The Complete Valuation Playbook for Billing and Subscription Software Businesses

A practical guide to how billing and subscription software businesses are valued and what drivers high multiples

Billing and subscription software sits at a valuable point in the software market: close to revenue, close to payments, and close to customer retention. When a platform helps companies price, invoice, collect, renew, bundle, or manage subscriptions, it often becomes part of the financial operating system of the customer.

Now is an important time to think seriously about valuation. Subscription models are everywhere, but buyers are becoming more selective. They still like recurring revenue, usage-based pricing, payments data, and embedded workflows, but they are less willing to pay premium multiples for businesses that look service-heavy, customized, low-margin, or hard to scale.

This playbook shows what billing and subscription software businesses actually sell for, how public market multiples create valuation reference points, what pushes a company toward the high or low end of the range, and what you can do in the next 6-12 months to improve your outcome.

1. What Makes Billing and Subscription Software Unique

Billing and subscription software companies are not valued like generic software companies. Buyers do not only ask, "How much revenue do you have?" They ask, "How close are you to the customer's revenue engine?"

The sector includes several types of businesses:

The strongest companies in this sector usually combine recurring software revenue, high customer retention, and deep integrations into systems like payment processors, commerce platforms, enterprise resource planning tools, accounting software, customer relationship management systems, and tax engines.

The key valuation question is simple: are you a scalable software platform, or are you a services business wrapped in software?

Buyers will always test that question. They will look at how much revenue is truly recurring, how much work is needed to onboard each customer, how much support each customer requires, whether billing rules are standardized or heavily customized, and whether the platform can grow without hiring lots of people.

They will also check risk factors that are specific to billing and subscription software. These include billing accuracy, failed payments, compliance with tax and consumer subscription rules, payment security, customer data handling, churn, revenue recognition, and dependency on a small number of payment or commerce partners.

2. What Buyers Look For in a Billing and Subscription Software Business

Most buyers start with the obvious factors: revenue scale, growth, profitability, gross margin, customer concentration, and retention. But in billing and subscription software, those numbers only tell part of the story.

A company growing 25% per year with 85% gross margin and low churn will be viewed very differently from a company growing 25% per year with heavy implementation work, customer-specific code, and weak renewal data.

Buyers want to understand whether your software helps customers make money, collect money, or avoid losing money. Billing is close to all three. If your platform reduces failed payments, automates renewals, manages complex subscription plans, handles tax or compliance rules, or supports multi-channel commerce, it can be seen as more strategic than a back-office tool.

Strategic buyers often ask, "What can we do with this asset that the founder cannot do alone?" They may see value in adding your product to a larger commerce suite, payments platform, accounting system, customer engagement platform, or enterprise software ecosystem.

Private equity buyers think slightly differently. They usually ask:

- Can we buy this business at a fair entry multiple?

- Can we grow it for 3-7 years?

- Can we sell it later to a larger strategic buyer, another private equity firm, or potentially the public markets?

- Can we improve pricing, cross-sell more products, reduce churn, improve margins, or acquire smaller competitors?

A private equity buyer does not only buy the company you have today. They buy the company they believe they can create. That is why clean data, a clear growth plan, and a strong management team matter so much.

3. Deep Dive: Embedded Billing Infrastructure vs Service-Heavy Enablement

The most important valuation nuance in this sector is the difference between embedded infrastructure and service-heavy enablement.

Both businesses may describe themselves as "subscription platforms." Both may help customers manage billing, payments, or commerce operations. But buyers value them very differently.

Embedded infrastructure means your product sits inside the customer's daily workflow. It connects to payment systems, accounting tools, customer databases, commerce platforms, tax engines, and subscription plans. If the customer removes your software, billing breaks, reporting becomes messy, or revenue collection gets worse.

Service-heavy enablement means your company helps customers operate better, but much of the value comes from people, manual support, custom work, or outsourced operations. That can still be a good business, but it usually receives lower software valuation multiples because it is harder to scale.

The source data shows this clearly. Higher private transaction outcomes were associated with software platforms that were deeply integrated into merchant workflows, API-driven, multi-endpoint, high gross margin, and strategically useful to acquirers. Lower outcomes appeared where the business looked more operational, fulfillment-heavy, or service-led.

