

The premium drivers in the data point in this direction. Businesses positioned around banking digitization, lending, regulatory reporting, compliance, open banking, credit risk, decisioning software, and payment technologies tend to have stronger strategic appeal than generic IT services businesses. The reason is simple: these tools and capabilities are harder to replace.

In Mortgage Services, this matters because buyers are not just buying software screens or service capacity. They are buying trust. A lender that relies on your workflow for borrower documentation, loan status tracking, compliance evidence, underwriting exceptions, or servicing processes is less likely to switch casually.

This does not mean every compliance feature creates a premium. Buyers will test the claim. They will ask: do customers use it daily? Does it reduce real risk? Is it required for audits? Does it integrate with core lender systems? Does it create a record that helps the lender prove compliance? Do customers renew because of it?

Founders can improve this story by showing clear evidence. Track how many workflows are handled through your platform. Show renewal rates for customers using your compliance modules. Document customer references where your product reduced loan defects, lowered manual review time, improved audit readiness, or shortened cycle times.

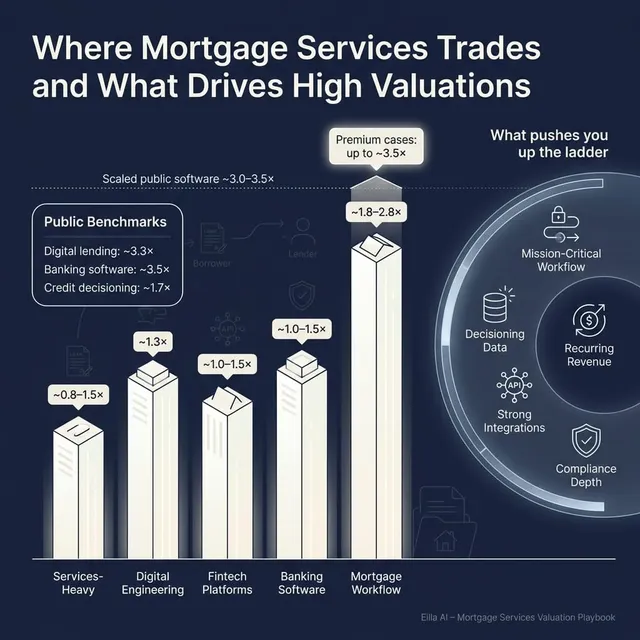

5. What Mortgage Services Businesses Sell For - and What Public Markets Show

Valuation data should be used carefully. Public companies are larger, more liquid, and usually more diversified than private founder-owned businesses. Private transactions are often affected by buyer strategy, competitive tension, deal structure, earnouts, customer concentration, and profitability.

Still, the data gives useful reference points. The key is to interpret it properly: public multiples help frame the market's view of scaled financial technology and lending software, while private transactions are often a better guide for what smaller privately held businesses can actually achieve.

5.1 Private Market Deals - Similar Acquisitions

The private deal set shows financial software, fintech platform, and digital engineering businesses transacting at much more moderate revenue multiples than the highest public fintech narratives might suggest.

Across the private precedent transactions, the overall average EV/Revenue multiple is about 1.4x, with a median of about 1.0x. For banking and financial software or fintech platforms, the average is about 1.5x revenue, with a median around 1.0x. Enterprise digital engineering and transformation software/services businesses show an average and median around 1.3x revenue.

On EBITDA, the private data is more interesting. The overall average EV/EBITDA multiple is about 11.4x, with a median around 12.3x. Banking and financial software/fintech platform deals average and median around 12.3x EBITDA. Enterprise digital engineering and transformation businesses average around 11.0x EBITDA.

That means founders should be careful about relying only on revenue multiples. In this dataset, the better valuation support often comes from earnings quality, not just top-line scale.

These ranges are illustrative. A small, services-heavy business with customer concentration may trade below these bands. A highly profitable, sticky, product-led mortgage workflow business with low churn and a strategic buyer process may trade above them.

5.2 Public Companies

Public market multiples are useful because they show how investors value scaled financial software, digital lending, credit decisioning, core banking, and related workflow platforms as of mid to late 2025. They are not direct price tags for private companies.

The public company data shows a much wider spread than the private deal data. Overall public EV/Revenue averages about 9.1x, but the median is only about 3.2x. That large gap tells you there are outliers. For founder valuation work, the median and relevant segment averages are usually more useful than the headline average.

The most relevant categories for Mortgage Services are digital lending origination, loan management and banking workflow software; banking core platforms and broad BFSI software suites; and AI-driven consumer and SME lending platforms or credit decisioning. These categories generally sit around low-to-mid single-digit revenue multiples on average or median, with EBITDA multiples varying widely based on profitability.

