The Complete Valuation Playbook for Catering and Food Services Businesses

A practical guide to how catering and food service businesses are valued and what drives high multiples.

If you run a catering, foodservice distribution, meal services, or food logistics business, valuation can feel confusing. Some companies in the sector sell for less than 0.5x revenue. Others, especially specialist food suppliers, meal service platforms, or higher-margin category leaders, can trade at meaningfully higher levels.

Now is an important time to understand where your business fits. The catering and food services market is still consolidating, larger groups are looking for route density and category expansion, and buyers are paying close attention to margins, labor pressure, food inflation, contract quality, customer retention, and supply chain resilience.

This playbook is designed to show you what catering and food services businesses actually sell for, what drives higher or lower multiples, how buyers think about your company, and what you can do in the next 6-12 months to improve your exit outcome.

1. What Makes Catering and Food Services Unique

Catering and food services is not one single business model. It includes broadline foodservice distributors, contract caterers, meal service providers, specialty ingredient suppliers, event caterers, airline and travel catering, food logistics operators, and adjacent suppliers such as packaging or beverage businesses.

That matters because buyers do not value all of these businesses the same way. A low-margin regional distributor is usually valued differently from a specialist catering butcher, a branded prepared food manufacturer, a high-margin flavor house, or a contract catering business with long-term institutional customers.

At a simple level, this sector sits between food, logistics, hospitality, manufacturing, and services. That creates a wide valuation range. Buyers are not just asking, "How much revenue do you have?" They are asking, "How much of that revenue turns into reliable profit, how hard is it to replace you, and how much risk is hidden inside the operation?"

The main company types usually include:

The key valuation challenge is that many companies in the sector have high revenue but modest profit margins. Food costs, fuel, labor, refrigeration, waste, delivery density, and working capital all matter. A business can have USD 50m of revenue and still be worth less than another company with USD 20m of revenue if the smaller business has better margins, stronger customer contracts, and a more defensible niche.

Buyers will always check several sector-specific risks. They will look at customer concentration, supplier dependency, food safety processes, contract terms, route economics, labor availability, wastage, pricing power, and whether recent margin gains are real or temporary. They will also look closely at whether your growth came from profitable customers or simply from taking on more volume at thin margins.

2. What Buyers Look For in a Catering and Food Services Business

Buyers start with the basics: revenue size, revenue growth, EBITDA, gross margin, customer concentration, and cash flow. EBITDA is a common profit measure. In simple terms, it is profit before interest, tax, depreciation, and amortization, and buyers use it as a rough way to compare operating profitability across companies.

But in catering and food services, the basics are only the starting point. Buyers want to understand the quality of your revenue. A buyer will value USD 10m of repeat contracted meal service revenue differently from USD 10m of one-off event catering revenue. They will also value a sticky school, hospital, or corporate catering contract differently from a customer list that can disappear quickly if pricing changes.

Buyers also care about the mix of services. If you are just moving boxes from supplier to customer, you may be seen as more replaceable. If you provide menu development, specialist food preparation, culinary support, reliable last-mile delivery, branded products, or hard-to-replicate local relationships, you may be seen as more strategic.

Strategic buyers, such as larger foodservice groups, distributors, caterers, or food manufacturers, usually ask: "Can this business strengthen our existing platform?" They care about route density, procurement savings, customer overlap, new territories, category expansion, and whether they can plug your operation into their existing infrastructure.

Private equity buyers ask a slightly different question: "Can we buy this business today, improve it, and sell it for more in 3-7 years?" That means they care about the price they pay on entry, the multiple they might achieve on exit, and the practical levers they can pull to grow EBITDA.

How Private Equity Buyers Think

Private equity buyers usually focus on three things.

First, they ask whether the entry multiple is sensible. If they buy your company at too high a valuation, they need a very strong growth story to make the investment work.

Second, they ask who might buy the business from them later. That could be a larger strategic buyer, a larger private equity fund, or in rare cases a public market exit. If your business is too small, too local, or too dependent on the founder, the future buyer universe may be limited.