If your business looks more like the left column today, that does not mean you cannot sell. It means you need to be honest about how buyers will see it.

The practical path is to move more revenue toward repeatable software. Package implementation work. Reduce one-off customization. Track gross margin by revenue type. Build integrations that make the platform harder to replace. Show that customers expand over time, not just renew.

In billing and subscription software, the highest valuation argument is not "we do many things." It is "we do important things that are hard to remove."

4. What Billing and Subscription Software Businesses Sell For - and What Public Markets Show

Valuation multiples in this sector vary widely. The reason is that "billing and subscription software" overlaps with several related categories: subscription management, commerce platforms, payment infrastructure, order management, customer engagement, and service-enabled commerce operations.

The right way to use multiples is not to pick the highest number in the data and apply it to your revenue. The right way is to identify which group your business most closely resembles, then adjust up or down based on growth, margin, retention, strategic value, and risk.

4.1 Private Market Deals - Similar Acquisitions

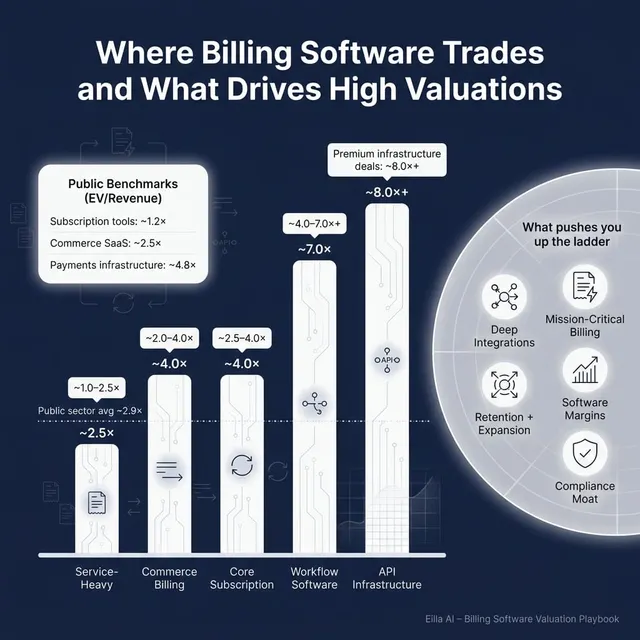

The private transaction data shows a wide spread. Across the precedent transaction set, the overall average EV/Revenue multiple was about 5.6x, while the median was closer to 2.2x. That gap matters. It tells you that a few strong premium deals pulled the average upward, while many more normal deals happened at more moderate levels.

For businesses most similar to billing, subscription, and commerce management software, the relevant private deal ranges are often more grounded. Retail and commerce management software transactions averaged around 3.8x revenue, with a median near 2.2x revenue. E-commerce operations, fulfillment, and logistics software or services showed a higher average around 8.2x revenue, but that group includes some unusually strategic, high-growth, or high-margin assets.

The highest private multiples were linked to businesses that looked like infrastructure: platforms with deep integrations, broad customer reach, high gross margin, and a clear role in mission-critical workflows. Lower multiples were linked to businesses that had operational breadth but less evidence of scalable software economics.

For founders, the key message is this: the headline range is wide, but the buyer's logic is usually consistent. The more your company looks like repeatable, embedded, high-margin software, the more likely it is to land toward the upper end.

4.2 Public Companies

Public company multiples are useful, but they are not direct price tags for private businesses. Public companies are usually larger, more liquid, better known, and easier for investors to buy and sell. Private companies are typically discounted for smaller scale, lower disclosure, customer concentration, and execution risk.

As of mid to end 2025, the public comparable groups around billing, subscription, commerce, and payments showed the following average multiples:

Several patterns stand out.

Payment-adjacent and risk infrastructure companies can trade at higher revenue multiples because they are close to transaction flow. E-commerce operations software can also trade well when it automates important workflows across orders, inventory, fulfillment, billing, or merchant operations. Subscription management alone does not automatically command a premium unless it is growing, sticky, profitable, and deeply embedded.