The banking core category shows a very high average EBITDA multiple because of outliers and differences in profitability. That is why the median is often the better guide. In simple terms, scaled public financial software businesses can trade around 3.0-3.5x revenue, while strong profitable platforms can support healthier EBITDA multiples.

For a private Mortgage Services founder, public multiples should be treated as reference bands, not automatic valuation outcomes. Buyers usually discount public multiples for smaller scale, customer concentration, lower liquidity, weaker reporting, and higher execution risk. But in rare cases, a private company can still command a premium if it is scarce, strategic, growing, profitable, and deeply embedded in lender workflows.

6. What Drives High Valuations - Premium Valuation Drivers

High valuations usually come from a combination of business quality, strategic relevance, and deal process tension. In Mortgage Services, the biggest premium drivers are not abstract. They show up in how buyers talk about risk, replacement difficulty, and future growth.

Mission-Critical Mortgage and Lending Workflows

Buyers pay more for businesses that sit inside workflows lenders rely on every day. That can include origination, underwriting support, servicing, compliance, regulatory reporting, payment workflows, credit risk, or document management.

The reason is simple: replacement risk is high. If your system helps a lender close loans, stay compliant, manage servicing, or make better credit decisions, switching away from you can be painful. Buyers see that as a sign of customer stickiness.

Examples include platforms that are used by operations teams daily, systems that create audit trails, or tools that reduce manual exceptions in underwriting or servicing.

Regulatory and Domain Expertise

Mortgage is heavily regulated. Buyers value teams that understand lender workflows, compliance rules, audit expectations, and the practical reality of mortgage operations.

This is different from being a generic software vendor. If your team can credibly speak the language of lenders, compliance officers, servicing teams, and operations leaders, that reduces buyer risk.

A strong premium story might include long customer relationships with regulated lenders, low compliance-related churn, strong documentation, and a product roadmap shaped by real mortgage workflow pain points.

API-First and Integration-Led Architecture

Mortgage Services businesses rarely operate in isolation. They often need to connect with loan origination systems, servicing systems, customer relationship tools, document providers, payment platforms, identity vendors, data providers, and bank systems.

Buyers care about integration because it lowers implementation risk. If your platform is easy to connect, easier to deploy, and well documented, it becomes more valuable to both customers and acquirers.

This driver only gets full credit if it is real. Buyers will not pay a premium just because the word "API" appears in a sales deck. They will look for live integrations, implementation timelines, partner relationships, documentation, and customer proof.

Proprietary Data and Decisioning Assets

Credit data, borrower behavior insights, risk scoring, decisioning logic, and performance data can increase valuation if they create a real advantage.

This is not the same as simply storing customer data. Buyers want to know whether your data improves outcomes, strengthens underwriting, reduces loss risk, increases approval quality, or creates a feedback loop competitors cannot easily copy.

A Mortgage Services company with genuine decisioning assets may attract a broader buyer universe than a workflow-only business. But the bar is higher. You need to prove the data advantage, not just describe it.

Demonstrated Profitability and Margin Quality

The private deal data shows that strong EBITDA support matters. In several relevant transactions, premium valuation logic was tied more to earnings quality than to revenue growth alone.

Buyers like businesses that can turn revenue into cash flow. That means clean gross margins, controlled delivery costs, efficient customer support, and a clear split between product revenue and service revenue.

For founders, this means margin reporting is not just accounting housekeeping. It is part of the valuation story.

Clean Financials and Predictable Revenue

A buyer can only pay for what they can understand. Clean monthly financials, clear revenue recognition, reliable customer reporting, and accurate margin data reduce uncertainty.

Predictable revenue also matters. Long-term contracts, high renewal rates, low churn, recurring platform fees, and stable servicing-related revenue all help buyers feel more confident.

The less uncertainty buyers feel, the less they will try to protect themselves through lower price, earnouts, holdbacks, or aggressive deal terms.

Diversified Customers and Strong Leadership Bench

A business with one or two very large customers can still be valuable, but buyers will discount concentration risk. They will ask what happens if the largest lender leaves, slows volume, or brings work in-house.

The same applies to founder dependence. If every major sale, implementation, customer escalation, or product decision depends on you, buyers will worry about transition risk.

A strong second layer of leadership can materially improve buyer confidence. It shows the business can survive and grow after closing.

7. Discount Drivers - What Lowers Multiples

Discount drivers are not always fatal. Many can be improved before a sale. But buyers will notice them, and if they are not addressed, they usually show up as lower valuation, tighter deal terms, or more deferred consideration.

The most common discount driver is low-quality revenue. If revenue is mostly project-based, unpredictable, or tied to one-time custom work, buyers will apply more conservative multiples. This is especially true if there is limited recurring revenue or weak visibility into the next 12 months.