Third, they look for practical value creation levers. In this sector, those levers often include price increases, purchasing savings, better route planning, cross-selling to existing customers, adding specialty categories, improving labor scheduling, reducing waste, and acquiring smaller local competitors.

That is why the best-positioned businesses usually have both stability and improvement potential. Buyers want evidence that the company is strong today, but they also want to believe there is a clear path to making it better.

3. Deep Dive: Why Margin Quality Matters More Than Revenue Size

In catering and food services, revenue can be misleading. This is one of the most important valuation lessons in the sector.

A distributor with USD 80m of revenue but a 2% EBITDA margin may not be more valuable than a specialist supplier with USD 25m of revenue and a 15% EBITDA margin. The first business has more sales, but the second business may convert far more of each dollar into profit.

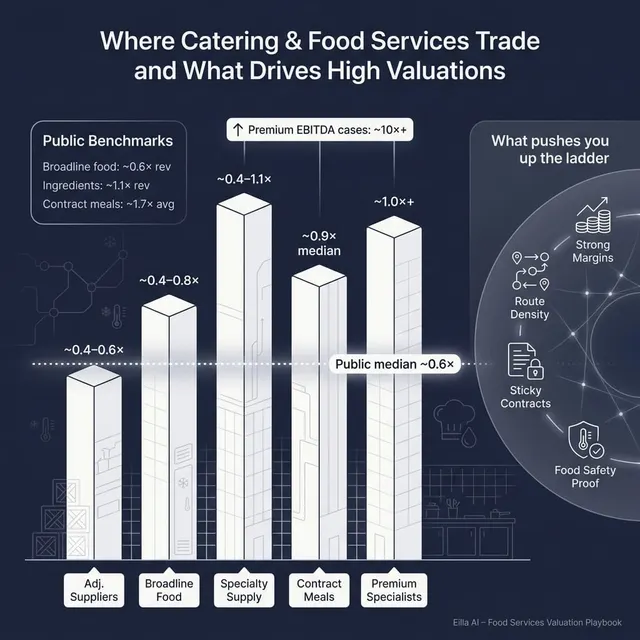

The source data shows this clearly. Broadline foodservice and catering distributors typically traded around 0.6x revenue in the private transaction data. Foodservice-focused specialty suppliers also averaged around 0.6x revenue, but their EBITDA multiples were much higher, with average EV/EBITDA around 17.7x and median around 10.3x. That tells an important story: buyers may pay more for profit quality, specialist capability, and differentiated margin structure than for revenue alone.

For founders, the key question is not just "How big are we?" It is "How valuable is each dollar of revenue?" Buyers pay more when they believe your revenue is repeatable, profitable, defensible, and capable of growing without breaking the operating model.

This is especially important when food inflation has helped increase top-line revenue. If revenue went up because prices rose, but margins did not improve, buyers may not give you much credit. If revenue grew while gross margin and EBITDA margin also improved, that is much more compelling.

If your business looks more like the left column today, you do not need to reinvent it overnight. The 6-12 month opportunity is to prove which customers, routes, menus, categories, and contracts are actually profitable. Then you can focus growth around the parts of the business buyers will value most.

4. What Catering and Food Services Businesses Sell For - and What Public Markets Show

The valuation data points to a simple conclusion: most catering and food services businesses are not valued like technology companies. Revenue multiples are often modest because many companies operate with low margins, high working capital needs, and operational complexity.

But the range is wide. Businesses with specialist capabilities, strong market positions, contract visibility, differentiated products, or unusually high margins can move meaningfully above generic distributor levels.

4.1 Private Market Deals (Similar Acquisitions)

The private transaction data shows that broadline foodservice and catering distributors typically transact around 0.6x revenue on average and around 0.7x revenue at the median. The disclosed EBITDA data is less complete for broadline distributors, so revenue multiples are often more useful for initial benchmarking.

Foodservice-focused specialty suppliers and ingredient providers also show average and median revenue multiples around 0.6x. But the EBITDA multiples are higher, with average EV/EBITDA around 17.7x and median around 10.3x. This suggests that specialist businesses can command stronger profit-based valuations when buyers believe the earnings are defensible.