Founders should use public multiples as reference bands, not as valuation answers. If a public group trades at 3.0x revenue, a smaller private company may sell below that if it has lower growth, higher churn, weaker margins, or more customer concentration. But a scarce private asset can trade above public averages if it is strategically important, growing quickly, and hard to replicate.

5. What Drives High Valuations - Premium Valuation Drivers

Premium valuations happen when buyers believe your business is not just good, but scarce. In billing and subscription software, scarcity usually comes from infrastructure value, high retention, clean software economics, and strategic relevance to larger platforms.

Deep API and Integration Infrastructure

Buyers pay more when your product connects deeply into the systems your customers already use. Integrations with payment processors, accounting tools, commerce platforms, tax engines, customer databases, and enterprise software make your platform harder to remove.

This matters because billing is not isolated. A subscription business needs billing data to connect with finance, customer success, payments, reporting, tax, and revenue operations. If your platform becomes the connective tissue across those systems, buyers see stronger retention and better strategic value.

A weak version of this driver is "we have integrations." A strong version is "customers rely on our integrations every day to run billing, collections, renewals, and reporting."

Mission-Critical Workflow Position

The closer your software sits to revenue collection, the more strategic it becomes. Buyers care about whether customers would suffer real pain if your product disappeared.

For example, a dashboard that shows subscription data may be helpful. A platform that calculates invoices, manages plan changes, retries failed payments, handles tax logic, and syncs revenue data into finance systems is much harder to replace.

The highest-value billing platforms are not just tools. They become systems of record for subscription revenue.

High Gross Margin and Scalable Delivery

Gross margin is one of the clearest signs of whether your company is software-like. If each new customer requires heavy manual work, custom development, or a large support burden, buyers will discount the business.

Premium buyers like platforms where new revenue can be added without adding the same level of cost. That does not mean services are bad. Implementation, support, and migration help can improve customer success. But they should support the software business, not define it.

A clean story sounds like this: "Services help customers go live, but the long-term value and margin come from recurring software."

Strong Retention and Expansion

Buyers care about whether your customers stay and pay more over time. This is especially important in billing and subscription software because the product should naturally grow with the customer's subscriber base, payment volume, product catalog, or billing complexity.

If your customers add more plans, more geographies, more payment methods, more users, or more transaction volume over time, you may have a built-in expansion engine.

Founders should be ready to show renewal rates, customer churn, revenue retention, expansion revenue, and examples of customers that grew their spend after adoption.

Compliance, Tax, and Localization Complexity

Billing and subscription businesses often face messy rules: tax, invoicing, payment regulations, cancellation rules, data privacy, regional billing requirements, and consumer subscription laws.

Compliance can support a premium when it creates real switching costs. If your platform helps customers avoid billing errors, tax mistakes, failed compliance checks, or payment risk, it can make the software more valuable.

But compliance alone is usually not enough. Buyers will ask whether it is proprietary, widely used, monetized, and connected to customer retention.

Strategic Fit with Larger Platforms

A billing and subscription software company can be more valuable to a strategic buyer than to a financial buyer if it fills a gap in a larger ecosystem.

Potential acquirers may include commerce platforms, payment companies, accounting software providers, customer engagement platforms, enterprise software vendors, or subscription management suites. If your product helps them win more customers, reduce churn, or expand into a new market, they may pay more than a buyer looking only at current revenue.

The strongest strategic stories are specific. "We help merchants manage recurring revenue across payment, commerce, and finance systems" is stronger than "we are a subscription software company."

Clean Financials and Leadership Depth

Even a strong product can lose value if the financial story is messy. Buyers want clean revenue recognition, clear gross margin by revenue type, accurate churn reporting, and reliable monthly financials.

They also want to know the company can run without the founder making every decision. A strong second layer of leadership reduces risk and makes buyers more comfortable paying up.

6. Discount Drivers - What Lowers Multiples

Discounts happen when buyers see risk, uncertainty, or lower scalability. Most discount drivers are fixable, but only if you address them before a sale process starts.

The most common discount driver is unclear recurring revenue quality. If a large share of revenue comes from one-time implementation, custom projects, or manual services, buyers will not value it like pure software revenue.