Customer concentration is another major issue. If a large share of revenue comes from one lender, one channel partner, or one mortgage segment, buyers will worry about downside risk. They may still pursue the deal, but they will often structure around that risk.

Weak profitability also lowers valuation. In the public company data, some companies have high revenue multiples despite losses, but that is less reliable for private founder-owned businesses. In private M&A, buyers usually want to see either current profitability or a very clear path to it.

Other common discount drivers include:

For Mortgage Services specifically, buyers will also discount businesses that are overly exposed to refinance cycles, lack clear compliance controls, have weak cybersecurity practices, or cannot explain how revenue behaves when mortgage origination volume falls.

The best way to think about discount drivers is this: buyers do not need perfection, but they do need clarity. If you can name the issue, show data around it, and explain the plan, you are in a stronger position than a seller who ignores it.

8. Valuation Example: A Mortgage Services Company

This example is fictional. The company, revenue level, valuation range, and multiples are illustrative and designed to show how valuation logic works. This is not investment advice, and it is not a formal valuation.

Assume a fictional company called HarborPoint Mortgage Systems. HarborPoint has USD 10m of annual revenue. It provides workflow software and implementation support for mortgage lenders, including borrower intake, document management, underwriting workflow, compliance evidence, and servicing handoff tools.

The company has a mix of recurring software revenue and implementation revenue. It has strong lender relationships and good domain expertise, but it is not a pure high-growth SaaS company. It has some custom work, moderate customer concentration, and limited proof of proprietary credit data.

Step 1: Select the Relevant Valuation Anchors

The private transaction data suggests that banking and financial software or fintech platform deals often cluster around 1.0-1.5x revenue, with stronger EBITDA support around 12.3x. Enterprise digital engineering and transformation businesses are around 1.3x revenue and around 11.0x EBITDA.

The public market data suggests scaled digital lending and workflow software businesses trade around 3.2-3.3x revenue on average or median, with EBITDA multiples around the low-to-mid teens on a median basis.

HarborPoint is smaller and private, so it should not simply receive the public company multiple. But because it has product exposure, mortgage workflow relevance, and regulated lending specialization, it may deserve a premium to generic services-heavy businesses.

A reasonable illustrative revenue multiple range might be 1.8-2.8x revenue. The lower end reflects the private transaction data. The higher end reflects relevant public lending workflow software benchmarks, discounted for smaller scale, mixed revenue quality, and private company risk.

Step 2: Apply the Range to USD 10m Revenue

In the discounted case, HarborPoint has too much custom work, unclear retention data, weak margins, and high customer concentration. Buyers like the sector exposure, but they see execution risk.

In the base case, HarborPoint has credible mortgage workflow software, decent recurring revenue, solid lender relationships, and acceptable profitability. It is not a category-defining asset, but it is a real strategic business.

In the premium case, HarborPoint has high retention, clean financials, strong EBITDA margins, a clear API-first architecture, low customer concentration, and strong evidence that its software is embedded in lender compliance and servicing workflows. It may also have multiple strategic buyers who see immediate cross-sell potential.

Step 3: What This Means for Founders

Two Mortgage Services businesses with the same USD 10m of revenue can be worth very different amounts.

One may be worth closer to USD 12-17m if revenue is project-based, concentrated, low-margin, and hard to forecast. Another may be worth USD 30m+ if revenue is recurring, profitable, sticky, integrated into lender workflows, and supported by a competitive buyer process.

That is why valuation preparation matters. You are not only trying to grow revenue. You are trying to improve the quality, predictability, and strategic importance of that revenue.

9. Where Your Business Might Fit - Self-Assessment Framework

Use this framework as a rough self-check before going to market. Score each factor from 0 to 2.

A score of 0 means the issue is weak or not proven. A score of 1 means it is acceptable but not clearly premium. A score of 2 means it is a real strength that buyers would likely notice.

How to Interpret Your Score

If you score 13-16, you may be closer to a premium outcome, assuming buyers agree with the evidence. You likely have a strong story around predictable revenue, workflow depth, and strategic value.

If you score 8-12, you are probably in the fair market zone. You may still achieve a good result, but buyers will look closely at weaknesses, and process quality will matter a lot.

If you score below 8, you may have meaningful preparation work to do before launching a sale. That does not mean your business is not valuable. It means you may need to clean up reporting, reduce risk, improve margins, or sharpen the story before asking buyers to pay a strong multiple.

The goal is not to make yourself feel good or bad. The goal is to find the few improvements that can move valuation the most in the next 6-12 months.

10. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Many founders go to market before their numbers, story, customer data, and buyer list are ready. That usually leads to weaker buyer interest and more difficult diligence.

The second mistake is hiding problems. Every business has issues. Buyers expect that. What destroys trust is when issues appear late in due diligence after the seller has avoided them. If you have customer concentration, churn, margin pressure, compliance concerns, or technical debt, it is usually better to prepare the explanation early.