Adjacent foodservice operators, packaging suppliers, and beverage producers were closer to 0.5x revenue on average and median, with EBITDA multiples around 6.8x. These businesses can be attractive, but valuation depends heavily on profitability, repeat demand, brand strength, and whether the business is strategic to the buyer.

These ranges are illustrative, not automatic. A regional distributor with improving margins may sit in the lower-to-mid range. A category leader with strong profitability, proprietary products, and clear strategic buyer fit may justify a higher outcome.

Deal size also matters. Larger businesses with stronger systems, management teams, and customer diversification usually face less buyer risk. Smaller founder-led companies often receive a discount unless they have unusually strong margins, a niche position, or a clear strategic reason for a buyer to pay up.

4.2 Public Companies

Public company multiples provide a useful reference point, but they are not a direct price tag for private companies. Public companies are usually larger, more diversified, better financed, and easier for investors to buy and sell. Smaller private companies often trade at a discount to public market averages.

As of the mid to end 2025 data provided, the overall public company set traded around 1.0x average EV/Revenue and 11.3x average EV/EBITDA, with medians of 0.6x EV/Revenue and 8.0x EV/EBITDA. That median is often more helpful than the average because a few high-growth or high-margin businesses can pull the average upward.

The public data also shows major differences by segment.

Contract catering and meal services show the highest average EV/Revenue in the public set at around 1.7x, but the median is much lower at around 0.9x. That gap means a few high-performing or strategically unusual companies can lift the average. Founders should not assume every catering business deserves the average.

Broadline foodservice distribution is a more grounded reference for many private companies in this sector. The public bucket averages around 0.6x revenue and around 8.0x EBITDA. That lines up reasonably well with the private deal data for broadline foodservice and catering distributors.

The right way to use public multiples is as a reference band. If your business is smaller, lower-growth, founder-dependent, or margin-challenged, buyers will usually adjust downward. If your business has scarce strategic value, high customer retention, strong contracts, high margins, or a unique category position, it may push upward.

5. What Drives High Valuations (Premium Valuation Drivers)

High valuations are rarely random. Buyers pay more when they see proof that the business is larger, stronger, safer, or more strategic than the average company in the sector.

The premium drivers below reflect patterns from the transaction data and broader M&A practice in catering and food services.

5.1 Margin Expansion and Earnings Inflection

Buyers like businesses that are getting more profitable, not just bigger. If your revenue is growing but margins are falling, buyers worry that growth is being bought through discounts, poor pricing, or weak cost control.

A strong story is different: revenue grows, gross margin improves, and EBITDA turns upward. That suggests the business has better pricing discipline, improved purchasing, stronger route economics, tighter labor control, or a better customer mix.

Practical examples include:

- Passing through food cost inflation in a disciplined way

- Cutting unprofitable customers or routes

- Improving delivery density

- Reducing kitchen waste

- Tracking margin by menu, customer, site, or category

A recovery story can help close the discount to peers. But to earn a true premium, buyers usually need to see that the improvement is structural, not just a one-year rebound.

5.2 Regional Leadership and Route Density

In foodservice, local scale matters. A distributor with strong density in a region can serve customers faster, use trucks more efficiently, and build deeper customer relationships. A contract caterer with a strong base in schools, hospitals, or corporate campuses can build local labor pools and operating know-how.

Buyers care because regional density is hard to build quickly. It can take years to build supplier trust, customer relationships, delivery routes, food safety systems, and local brand reputation.

But there is a difference between presence and leadership. Saying "we operate in three regions" is not the same as proving you are the strongest or most profitable player in those regions. Buyers will want evidence such as customer share, repeat order rates, route profitability, retention, and local reputation.

5.3 Strategic Fit With the Buyer

A business can be worth more to one buyer than another. This is especially true in catering and food services.

A regional distributor may be more valuable to a larger group trying to fill a geographic gap. A specialist meat, bakery, beverage, or ingredients supplier may be valuable to a company trying to deepen its category offering. A contract caterer with healthcare clients may be attractive to a buyer already serving hospitals and senior living facilities.