Customer concentration is another major issue. If a few customers represent a large share of revenue, buyers worry that losing one account could change the business overnight. This risk is even bigger if those customers have short contracts or weak renewal histories.

Churn also matters. A billing platform should be sticky. If customers leave often, buyers will ask whether the product is truly mission-critical or whether it is being replaced by better platforms.

Other major discount drivers include:

In this sector, one extra discount driver is billing accuracy risk. If buyers find invoice errors, failed payment problems, poor reconciliation, or weak controls around customer money movement, they will be cautious.

Another sector-specific issue is platform dependency. If your product depends heavily on one payment processor, commerce platform, tax provider, or marketplace, buyers may discount the business because a partner change could damage revenue.

7. Valuation Example: A Billing and Subscription Software Company

This example is fictional. The company, revenue level, valuation range, and multiples are illustrative only. This is not investment advice, and it is not a formal valuation.

Assume a fictional company called LedgerLoop Billing has USD 10m of revenue. LedgerLoop helps mid-market software and commerce companies manage subscription billing, usage-based pricing, payment retries, tax logic, renewals, and finance system integrations.

Step 1: Select the Relevant Valuation Anchors

For LedgerLoop, we would not use only pure subscription management public comps. We would also look at nearby categories: commerce platforms, e-commerce operations software, merchant payments and risk infrastructure, and customer engagement platforms.

The public market data suggests broad revenue multiple reference points from roughly 1.0x to 5.0x depending on segment quality, with stronger categories such as payments-adjacent infrastructure and e-commerce operations trading higher on average.

The private transaction data suggests that normal commerce management software often lands closer to the low-to-mid single-digit revenue multiple range, while very strategic, high-margin, deeply integrated software infrastructure can push materially higher.

Step 2: Apply a Core Range

If LedgerLoop is a solid but not elite business, a defensible core range might be 2.5-4.0x revenue.

On USD 10m of revenue, that implies:

A core case would fit a company with good recurring revenue, useful integrations, moderate growth, decent margins, and a real role in customer billing workflows, but not yet proof of elite retention, very high growth, or unusual strategic scarcity.

Step 3: What Could Push It Up?

LedgerLoop could move toward the strong or premium case if it has:

- High recurring software revenue

- Gross margin that looks like software, not services

- Strong net revenue retention, meaning existing customers spend more over time

- Low churn

- Deep integrations into payments, commerce, tax, accounting, and finance systems

- Clear evidence that customers use it as core billing infrastructure

- A credible strategic buyer universe

In that case, buyers may stop viewing the company as a small billing tool and start viewing it as embedded revenue infrastructure.

Step 4: What Could Push It Down?

LedgerLoop could fall into the discounted case if it has:

- Heavy customer-specific implementation work

- Low gross margin

- Weak churn data

- Limited integrations

- High customer concentration

- Unclear revenue recognition

- Dependency on one payment partner or commerce platform

- A founder-led sales and product process with little management depth

This is why two companies with the same USD 10m of revenue can be worth very different amounts. Revenue is the starting point. Revenue quality, growth, margin, retention, and strategic fit drive the actual valuation.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a simple gut-check before starting a sale process. Score each factor from 0 to 2.

- 0 = weak or not proven

- 1 = decent but needs work

- 2 = strong and well documented

How to Interpret Your Score

This framework is not a valuation formula. It is a way to identify where your business might sit in the buyer's mind.

The goal is not to pretend everything is perfect. The goal is to find the few improvements that could move the multiple the most before you go to market.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Many founders start talking to buyers before the numbers, story, and process are ready. That usually weakens leverage.

A buyer's first impression matters. If your financials are messy, churn data is unclear, or the growth story is vague, the buyer may anchor on risk early. It is hard to recover from that.

The second mistake is hiding problems. Issues will surface in diligence. If you hide churn, customer disputes, payment failures, tax issues, security gaps, or revenue recognition problems, buyers will lose trust. Lost trust often turns into a lower price, tougher deal terms, or a failed process.

The third mistake is weak financial records. Billing and subscription companies should be able to show recurring revenue, one-time revenue, services revenue, gross margin by revenue type, churn, expansion, customer concentration, and monthly trends. If those numbers are not clean, buyers assume more risk.