Weak financial records are another major value killer. If buyers cannot clearly see revenue by type, margin by product or service line, customer retention, implementation cost, and recurring revenue, they will protect themselves with lower offers. In Mortgage Services, you should be able to explain how much revenue is recurring, how much is project-based, how much is tied to mortgage volume, and how much is servicing or compliance-related.

A lack of a structured competitive sale process can also reduce valuation. Research and market experience often show that running a structured process with an advisor can lead to meaningfully higher purchase prices, often cited around 25%, because more qualified buyers are approached and competitive tension is created.

Another mistake is revealing the price you want too early. If you tell buyers you want USD 10m, do not be surprised when offers come back at USD 10.1m or USD 10.2m. You have anchored the market. A good process lets buyers show you what they are willing to pay before you narrow the range.

Mortgage-specific mistakes include underestimating compliance diligence and failing to explain mortgage cycle exposure. Buyers will want to know how your business performs when origination volume falls, when refinance activity slows, or when lenders tighten spending. If you have servicing, compliance, or recurring workflow revenue that offsets cyclicality, show it clearly.

11. What Mortgage Services Founders Can Do in 6-12 Months to Increase Valuation

You do not need to transform the entire business before a sale. But you can make targeted changes that reduce buyer uncertainty and strengthen the valuation story.

Improve the Numbers

Start by cleaning up financial reporting. Separate recurring software revenue, implementation revenue, managed services revenue, project revenue, and pass-through revenue. Show gross margin by revenue type.

Track monthly recurring revenue if applicable. Track churn, renewal rates, expansion revenue, customer concentration, and backlog. Buyers should not have to guess how predictable your revenue is.

Review pricing. Many founder-led businesses underprice legacy customers or give away high-value support. Even modest pricing discipline can improve margin and show buyers there is room for future growth.

Strengthen the Mortgage-Specific Story

Map exactly where your business sits in the mortgage workflow. Are you used before application, during origination, in underwriting, in closing, in servicing, in compliance, or across multiple stages?

Collect customer proof. Ask customers why they stay, what workflows you support, what systems you integrate with, and what risk or cost you reduce. These references can be powerful in a sale process.

Document compliance relevance. If your platform supports audit trails, regulatory reporting, borrower communications, document controls, exception workflows, or servicing evidence, make that clear and measurable.

Reduce Buyer Risk

Address customer concentration where possible. If one lender is too large a share of revenue, expand other accounts or build a credible pipeline that reduces the perceived risk.

Build the leadership bench. Buyers want to know the business can operate without you. Identify who owns sales, delivery, product, finance, customer success, and technology.

Clean up contracts. Make sure key customer agreements are signed, assignable where possible, and clear on pricing, renewal terms, service levels, data usage, and termination rights.

Improve Product and Integration Credibility

If your product is API-first, prove it. Prepare integration documentation, architecture diagrams, implementation timelines, and examples of live integrations.

Reduce custom delivery burden. Turn repeated implementation steps into templates. Create standard onboarding materials. Track average time to deploy.

Separate product roadmap from customer-specific work. Buyers like customer-led development, but they do not like a roadmap that is entirely controlled by one or two large customers.

Prepare the Sale Process Before Launch

Build a buyer universe early. Include strategic buyers, financial software platforms, mortgage technology companies, data and decisioning businesses, private equity-backed platforms, and services firms looking for mortgage domain expertise.

Prepare the story around why now is the right time. That might include market consolidation, lender digitization, compliance complexity, servicing demand, or customer demand for better automation.

Do not wait until buyers ask for diligence materials. Prepare financials, customer data, product materials, contracts, security documentation, and management presentations before outreach begins.

12. How an AI-Native M&A Advisor Helps

Selling a Mortgage Services business is not just about finding a buyer. It is about finding the right buyers, creating competition, framing the story properly, and helping buyers understand why your business matters inside the mortgage and lending ecosystem.

An AI-native M&A process can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, sector focus, product gaps, and likely synergies. More relevant buyers usually means more competition, stronger offers, and a better chance the deal closes because you are not dependent on one interested party.

AI can also speed up the early process. Buyer matching, outreach preparation, marketing materials, market mapping, diligence support, and data organization can move faster than a manual-only process. That can help founders reach initial conversations and offers in under 6 weeks when the business and materials are ready.

The best outcomes still require expert human judgment. Experienced M&A advisors help frame the business, prepare the numbers, manage buyer psychology, negotiate terms, and keep the process competitive. AI enhances that work by making the process broader, faster, and more data-driven.

For founders, the result is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how an AI-native process can support your exit, book a demo with one of Eilla AI's expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.