Strategic fit becomes more powerful when the buyer can clearly see the benefit:

- Better truck utilization

- Procurement savings

- Cross-selling existing products into your customer base

- Access to a new region

- Entry into a specialist category

- A stronger position with national accounts

Founders often overestimate "synergies." Buyers only pay for synergies they believe they can actually capture.

5.4 Specialist Capabilities and Value-Add Services

The data shows that category-specialist, value-add models can earn stronger outcomes than plain distribution businesses. The reason is simple: they are harder to replace.

A specialist supplier that helps chefs develop menus, creates proprietary products, offers food development support, or provides technical expertise may be seen as more than a logistics provider. It may be seen as part of the customer’s operating model.

Examples include:

- Bespoke flavor or ingredient formulation

- Premium butchery or protein expertise

- Menu innovation support

- Chef education or training

- Product development for foodservice customers

- Prepared meal or ready-to-use solutions

The more you help customers make money, save labor, or improve quality, the more valuable the relationship becomes.

5.5 High-Margin Products, Brands, or Intellectual Property

Revenue multiples expand when revenue quality is unusually high. In this sector, that often means branded products, proprietary recipes, specialist formulations, prepared foods, or unique supply relationships.

A business that simply resells commodity products is more exposed to price pressure. A business that owns a product, brand, recipe, or specialist capability has more control over margin.

This does not mean every founder needs to build a national food brand. But even modest owned-label products, signature menus, preferred supplier programs, or proprietary preparation processes can improve the buyer narrative if they create measurable margin and retention benefits.

5.6 Clean Financials and Strong Management

Even if this is not always visible in headline deal data, it matters in every sale process.

Buyers pay more when they trust the numbers. That means clean monthly accounts, clear revenue recognition, reliable margin reporting, customer-level profitability, and a management team that can explain the business without the founder answering every question.

A strong leadership bench also reduces buyer risk. If the buyer believes the company will struggle after you leave, valuation suffers. If they believe the team can run the business and keep improving it, the business becomes much easier to buy.

6. Discount Drivers (What Lowers Multiples)

Not every business in catering and food services deserves a premium multiple. Many sell at the lower end because buyers see risks that reduce confidence in future profit.

The first major discount driver is low or unstable margins. If EBITDA margin is thin, volatile, or unclear, buyers may rely more heavily on conservative revenue multiples. They may also question whether earnings are sustainable after food costs, labor costs, fuel, and customer pricing pressure are fully reflected.

The second discount driver is commodity positioning. If customers view you mainly as a replaceable supplier, buyers will worry about pricing power and retention. This is common in plain resale models where the buyer does not see proprietary products, strong contracts, or deep service integration.

The third discount driver is small scale and geographic concentration. A regional business can still be attractive, but buyers will discount it if it is too dependent on one area, one customer type, or a small number of key accounts.

Other common discount drivers include:

Food safety and compliance deserve special attention. In this sector, a buyer will usually check hygiene standards, cold chain controls, allergen processes, incident history, certifications, insurance, and supplier quality. A problem here can reduce valuation quickly, even if the financials look strong.

The good news is that many discount drivers can be improved. You may not be able to triple your revenue in 12 months, but you can clean up reporting, improve margin visibility, reduce customer concentration, strengthen contracts, document food safety processes, and build a more credible management story.

7. Valuation Example: A Catering and Food Services Company

This example is fictional. The company, revenue level, multiples, and valuation ranges are illustrative only. This is not investment advice, not a formal valuation, and not a fairness opinion.

Imagine a fictional company called NorthBridge Foodservice, a regional catering and foodservice distributor with USD 10m of revenue. It serves independent restaurants, schools, event caterers, and small hospitality groups across a defined regional territory.

NorthBridge has a broad product catalog, daily delivery routes, a good local reputation, and improving profitability. It is not a software platform. It is not a high-margin branded food manufacturer. It is a traditional foodservice distributor with some value-add services.