The fourth mistake is not running a structured competitive process. Research on advised sale processes often shows that a well-run competitive process can lead to meaningfully higher purchase prices, commonly cited around 25%. The reason is simple: buyers behave differently when they know they are not alone.

The fifth mistake is revealing your target price too early. If you tell buyers you want USD 10m of enterprise value, many will come back at USD 10.1m or USD 10.2m. You have killed price discovery. A better process lets the market show you what the business is worth.

There are also two mistakes that are especially relevant in billing and subscription software.

First, do not underestimate data room preparation. Buyers will ask for billing cohorts, churn by customer type, payment failure rates, renewal history, implementation timelines, gross margin by product, and integration dependencies. If you cannot provide these quickly, confidence drops.

Second, do not overstate "platform" value. Many companies say they are a platform. Buyers will test whether that is true. If the product is really a set of custom workflows supported by people, the valuation will reflect that.

10. What Billing and Subscription Software Founders Can Do in 6-12 Months to Increase Valuation

You do not need to reinvent the company in 6-12 months. But you can improve how buyers see risk, quality, and upside.

Improve the Numbers

Start by cleaning up revenue categories. Separate recurring software revenue, usage-based revenue, implementation revenue, services revenue, and pass-through payments or third-party costs. Buyers need to see what revenue deserves a software multiple.

Track gross margin by revenue type. If implementation or support is dragging down blended margin, show that clearly and explain how it improves over time.

Build a simple monthly KPI pack. Include revenue growth, gross margin, churn, expansion, customer count, average contract value, customer concentration, and sales pipeline.

Strengthen Retention and Expansion

Buyers pay close attention to whether customers stick around. In billing software, churn should be low if the product is truly embedded.

Focus on renewals before the sale process. Resolve weak accounts, improve customer success coverage, and document expansion opportunities.

Show examples of customers that started with one billing use case and expanded into payments, tax, reporting, renewals, usage pricing, or more geographies. That is a powerful buyer narrative.

Make the Product Look More Scalable

Reduce custom work where possible. Package common workflows into productized modules. Create clear implementation playbooks.

If your onboarding process depends on a few key people, document it. Buyers want to know the company can scale without heroic effort.

Invest in integrations that matter. In this sector, stronger connectivity to payments, accounting, commerce, tax, and customer systems can directly improve strategic value.

Reduce Buyer Risk

Clean up contracts. Make sure assignment clauses, renewal terms, pricing, service commitments, and data rights are clear.

Document security, compliance, and payment controls. Billing platforms touch sensitive customer and financial data, so buyers will look closely.

Address customer concentration where possible. Even if you cannot fully fix it in 6-12 months, you can show a plan, pipeline, and evidence of diversification.

Build the Exit Story

A good exit story is not a pitch full of buzzwords. It is a clear explanation of why your company matters, why now is the right time, and why buyers can do more with the asset than you can alone.

Your story should answer:

- Why customers buy

- Why they stay

- Why they expand

- Why the market is growing

- Why the product is hard to replace

- Why a strategic buyer or private equity buyer can create more value

If you can support that story with clean data, your valuation conversation becomes much stronger.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can improve outcomes by expanding the buyer universe. Instead of relying only on obvious acquirers, AI can identify hundreds of qualified buyers based on deal history, strategic fit, financial capacity, product synergies, geography, and sector appetite. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes if one buyer drops out.

AI can also speed up the process. Buyer matching, outreach preparation, process materials, diligence support, and market mapping can happen much faster when technology supports the advisor. For many founders, that can mean initial conversations and offers in under 6 weeks, rather than waiting months for a manual-only process to build momentum.

The best model is not AI instead of expert advice. It is expert advisory enhanced by AI. Experienced M&A advisors still drive positioning, negotiation, buyer psychology, process tension, and judgment. AI helps them move faster, reach more buyers, prepare sharper materials, and support diligence more efficiently.

For billing and subscription software founders, that combination matters. The right advisor can frame your business as revenue infrastructure, not just software. They can present your metrics in the buyer's language, build a broader buyer universe, and run a professional process without traditional bulge bracket costs.

If you would like to understand how Eilla AI's AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.