Step 1: Select the Right Comparable Set

The first mistake would be to compare NorthBridge to high-growth technology companies or global branded food giants. That would overstate value.

The better starting point is the distribution and catering-related transaction data:

- Broadline foodservice and catering distributors averaged around 0.6x revenue

- Specialty suppliers and ingredient providers also averaged around 0.6x revenue, but can earn higher EBITDA multiples when differentiated

- Adjacent foodservice operators and suppliers averaged around 0.5x revenue

- Public broadline foodservice distribution traded around 0.6x average EV/Revenue and around 8.0x average EV/EBITDA

Because NorthBridge is a smaller private company, the public company range should be adjusted down unless there are clear premium drivers.

Step 2: Narrow the Core Multiple Range

For a traditional regional foodservice distributor, a reasonable core revenue multiple range might be around 0.3x-0.5x revenue. This is consistent with the logic in the source data for a regional distributor with positive EBITDA, but without strong evidence of premium specialist capabilities.

On USD 10m of revenue, that creates a base enterprise value range of roughly USD 3m-5m.

If NorthBridge has stronger traits, such as high gross margin, improving EBITDA, strong route density, contracted customers, and a clear strategic fit for multiple buyers, the multiple could move higher. If it has weak margins, poor reporting, heavy founder dependence, or customer concentration, the multiple could move lower.

Step 3: Cross-Check With EBITDA

Revenue multiples are useful in this sector, but EBITDA matters because buyers ultimately care about cash profit.

Assume NorthBridge has USD 10m of revenue and a 5% EBITDA margin. That means USD 0.5m of EBITDA. If a buyer applied a 6.5x-9.0x EBITDA range, the implied enterprise value would be around USD 3.3m-4.5m.

That cross-check supports the base revenue multiple range. If the revenue multiple suggests USD 8m but EBITDA supports only USD 4m, buyers will challenge the valuation unless there is a very strong growth or margin expansion story.

Illustrative Valuation Table

The premium specialist case is not automatic. To reach it, NorthBridge would need to look less like a commodity distributor and more like a differentiated foodservice platform. That could mean high-margin specialty categories, strong contracts, clear route density, proprietary products, menu support, or a compelling strategic fit for several buyers.

The lesson is simple: two companies with the same USD 10m of revenue can be worth very different amounts. A low-margin, customer-concentrated distributor may be valued near the lower end. A higher-margin, specialist, sticky, well-run business with multiple strategic buyers may be worth much more.

8. Where Your Business Might Fit (Self-Assessment Framework)

Use this framework as a rough self-assessment, not as a formal valuation. Score each factor from 0 to 2.

A score of 0 means weak or unclear. A score of 1 means acceptable. A score of 2 means strong and well evidenced.

Add up your score out of 18.

Be honest with yourself. The goal is not to create a flattering score. The goal is to identify which improvements could move the valuation needle before you go to market.

If your score is low because of messy financials, weak reporting, or unclear margins, that can often be improved within 6-12 months. If your score is low because the business has no differentiation, no contracts, and heavy customer concentration, the improvement plan may take longer.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Many founders wait until they are tired, under pressure, or already speaking to one buyer. That usually leads to weaker preparation and less competition.

Before going to market, you need clean numbers, a clear story, a buyer list, a process plan, and answers to obvious buyer questions. If you skip that work, buyers will discover the gaps and price in risk.

The second mistake is hiding problems. If you have customer concentration, margin pressure, food safety incidents, supplier issues, or messy accounting, these issues will come out during diligence. Hiding them destroys trust and can lead to price cuts, delayed closing, or a failed deal.

The third mistake is weak financial records. This is especially damaging in catering and food services because buyers need to understand gross margin, EBITDA, inventory, waste, route profitability, customer profitability, and working capital. If you cannot show those clearly, buyers will usually assume more risk.

The fourth mistake is not running a structured, competitive sale process. Research and market experience show that a structured process with an advisor can lead to meaningfully higher purchase prices, often around 25%, because multiple buyers compete and price discovery improves. One buyer is not a market. It is just one buyer’s opinion.

The fifth mistake is revealing the price you want too early. If you tell buyers you want USD 10m, many will anchor around USD 10.1m or USD 10.2m, even if they might have paid more. Let the market come back with offers. That is how you discover the real buyer ceiling.

Industry-specific mistakes also matter. One is failing to separate profitable and unprofitable revenue. If you show only total revenue, buyers may worry that growth is hiding weak routes, low-margin customers, or poor pricing. Another is under-documenting food safety, cold chain, allergen, and compliance processes. In this sector, operational risk can become valuation risk very quickly.

10. What Catering and Food Services Founders Can Do in 6-12 Months to Increase Valuation

You do not need to transform the whole business before a sale. But you should focus on the changes buyers will actually reward.

Improve the Numbers

Start by improving margin visibility. Break down revenue and gross margin by customer, category, route, contract, and site where possible. Buyers want to know which parts of the business are attractive and which parts are dragging performance down.

Then look for practical margin improvements:

- Reprice low-margin accounts

- Add fuel or delivery surcharges where appropriate

- Reduce waste and spoilage

- Improve route density

- Tighten labor scheduling

- Renegotiate supplier terms

- Push higher-margin specialty categories

Even modest EBITDA improvement can matter. If a buyer values your business at 7x EBITDA, every additional USD 100k of sustainable EBITDA could theoretically support USD 700k of enterprise value, before other adjustments.

Strengthen Revenue Quality

Buyers pay more for revenue that is likely to stay. Focus on contract length, renewal history, order frequency, customer retention, and share of wallet.

If you have recurring institutional customers, long-term school or healthcare contracts, corporate catering agreements, or repeat foodservice accounts, document them clearly. If too much revenue is one-off event work, show repeat event history, pipeline visibility, and customer rebooking rates.

Also reduce customer concentration where possible. If your largest customer represents too much revenue or EBITDA, buyers will discount the business unless the relationship is very secure.

Build a Better Buyer Story

Your story should explain why the business is not just another catering or distribution company.

That might include:

- A strong regional position

- Dense delivery routes

- A high-retention customer base

- A specialist category

- Strong food safety processes

- Proprietary menus or products

- High-margin value-add services

- A management team that can run the business without you

The story has to be backed by data. Buyers do not pay for claims. They pay for proof.

Prepare the Business for Diligence

Create a clean data room before buyers ask for it. Include financial statements, monthly management accounts, customer data, supplier lists, contracts, insurance, food safety records, employee information, lease details, fleet data, and key operating metrics.

Fix obvious issues early. If your inventory process is messy, clean it up. If customer contracts are unsigned or outdated, organize them. If food safety documentation is scattered, centralize it. If management reporting is weak, improve it before you launch a process.

Reduce Founder Dependence

If every major customer relationship, supplier negotiation, and operational decision runs through you, buyers will see risk.

In the next 6-12 months, start shifting responsibility to your senior team. Document key processes. Let managers lead customer reviews. Build reporting routines that do not depend on you personally.

A business that can run without the founder is usually easier to sell and easier to value.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor like Eilla AI can help founders run a broader, faster, and more competitive sale process without losing the human judgment that matters in a high-stakes transaction.

The first advantage is broader buyer reach. AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, geography, category focus, and likely synergies. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes because you have more options if one buyer drops out.

The second advantage is speed. AI-driven buyer matching, outreach support, marketing material creation, and due diligence preparation can help founders reach initial conversations and offers in under 6 weeks. That does not mean rushing the process. It means reducing manual bottlenecks that often slow traditional M&A work.

The third advantage is expert advisory enhanced by AI. You still need experienced human M&A advisors who know how to position the business, negotiate with buyers, create tension, and protect value. AI improves the process by helping advisors prepare better materials, analyze buyer fit faster, and frame the company in language acquirers understand.

The outcome is Wall Street-grade advisory quality without traditional "bulge bracket" costs. If you would like to understand how an AI-native process can support your exit, book a demo with one of Eilla AI’s expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.